Quarterly Management Discussion & Analysis (MDA300905.pdf)

Quarterly Management Discussion & Analysis (MDA300905.pdf) Quarterly Management Discussion & Analysis (MDA300905.pdf)

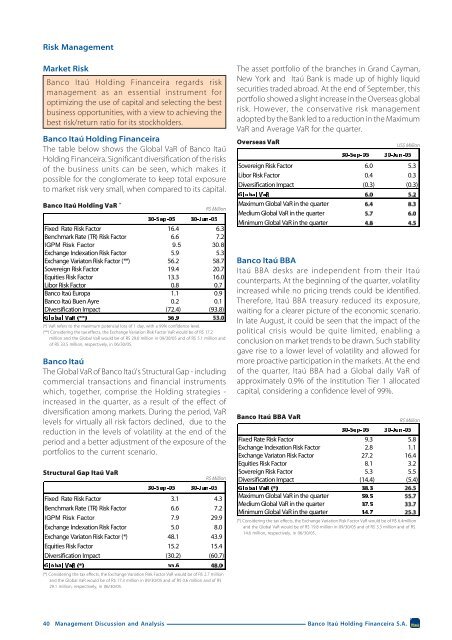

Risk ManagementMarket RiskBanco Itaú Holding Financeira regards riskmanagement as an essential instrument foroptimizing the use of capital and selecting the bestbusiness opportunities, with a view to achieving thebest risk/return ratio for its stockholders.Banco Itaú Holding FinanceiraThe table below shows the Global VaR of Banco ItaúHolding Financeira. Significant diversification of the risksof the business units can be seen, which makes itpossible for the conglomerate to keep total exposureto market risk very small, when compared to its capital.Banco Itaú Holding VaR *(*) VaR refers to the maximum potencial loss of 1 day, with a 99% confidence level.(**) Considering the tax effects, the Exchange Variation Risk Factor VaR would be of R$ 17.2million and the Global VaR would be of R$ 29.6 million in 09/30/05 and of R$ 5.1 million andof R$ 33.5 million, respectively, in 06/30/05.Structural Gap Itaú VaRR$ MillionFixed Rate Risk Factor 16.4 6.3Benchmark Rate (TR) Risk Factor 6.6 7.2 Exchange Indexation Risk Factor 5.9 5.3Exchange Variaton Risk Factor (**) 56.2 58.7Sovereign Risk Factor 19.4 20.7Equities Risk Factor 13.3 16.0Libor Risk Factor 0.8 0.7Banco Itaú Europa 1.1 0.9Banco Itaú Buen Ayre 0.2 0.1Diversification Impact (72.4) (93.8)Banco ItaúThe Global VaR of Banco Itaú's Structural Gap - includingcommercial transactions and financial instrumentswhich, together, comprise the Holding strategies -increased in the quarter, as a result of the effect ofdiversification among markets. During the period, VaRlevels for virtually all risk factors declined, due to thereduction in the levels of volatility at the end of theperiod and a better adjustment of the exposure of theportfolios to the current scenario.R$ MillionFixed Rate Risk Factor 3.1 4.3Benchmark Rate (TR) Risk Factor 6.6 7.2 7.9 29.9Exchange Indexation Risk Factor 5.0 8.0Exchange Variaton Risk Factor (*) 48.1 43.9Equities Risk Factor 15.2 15.4Diversification Impact (30.2) (60.7)The asset portfolio of the branches in Grand Cayman,New York and Itaú Bank is made up of highly liquidsecurities traded abroad. At the end of September, thisportfolio showed a slight increase in the Overseas globalrisk. However, the conservative risk managementadopted by the Bank led to a reduction in the MaximumVaR and Average VaR for the quarter.Overseas VaRUS$ MillionSovereign Risk Factor 6.0 5.3Libor Risk Factor 0.4 0.3Diversification Impact (0.3) (0.3)Maximum Global VaR in the quarterMedium Global VaR in the quarterMinimum Global VaR in the quarterBanco Itaú BBAItaú BBA desks are independent from their Itaúcounterparts. At the beginning of the quarter, volatilityincreased while no pricing trends could be identified.Therefore, Itaú BBA treasury reduced its exposure,waiting for a clearer picture of the economic scenario.In late August, it could be seen that the impact of thepolitical crisis would be quite limited, enabling aconclusion on market trends to be drawn. Such stabilitygave rise to a lower level of volatility and allowed formore proactive participation in the markets. At the endof the quarter, Itaú BBA had a Global daily VaR ofapproximately 0.9% of the institution Tier 1 allocatedcapital, considering a confidence level of 99%.Banco Itaú BBA VaRR$ MillionFixed Rate Risk Factor 9.3 5.8Exchange Indexation Risk Factor 2.8 1.1Exchange Variaton Risk Factor 27.2 16.4Equities Risk Factor 8.1 3.2Sovereign Risk Factor 5.3 5.5Diversification Impact (14.4) (5.4)Maximum Global VaR in the quarterMedium Global VaR in the quarterMinimum Global VaR in the quarter(*) Considering the tax effects, the Exchange Variation Risk Factor VaR would be of R$ 6.4millionand the Global VaR would be of R$ 19.8 million in 09/30/05 and of R$ 3.3 million and of R$14.6 million, respectively, in 06/30/05.(*) Considering the tax effects, the Exchange Variation Risk Factor VaR would be of R$ 2.7 millionand the Global VaR would be of R$ 17.3 million in 09/30/05 and of R$ 0.6 million and of R$29.1 million, respectively, in 06/30/05.40 Management Discussion and AnalysisBanco Itaú Holding Financeira S.A.

