Marketing and innovation

New opportunities hit global investors' radar screens Global Investor, 02/2005 Credit Suisse

New opportunities hit global investors' radar screens

Global Investor, 02/2005

Credit Suisse

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

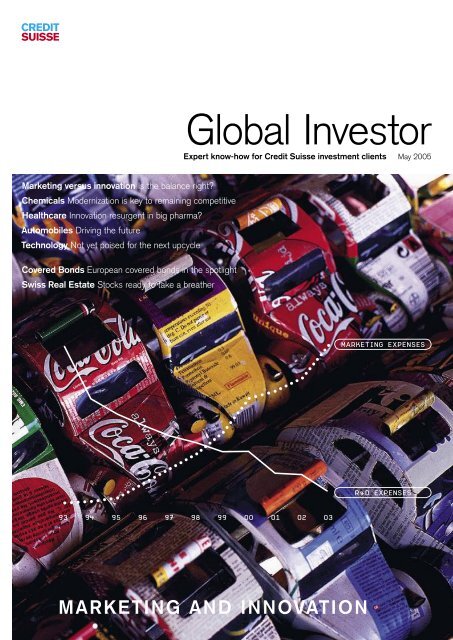

Global Investor<br />

Expert know-how for Credit Suisse investment clients May 2005<br />

<strong>Marketing</strong> versus <strong>innovation</strong> Is the balance right?<br />

Chemicals Modernization is key to remaining competitive<br />

Healthcare Innovation resurgent in big pharma?<br />

Automobiles Driving the future<br />

Technology Not yet poised for the next upcycle<br />

Covered Bonds European covered bonds in the spotlight<br />

Swiss Real Estate Stocks ready to take a breather<br />

MARKETING EXPENSES<br />

R&D EXPENSES<br />

93 94 95 96 97 98 99 00 01 02 03<br />

MARKETING AND INNOVATION

GLOBAL INVESTOR 2.05 Editorial—3<br />

Long-term investing as volatility rises<br />

With volatile <strong>and</strong> often downward movements across many of<br />

the world’s financial markets, investors have tended to seek risk<br />

reduction <strong>and</strong> capital preservation strategies, <strong>and</strong> our shorterterm<br />

research has focused on this. But we believe that now is<br />

also a good moment to look at much longer-term issues, so that<br />

investors can start to identify opportunities that may emerge<br />

once the current phase of volatility settles down. Accordingly,<br />

much of this issue of Global Investor is devoted to a big-picture<br />

analysis of the balance between marketing <strong>and</strong> <strong>innovation</strong> in<br />

major industries. We argue that an overemphasis on marketing<br />

at the expense of genuine <strong>innovation</strong> has contributed to<br />

underperformance in recent years of global sectors such as<br />

automobiles <strong>and</strong> pharmaceuticals, <strong>and</strong> stunted the growth<br />

prospects of consumer electronics companies. Looking forward,<br />

we suggest that the big pharma companies may be on the<br />

brink of rectifying this imbalance, potentially opening exciting<br />

opportunities for investors. By contrast, most major automobile<br />

manufacturers seem stuck in their old ways. Separately, we<br />

look at Europe-wide covered bonds, <strong>and</strong> Swiss real estate<br />

assets, as possibly attractive diversification amid an uncertain<br />

market environment for bonds. Here, we conclude that the<br />

underlying collateralization of covered bonds does indeed make<br />

them interesting, while for Swiss real estate assets, investors<br />

should wait for valuations to become less rich.<br />

As usual, the medium-term analysis in the Global Investor will<br />

be complemented by our shorter-term research, which will<br />

advise in detail on the timing <strong>and</strong> the vehicles for implementing<br />

the bigger themes discussed here. And as with all our<br />

publications, we welcome your comments <strong>and</strong> feedback –<br />

good or bad.<br />

Giles Keating, Head of Global Research

GLOBAL INVESTOR 2.05 Contents—4<br />

Themes<br />

<strong>Marketing</strong> versus <strong>innovation</strong><br />

Is the balance right? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5<br />

Chemicals<br />

The European chemicals industry: Innovation is the key<br />

to remaining competitive . . . . . . . . . . . . . . . . . . . . . . . . . . . 12<br />

Healthcare<br />

Will <strong>innovation</strong> regain the upper h<strong>and</strong> over marketing<br />

in pharma? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17<br />

Automobiles<br />

Driving the future . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24<br />

Technology<br />

Technology not yet poised for the next upcycle . . . . . . . . . . . . 31<br />

Topics<br />

Covered Bonds<br />

European covered bonds in the spotlight . . . . . . . . . . . . . . . . 39<br />

Real Estate<br />

Swiss real estate stocks ready to take a breather . . . . . . . . . . 42<br />

Services<br />

Credit Suisse publication l<strong>and</strong>scape . . . . . . . . . . . . . . . . . . . 46<br />

Author index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48<br />

Imprint . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Mass <strong>Marketing</strong><br />

GLOBAL INVESTOR 2.05 <strong>Marketing</strong> versus <strong>innovation</strong>—5

Limited Innovation?<br />

Mass-marketed br<strong>and</strong>s have guaranteed quality <strong>and</strong> consistency to consumers since the nineteenth century,<br />

but do they make companies complacent about <strong>innovation</strong>?

GLOBAL INVESTOR 2.05 <strong>Marketing</strong> versus <strong>innovation</strong>—7<br />

<strong>Marketing</strong> versus <strong>innovation</strong>: Is the balance right?<br />

<strong>Marketing</strong> <strong>and</strong> <strong>innovation</strong> have been two inseparable parts of capitalist success<br />

since the earliest days of the industrial revolution. Craftsman Thomas Chippendale<br />

published his Furniture Catalogue in 1754. Giles Keating<br />

Mr. Chippendale’s fine products, previously sold only in small<br />

quantities, were transformed into the ultimate interior design<br />

feature for the English middle class, <strong>and</strong> he became a wealthy<br />

man. The following century, international br<strong>and</strong>s such as Lipton’s<br />

Tea <strong>and</strong> then Coca-Cola emerged, offering consumers the guarantee<br />

of a product with consistent taste <strong>and</strong> quality, <strong>and</strong> making<br />

fortunes for their owners.<br />

Initially, marketing <strong>and</strong> br<strong>and</strong>ing were about taking a product<br />

that had already been invented <strong>and</strong> making sure that it sold. Gradually,<br />

many successful companies introduced feedback in the<br />

other direction, giving marketing people a say in the way that<br />

products were developed, aiming to leverage their br<strong>and</strong>s <strong>and</strong><br />

increasing the chances of commercial success for new products.<br />

This process gathered momentum in the later decades of the<br />

twentieth century as marketing <strong>and</strong> pricing strategies became<br />

increasingly refined, bringing benefits to both companies <strong>and</strong> their<br />

customers. But arguably, it has now gone too far for the good of<br />

either, with marketing now dominating R&D in many firms. In<br />

some major pharmaceutical companies, the heads of each of the<br />

main br<strong>and</strong> lines are now paid multiples of what is earned by the<br />

research chief. And across many of the sectors covered in this<br />

edition of Global Investor, the budget for marketing far exceeds<br />

that for R&D.<br />

This dominance of marketing over R&D is very often associated<br />

with a reliance on ever more incremental product improvement,<br />

rather than the development of truly life-altering <strong>innovation</strong>s. In<br />

the short-term, this is a nice safe <strong>and</strong> easy strategy for managements,<br />

since instead of the risk of costly development of unknown<br />

novelties, it leverages existing br<strong>and</strong>s, taps into apparently loyal<br />

consumer groups, <strong>and</strong> may allow new look-alike patents to replace<br />

old ones that are expiring. The sense of comfort is enhanced when<br />

all the major incumbent companies in a sector are doing much the<br />

same. However, in the medium to long term, this kind of strategy<br />

can be a recipe for disaster, as utterly unexpected competitors<br />

appear with genuinely new <strong>innovation</strong>s that sweep the market.<br />

