growers@sgcotton.com.au Roger Tomkins - Greenmount Press

growers@sgcotton.com.au Roger Tomkins - Greenmount Press

growers@sgcotton.com.au Roger Tomkins - Greenmount Press

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

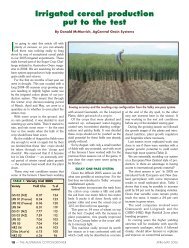

THE period since the end of May (when last we <strong>com</strong>mented<br />

in these pages) has been characterised by a degree of<br />

stability in world cotton prices – following the sharp<br />

downturn that we described in our last contribution. The<br />

international market (as measured by the Cotlook A Index) lost<br />

over 18 per cent of its value during the month of May. For most<br />

of the period since then, prices have remained within a trading<br />

range in the low to mid 80s, rather more familiar territory than<br />

that explored over the past couple of years. The Cotlook A Index<br />

dipped below the 80-cent level for just a single day – the value<br />

(77.65) recorded on June 6, proved to be the lowest of the<br />

2011–12 (August–July) season. The high point of the season had<br />

been reached as early as last September.<br />

The wel<strong>com</strong>e stability prompted a gradual return of mill<br />

buying confidence during the course of July and, by the end of<br />

the month a broad range of import markets was daily enquiring<br />

for raw cotton to fill their short-term requirements. But demand<br />

remained almost exclusively of a hand-to-mouth nature. The<br />

market volatility of the past couple of years continues to cast a<br />

long shadow, and has instilled an aversion to risk that is evident in<br />

the behaviour both of mill buyers and international trade sellers.<br />

A glance at the prevailing world supply and demand<br />

fundamentals would also tend to argue in favour of a patient<br />

Specialists in the<br />

Sale and Valuation<br />

of Rural Properties<br />

• Rural Properties • Cargill Cotton Agents<br />

• Town Sales • Registered Valuers<br />

• Property Management • Auctions<br />

• Clearing Sales<br />

MOREE REAL ESTATE<br />

www.moreerealestate.<strong>com</strong>.<strong>au</strong><br />

Phone: 02 7651 1100<br />

Fax: 02 6751 1766<br />

After Hours:<br />

P<strong>au</strong>l Kelly 0428 281 428<br />

Cliff Brown 02 6752 3970<br />

Allan Gobbert 0428 523 375<br />

marketing<br />

The World Cotton Market<br />

■ By Michael Edwards, Cotton Outlook<br />

FIGuRE 1: Cootlook A Index since January 2012<br />

raw cotton purchasing policy. At the end of July, Cotton<br />

Outlook’s estimates continued to show a surplus of supply over<br />

demand during 2011–12 in excess of five million tonnes – an<br />

unprecedented addition to world stocks – and a further increase,<br />

of more than 1,700,000 tonnes, is forecast for 2012–13.<br />

But the location and ownership of this apparently d<strong>au</strong>nting<br />

surplus supply repays some scrutiny. As has been well<br />

Cargill’s Cotton Division –<br />

Buying cotton bales<br />

direct from the grower<br />

Phil Sloan<br />

PO Box 1203<br />

GOONDIWINDI Qld 4390<br />

Ph: (07) 4671 0222<br />

Fax: (07) 4671 3833<br />

AGENTS:<br />

Pete Johnson<br />

Left Field Solutions<br />

Mob: 0409 893 139<br />

P<strong>au</strong>l Kelly<br />

Moree Real Estate<br />

MOREE<br />

Ph: (02) 6751 1100<br />

David Dugan<br />

TRANGIE<br />

Ph: (02) 6888 7122<br />

<strong>Roger</strong> McCumstie<br />

BRISBANE<br />

Ph: (07) 3367 2629<br />

cotton_<strong>au</strong>st@cargill.<strong>com</strong><br />

www.cargill.<strong>com</strong>.<strong>au</strong><br />

36 — The Australian Cottongrower August–September 2012