slides - NABE

slides - NABE

slides - NABE

SHOW LESS

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

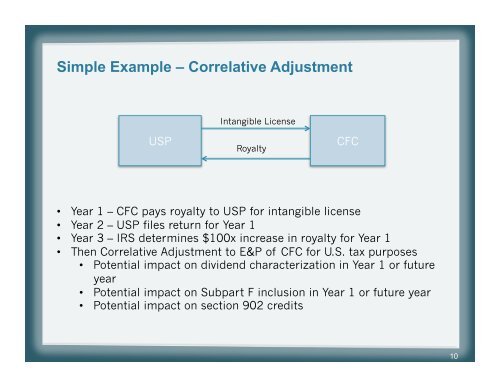

Simple Example – Correlative AdjustmentIntangible LicenseUSPRoyaltyCFC• Year 1 – CFC pays royalty to USP for intangible license• Year 2 – USP files return for Year 1• Year 3 – IRS determines $100x increase in royalty for Year 1• Then Correlative Adjustment to E&P of CFC for U.S. tax purposes• Potential impact on dividend characterization in Year 1 or futureyear• Potential impact on Subpart F inclusion in Year 1 or future year• Potential impact on section 902 credits10