The classic case is the rise of the low-cost airlines, which has left<br />

Southwest Airlines with a higher market capitalization than the<br />

three traditional carriers combined.<br />

Another obvious example is in the consumer electronics sector,<br />

where Sony’s focus on incremental improvements to its<br />

famous Walkman (allowing, for example, ever-larger jolts without<br />

upsetting the music flow) has left it gasping in the face of the

assault from the iPod produced by Apple – a company that previously<br />

had not been a direct competitor to Sony at all. The iPod’s<br />

ability to play <strong>and</strong> organize large amounts of downloaded music<br />

makes it utterly different from the Walkman. This followed a similar<br />

incident some two years earlier where Sony’s emphasis on its<br />

Trinitron TV technology left it far behind in the development of<br />

flat-screen TVs, where South Korea’s Samsung has raced ahead.<br />

For Sony, there seems to be a pattern of over-reliance on a<br />

powerful br<strong>and</strong>, backed up by merely incremental <strong>innovation</strong>. This<br />

is especially striking since Sony had itself, half a century before,<br />

emerged from nowhere on the back of radical product <strong>innovation</strong>.<br />

In the automobile sector, the annual reports of the major<br />

companies suggest large expenditure on <strong>innovation</strong>, which is<br />

apparently much more than is spent on marketing (where data<br />

are available). But it is an open question whether this <strong>innovation</strong><br />

really offers genuinely new responses to consumer needs, or<br />

whether it is over-reliant on a marketing-dominated strategy that<br />

leverages off consumers’ desire to keep up with the latest models<br />

in a strong br<strong>and</strong>. DaimlerChrysler’s recent problems with reliability,<br />

largely caused by the unnecessary electronics packed into<br />

its latest automobiles, provide a stark reminder that the core<br />

business model of the US <strong>and</strong> European manufacturers over the<br />

last two decades has been to add extra gizmos into their cars to<br />

persuade people to upgrade. While driving their business down<br />

this route, they have failed to come up with far more fundamental<br />

<strong>innovation</strong>s under the hood. No one has produced a viable massmarket<br />

fuel-cell-powered automobile or electric car, suggesting<br />

that more than two decades of research has been underfunded<br />

<strong>and</strong> under-focused by the major companies. Instead, they offer<br />

an ever-increasing number of voice options on sat-nav systems<br />

<strong>and</strong> yet larger number of pre-set memories for electric seats. The<br />

prospect of sustained high oil prices may eventually cause the<br />

management at the major US <strong>and</strong> European carmakers to inject<br />

badly needed urgency into this research. But meanwhile, successful<br />

genuine <strong>innovation</strong> in fuel systems has been realized by<br />

other companies. In Japan, Toyota has achieved world-beating<br />

success with its petrol-electric hybrid car (the Prius), which has<br />

caught the imagination of consumers. And Valeo, a medium-sized<br />

component manufacturer, has developed a system that substantially<br />

boosts urban fuel efficiency through the simple expedient of<br />

shutting off the engine at red traffic lights <strong>and</strong> re-starting automatically<br />

when the driver hits the gas.<br />

The next big competitive threat could well come from ultra-cheap<br />

urban cars, costing perhaps only two or three thous<strong>and</strong> euros or<br />

dollars, lightweight <strong>and</strong> with unnecessary gizmos stripped out.<br />

Companies such as Shanghai Motor Corporation, or Tata Motors<br />

in India, are well positioned to produce these automobiles. So are<br />

the Japanese companies contributing to the one-person transport<br />

in use at this year‘s World Expo in Aichi, Japan. This kind of product<br />

would strike at the heart of the marketing strategy of the<br />

major US <strong>and</strong> European carmakers, which have focused for decades<br />

on pushing customers up-market to maintain sales values<br />

in the face of falling production costs.<br />

And in the pharmaceuticals sector, the biggest companies<br />

have focused heavily on marketing. Large sales teams targeted<br />

at health professionals, <strong>and</strong> ad campaigns aimed at the general<br />

public, have pushed marketing budgets up to more than double<br />

R&D budgets. And a major part of the research budgets has<br />

generated products designed to cope with patent expiry by, for<br />

example, offering weekly doses of a drug that previously had to<br />

be taken daily. Very useful for the patients involved – <strong>and</strong> very<br />

profitable in the short to medium term – but for the long-term<br />

health of both companies <strong>and</strong> their customers, this kind of<br />

incremental <strong>innovation</strong> is hardly in the same class as inventing<br />

drugs that really address currently incurable diseases such as<br />

Alzheimer’s.<br />

With researchers playing second fiddle to marketing people<br />

in the corporate culture, <strong>and</strong> often much less well paid, it is unsurprising<br />

that many of the best <strong>and</strong> brightest research scientists<br />

have quit big pharma companies to go work in biotech companies<br />

where they can participate in the upside of their work. Unsurprisingly,<br />

a broad index of biotech shares, although volatile, has<br />

substantially outperformed the largest pharma stocks over the<br />

last decade. And a new competitive threat is now appearing, with<br />

India moving toward international patent law, <strong>and</strong> large Indian<br />

generics companies, such as Ranbaxy, starting to develop the<br />

capability to produce their own original drugs.<br />

If there is good news in the big pharma sector, it is that the<br />

situation has become so bad, that finally a constructive reaction<br />

may be starting to emerge. The takeover by Novartis of the generics<br />

producers Hexal <strong>and</strong> Eon Labs may yet turn out to have<br />

significance beyond mere business-line diversification, if it allows<br />

the combined company to focus on offering its own generic<br />

response to patent expiry, rather than researching <strong>and</strong> marketing

GLOBAL INVESTOR 2.05 <strong>Marketing</strong> versus <strong>innovation</strong>—9<br />

Three steps on the path of evolution of the Walkman …<br />

Sony created <strong>and</strong> dominated the mass mobile music market with the Walkman, then lapsed into low-<strong>innovation</strong><br />

complacency <strong>and</strong> lost out to Apple‘s iPod.

follow-on patentable drugs that differ only marginally from those<br />

expiring. This should then free up research resources for genuine<br />

<strong>innovation</strong>. And in another potentially very positive development,<br />

GSK recently signaled that it is prepared to make a substantial<br />

cut in its marketing budget, with the money to be re-directed to<br />

research, provided its major competitor Pfizer takes the lead. This<br />

move (still uncertain at the time of publication) would represent an<br />

end to the marketing “arms race.” Investors should reap the peace<br />

dividend.<br />

The message from these <strong>and</strong> other sectors, is that the progressive<br />

takeover by marketing seen over the last few decades is<br />

either already reversing, or is set to do so soon. In our view, this<br />

can only be good for companies, investors <strong>and</strong> customers, not<br />

because we think marketing is somehow bad, but because we<br />

perceive there is an optimum mixture between marketing <strong>and</strong><br />

research within a company, both in terms of money spent <strong>and</strong> in<br />

terms of corporate power. Moreover, we believe that the pendulum<br />

has swung too far away from research. The companies that move<br />

fastest to bring it back to a better balance will outperform; those<br />

that lag will underperform. In this issue of Global Investor we<br />

provide more detailed analysis on this, <strong>and</strong> in further publications<br />

over the next few months, we will bring detailed investment<br />

recommendations based on these concepts.<br />

Furthermore, this re-balancing toward R&D, with more genuine<br />

<strong>innovation</strong> <strong>and</strong> less marketing-led incremental product development,<br />

could have broader economic <strong>and</strong> political ramifications. One<br />

of the big debates among economists at the moment focuses on<br />

why people say they are no happier today than they were 40 years<br />

ago, despite the fact that real per capita gross domestic product<br />

has doubled over that period (see chart on page 11, derived from<br />

data cited in a new book titled “Happiness: Lessons from a new<br />

science,” by Professor Richard Layard). Among the various likely<br />

explanations for this, there is much focus on the notion that much<br />

of consumer spending is focused on one-upmanship, i.e., simply<br />

trying to be better than the person next door. This is, of course,<br />

a zero-sum game: If I buy a bigger car purely to get ahead of my<br />

neighbor, then I feel better, but as soon as he or she follows suit,<br />

we are both back where we started in terms of happiness, although<br />

GDP has gone up. By contrast, if we both buy a genuinely new<br />

product that enables us to do something that was impossible<br />

before, or makes us both healthier, than we are both better off.<br />

The increasing emphasis given to marketing by major companies<br />

in the last four decades, with the accompanying tendency<br />

to make marginal product improvements rather than to seek out<br />

quantum leaps, tends to prey off people’s natural inclination<br />

toward one-upmanship. If within companies there is now a return<br />

to focus on genuine <strong>innovation</strong>, there should be an accompanying<br />

upswing in happiness. That would be a worthwhile change in itself,<br />

representing a major shift in society, <strong>and</strong> it might be accompanied<br />

by a new dynamism in people’s economic attitudes, which (together<br />

with a re-engagement with politics) is most especially needed<br />

in Europe, in our view. But whether or not this truly represents a<br />

new Zeitgeist, for investors there is a simple message: to invest<br />

in companies that are riding this wave of change. |

GLOBAL INVESTOR 2.05 <strong>Marketing</strong> versus <strong>innovation</strong>—11<br />

