TIAPS Module 1 Audit and Assurance workbook

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

A.3 Governance Models<br />

When evaluating governance, internal auditors must consider whether the organization has<br />

used “adequate criteria” for monitoring purposes.<br />

If adequate, internal auditors must use such criteria in their evaluation. If inadequate, internal<br />

auditors must identify appropriate evaluation criteria through discussion with management<br />

<strong>and</strong>/or the board.<br />

Types of criteria may include:<br />

• Internal (e.g., policies <strong>and</strong> procedures of the organization).<br />

• External (e.g., laws <strong>and</strong> regulations imposed by statutory bodies).<br />

• Leading practices (e.g., industry <strong>and</strong> professional guidance). 9<br />

To explore governance further we will consider four important models that may be said to<br />

represent “leading practices,” although they must always be contextualized:<br />

• ISO 37000:2021 Governance of organizations – Guidance.<br />

• IIA Three Lines Model.<br />

• CIPFA International Framework: Good Governance in the Public Sector.<br />

• King IV Corporate Governance Report, 2016.<br />

These models have many similarities. Corporate governance codes such as the King IV<br />

Code, while being applicable primarily to private sector companies, are also very informative<br />

for government entities.<br />

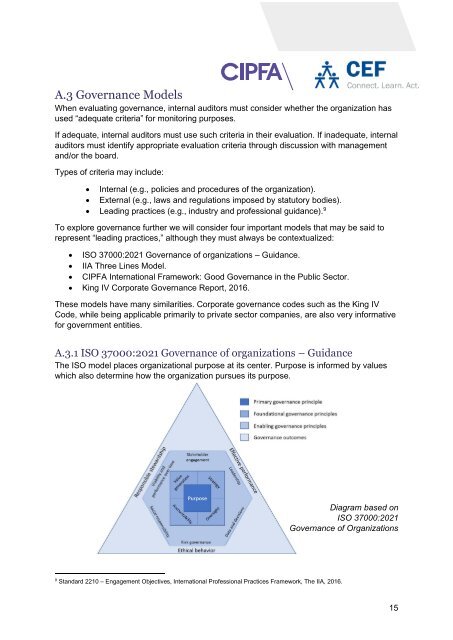

A.3.1 ISO 37000:2021 Governance of organizations – Guidance<br />

The ISO model places organizational purpose at its center. Purpose is informed by values<br />

which also determine how the organization pursues its purpose.<br />

Diagram based on<br />

ISO 37000:2021<br />

Governance of Organizations<br />

9<br />

St<strong>and</strong>ard 2210 – Engagement Objectives, International Professional Practices Framework, The IIA, 2016.<br />

15