FPT 2010-2014 Plan - FIAT Industrial

FPT 2010-2014 Plan - FIAT Industrial FPT 2010-2014 Plan - FIAT Industrial

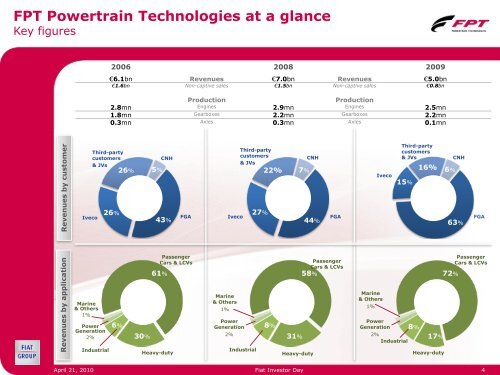

FPT Powertrain Technologies at a glance Key figures Revenues by application Revenues by customer Third-party customers & JVs Iveco Marine & Others 1% Power Generation 2% Industrial 2006 2008 2009 €6.1bn Revenues €7.0bn Revenues €5.0bn €1.6bn Non-captive sales €1.5bn Non-captive sales €0.8bn Production Production 2.8mn Engines 2.9mn Engines 2.5mn 1.8mn Gearboxes 2.2mn Gearboxes 2.2mn 0.3mn Axles 0.3mn Axles 0.1mn 26% CNH 26% 5% 22% 6% 30% 43% Heavy-duty FGA Passenger Cars & LCVs 61% Iveco Marine & Others 1% Power Generation 2% Third-party customers & JVs Industrial 27% 8% April 21, 2010 Fiat Investor Day 4 31% 7% CNH 44% Heavy-duty FGA Passenger Cars & LCVs 58% Marine & Others 1% Iveco Third-party customers & JVs 15% Power Generation 8% 2% Industrial 16% 17% Heavy-duty 6% CNH 63% 72% FGA Passenger Cars & LCVs

Passenger & Commercial Vehicles Major achievements during last 4 years � New technologies transferred to production • Gasoline: MultiAir & TwinAir • Diesel: MultiJet II • Transmissions: Dual Dry Clutch Technology � New product launches • Gasoline: Fire T-jet, 1.8 Turbo GDI, E-torQ • Diesel: 1.9 Twin turbo, 1.6 Midsize diesel engine • Transmissions: new Manual 6 speed C635 � International expansion • Supported FGA in India & China • Exploited BCC opportunities leveraging on local JVs ...but... Development of non-captive sales down, mainly due to reduced GM activity (-75%) April 21, 2010 Fiat Investor Day 5

- Page 1 and 2: April 21, 2010 FPT Powertrain Techn

- Page 3: FPT Powertrain Technologies Perform

- Page 7 and 8: Passenger & Commercial Vehicles Lev

- Page 9 and 10: Passenger & Commercial Vehicles Hyb

- Page 11 and 12: Passenger & Commercial Vehicles Die

- Page 13 and 14: Passenger & Commercial Vehicles Thi

- Page 15 and 16: Industrial & Marine Major achieveme

- Page 17 and 18: Industrial & Marine FPT SCR technol

- Page 19 and 20: Industrial & Marine Engine portfoli

- Page 21 and 22: Industrial & Marine Development of

- Page 23 and 24: Industrial & Marine Optimization of

- Page 25 and 26: FPT Powertrain Technologies Improve

- Page 27 and 28: 2010-14 Financial targets Nearly br

<strong>FPT</strong> Powertrain Technologies at a glance<br />

Key figures<br />

Revenues by application<br />

Revenues by customer<br />

Third-party<br />

customers<br />

& JVs<br />

Iveco<br />

Marine<br />

& Others<br />

1%<br />

Power<br />

Generation<br />

2%<br />

<strong>Industrial</strong><br />

2006 2008 2009<br />

€6.1bn Revenues €7.0bn Revenues €5.0bn<br />

€1.6bn Non-captive sales €1.5bn Non-captive sales €0.8bn<br />

Production Production<br />

2.8mn Engines 2.9mn Engines 2.5mn<br />

1.8mn Gearboxes 2.2mn Gearboxes 2.2mn<br />

0.3mn Axles 0.3mn Axles 0.1mn<br />

26%<br />

CNH<br />

26% 5%<br />

22%<br />

6%<br />

30%<br />

43%<br />

Heavy-duty<br />

FGA<br />

Passenger<br />

Cars & LCVs<br />

61%<br />

Iveco<br />

Marine<br />

& Others<br />

1%<br />

Power<br />

Generation<br />

2%<br />

Third-party<br />

customers<br />

& JVs<br />

<strong>Industrial</strong><br />

27%<br />

8%<br />

April 21, <strong>2010</strong> Fiat Investor Day 4<br />

31%<br />

7%<br />

CNH<br />

44%<br />

Heavy-duty<br />

FGA<br />

Passenger<br />

Cars & LCVs<br />

58%<br />

Marine<br />

& Others<br />

1%<br />

Iveco<br />

Third-party<br />

customers<br />

& JVs<br />

15%<br />

Power<br />

Generation 8%<br />

2%<br />

<strong>Industrial</strong><br />

16%<br />

17%<br />

Heavy-duty<br />

6%<br />

CNH<br />

63%<br />

72%<br />

FGA<br />

Passenger<br />

Cars & LCVs