%<br />

USD<br />

80<br />

40,000<br />

70<br />

35,000<br />

60<br />

30,000<br />

50<br />

GDP per capita (real), r.h. scale<br />

25,000<br />

40<br />

20,000<br />

30<br />

20<br />

Happiness (% very happy), l.h.scale<br />

15,000<br />

10,000<br />

10<br />

5000<br />

Source: Credit Suisse<br />

Note: Data from the book titled “Happiness: Lessons from a new science” by Richard Layard<br />

0<br />

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000<br />

0<br />

Corporate emphasis on marketing over <strong>innovation</strong> implies that much of rising GDP has gone to bigger, shinier<br />

versions of existing products, which doesn’t really make us happier.

The European chemicals industry: Innovation is the key to remaining competitive<br />

The golden age of chemicals <strong>innovation</strong> (i.e., dyes, fertilizers, plastics<br />

<strong>and</strong> many other products) ended in the 1960s <strong>and</strong> was followed by<br />

decades of limited, incremental development. Now at last, that is changing<br />

as interdisciplinary research promises a new era of genuine <strong>innovation</strong>. Dr. Maria Custer<br />

Chemistry is all around us. Industrial chemicals enrich daily life,<br />

whether in food production, agriculture, medicines, cosmetics,<br />

textiles, electronics or cars. The industry produces a vast array<br />

of diverse products, originating from raw materials derived from<br />

oil, natural gas, minerals <strong>and</strong> air, <strong>and</strong> it supplies practically all<br />

sectors of the economy. Until around the 1990s, specialty chemicals<br />

were high-margin products produced in small volumes <strong>and</strong><br />

sold at high prices, justified by the products’ capacity to fulfill<br />

specific functions. These businesses sat reasonably comfortably<br />

alongside pharmaceuticals, which were also high-margin, intellectual-property-driven<br />

activities. However, at that time parent<br />

companies decided to concentrate on pharmaceuticals, spinning<br />

off their specialty chemicals businesses into separate firms. For<br />

example, S<strong>and</strong>oz demerged its specialty chemicals business by<br />

floating Clariant before creating Novartis with Ciba-Geigy, while<br />

Astra-Zeneca <strong>and</strong> Novartis hived off their agrochemicals divisions<br />

to create Syngenta. Nevertheless, the newly formed specialty<br />

chemicals companies were rapidly confronted with the commoditization<br />

of many of their products.<br />

While the global specialty chemicals market has traditionally<br />

been dominated by the USA <strong>and</strong> Europe, Asian countries – particularly<br />

China <strong>and</strong> India – are becoming important players too.<br />

These countries benefit not only from low-cost manufacturing, but<br />

from the strong dem<strong>and</strong> for chemicals in the region as well.<br />

Roughly 70% of the plastic toys worldwide, for instance, are produced<br />

in China, where the market for plastics is growing at a rate<br />

of 15% per annum. Other segments with high dem<strong>and</strong> for chemicals<br />

in Asia are footwear (accounting for 74% of global dem<strong>and</strong><br />

for chemicals) leather (50%) <strong>and</strong> textile processing (53%).<br />

Europe’s leading position as chemicals producer threatened<br />

The European chemicals industry has enjoyed a leading global<br />

position in past decades, though this position is weakening rapidly.<br />

In 1992, the EU produced 32% of available chemicals worldwide.<br />

According to the European Chemical Industry Council<br />

(CEFIC), this market share dropped to 28% in 2002. By 2015, the<br />

CEFIC expects Europe’s share of global chemicals production to<br />

be between 23% (best-case scenario) <strong>and</strong> 16% (worst-case<br />

scenario) (see Figure 1). In a study titled “Horizon 2015, Perspectives<br />

for the Chemical Industry,” published in 2004, CEFIC explains<br />

that the main factors negatively affecting competitiveness in<br />

Figure 1<br />

The EU’s share of global chemicals production<br />

is declining<br />

Source: CEFIC<br />

34<br />

32<br />

30<br />

28<br />

26<br />

24<br />

22<br />

20<br />

18<br />

16<br />

14<br />

12<br />

10<br />

8<br />

%<br />

32<br />

32<br />

30 30 30<br />

20.5<br />

19.0<br />

13.2<br />

14.815.817.1<br />

27 28 23.7<br />

23?<br />

16?<br />

90 92 94 96 98 00 02 04 06 08 10 12 14 16<br />

EU USA Asia excluding Japan Japan

GLOBAL INVESTOR 2.05 Chemicals—13<br />

Innovation feeds ideas<br />

Ciba SC offers a broad range of innovative products for packaging, enhancing product protection <strong>and</strong> conservation.<br />

Ciba’s Shelfplus UV filters block ultraviolet light, extending the shelf life of the product.

Europe are 1) the decreasing attractiveness of investments in<br />

Europe due to low dem<strong>and</strong> growth in the region, delocalization<br />

of customer industries, high production costs <strong>and</strong> highly regulated<br />

environment; 2) the decline in R&D spending in the region<br />

(see Figure 2); <strong>and</strong> 3) an eroding skill base (according to<br />

CEFIC, the number of graduates in the field of chemicals in the<br />

EU is estimated to decrease by 10% per annum between 1996<br />

<strong>and</strong> 2007).<br />

Strategies of European companies to remain competitive<br />

p Expansion to Asia … The importance of the Asian markets for<br />

the chemicals industry is well known, <strong>and</strong> for virtually all companies<br />

under our research coverage, expansion to Asia is a key point<br />

in their strategy. Between 2001 <strong>and</strong> 2005, BASF, for example, is<br />

investing approximately 20% – 25% of the group’s total capital<br />

expenditure, or USD 5.6 billion (including USD 2 billion in China),<br />

in Asia. European companies follow diverse strategies in Asia, but<br />

it is clear that their activities in the region are not confined to<br />

production, in order to reduce costs or to be closer to the chemical<br />

consumer markets. They also include the formation of R&D<br />

centers. Ciba Specialty Chemicals, for example, has just opened<br />

a new R&D center in Shanghai.<br />

p … <strong>and</strong> differentiation through <strong>innovation</strong>. The other pillar of<br />

the strategy currently followed by the industry to remain competitive<br />

is product differentiation through <strong>innovation</strong> <strong>and</strong> improving<br />

customer relationships. We observe a strong trend in the sector<br />

toward <strong>innovation</strong>, driven by the need of providing solutions to<br />

customers. Clariant, for example, is able to offer color systems<br />

for every element in the interior of a car. The “Clariant Color Concept”<br />

for the automotive industry enables the harmonization of<br />

colors of textiles, leather, plastics <strong>and</strong> aluminum inside the car.<br />

