TIAPS Module 1 Audit and Assurance workbook

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

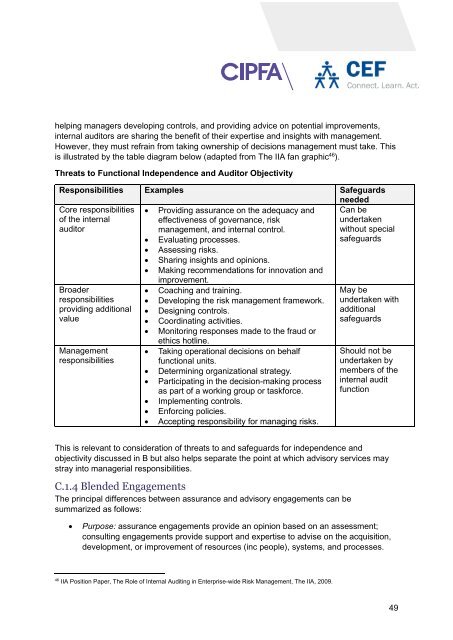

helping managers developing controls, <strong>and</strong> providing advice on potential improvements,<br />

internal auditors are sharing the benefit of their expertise <strong>and</strong> insights with management.<br />

However, they must refrain from taking ownership of decisions management must take. This<br />

is illustrated by the table diagram below (adapted from The IIA fan graphic 46 ).<br />

Threats to Functional Independence <strong>and</strong> <strong>Audit</strong>or Objectivity<br />

Responsibilities Examples Safeguards<br />

needed<br />

Core responsibilities<br />

of the internal<br />

auditor<br />

Broader<br />

responsibilities<br />

providing additional<br />

value<br />

Management<br />

responsibilities<br />

• Providing assurance on the adequacy <strong>and</strong><br />

effectiveness of governance, risk<br />

management, <strong>and</strong> internal control.<br />

• Evaluating processes.<br />

• Assessing risks.<br />

• Sharing insights <strong>and</strong> opinions.<br />

• Making recommendations for innovation <strong>and</strong><br />

improvement.<br />

• Coaching <strong>and</strong> training.<br />

• Developing the risk management framework.<br />

• Designing controls.<br />

• Coordinating activities.<br />

• Monitoring responses made to the fraud or<br />

ethics hotline.<br />

• Taking operational decisions on behalf<br />

functional units.<br />

• Determining organizational strategy.<br />

• Participating in the decision-making process<br />

as part of a working group or taskforce.<br />

• Implementing controls.<br />

• Enforcing policies.<br />

• Accepting responsibility for managing risks.<br />

Can be<br />

undertaken<br />

without special<br />

safeguards<br />

May be<br />

undertaken with<br />

additional<br />

safeguards<br />

Should not be<br />

undertaken by<br />

members of the<br />

internal audit<br />

function<br />

This is relevant to consideration of threats to <strong>and</strong> safeguards for independence <strong>and</strong><br />

objectivity discussed in B but also helps separate the point at which advisory services may<br />

stray into managerial responsibilities.<br />

C.1.4 Blended Engagements<br />

The principal differences between assurance <strong>and</strong> advisory engagements can be<br />

summarized as follows:<br />

• Purpose: assurance engagements provide an opinion based on an assessment;<br />

consulting engagements provide support <strong>and</strong> expertise to advise on the acquisition,<br />

development, or improvement of resources (inc people), systems, <strong>and</strong> processes.<br />

46<br />

IIA Position Paper, The Role of Internal <strong>Audit</strong>ing in Enterprise-wide Risk Management, The IIA, 2009.<br />

49