PDF, 3.2 MB - Pfleiderer AG

PDF, 3.2 MB - Pfleiderer AG

PDF, 3.2 MB - Pfleiderer AG

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

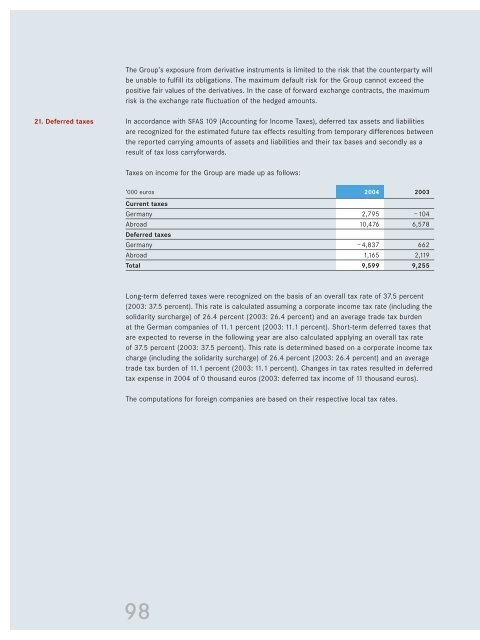

21. Deferred taxes<br />

The Group’s exposure from derivative instruments is limited to the risk that the counterparty will<br />

be unable to fulfill its obligations. The maximum default risk for the Group cannot exceed the<br />

positive fair values of the derivatives. In the case of forward exchange contracts, the maximum<br />

risk is the exchange rate fluctuation of the hedged amounts.<br />

In accordance with SFAS 109 (Accounting for Income Taxes), deferred tax assets and liabilities<br />

are recognized for the estimated future tax effects resulting from temporary differences between<br />

the reported carrying amounts of assets and liabilities and their tax bases and secondly as a<br />

result of tax loss carryforwards.<br />

Taxes on income for the Group are made up as follows:<br />

‘000 euros<br />

Current taxes<br />

2004 2003<br />

Germany 2,795 –104<br />

Abroad<br />

Deferred taxes<br />

10,476 6,578<br />

Germany –4,837 662<br />

Abroad 1,165 2,119<br />

Total 9,599 9,255<br />

Long-term deferred taxes were recognized on the basis of an overall tax rate of 37.5 percent<br />

(2003: 37.5 percent). This rate is calculated assuming a corporate income tax rate (including the<br />

solidarity surcharge) of 26.4 percent (2003: 26.4 percent) and an average trade tax burden<br />

at the German companies of 11.1 percent (2003: 11.1 percent). Short-term deferred taxes that<br />

are expected to reverse in the following year are also calculated applying an overall tax rate<br />

of 37.5 percent (2003: 37.5 percent). This rate is determined based on a corporate income tax<br />

charge (including the solidarity surcharge) of 26.4 percent (2003: 26.4 percent) and an average<br />

trade tax burden of 11.1 percent (2003: 11.1 percent). Changes in tax rates resulted in deferred<br />

tax expense in 2004 of 0 thousand euros (2003: deferred tax income of 11 thousand euros).<br />

The computations for foreign companies are based on their respective local tax rates.<br />

98