This process takes place mainly in collaboration with customers,<br />

which means that R&D <strong>and</strong> marketing efforts come together to<br />

ensure the market relevance of new products <strong>and</strong> services. Specialty<br />

chemical companies aim to have a proportion of approximately<br />

25% new products (products less than five years old) in<br />

their portfolios.<br />

Despite the focus on <strong>innovation</strong>, R&D expenses as a percentage<br />

of sales have remained more or less stable during the past<br />

ten years (see Figure 3). The fact that the focus on <strong>innovation</strong> as<br />

a key for competitiveness does not translate into higher R&D<br />

expenses as a percentage of sales is due to several factors. First,<br />

R&D expenses do not necessarily correlate with productivity of<br />

R&D. Second, the most important trend in R&D seems to be the<br />

necessity of focusing on a smaller number of projects with potential<br />

for quick commercialization, rather than following a large<br />

number of projects in parallel.<br />

Besides in-house research <strong>and</strong> collaborations with companies<br />

with new technologies <strong>and</strong> academic groups, a possibility to<br />

drive <strong>innovation</strong> is the acquisition of technologies or smaller firms<br />

with expertise in specific fields (see Figure 4). BASF, for example,<br />

invests in start-up companies through its BASF Venture Capital<br />

GmbH subsidiary.<br />

Figure 2<br />

R&D expenditures as percentage<br />

of sales by region<br />

Source: The European Chemical Industry Council (CEFIC)<br />

4.5<br />

4.0<br />

3.5<br />

3.0<br />

2.5<br />

2.0<br />

1.5<br />

25<br />

20<br />

15<br />

10<br />

5<br />

%<br />

95 96 97 98 99 00 01 02<br />

EU USA Japan<br />

Figure 3<br />

Despite more focus on <strong>innovation</strong>, R&D<br />

expenses as a percentage of sales<br />

remain stable, at approximately 5% on average<br />

for the sector<br />

Source: CSFB HOLT<br />

%<br />

R&D focus on extending product lines, improving processes<br />

The golden age of <strong>innovation</strong> in the chemicals sector was in the<br />

1930s to 1950s, when the industry brought to the market life-changing<br />

products such as plastics <strong>and</strong> man-made fibers. During the<br />

last 20 years, there have been only a few really “revolutionary”<br />

products.<br />

0<br />

94 95 96 97 98 99 00 01 02 03<br />

R&D as % of sales<br />

SG&A as % of sales

GLOBAL INVESTOR 2.05 Chemicals—15<br />

Fertilizers<br />

Nanotechnology, biotechnology<br />

Dyes<br />

Nylon, plastics<br />

Real <strong>innovation</strong>:<br />

plastics, dyes …<br />

Development <strong>and</strong><br />

commoditization<br />

Interdisciplinary<br />

<strong>innovation</strong><br />

opportunities<br />

1865 1925 1950<br />

1970<br />

1990<br />

2005<br />

Source: Credit Suisse<br />

The golden age of <strong>innovation</strong> in the chemicals sector was in the 1930s to 1950s, when the industry brought to<br />

[Topic_Quote] the market life-changing products [Topic_Quote_Autor]<br />

such as plastics <strong>and</strong> man-made fibers. Looking ahead from now,<br />

<strong>innovation</strong> will mainly come from new research areas such as nanotechnology <strong>and</strong> biotechnology, <strong>and</strong> these<br />

interdisciplinary approaches offer significant potential for growth over the coming decade.

p Packaging, performance <strong>and</strong> appearance: Ciba SC offers a<br />

broad range of innovative products for the production of paper<br />

<strong>and</strong> plastic packaging. These specialty chemicals enhance product<br />

protection <strong>and</strong> conservation, packaging integrity, product<br />

promotion <strong>and</strong> manufacturing ease. Fast food packaged in paper<br />

for microwave cooking (e.g., popcorn, french fries, fried chicken)<br />

requires a stain-resistant barrier. Ciba’s LODYNE ® is a repellent for<br />

oil, grease <strong>and</strong> water that helps to keep the package stain-free. Light<br />

can cause colors to fade <strong>and</strong> loss of vitamins in products packaged<br />

in plastic bottles. Ciba’s Shelfplus UV filters block ultraviolet<br />

light, extending the shelf life of the product (see page 13).<br />

Really innovative new products will emerge from interdisciplinary<br />

research combining knowledge of chemicals with new technological<br />

developments such as biotechnology <strong>and</strong> nanotechnology:<br />

p Biotechnological processes are used for the synthesis of<br />

chemicals. The advance of scientific knowledge in areas such as<br />

biotechnology <strong>and</strong> nanotechnology have opened new opportunities<br />

for the chemicals industry. The traditional chemicals-based<br />

methods are often more awkward than the biotechnological processes.<br />

Biotechnology uses microorganisms or cell cultures as<br />

“production machines.” One example is chiral compounds. BASF<br />

uses an enzymatic process for the production of chiral intermediates.<br />

These products are sold under the br<strong>and</strong> name ChiPros.<br />

Syngenta has extensive expertise in plant biotechnology <strong>and</strong> a<br />

dedicated scientific team working closely with academia to develop<br />

biopharmaceuticals that can be produced by plants.<br />

p Nanotechnology will most likely play an important role in future<br />

<strong>innovation</strong>: Many chemical companies are investigating the application<br />

of nanotechnology to areas such as plastics, electronics<br />

<strong>and</strong> pharmaceuticals. Nanotechnology opens up new opportunities<br />

for the chemicals industry. At the nano level, materials show<br />

different properties (e.g., color, magnetic properties, electrical<br />

properties, etc.) than at the macroscopic level, allowing the design<br />

<strong>and</strong> construction of innovative materials with better or distinct<br />

electrical, optical or thermal properties.<br />

Innovation versus marketing<br />

The chemicals industry has a distinctive feature in that a substantial<br />

part of the supply chain involves companies in the same or<br />

related industries (automotive, electronics, food, etc.), rather than<br />

consumers, so marketing is not considered as an industry strength.<br />

This is not the case, however, in some specialty chemicals areas,<br />

where customer relationships <strong>and</strong> product development, in close<br />

collaboration with consumers in order to provide solutions for their<br />

needs, is increasingly playing an important role.<br />

In summary, the European chemicals industry of the future<br />

will rely on both <strong>innovation</strong> <strong>and</strong> marketing to remain competitive<br />

amid a tough environment. The role of marketing will be to improve<br />

customer relationships in order to underst<strong>and</strong> client needs <strong>and</strong><br />

to develop new, innovative <strong>and</strong> market-oriented products. Innovation<br />

will mainly come from new research areas such as nanotechnology<br />

<strong>and</strong> biotechnology, <strong>and</strong> these interdisciplinary approaches<br />

offer significant potential for growth over the coming<br />

decade. |<br />

Figure 4<br />

M&A activities in the industry;<br />

acquisition of technology<br />

Source: Company data, Credit Suisse<br />

Materials<br />

Biotech/Food<br />

Genencor<br />

(enzymes)<br />

Eastman high<br />

performance<br />

christaline<br />

plastics<br />

DuPont<br />

Danisco<br />

(Food Ingr.)<br />

ICI Quest’s<br />

Food<br />

Ingredients<br />

Chemicals<br />

Kerry<br />

Food<br />

Monsanto<br />

Emergent<br />

genetics<br />

Syngenta<br />

Merck<br />

KGaA<br />

Avecia’s<br />

OLED <strong>and</strong><br />

polymers<br />

Biotech/Seeds<br />

Golden Harvest<br />

Seeds<br />

Technology/<br />

Nanotechnology

GLOBAL INVESTOR 2.05 Healthcare—17<br />

Will <strong>innovation</strong> regain the upper h<strong>and</strong> over marketing in pharma?<br />

