Presentation to the analysts and investors - Lafarge

Presentation to the analysts and investors - Lafarge Presentation to the analysts and investors - Lafarge

72 Cement Internal Development Plan Our Revised Plan Correspond to 48 MT Capacity and 32 MT Additional Sales* Contributing to 750/850M€ EBITDA*, 12-15% ROCE in 2012 Additional sales - net (MT)* Additional sales (M€)* Additional EBITDA (M€)* ROCE* after tax on assets started up * New Capacity after replacement, Group share 2010 20 1,100 450 11% 2012 33 2,000 750 / 850 12-15%

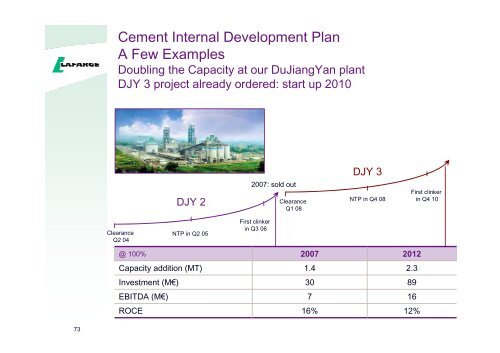

73 Cement Internal Development Plan A Few Examples Doubling the Capacity at our DuJiangYan plant DJY 3 project already ordered: start up 2010 Clearance Q2 04 @ 100% Capacity addition (MT) Investment (M€) EBITDA (M€) ROCE DJY 2 NTP in Q2 05 2007: sold out First clinker in Q3 06 Clearance Q1 08 2007 1.4 30 7 16% DJY 3 NTP in Q4 08 First clinker in Q4 10 2012 2.3 89 16 12%

- Page 21 and 22: 21 III - In What Conditions Could t

- Page 23 and 24: 23 Conclusion � Uncertainty is ca

- Page 25 and 26: 25 Orascom - A Major Step for Lafar

- Page 27 and 28: 27 Orascom - A Major Step for Lafar

- Page 29 and 30: 29 Synergies Have Been Implemented

- Page 31 and 32: 31 Synergies Have Been Implemented

- Page 33 and 34: 33 Solid Market Fundamentals 2008 M

- Page 35 and 36: New capacity management 35 4 MT of

- Page 37 and 38: 37 Managing Costs and Margins � I

- Page 39 and 40: 39 Managing Costs and Margins � U

- Page 41 and 42: 41 Aggregates & Concrete Opportunit

- Page 43 and 44: 43 Egypt ReadyMix Developing for th

- Page 45 and 46: Orascom A Major Step for Lafarge Fo

- Page 47 and 48: 47 Cement - Realizing New Potential

- Page 49 and 50: Leading Through Innovation in Ready

- Page 51 and 52: 51 The Rationale for Innovation in

- Page 53 and 54: 53 Boosting Innovation via TURBO

- Page 55 and 56: 55 Innovation Works in all Economic

- Page 57 and 58: 57 Continuous Deployment of Branded

- Page 59 and 60: 59 Pipeline is Also Full of New Pro

- Page 61 and 62: Capital Expenditures Jean Carlos AN

- Page 63 and 64: 63 Overview of Group’s 2009 Capex

- Page 65 and 66: 65 Cement Internal Development Plan

- Page 67 and 68: 67 Cement Internal Development Plan

- Page 69 and 70: 69 Cement Internal Development Plan

- Page 71: 71 Cement Internal Development Plan

- Page 75 and 76: 75 Cement Internal Development Plan

- Page 77 and 78: Cost Reduction Program Tom Farrell

- Page 79 and 80: 79 Lafarge Cost Reduction Program i

- Page 81 and 82: 81 Cost Reduction Target 2005 - 200

- Page 83 and 84: 83 The 2005 - 2008 Cost Reduction P

- Page 85 and 86: 85 Savings are Delivered Thanks to

- Page 87 and 88: 87 Cost Consciousness is Now Well E

- Page 89 and 90: 89 These Further Savings are Made P

- Page 91 and 92: 91 Priorities are Being Converted i

- Page 93 and 94: 93 Cement Division will Contribute

- Page 95 and 96: 95 Solid Fuel Optimization: Ashaka

- Page 97 and 98: 97 Reduce Electricity Bill: Sonadih

- Page 99 and 100: 99 Reduce Fixed Costs and SG&A: A P

- Page 101 and 102: 101 Gypsum Division will Generate

- Page 103 and 104: Cost Reduction Program: Aggregates

- Page 105 and 106: 105 1 A Comprehensive ROCK Operatin

- Page 107 and 108: 107 1 ROCK Operating Model Example

- Page 109 and 110: 109 2 Capacity Optimization Example

- Page 111 and 112: 111 2 Capacity Optimization � Rig

- Page 113 and 114: 113 3 Logistics Improvement Quick W

- Page 115 and 116: Credit: Rudy Ricciotti (Architect)

73<br />

Cement Internal Development Plan<br />

A Few Examples<br />

Doubling <strong>the</strong> Capacity at our DuJiangYan plant<br />

DJY 3 project already ordered: start up 2010<br />

Clearance<br />

Q2 04<br />

@ 100%<br />

Capacity addition (MT)<br />

Investment (M€)<br />

EBITDA (M€)<br />

ROCE<br />

DJY 2<br />

NTP in Q2 05<br />

2007: sold out<br />

First clinker<br />

in Q3 06<br />

Clearance<br />

Q1 08<br />

2007<br />

1.4<br />

30<br />

7<br />

16%<br />

DJY 3<br />

NTP in Q4 08<br />

First clinker<br />

in Q4 10<br />

2012<br />

2.3<br />

89<br />

16<br />

12%