Module 4 - Introduction to Performance Audit_4B

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

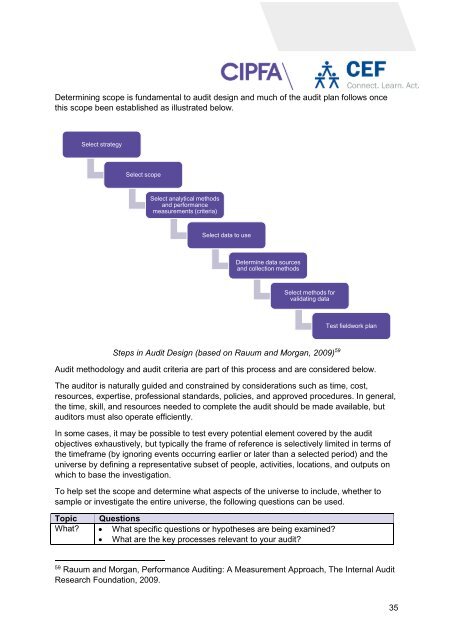

Determining scope is fundamental <strong>to</strong> audit design and much of the audit plan follows once<br />

this scope been established as illustrated below.<br />

Select strategy<br />

Select scope<br />

Select analytical methods<br />

and performance<br />

measurements (criteria)<br />

Select data <strong>to</strong> use<br />

Determine data sources<br />

and collection methods<br />

Select methods for<br />

validating data<br />

Test fieldwork plan<br />

Steps in <strong>Audit</strong> Design (based on Rauum and Morgan, 2009) 59<br />

<strong>Audit</strong> methodology and audit criteria are part of this process and are considered below.<br />

The audi<strong>to</strong>r is naturally guided and constrained by considerations such as time, cost,<br />

resources, expertise, professional standards, policies, and approved procedures. In general,<br />

the time, skill, and resources needed <strong>to</strong> complete the audit should be made available, but<br />

audi<strong>to</strong>rs must also operate efficiently.<br />

In some cases, it may be possible <strong>to</strong> test every potential element covered by the audit<br />

objectives exhaustively, but typically the frame of reference is selectively limited in terms of<br />

the timeframe (by ignoring events occurring earlier or later than a selected period) and the<br />

universe by defining a representative subset of people, activities, locations, and outputs on<br />

which <strong>to</strong> base the investigation.<br />

To help set the scope and determine what aspects of the universe <strong>to</strong> include, whether <strong>to</strong><br />

sample or investigate the entire universe, the following questions can be used.<br />

Topic Questions<br />

What? What specific questions or hypotheses are being examined?<br />

What are the key processes relevant <strong>to</strong> your audit?<br />

59<br />

Rauum and Morgan, <strong>Performance</strong> <strong>Audit</strong>ing: A Measurement Approach, The Internal <strong>Audit</strong><br />

Research Foundation, 2009.<br />

35