Hope looms for a turnaround in big pharma as strategies begin to shift toward<br />

meaningful <strong>innovation</strong> – rather than progressing in small increments – to provide<br />

long-lasting value creation. Dr. Luís Correia, Dr. Maria Custer<br />

The pharmaceuticals sector has fallen out of favor with many<br />

investors. We believe this mainly reflects pricing pressure, patent<br />

expirations <strong>and</strong> slowing research productivity. We think that this<br />

can be traced back to overemphasis on marketing compared with<br />

<strong>innovation</strong>. Many big pharma companies now spend more on<br />

marketing than some of the large consumer goods companies,<br />

<strong>and</strong> their sales forces have grown rapidly. Although this marketingdominated<br />

approach proved very profitable for some time, we<br />

believe that it has sapped the large pharmaceutical companies’<br />

ability to deliver true <strong>innovation</strong>. This damages profitability in the<br />

long run, <strong>and</strong> we argue that this is a key driving force behind the<br />

recent poor performance of pharmaceuticals shares. Looking<br />

ahead, we feel that there is hope for a turnaround in big pharma<br />

as strategy begins to shift toward meaningful <strong>innovation</strong> – rather<br />

than advancing in small increments – providing long-lasting value<br />

creation.<br />

The rise of marketing in the pharmaceuticals industry<br />

Over the last two decades, the importance of marketing in the<br />

pharmaceuticals industry has risen sharply, <strong>and</strong> now surpasses<br />

that of many consumer goods companies (see Figure 1). Several<br />

factors have driven this development:<br />

p The realization that primary care products were promotion<br />

sensitive <strong>and</strong> that greater product sales meant more profits. The<br />

undisputed leader of this marketing/blockbuster strategy is Pfizer,<br />

which managed to achieve the industry’s highest operating margins<br />

– close to 40%. As competitors tried to keep pace, this<br />

inevitably led to a race: i.e., a sharp increase in the size of sales<br />

forces (see page 18).<br />

p The introduction of direct-to-consumer advertising. Over the<br />

last 10 years, spending on direct-to-consumer advertising has<br />

risen sharply (see Figure 2). While this spending still represents<br />

a small fraction of overall marketing costs, it can mean allocations<br />

of significant proportions for specific mass-market products (such<br />

as allergy treatments or oral contraceptives). The objective of the<br />

pharmacy industry was to generate dem<strong>and</strong> driven by patients,<br />

rather than relying exclusively on promotion to physicians.<br />

p Crowded therapy classes driving the need for intense spending<br />

in clinical trials, with the aim of differentiation. In this regard, the<br />

state of things has not changed much as analyses such as those<br />

shown in Figure 3 suggest. As a rough approximation, we regard<br />

the number of products in development as a measure of R&D<br />

Figure 1<br />

Selling, general & administrative (SG&A)<br />

expenses as % of sales for pharma <strong>and</strong><br />

consumer goods companies<br />

Source: GS (Note: As a proxy for marketing costs, we use data on SG&A expenses)

Number of sales representatives in the US pharmaceuticals market (1994 – 2003)<br />

Source: Verispan<br />

thous<strong>and</strong>s<br />

100<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

94 95 96 97 98 99 00 01 02 03<br />

Big pharma new product approvals in the USA (1998 – 2004)<br />

Source: FDA, LB, Credit Suisse<br />

40<br />

35<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

98 99 00 01 02 03 04E<br />

While marketing expenditures have risen, the number of new product approvals in big pharma has declined.

effort. The figure indicates that companies continue focusing their<br />

efforts on the largest commercial opportunities. In our view, they<br />

do not seem to be taking into account the fact that if they all do<br />

the same, they will be paving the way for tough competition <strong>and</strong><br />

decreasing value at a later stage!<br />

GLOBAL INVESTOR 2.05 Healthcare—19<br />

The marketing/lifecycle management game cannot last forever<br />

Before patents expire <strong>and</strong> in the absence of a truly novel molecule<br />

to replace the old one, companies attempt to launch so-called<br />

line extensions, or second-generation drugs, which correspond<br />

to minor improvements over the older product. While the old<br />

product is charged at 30% of the price in the USA once it goes<br />

generic, a line extension can retain a price similar to the original<br />

price of the old drug. It is this sort of strategy that annoys healthcare<br />

payers <strong>and</strong> damages the reputation of the pharmaceutical<br />

industry.<br />

The combination of lifecycle extension tactics with the blockbuster<br />

strategy described previously has been almost consensual<br />

in big pharma. In our view, it explains the developments of<br />

recent years of increased pricing pressure already before patents<br />

expire. Healthcare payers have resorted to tools such as increasing<br />

patient co-payments for the more expensive drugs within a class,<br />

so that they are encouraged to use generics or the cheaper drug.<br />

A further downside to the blockbuster strategy is the dependecy<br />

it creates on few drugs. This can pose high risk of a sharp decline<br />

in earnings once patents expire <strong>and</strong> there are no substitutes.<br />

Best innovators moved away from supremacy of marketing<br />

Under this new, more competitive environment, analysts have<br />

started to evaluate companies’ portfolios to identify the better<br />

placed companies, i.e. the ones with more unique products that<br />

are subject to less pricing competition (see Figure 4).<br />

The rise in importance of marketing has meant that marketing<br />

departments have gained such a high profile in pharmaceutical<br />

companies that the key decision makers <strong>and</strong> best-paid workers<br />

are the marketers. Dissatisfaction with this state of things has led<br />

many scientists <strong>and</strong> medical developers to start their own businesses.<br />

We believe this was a main driving factor beyond the<br />

emergence of the biotechnology industry. As biotechnology companies<br />

matured over the last 20 years, their importance has<br />

become evident in terms of the weight of their products <strong>and</strong> R&D<br />

pipelines. A good case in point is Genentech.<br />

Genentech<br />

Genentech is a very innovative company within the healthcare<br />

sector. Since its founding in 1976, it has remained at the forefront<br />

of <strong>innovation</strong> based on its scientific strengths. Scientists at<br />

Genentech have focused on the underst<strong>and</strong>ing of the molecular<br />

basis of disease. The strong expertise in oncology allowed the<br />

development of several cancer drugs with novel <strong>and</strong> more specific<br />

mechanisms of action. Although these drugs are commonly<br />

used in combination with existing chemotherapeutic agents, they<br />

represent an important step into targeted <strong>and</strong> less aggressive<br />

therapies. Rituxan, the first therapeutic antibody to treat cancer<br />

in the USA, was approved in 1997. Rituxan works by binding to a<br />

particular protein on the surface of healthy <strong>and</strong> malignant B-cells,<br />

making them susceptible for the body’s natural defenses. After<br />

treatment, new normal B-cells regenerate from the bone marrow<br />

<strong>and</strong> return to normal levels within months. Avastin, approved in<br />

2004, is the first therapy that inhibits angiogenesis (the process

Figure 2<br />

Amount spent on direct-to-consumer<br />

advertising in the US pharmaceuticals market<br />

1993 to 2003 (USD millions)<br />

Source: Verispan<br />

Figure 4<br />

Product portfolio analysis by degree<br />

of innovativeness<br />

Source: LB<br />

USD millions<br />

3500<br />

3000<br />

2500<br />

2000<br />

1500<br />

1000<br />

500<br />

0<br />

93 94 95 96 97 98 99 00 01 02 03<br />

% of pharma sales in 2004E<br />

100<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

More novel portfolio<br />

Less novel portfolio<br />

Amount spent on direct-to-consumer advertising<br />

in the US pharmaceuticals market 1993–2003<br />

Eli Lilly<br />

Roche<br />

GlaxoSmithKline<br />

Bristol Myers Squib<br />

Schering Plough<br />

Novartis<br />

Sanofi-Aventis<br />

AstraZeneca<br />

Johnson & Johnson<br />

Abbott<br />

Merck<br />

Wyeth<br />

Pfizer<br />

Novel<br />

Genericized<br />

Discountable<br />

Other products<br />

Figure 3<br />

Net present value by therapeutic class versus<br />

number of products in development<br />

Source: GS analysis<br />

Figure 5<br />

Number of projects in R&D by phase 1<br />

Source: Company data <strong>and</strong> LB analysis. P1 P2 P3 refer to the phases of clinical development.<br />

Please note that P1 companies only partially disclose their projects.<br />

NPV (USD billions)<br />

24<br />

20<br />

16<br />

12<br />

8<br />

4<br />

0<br />

Diabethes/Metabolism/<br />

Endocrinology<br />

20.5 bn<br />

Cardiovascular/Thrombosis<br />

13.3 bn<br />

6.3 bn Arthritis/Immunology<br />

Respiratory/<br />

Allergy 5 bn<br />

4.5 bn Others<br />

3.9 bn Anti-infectives/Virology<br />

0.8 bn Reproductive/WH/Fertility<br />

15.8 bn Oncology<br />

15.8 bn CNS<br />

Number of drugs<br />

160<br />

140<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

Number of<br />

molecules<br />

0<br />

5 10 15 20 25 30 35 40 45 50 55 60 65 70 75<br />

P1<br />

P2 P3 Filed<br />

1998 1999 2000 2001<br />

2002 2003 2004<br />

Late-stage projects have been declining,<br />

but signs from the early pipeline are encouraging<br />

1<br />

(AZN,AVE,GSK,NVS,ROG,SASY)

y which new blood vessels develop needed for a tumor to grow)<br />

<strong>and</strong> interferes with the blood supply to tumors.<br />

Beyond the cancer portfolio, the company has pursued highly<br />

novel product opportunities outside the area of cancer. These<br />

products have highly novel mechanisms of action <strong>and</strong> can be considered<br />

first in class: e.g., Raptiva (psoriasis), Xolair (asthma).<br />

Psoriasis occurs when the skin replaces itself too quickly.<br />

This process begins when T-lymphocytes, also called T-cells,<br />

become activated <strong>and</strong> travel to the skin leading to inflammation.<br />

