Modelli per il Calcolo del Value at Risk

Modelli per il Calcolo del Value at Risk

Modelli per il Calcolo del Value at Risk

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

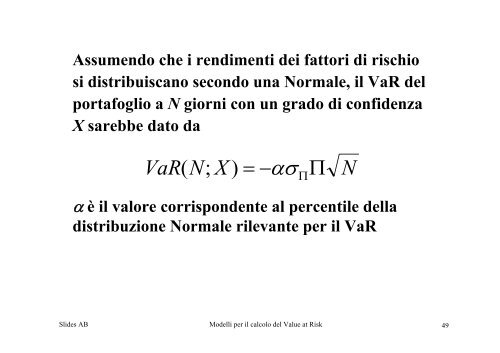

Assumendo che i rendimenti dei f<strong>at</strong>tori di rischio<br />

si distribuiscano secondo una Normale, <strong>il</strong> VaR <strong>del</strong><br />

portafoglio a N giorni con un grado di confidenza<br />

X sarebbe d<strong>at</strong>o da<br />

VaR( N;<br />

X ) = −ασ<br />

Π Π<br />

α è <strong>il</strong> valore corrispondente al <strong>per</strong>cent<strong>il</strong>e <strong>del</strong>la<br />

distribuzione Normale r<strong>il</strong>evante <strong>per</strong> <strong>il</strong> VaR<br />

Slides AB <strong>Mo<strong>del</strong>li</strong> <strong>per</strong> <strong>il</strong> calcolo <strong>del</strong> <strong>Value</strong> <strong>at</strong> <strong>Risk</strong><br />

N<br />

49