Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

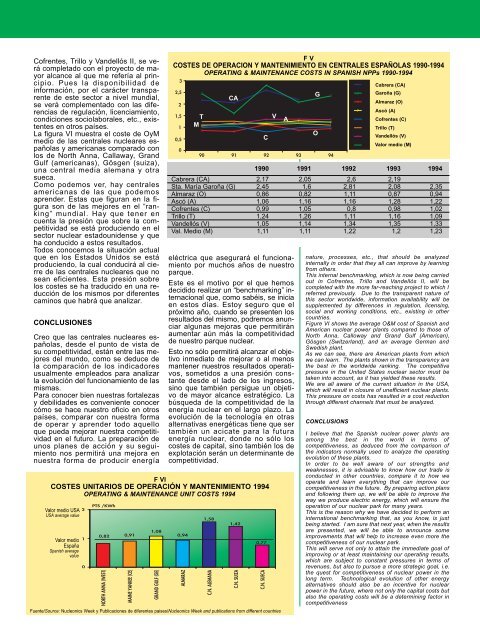

Cofrentes, Trillo y Vandellós II, se verácompletado con el proyecto de mayoralcance al que me refería al principio.Pues la disponibilidad deinformación, por el carácter transparentede este sector a nivel mundial,se verá complementado con las diferenciasde regulación, licenciamiento,condiciones sociolaborales, etc., existentesen otros países.La figura VI muestra el coste de OyMmedio de las centrales nucleares españolasy americanas comparado conlos de North Anna, Callaway, GrandGulf (americanas), Gösgen (suiza),una central media alemana y otrasueca.Como podemos ver, hay centralesamericanas de las que podemosaprender. Estas que figuran en la figurason de las mejores en el “ranking”mundial. Hay que tener encuenta la presión que sobre la competitividadse está produciendo en elsector nuclear estadounidense y queha conducido a estos resultados.Todos conocemos la situación actualque en los Estados Unidos se estáproduciendo, la cual conducirá al cierrede las centrales nucleares que nosean eficientes. Esta presión sobrelos costes se ha traducido en una reducciónde los mismos por diferentescaminos que habrá que analizar.CONCLUSIONESCreo que las centrales nucleares españolas,desde el punto de vista desu competitividad, están entre las mejoresdel mundo, como se deduce dela comparación de los indicadoresusualmente empleados para analizarla evolución del funcionamiento de lasmismas.Para conocer bien nuestras fortalezasy debilidades es conveniente conocercómo se hace nuestro oficio en otrospaíses, comparar con nuestra formade operar y aprender todo aquelloque pueda mejorar nuestra competitividaden el futuro. La preparación deunos planes de acción y su seguimientonos permitirá una mejora ennuestra forma de producir energía210PTS /KWh0,82 0,91NORTH ANNA (WEST)MAINE YANKEE (CE)1,08GRAND GULF (GE)1990 1991 1992 1993 1994Cabrera (CA) 2,17 2,05 2,6 2,19Sta. María Garoña (G) 2,45 1,6 2,81 2,08 2,35Almaraz (O) 0,86 0,82 1,11 0,87 0,94Ascó (A) 1,06 1,16 1,16 1,28 1,22Cofrentes (C) 0,99 1,05 0,8 0,98 1,02Trillo (T) 1,24 1,26 1,11 1,16 1,09Vandellós (V) 1,05 1,14 1,34 1,35 1,33Val. Medio (M) 1,11 1,11 1,22 1,2 1,23eléctrica que asegurará el funcionamientopor muchos años de nuestroparque.Este es el motivo por el que hemosdecidido realizar un “benchmarking” internacionalque, como sabéis, se iniciaen estos días. Estoy seguro que elpróximo año, cuando se presenten losresultados del mismo, podremos anunciaralgunas mejoras que permitiránaumentar aún más la competitividadde nuestro parque nuclear.Esto no sólo permitirá alcanzar el objetivoinmediato de mejorar o al menosmantener nuestros resultados operativos,sometidos a una presión constantedesde el lado de los ingresos,sino que también persigue un objetivode mayor alcance estratégico. Labúsqueda de la competitividad de laenergía nuclear en el largo plazo. Laevolución de la tecnología en otrasalternativas energéticas tiene que sertambién un acicate para la futuraenergía nuclear, donde no sólo loscostes de capital, sino también los deexplotación serán un determinante decompetitividad.F VICOSTES UNITARIOS DE OPERACIÓN Y MANTENIMIENTO 1994OPERATING & MAINTENANCE UNIT COSTS 1994Valor medio USAUSA average valueValor medioEspañaSpanish averagevalueFuente/Source: Nucleonics Week y Publicaciones de diferentes paises/Nucleonics Week and publications from different countriesF VCOSTES DE OPERACION Y MANTENIMIENTO EN <strong>CENTRALES</strong> ESPAÑOLAS 1990-1994OPERATING & MAINTENANCE COSTS IN SPANISH NPPs 1990-199432,521,510,500,94ALMARAZJBTM7FH1,58C.N. ALEMANACABJF7H1,42C.N. SUIZA0,77C.N. SUECAJBBJ7 7F7HFF HHC90 91 92 93 94VAGOJnature, processes, etc., that should be analyzedinternally in order that they all can improve by learningfrom others.This internal benchmarking, which is now being carriedout in Cofrentes, Trillo and Vandellós II, will becompleted with the more far-reaching project to which Ireferred previously. Due to the transparent nature ofthis sector worldwide, information availability will besupplemented by differences in regulation, licensing,social and working conditions, etc., existing in othercountries.Figure VI shows the average O&M cost of Spanish andAmerican nuclear power plants compared to those ofNorth Anna, Calloway and Grand Gulf (American),Gösgen (Switzerland), and an average German andSwedish plant.As we can see, there are American plants from whichwe can learn. The plants shown in the transparency arethe best in the worldwide ranking. The competitivepressure in the United States nuclear sector must betaken into account, as it has yielded these results.We are all aware of the current situation in the USA,which will result in closure of unefficient nuclear plants.This pressure on costs has resulted in a cost reductionthrough different channels that must be analyzed.CONCLUSIONSBJHF7Cabrera (CA)Garoña (G)Almaraz (O)Ascó (A)Cofrentes (C)Trillo (T)Vandellós (V)Valor medio (M)I believe that the Spanish nuclear power plants areamong the best in the world in terms ofcompetitiveness, as deduced from the comparison ofthe indicators normally used to analyze the operatingevolution of these plants.In order to be well aware of our strengths andweaknesses, it is advisable to know how our trade isconducted in other countries, compare it to how weoperate and learn everything that can improve ourcompetitiveness in the future. By preparing action plansand following them up, we will be able to improve theway we produce electric energy, which will ensure theoperation of our nuclear park for many years.This is the reason why we have decided to perform aninternational benchmarking that, as you know, is justbeing started. I am sure that next year, when the resultsare presented, we will be able to announce someimprovements that will help to increase even more thecompetitiveness of our nuclear park.This will serve not only to attain the immediate goal ofimproving or at least maintaining our operating results,which are subject to constant pressures in terms ofrevenues, but also to pursue a more strategic goal, i.e.the quest for competitiveness of nuclear power in thelong term. Technological evolution of other energyalternatives should also be an incentive for nuclearpower in the future, where not only the capital costs butalso the operating costs will be a determining factor incompetitiveness