Raptiva, the first biologic therapy for psoriasis, prevents T-cells<br />

from being activated <strong>and</strong> entering the skin.<br />

Interestingly, Genentech’s majority owner, Roche, has decided<br />

not to exercise its opt-in rights on these non-cancer products.<br />

Instead, Genentech has partnered them with other companies. A<br />

possible reason that Roche decided not to license these products<br />

is that they did not satisfy a minimum level of commercial potential.<br />

GLOBAL INVESTOR 2.05 Healthcare—21<br />

Decline in R&D productivity is mainly a big pharma problem<br />

In recent years, big pharma has had an effective decline in products<br />

in phase III trials <strong>and</strong> flat trend in new product filings, as<br />

illustrated in Figure 5.<br />

This has several possible reasons, in our view. Mergers have<br />

typically led to streamlining of R&D projects. More stringent<br />

requirements by the authorities have led companies to resize <strong>and</strong><br />

redesign their late-stage clinical trials. The pharmacological targets<br />

that could be exploited for new drug discovery with the knowledge<br />

of ten years ago reached a saturation point. The first fruits of new<br />

research methodology based on genomics <strong>and</strong> proteomics could<br />

start to bear fruit.<br />

New technologies in research should start delivering soon<br />

During the 1950s <strong>and</strong> 1960s, the strategy for drug development<br />

was screening of known compounds <strong>and</strong> new molecules in animal<br />

models. Although several important drugs were discovered using<br />

this approach (e.g., benzodiazepines), the method was limited in<br />

that the number of molecules with structural diversity was not<br />

enough, <strong>and</strong> that the mechanism of action of many drugs was<br />

unknown.<br />

With the development of knowledge in cell biology during the<br />

1960s <strong>and</strong> early 1970s, it was possible to use a more rational<br />

approach. Scientists would identify proteins (receptors) relevant<br />

to conditions such as asthma or diseases such as glaucoma, <strong>and</strong><br />

then find a drug to inhibit its action (in some cases, the problem<br />

would be the other way round, where a receptor was meant to do<br />

something desirable but was failing to do so, <strong>and</strong> in such cases<br />

the aim would be to find a drug to enhance the action of the<br />

receptor). For example, beta-blockers (i.e., drugs that block the<br />

β-adrenergic receptors) have around 30 different indications,<br />

such as treating irregular heartbeats, addressing high blood pressure,<br />

<strong>and</strong> relieving migraines, to cite just three.<br />

From the mid-1980s, new solutions based on biotechnology<br />

began to appear. The earliest major example was the development<br />

of biotechnologically produced insulin, which has transformed<br />

the lives of diabetics around the world.<br />

With the start of the new millennium, biotechnology has<br />

taken another big step forward, helped by three key factors. First,<br />

scientists’ underst<strong>and</strong>ing of the biochemical factors causing<br />

diseases has been greatly enhanced by advances in genetics,<br />

including the sequencing of the human genome. Second, modern<br />

combinatorial chemistry greatly facilitates the creation of large<br />

Figure 6<br />

Number of new product approvals<br />

in the USA (1998 – 2004)<br />

Source: FDA, LB, Credit Suisse<br />

40<br />

35<br />

30<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

98 99 00 01 02 03 04E<br />

Pharmaceuticals<br />

Biotechnology

Generica<br />

Line extension<br />

Before patents expire <strong>and</strong> in the absence of a truly novel molecule to replace the old one, companies attempt<br />

to launch so-called line extensions, or second-generation drugs, which correspond to minor improvements over<br />

the older product.

numbers of possible drugs. Third, mass screening techniques<br />

allow this plethora of possible drugs to be subjected to at<br />

least a preliminary testing of their effectiveness in a very short<br />

time span. Processes of this kind are only preliminary, but they<br />

prevent a large number of dead-ends very quickly so that the<br />

much more expensive <strong>and</strong> time-consuming phase of full testing<br />

focuses on putative drugs, for which the chance of success is<br />

reasonably high. The result is that the number of diseases for<br />

which a cure may be found has risen substantially <strong>and</strong> continues<br />

to grow.<br />

Reflecting these advances, an increase in the number of<br />

early stage R&D projects (phase I <strong>and</strong> II, see Figure 4) provides<br />

some reasons to be hopeful in the coming years. GlaxoSmithKline<br />

could be the focal point for the industry on this front. The company<br />

expects to report phase II results for 15 new drugs as soon<br />

as 2005.<br />

GLOBAL INVESTOR 2.05 Healthcare—23<br />

The future belongs to innovators<br />

Typical analyses of the industry tend to focus on the decline<br />

of new product launches, but we believe that these analyses<br />

very often exclude biotechnological products. If we include the<br />

approvals of products from biotechnology <strong>and</strong> smaller pharma<br />

companies, we arrive at a positive trend over the last years (see<br />

Figure 6). What is more, the importance of biotechnology companies<br />

is gaining significance in terms of new product output.<br />

In summary, we believe that <strong>innovation</strong> is still the lifeblood of<br />

the pharmaceutical industry. Overall, the biotechnology industry<br />

has generated higher returns (see Figure 7), which seems only a<br />

fair reward for the greater risk taking <strong>and</strong> willingness to genuinely<br />

innovate. Can the pharmaceutical industry balance the power<br />

between research <strong>and</strong> marketing in a better way? This is an issue<br />

that is even more concerning since many of the large blockbuster<br />

products will lose patent exclusivity over the next three<br />

years, <strong>and</strong> it is difficult to see enough pipeline opportunities to<br />

make up for the lost sales. Some views in the financial markets<br />

point to the inevitability of a reduction in sales force for companies<br />

with significant patent expirations, which would avoid a sizable<br />

earnings shortfall in the near term. Some in the industry have<br />

said that an initiative by industry leader Pfizer to reduce its sales<br />

force would be greatly welcomed. However, the same circles<br />

emphasize that cost savings from such a move would be reinvested<br />

in R&D. It may still be only wishful thinking, but we see it<br />

as an encouraging sign. |<br />

Figure 7<br />

Performance of biotechnology versus<br />

pharmaceuticals over ten years<br />

Source: Datastream<br />

1400<br />

1200<br />

1000<br />

800<br />

600<br />

400<br />

200<br />

0<br />

12/93<br />

12/94<br />

12/95<br />

12/96<br />

12/97<br />

12/98<br />

12/99<br />

12/00<br />

12/01<br />

12/02<br />

12/03<br />

12/04<br />

World DS Biotechnology price index<br />

World DS Pharaceuticals price index

GLOBAL INVESTOR 2.05 Automobiles—24<br />

Driving the future<br />

For the car industry, developed countries are replacement markets, where new<br />

customers can only be acquired by gaining market share from the competition.<br />

<strong>Marketing</strong> <strong>and</strong> sales incentives are key elements of this strategy, but in mature markets<br />

like Europe <strong>and</strong> North America, they rapidly become a zero-sum game. Markus Mächler<br />

Penetration into fast-growing emerging markets is one response<br />

to this problem, but the competition is fierce here too. The other<br />

response would be to try to re-invigorate the developed markets<br />

through radical <strong>innovation</strong>, for example, in new fuel systems or<br />

utterly new market segments such as ultra-lightweight urban<br />

vehicles. Instead, the major automobile manufacturers have<br />

focused on relatively marginal <strong>innovation</strong>, which is rapidly copied<br />