Risk ManagementSecurities PortfolioEvolution of Securities PortfolioR$ MillionPublic Securities - Domestic 6,794 22.0% 7,321 25.1% 7,486 25.7% -7.2% -9.2%Public Securities - Foreign 793 2.6% 759 2.6% 1,065 3.7% 4.4% -25.6%Total Public Securities 7,587 24.6% 8,080 27.7% 8,551 29.3% -6.1% -11.3%Private Securities 11,517 37.4% 10,668 36.6% 12,145 41.6% 8.0% -5.2%PGBL/VGBL Funds Quotas 9,182 29.8% 8,274 28.4% 6,918 23.7% 11.0% 32.7%Derivative Financial Instruments 2,944 9.5% 2,535 8.7% 1,962 6.7% 16.1% 50.1%Additional Provision (400) -1.3% (400) -1.4% (400) -1.4% 0.0% 0.0%At September 30, 2005, the balance of Itaú's securitiesportfolio reached R$ 30,830 million, corresponding to a5.7% increase in relation to the closing balance of the priorquarter. Once more, the highlight of the quarter was the11.0% growth seen in the balance of quotas of PGBL/VGBL funds, which totaled R$ 9,182 million at the end ofthe period. It should be kept in mind that the securitiesportfolio of the PGBL/VGBL plans belongs to thecustomers, with a contra entry in liabilities under theheading of Technical Pension Plan Provisions.The share of the government securities in the total of Itaú'ssecurities portfolio at September 30, 2005 was 24.6%,compared to 27.7% in the previous quarter.Private Securities Portfolio and Credit PortfolioTotal funds allocated to finance the activities of thedifferent economic agents who have relationships withItaú amounted to R$ 73,133 million, which represents aR$ 3,818 million growth on the closing balance for thesecond quarter of 2005. The increase in the balance ofcredit transactions rated as AA risk level is partly due tothe risk reassessment process carried out by Banco ItaúBBA in the quarter, as a result of the adjustment of itsmodels in accordance with the Basel II Accord criteria.Funds intended for the economic agentsR$ MillionEuro Bond’s and Similars 3,465 390 111 42 52 4,059Certificates of Deposits 3,016 123 81 11 - 3,230Debentures 1,033 552 79 63 10 1,736Shares 868 206 25 2 0 1,101Promissory Notes 53 32 76 15 - 176Other 504 342 338 28 3 1,215Credit Operations (*) 14,013 25,943 13,055 3,048 5,556 61,616Euro Bond’s and Similars 3,599 559 173 44 32 4,407Certificates of Deposits 2,594 168 1 10 1 2,774Debentures 388 655 114 29 - 1,186Shares 244 829 42 7 1 1,123Promissory Notes 57 28 195 85 - 365Other 184 140 462 26 - 812Credit Operations (*) 9,685 29,255 12,225 2,661 4,821 58,647(*) Endorsements and Sureties included.41 Management Discussion and AnalysisBanco Itaú Holding Financeira S.A.

