Financial Stability Report No1 20 December 2010 - Banka Qendrore ...

Financial Stability Report No1 20 December 2010 - Banka Qendrore ...

Financial Stability Report No1 20 December 2010 - Banka Qendrore ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

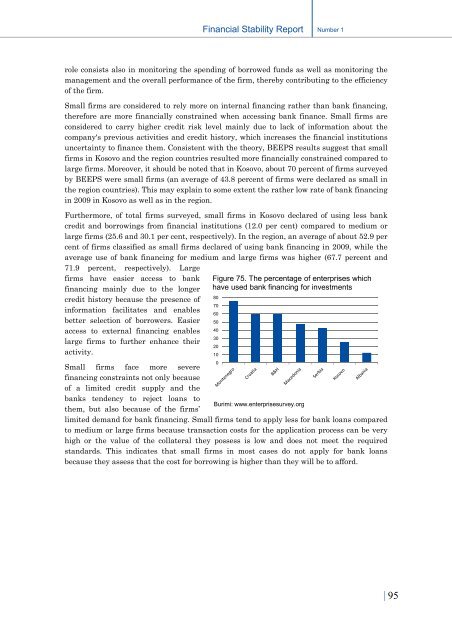

<strong>Financial</strong> <strong>Stability</strong> <strong>Report</strong>Number 1role consists also in monitoring the spending of borrowed funds as well as monitoring themanagement and the overall performance of the firm, thereby contributing to the efficiencyof the firm.Small firms are considered to rely more on internal financing rather than bank financing,therefore are more financially constrained when accessing bank finance. Small firms areconsidered to carry higher credit risk level mainly due to lack of information about thecompany's previous activities and credit history, which increases the financial institutionsuncertainty to finance them. Consistent with the theory, BEEPS results suggest that smallfirms in Kosovo and the region countries resulted more financially constrained compared tolarge firms. Moreover, it should be noted that in Kosovo, about 70 percent of firms surveyedby BEEPS were small firms (an average of 43.8 percent of firms were declared as small inthe region countries). This may explain to some extent the rather low rate of bank financingin <strong>20</strong>09 in Kosovo as well as in the region.Furthermore, of total firms surveyed, small firms in Kosovo declared of using less bankcredit and borrowings from financial institutions (12.0 per cent) compared to medium orlarge firms (25.6 and 30.1 per cent, respectively). In the region, an average of about 52.9 percent of firms classified as small firms declared of using bank financing in <strong>20</strong>09, while theaverage use of bank financing for medium and large firms was higher (67.7 percent and71.9 percent, respectively). Largefirms have easier access to bankfinancing mainly due to the longercredit history because the presence ofinformation facilitates and enablesbetter selection of borrowers. Easieraccess to external financing enableslarge firms to further enhance theiractivity.Figure 75. The percentage of enterprises whichhave used bank financing for investments807060504030<strong>20</strong>100Small firms face more severefinancing constraints not only becauseof a limited credit supply and thebanks tendency to reject loans toBurimi: www.enterprisesurvey.orgthem, but also because of the firms’limited demand for bank financing. Small firms tend to apply less for bank loans comparedto medium or large firms because transaction costs for the application process can be veryhigh or the value of the collateral they possess is low and does not meet the requiredstandards. This indicates that small firms in most cases do not apply for bank loansbecause they assess that the cost for borrowing is higher than they will be to afford.| 95