<strong>and</strong> ultimately is little better than marketing spending in terms of<br />

the benefits it brings to companies <strong>and</strong> consumers.<br />

US <strong>and</strong> European car registrations reached their peak in 2000,<br />

followed by a sharp correction of the economy (due to post 9/11<br />

shock, the economic slowdown <strong>and</strong> end of the so-called technology<br />

bubble). As consumer confidence diminished, especially in the USA,<br />

the automobile industry increased sales incentives <strong>and</strong> marketing<br />

led strategy did achieve its narrow objective of sustaining sales<br />

volumes. As Figure 1 shows, this marketing-led strategy did<br />

achieve its narrow objective of sustaining sales volumes. However,<br />

it did so at the expense of margins. This was a deliberate<br />

choice by the US mass-market manufacturers, which were not<br />

flexible enough to cut volumes substantially due to their pension<br />

<strong>and</strong> healthcare costs. Measured as a percentage of sales, average<br />

incentives per automobile have risen steeply in the last six<br />

years, while R&D spending has fallen (see Figure 2).<br />

The US <strong>and</strong> the European market are both over-saturated car<br />

markets. Despite greater spending on marketing, only a few car<br />

manufacturers have managed to grow during the last few years.<br />

Consumer response to higher incentive spending is decreasing.<br />

Pressure from raw-materials prices has become an issue <strong>and</strong><br />

does not allow carmakers to further cut prices either. The question<br />

is how to keep consumer spending at least stable. In our view,<br />

only serious <strong>innovation</strong> can help bring the automobile industry out<br />

of this current predicament (see Figure 3).<br />

Increasingly, the major automobile manufacturers have concentrated<br />

on what we would describe as “pseudo-<strong>innovation</strong>,” i.e.,<br />

changing the size <strong>and</strong> shape of cars as part of a marketing-led<br />

strategy to appeal to image <strong>and</strong> perception, without fundamentally<br />

altering their functionality. The rapid growth of the sports<br />

utility vehicle (SUV) market is an example of this. In the short term,<br />

this can be highly successful, allowing early movers to capture<br />

significant market share. But over time, it becomes a zero-sum<br />

game as others enter the new market segment <strong>and</strong> drive margins<br />

Figure 1<br />

US consumer confidence <strong>and</strong> new passenger<br />

car registrations<br />

Source: Autodata<br />

150<br />

130<br />

110<br />

90<br />

70<br />

50<br />

30<br />

01/76<br />

07/78<br />

01/80<br />

07/82<br />

01/84<br />

07/86<br />

01/88<br />

07/90<br />

01/92<br />

07/94<br />

01/96<br />

07/98<br />

01/00<br />

07/02<br />

01/04<br />

US consumer confidence index SADJ (l.h. scale)<br />

US new passenger car <strong>and</strong> light truck sales (r.h. scale)<br />

millions of units<br />

18<br />

17<br />

16<br />

15<br />

14<br />

13<br />

12<br />

11<br />

10<br />

9<br />

8

China is currently the third-largest car market after the USA <strong>and</strong> Japan<br />

The Middle Kingdom experienced phenomenal growth in dem<strong>and</strong> for automobiles following the WTO entry in<br />

December 2001. China has a large number of local car producers facing increasing competition from<br />

Western car manufacturers in their home market. Will they be able to export their products to the Western world?

down again. Spending on research <strong>and</strong> development (R&D) was<br />

dispersed across a wider product range <strong>and</strong> more technical gizmos<br />

to cover every possible niche, instead of being focused on developing<br />

genuine <strong>innovation</strong>s. As a result, there has been miserably<br />

slow progress on new technologies that could have really breathed<br />

new life into the industry, such as fuel cells (see below). In addition,<br />

the life cycle of existing model lines shortened on increasing<br />

competition.<br />

While the life cycle of a car model is getting shorter <strong>and</strong><br />

shorter, the average car in use is getting older <strong>and</strong> older. In Germany,<br />

a country where the automobile plays a significant role, the<br />

average age of a car increased from 6.8 years to 7.6 years<br />

between 1999 <strong>and</strong> 2003. The same trend can be seen in the USA,<br />

where the average age of a car rose from 4.9 years back in the<br />

1970s to 8.6 years in 2004. Notwithst<strong>and</strong>ing marketing campaigns,<br />

such as 0% financing, this trend has only eased in the<br />

short term (see Figure 4).<br />

Due to cost pressure, development of key technology features<br />

has been carried out in cooperation with suppliers or in joint<br />

ventures with other manufacturers. The search for <strong>innovation</strong>s<br />

was not always successful, as seen from an investment point of<br />

view. Despite more than 20 years of research <strong>and</strong> several successful<br />

tests, fuel-cell technology is far from being introduced<br />

into the mass market. Hydrogen-powered engines are also known<br />

as zero-emission power. The best way to picture the evolutionary<br />

development of fuel cells is with the graph of Ballard Power. The<br />

Canada-based company, under control of Chrysler (now Daimler-<br />

Chrysler) <strong>and</strong> Ford, has focused on fuel-cell technology for more<br />

than a decade now (see Figure 5).<br />

The technology is available <strong>and</strong> running, but one big problem<br />

is cost. Fuel-cell units are ten times more expensive to make than<br />

petrol or diesel engines. Another problem is the lack of a refueling<br />

infrastructure, which requires huge investments. Optimistic estimates<br />

for commercial sales of hydrogen-powered cars are made<br />

for 2010, while realistic forecasts predict mass-market penetration<br />

no earlier than 2020. BMW, DaimlerChrysler, Ford <strong>and</strong> Opel<br />

(GM) currently have test vehicles running in Germany, while BMW<br />

uses the technology of liquid hydrogen for conventional car<br />

engines (bi-fuel). However, realizing the goal of making hydrogenpowered<br />

cars available for everyone is between two <strong>and</strong> three<br />

(car) generations away.<br />

Another very promising but unsuccessful technology – the<br />

electric-powered automobile – has fallen far short of market<br />

expectations. The electro car has not disappeared from the scene,<br />

but the lack of development of new-generation batteries has<br />

hampered the success in this segment. Electric-powered cars<br />

use lead acid or nickel metal hydrid batteries, but scientists say<br />

lithium ion batteries are more promising, though still insufficiently<br />

developed for use in automobiles. Lithium ion batteries are<br />

currently more appropriate for use in low-voltage equipment such<br />

as cell phones <strong>and</strong> h<strong>and</strong>-held electronic devices. In terms of<br />

environmental compatibility, the success of electric-powered passenger<br />

cars depends a lot on the means of electricity generation<br />

<strong>and</strong> battery recycling. Taking this <strong>and</strong> significantly higher buying<br />

costs into account, the environmental balance for the time being<br />

is similar to other technologies already in place, such as diesel or<br />

hybrids. Furthermore, after 80 to 100 kilometers, the batteries<br />

need to be recharged, which takes considerable time.<br />

Even with existing electric propulsion technology, it would be<br />

possible to build medium or lightweight urban cars with reason-<br />

Figure 2<br />

Annual US incentives compared<br />

with total marketing <strong>and</strong> R&D spending<br />

Source: Autodata, CSFB HOLT, company data<br />

3500<br />

3000<br />

2500<br />

2000<br />

1500<br />

1000<br />

6<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

%<br />

94 95 96 97 98 99 00 01 02 03 04<br />

US incentives (l.h. scale)<br />

BMW<br />

1994<br />

1998<br />

2002<br />

DCX<br />

Peugeot<br />

Renault<br />

1995<br />

1999<br />

2003<br />

Volkswagen<br />

Fiat<br />

<strong>Marketing</strong> as % of sales<br />

(estimate)<br />

R&D as % of sales<br />

Figure 3<br />

R&D spending by OEMs (original equipment<br />

manufacturers) as % of sales<br />

Source: Company data, broker research<br />

Ford<br />

1996<br />

2000<br />

GM<br />

Toyota<br />

1997<br />

2001<br />

5.0<br />

4.5<br />

4.0<br />

3.5<br />

3.0<br />

2.5<br />

2.0<br />

1.5<br />

Average<br />

%

able range, <strong>and</strong> indeed a few examples are available from specialist<br />