- Page 5: Executive SummaryConsolidated State

- Page 10 and 11: Executive Summary - Third Quarter o

- Page 12 and 13: Analysis of the Consolidated Net In

- Page 14 and 15: Analysis of the Consolidated Net In

- Page 16 and 17: Analysis of the Consolidated Perfor

- Page 18 and 19: Analysis of the Consolidated Net In

- Page 20 and 21: Analysis of the Consolidated Net In

- Page 22 and 23: 22 Management Discussion and Analys

- Page 24 and 25: Pro Forma Financial Statements by S

- Page 26 and 27: Pro Forma Financial Statements by S

- Page 28 and 29: Itaubanco - Branch BankingThe state

- Page 30 and 31: Insurance, Pension Plan and Capital

- Page 32 and 33: Insurance, Pension Plan and Capital

- Page 34 and 35: Investment Funds and Managed Portfo

- Page 36 and 37: ItaucredThe following tables are ba

- Page 38 and 39: ItaucredVehiclesThe Vehicle segment

- Page 42 and 43: Risk ManagementCredit RiskCredit Op

- Page 44 and 45: Analysis of the Consolidated Balanc

- Page 46 and 47: Activities AbroadTrade Lines Raisin

- Page 48 and 49: Ownership StructureOwnership Struct

- Page 50: PricewaterhouseCoopersAv. Francisco

Risk <strong>Management</strong>Market RiskBanco Itaú Holding Financeira regards riskmanagement as an essential instrument foroptimizing the use of capital and selecting the bestbusiness opportunities, with a view to achieving thebest risk/return ratio for its stockholders.Banco Itaú Holding FinanceiraThe table below shows the Global VaR of Banco ItaúHolding Financeira. Significant diversification of the risksof the business units can be seen, which makes itpossible for the conglomerate to keep total exposureto market risk very small, when compared to its capital.Banco Itaú Holding VaR *(*) VaR refers to the maximum potencial loss of 1 day, with a 99% confidence level.(**) Considering the tax effects, the Exchange Variation Risk Factor VaR would be of R$ 17.2million and the Global VaR would be of R$ 29.6 million in 09/30/05 and of R$ 5.1 million andof R$ 33.5 million, respectively, in 06/30/05.Structural Gap Itaú VaRR$ MillionFixed Rate Risk Factor 16.4 6.3Benchmark Rate (TR) Risk Factor 6.6 7.2 Exchange Indexation Risk Factor 5.9 5.3Exchange Variaton Risk Factor (**) 56.2 58.7Sovereign Risk Factor 19.4 20.7Equities Risk Factor 13.3 16.0Libor Risk Factor 0.8 0.7Banco Itaú Europa 1.1 0.9Banco Itaú Buen Ayre 0.2 0.1Diversification Impact (72.4) (93.8)Banco ItaúThe Global VaR of Banco Itaú's Structural Gap - includingcommercial transactions and financial instrumentswhich, together, comprise the Holding strategies -increased in the quarter, as a result of the effect ofdiversification among markets. During the period, VaRlevels for virtually all risk factors declined, due to thereduction in the levels of volatility at the end of theperiod and a better adjustment of the exposure of theportfolios to the current scenario.R$ MillionFixed Rate Risk Factor 3.1 4.3Benchmark Rate (TR) Risk Factor 6.6 7.2 7.9 29.9Exchange Indexation Risk Factor 5.0 8.0Exchange Variaton Risk Factor (*) 48.1 43.9Equities Risk Factor 15.2 15.4Diversification Impact (30.2) (60.7)The asset portfolio of the branches in Grand Cayman,New York and Itaú Bank is made up of highly liquidsecurities traded abroad. At the end of September, thisportfolio showed a slight increase in the Overseas globalrisk. However, the conservative risk managementadopted by the Bank led to a reduction in the MaximumVaR and Average VaR for the quarter.Overseas VaRUS$ MillionSovereign Risk Factor 6.0 5.3Libor Risk Factor 0.4 0.3Diversification Impact (0.3) (0.3)Maximum Global VaR in the quarterMedium Global VaR in the quarterMinimum Global VaR in the quarterBanco Itaú BBAItaú BBA desks are independent from their Itaúcounterparts. At the beginning of the quarter, volatilityincreased while no pricing trends could be identified.Therefore, Itaú BBA treasury reduced its exposure,waiting for a clearer picture of the economic scenario.In late August, it could be seen that the impact of thepolitical crisis would be quite limited, enabling aconclusion on market trends to be drawn. Such stabilitygave rise to a lower level of volatility and allowed formore proactive participation in the markets. At the endof the quarter, Itaú BBA had a Global daily VaR ofapproximately 0.9% of the institution Tier 1 allocatedcapital, considering a confidence level of 99%.Banco Itaú BBA VaRR$ MillionFixed Rate Risk Factor 9.3 5.8Exchange Indexation Risk Factor 2.8 1.1Exchange Variaton Risk Factor 27.2 16.4Equities Risk Factor 8.1 3.2Sovereign Risk Factor 5.3 5.5Diversification Impact (14.4) (5.4)Maximum Global VaR in the quarterMedium Global VaR in the quarterMinimum Global VaR in the quarter(*) Considering the tax effects, the Exchange Variation Risk Factor VaR would be of R$ 6.4millionand the Global VaR would be of R$ 19.8 million in 09/30/05 and of R$ 3.3 million and of R$14.6 million, respectively, in 06/30/05.(*) Considering the tax effects, the Exchange Variation Risk Factor VaR would be of R$ 2.7 millionand the Global VaR would be of R$ 17.3 million in 09/30/05 and of R$ 0.6 million and of R$29.1 million, respectively, in 06/30/05.40 <strong>Management</strong> <strong>Discussion</strong> and <strong>Analysis</strong>Banco Itaú Holding Financeira S.A.