manufacturers. But their costs are relatively high, which is<br />

unsurprising given that they are built on tiny production runs. What<br />

is noticeable by its absence is a viable medium or lightweight<br />

urban electric vehicle produced <strong>and</strong> marketed in large numbers<br />

by one of the major automobile manufacturers – a product which<br />

has the potential to open up whole new market segments.<br />

We cannot be sure whether greater focus on R&D spending<br />

in the key areas such as fuel cells or electric propulsion would<br />

have produced better results. But it is not unreasonable to believe<br />

that we could be far closer to success, if these projects had benefited<br />

from the R&D resources that were instead devoted to adding<br />

a few extra features to adjustable electric seats, or to designing<br />

the shape of yet another SUV, or creating yet another voice<br />

variation for the SatNav system.<br />

Next <strong>innovation</strong> driver will be ecological compatibility<br />

Safety has become a key issue in the automobile industry, but<br />

environmental friendliness is garnering more attention too. With only<br />

few exceptions, most obviously the United States, all major countries<br />

signed the Kyoto Protocol, which is now in place. With the<br />

current technology, it will be very difficult to reach the set targets<br />

of 6%–8% lower emissions by 2012 compared with 1990.<br />

Safety <strong>and</strong> technological features are very often developed<br />

by one of the supplier companies. The latest example comes from<br />

Valeo, which produces a start/stop alternator that automatically<br />

shuts down the engine when a car is stopped at traffic lights<br />

<strong>and</strong> re-starts it when the driver presses the gas pedal. This offers<br />

up to 10% fuel savings for mini <strong>and</strong> small cars. The system is<br />

already available in the Citroen C3 <strong>and</strong> will soon be available<br />

from Ford in its latest Fiesta model. Continental has a start/stop<br />

system available as well, but it is only used in a single GM light<br />

truck model so far. Safety features such as airbag systems <strong>and</strong><br />

seat belts are dominated by Autoliv. The two large US suppliers<br />

Johnson Controls <strong>and</strong> Delphi are very active in safety <strong>and</strong><br />

comfort equipment. Delphi has a special interest in the development<br />

of fuel cells <strong>and</strong> batteries technology. These constitute<br />

good examples underpinning our premise that <strong>innovation</strong> is<br />

currently originating from suppliers <strong>and</strong> to a lesser extent from<br />

OEMs. The exceptions are Japanese manufacturers, where<br />

Toyota <strong>and</strong> Honda heavily invest in hybrid technology. In general,<br />

OEMs try to use synergies resulting from cooperative agreements<br />

in key areas of technology such as engines <strong>and</strong> power-trains.<br />

This harbors the advantage that new developments become<br />

available to a number of OEMs within a short period of time,<br />

though this first-mover advantage from OEMs does not last very<br />

long. The implication for investors is that the more innovative<br />

parts suppliers may offer better medium-term prospects than the<br />

auto majors.<br />

Diesel boom in Europe; still no interest from rest of world<br />

Diesel engines are a real success story in Western Europe, where<br />

market share reached 43.7% of new car registrations in 2003.<br />

One reason for this success comes from improving technology,<br />

where suppliers such as Bosch <strong>and</strong> Beru once again supported<br />

the development significantly. French manufacturers, especially<br />

Peugeot, are the key driver behind the trend, overwhelming the<br />

competition by introducing a diesel catalyst system. Peugeot has<br />

offered this technology for four years now, <strong>and</strong> it seems to<br />

become a set st<strong>and</strong>ard for the European market as a whole.<br />

Figure 5<br />

Ballard Power <strong>and</strong> S&P 500<br />

Source: Bloomberg<br />

GLOBAL INVESTOR 2.05 Automobiles—27<br />

Figure 4<br />

Average age of light vehicles in the<br />

USA since 1970 <strong>and</strong> average age of cars<br />

in Germany since 1994<br />

Source: Polk (USA); VDO (Germany)<br />

9<br />

8.5<br />

8<br />

7.5<br />

7<br />

6.5<br />

6<br />

5.5<br />

5<br />

4.5<br />

1600<br />

1400<br />

1200<br />

1000<br />

800<br />

600<br />

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04<br />

Average age of cars in the USA<br />

Average age of cars in Germany<br />

01/97<br />

01/98<br />

01/99<br />

01/00<br />

S&P 500<br />

Ballard Power (r.h. scale)<br />

01/01<br />

01/02<br />

01/03<br />

01/04<br />

200<br />

180<br />

160<br />

140<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0

Several countries intend to make catalysts compulsory for new<br />

diesel engine-equipped cars in order to reduce particle emissions.<br />

The problem seems to be supply since only a few producers are<br />

able to deliver diesel catalysts at present. One key supplier is<br />

Faurecia, a 71% subsidiary of Peugeot.<br />

Recently, several German car manufacturers had to recall<br />

diesel cars <strong>and</strong> reduce or even close production of several model<br />

lines because supplier Bosch delivered a low-quality injection<br />

pump. OEMs are highly dependent on their suppliers <strong>and</strong> the<br />

quality that they deliver. Automobile suppliers are currently very<br />

powerful; they can pass on higher raw-materials costs to OEMs<br />

<strong>and</strong> even increase their own margins. German car manufacturers<br />

concentrate their diesel research on inner-engine solutions for<br />

the particular problem, but have failed to deliver a system in due<br />

time. The first generation of new diesel engines just hit the market.<br />

Diesel market penetration in North America is still below 1%,<br />

which is attributable to the poor history <strong>and</strong> lack of acceptance<br />

by customers as well as to the poor quality of diesel fuel in the<br />

past. The big question is whether diesel engines will eventually<br />

become a success story in the USA too. (see Figure 6)<br />

The current success story comes from Japan, where hybrids<br />

attract key attention for development. It took three years <strong>and</strong> a<br />

second-generation hybrid car to successfully launch this technology<br />

for the mass market. The latest-generation hybrid cars do<br />

not differ from other automobiles on the road with respect to<br />

shape, look or performance. The <strong>innovation</strong> is taking place behind<br />

the scenes, with an additional electric engine (or even two in the<br />

new Lexus 400h), a trunk of batteries <strong>and</strong> the latest electrical<br />

technology to coordinate the performance between the two different<br />

engines. Even hybrid cars have just started to undergo<br />

<strong>innovation</strong>. Toyota has been the first-mover in this field of technology,<br />

followed by Honda. Both companies are offering their technology<br />

to third parties, which will enable the industry to further<br />

develop this new st<strong>and</strong>ard. Several countries support this technology,<br />

with incentives similar to, or even exceeding, those for diesel<br />

catalyst cars in some European countries. Besides this support,<br />

hybrids provide a real alternative for anyone living in urban areas.<br />

Next-generation hybrid cars will be equipped with diesel-powered<br />

or natural-gas-powered engines, in combination with improved<br />

battery technology or even fuel cells later on.<br />

Natural gas on the edge<br />

Natural-gas technology is drawing more attention as the discussion<br />

for ecological compatibility seriously evolves. Argentina has<br />

the largest fleet of natural-gas-powered cars, with 750,000 units,<br />

followed by Italy with more than 400,000. More cars are available<br />

with bi-fuel tanks, where conventional gasoline <strong>and</strong> natural gas<br />

can be used together, providing the same power <strong>and</strong> performance<br />

as gasoline engines. A number of cars are now available with bifuel<br />

tanks. Besides the ordinary gasoline tank <strong>and</strong> engine, an<br />

additional fuel tank needs to be added <strong>and</strong> some electronics. With<br />

natural-gas technology, the number of fuel stations as well as tax<br />

advantages will be key for this environmentally friendly alternative<br />

to penetrate the market. Several countries in Europe support<br />

natural gas <strong>and</strong> the development of a fuel-station grid. Today,<br />

around 60 fuel stations for natural or biogas are already in place<br />

throughout Switzerl<strong>and</strong>, 555 in Germany <strong>and</strong> 24 in the UK. A full<br />

grid should be in place by 2007 given that political support for tax<br />

cuts on fuel continues. Several gas stations for bio-fuel are<br />

already in place. Bio-fuel is produced without any CO 2 emissions.<br />

Figure 6<br />

Market share of diesel engines in Europe<br />

by country<br />

Source: ACEA<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />