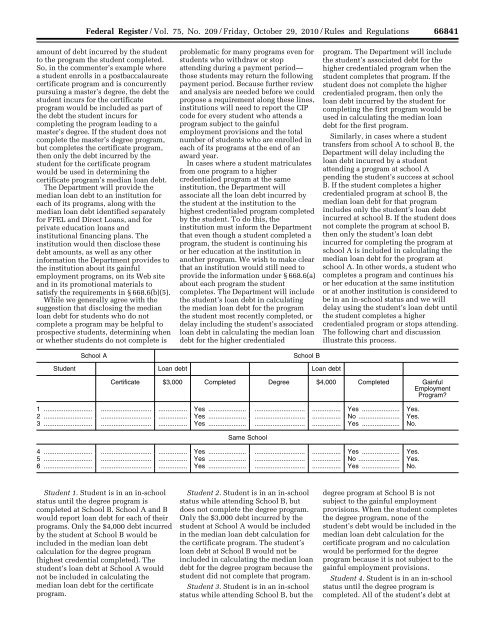

WReier-Aviles on DSKGBLS3C1PROD with RULES266840 Federal Register / Vol. 75, No. 209 / Friday, October 29, 2010 / Rules and Regulationsproviding a competitive advantage toinstitutions with smaller populations <strong>of</strong>student loan borrowers.Many commenters supported theproposed requirement for disclosing themedian debt <strong>of</strong> students who completea program, but suggested thatinstitutions should also disclose themedian debt <strong>of</strong> noncompleters. Thecommenters stated that it was one thingfor students to be told that 40 percentgraduate with $20,000 in loan debt, butit’s another for them to understand thatthe majority <strong>of</strong> students who don’tcomplete have $15,000 in loan debt theywould have to repay. The commentersbelieved that separating the disclosuresby completers and noncompleterswould enable better comparisonsbetween programs, and would not createthe appearance <strong>of</strong> low median debt forprograms with low completion rates. Inaddition, to minimize burden thecommenters suggested that collectingthe data needed to calculate the medianloan debt could appropriately be limitedto programs in which a significant share<strong>of</strong> students borrow. According to thecommenters, this approach wouldensure that potential students and the<strong>Department</strong> know when a program hashigh student borrowing rates and lowcompletion rates.Discussion: We agree with thecommenters that the debt an institutionreports under § 668.6(a)(4) forinstitutional financing plans is theamount a student is obligated to repayupon completing the program. Underthis same section, an institution mustalso report the amount <strong>of</strong> any privateeducation loans it knows that studentsreceived.The HEOA amended both the HEAand the Truth-in-Lending Act (TILA) torequire significant new disclosures forborrowers <strong>of</strong> private education loans.The HEOA also requires privateeducation lenders to obtain a privateloan self-certification form from everyborrower <strong>of</strong> such a loan before thelender may disburse the privateeducation loan.Although the term ‘‘private educationlender’’ is defined in the TILA, theFederal Reserve Board considers anentity to be a private education lender,including an institution <strong>of</strong> highereducation, if it meets the definition <strong>of</strong>‘‘creditor.’’ The term ‘‘creditor’’ is definedby the Federal Reserve Board in 12 CFR226.2(a)(17) as a person who regularlyextends consumer credit that is subjectto a finance charge or is payable bywritten agreement in more than fourinstallments (not including a downpayment), and to whom the obligation isinitially payable, either on the face <strong>of</strong>the note or contract, or by agreementwhen there is no note or contract. Aperson regularly extends consumercredit only if it extended credit morethan 25 times (or more than 5 times fortransactions secured by a dwelling) inthe preceding calendar year. If a persondid not meet these numerical standardsin the preceding calendar year, thenumerical standards must be applied tothe current calendar year.The term private education loan isdefined in 12 CFR 226.46(b)(5) as anextension <strong>of</strong> credit that:• Is not made, insured, or guaranteedunder title IV <strong>of</strong> the HEA;• Is extended to a consumerexpressly, in whole or in part, forpostsecondary educational expenses,regardless <strong>of</strong> whether the loan isprovided by the educational institutionthat the student attends;• Does not include open-end credit orany loan that is secured by real propertyor a dwelling; and• Does not include an extension <strong>of</strong>credit in which the covered educationalinstitution is the creditor if (1) the term<strong>of</strong> the extension <strong>of</strong> credit is 90 days orless (short-term emergency loans) or (2)an interest rate will not be applied tothe credit balance and the term <strong>of</strong> theextension <strong>of</strong> credit is one year or less,even if the credit is payable in morethan four installments (institutionalbilling plans).Examples <strong>of</strong> private education loansinclude, but are not limited to, loansmade expressly for educationalexpenses by financial institutions, creditunions, institutions <strong>of</strong> higher educationor their affiliates, States and localities,and guarantee agencies.As noted previously, the HEOArequires that before a creditor mayconsummate a private education loan, itmust obtain a self-certification formfrom the borrower. The <strong>Department</strong>, inconsultation with the Federal ReserveBoard, developed and disseminated theprivate loan self-certification form inDear Colleague Letter GEN 10–01published in February <strong>of</strong> 2010.The <strong>Department</strong>’s regulations in 34CFR 601.11(d), published on October28, 2009, require an institution toprovide the self-certification form andthe information needed to complete theform upon an enrolled or admittedstudent applicant’s request. Aninstitution must provide the privateloan self-certification form to theborrower even if the institution alreadycertifies the loan directly to the privateeducation lender as part <strong>of</strong> an existingprocess. An institution must alsoprovide the self-certification form to aprivate education loan borrower if theinstitution itself is the creditor. Oncethe private loan self-certification formVerDate Mar2010 14:10 Oct 28, 2010 Jkt 223001 PO 00000 Frm 00010 Fmt 4701 Sfmt 4700 E:\FR\FM\29OCR2.SGM 29OCR2and the information needed to completethe form are disseminated by theinstitution, there is no requirement thatthe institution track the status <strong>of</strong> aborrower’s private education loan.The Federal Reserve Board, in 12 CFR226.48, built some flexibility into theprocess <strong>of</strong> obtaining the selfcertificationform for a private educationlender. The private education lendermay receive the form directly from theconsumer, the private education lendermay receive the form from the consumerthrough the institution <strong>of</strong> highereducation, or the lender may providethe form, and the information theconsumer will require to complete theform, directly to the borrower. However,in all cases the information needed tocomplete the form, whether obtained bythe borrower or by the private educationlender, must come directly from theinstitution.Thus, even though an institution isnot required to track the status <strong>of</strong> itsstudent borrowers’ private educationloans, the institution will know aboutall the private education loans a studentborrower receives, with the exception <strong>of</strong>direct-to-consumer private educationloans, because most private educationloans are packaged and disbursedthrough the institution’s financial aid<strong>of</strong>fice. The institution must report theseloans under § 668.6(a)(4). Direct-toconsumerprivate education loans aredisbursed directly to a borrower, not tothe school. An institution is notinvolved in a certification process forthis type <strong>of</strong> loan.We wish to make clear that any loan,extension <strong>of</strong> credit, payment plan, orother financing mechanism that wouldotherwise not be considered a privateeducation loan but that results in a debtobligation that a student must pay to aninstitution after completing a program,is considered a loan debt arising from aninstitutional financing plan and must bereported as such under § 668.6(a)(4).The <strong>Department</strong> will use the debtreported for institutional financingplans and private education loans alongwith any FFEL or Direct Loan debt fromNSLDS that was incurred by studentswho completed a program to determinethe median loan debt for the program.In general, median loan debt for aprogram at an institution does notinclude debt incurred by students whoattended a prior institution, unless theprior and current institutions are undercommon ownership or control, or areotherwise related entities. In caseswhere a student changes programswhile attending an institution ormatriculates to a higher credentialedprogram at the institution, the<strong>Department</strong> will associate the total

Federal Register / Vol. 75, No. 209 / Friday, October 29, 2010 / Rules and Regulations66841amount <strong>of</strong> debt incurred by the studentto the program the student completed.So, in the commenter’s example wherea student enrolls in a postbaccalaureatecertificate program and is concurrentlypursuing a master’s degree, the debt thestudent incurs for the certificateprogram would be included as part <strong>of</strong>the debt the student incurs forcompleting the program leading to amaster’s degree. If the student does notcomplete the master’s degree program,but completes the certificate program,then only the debt incurred by thestudent for the certificate programwould be used in determining thecertificate program’s median loan debt.The <strong>Department</strong> will provide themedian loan debt to an institution foreach <strong>of</strong> its programs, along with themedian loan debt identified separatelyfor FFEL and Direct Loans, and forprivate education loans andinstitutional financing plans. Theinstitution would then disclose thesedebt amounts, as well as any otherinformation the <strong>Department</strong> provides tothe institution about its gainfulemployment programs, on its Web siteand in its promotional materials tosatisfy the requirements in § 668.6(b)(5).While we generally agree with thesuggestion that disclosing the medianloan debt for students who do notcomplete a program may be helpful toprospective students, determining whenor whether students do not complete isSchool Aproblematic for many programs even forstudents who withdraw or stopattending during a payment period—those students may return the followingpayment period. Because further reviewand analysis are needed before we couldpropose a requirement along these lines,institutions will need to report the CIPcode for every student who attends aprogram subject to the gainfulemployment provisions and the totalnumber <strong>of</strong> students who are enrolled ineach <strong>of</strong> its programs at the end <strong>of</strong> anaward year.In cases where a student matriculatesfrom one program to a highercredentialed program at the sameinstitution, the <strong>Department</strong> willassociate all the loan debt incurred bythe student at the institution to thehighest credentialed program completedby the student. To do this, theinstitution must inform the <strong>Department</strong>that even though a student completed aprogram, the student is continuing hisor her education at the institution inanother program. We wish to make clearthat an institution would still need toprovide the information under § 668.6(a)about each program the studentcompletes. The <strong>Department</strong> will includethe student’s loan debt in calculatingthe median loan debt for the programthe student most recently completed, ordelay including the student’s associatedloan debt in calculating the median loandebt for the higher credentialedSchool Bprogram. The <strong>Department</strong> will includethe student’s associated debt for thehigher credentialed program when thestudent completes that program. If thestudent does not complete the highercredentialed program, then only theloan debt incurred by the student forcompleting the first program would beused in calculating the median loandebt for the first program.Similarly, in cases where a studenttransfers from school A to school B, the<strong>Department</strong> will delay including theloan debt incurred by a studentattending a program at school Apending the student’s success at schoolB. If the student completes a highercredentialed program at school B, themedian loan debt for that programincludes only the student’s loan debtincurred at school B. If the student doesnot complete the program at school B,then only the student’s loan debtincurred for completing the program atschool A is included in calculating themedian loan debt for the program atschool A. In other words, a student whocompletes a program and continues hisor her education at the same institutionor at another institution is considered tobe in an in-school status and we willdelay using the student’s loan debt untilthe student completes a highercredentialed program or stops attending.The following chart and discussionillustrate this process.Student Loan debt Loan debtCertificate $3,000 Completed Degree $4,000 Completed GainfulEmploymentProgram?1 ........................... ............................ ................ Yes ..................... ............................ ................ Yes ..................... Yes.2 ........................... ............................ ................ Yes ..................... ............................ ................ No ....................... Yes.3 ........................... ............................ ................ Yes ..................... ............................ ................ Yes ..................... No.Same School4 ........................... ............................ ................ Yes ..................... ............................ ................ Yes ..................... Yes.5 ........................... ............................ ................ Yes ..................... ............................ ................ No ....................... Yes.6 ........................... ............................ ................ Yes ..................... ............................ ................ Yes ..................... No.WReier-Aviles on DSKGBLS3C1PROD with RULES2Student 1. Student is in an in-schoolstatus until the degree program iscompleted at School B. School A and Bwould report loan debt for each <strong>of</strong> theirprograms. Only the $4,000 debt incurredby the student at School B would beincluded in the median loan debtcalculation for the degree program(highest credential completed). Thestudent’s loan debt at School A wouldnot be included in calculating themedian loan debt for the certificateprogram.Student 2. Student is in an in-schoolstatus while attending School B, butdoes not complete the degree program.Only the $3,000 debt incurred by thestudent at School A would be includedin the median loan debt calculation forthe certificate program. The student’sloan debt at School B would not beincluded in calculating the median loandebt for the degree program because thestudent did not complete that program.Student 3. Student is in an in-schoolstatus while attending School B, but theVerDate Mar2010 14:10 Oct 28, 2010 Jkt 223001 PO 00000 Frm 00011 Fmt 4701 Sfmt 4700 E:\FR\FM\29OCR2.SGM 29OCR2degree program at School B is notsubject to the gainful employmentprovisions. When the student completesthe degree program, none <strong>of</strong> thestudent’s debt would be included in themedian loan debt calculation for thecertificate program and no calculationwould be performed for the degreeprogram because it is not subject to thegainful employment provisions.Student 4. Student is in an in-schoolstatus until the degree program iscompleted. All <strong>of</strong> the student’s debt at

- Page 1 and 2: Friday,October 29, 2010Part IIDepar

- Page 3 and 4: Federal Register / Vol. 75, No. 209

- Page 6 and 7: 66836 Federal Register / Vol. 75, N

- Page 8 and 9: 66838 Federal Register / Vol. 75, N

- Page 12 and 13: 66842 Federal Register / Vol. 75, N

- Page 14 and 15: 66844 Federal Register / Vol. 75, N

- Page 16 and 17: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 18 and 19: 66848 Federal Register / Vol. 75, N

- Page 20 and 21: 66850 Federal Register / Vol. 75, N

- Page 22 and 23: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 24 and 25: 66854 Federal Register / Vol. 75, N

- Page 26 and 27: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 28 and 29: 66858 Federal Register / Vol. 75, N

- Page 30 and 31: 66860 Federal Register / Vol. 75, N

- Page 32 and 33: 66862 Federal Register / Vol. 75, N

- Page 34 and 35: 66864 Federal Register / Vol. 75, N

- Page 36 and 37: 66866 Federal Register / Vol. 75, N

- Page 38 and 39: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 40 and 41: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 42 and 43: 66872 Federal Register / Vol. 75, N

- Page 44 and 45: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 46 and 47: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 48 and 49: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 50 and 51: 66880 Federal Register / Vol. 75, N

- Page 52 and 53: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 54 and 55: 66884 Federal Register / Vol. 75, N

- Page 56 and 57: 66886 Federal Register / Vol. 75, N

- Page 58 and 59: WReier-Aviles on DSKGBLS3C1PROD wit

- Page 60 and 61:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 62 and 63:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 64 and 65:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 66 and 67:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 68 and 69:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 70 and 71:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 72 and 73:

66902 Federal Register / Vol. 75, N

- Page 74 and 75:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 76 and 77:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 78 and 79:

66908 Federal Register / Vol. 75, N

- Page 80 and 81:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 82 and 83:

66912 Federal Register / Vol. 75, N

- Page 84 and 85:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 86 and 87:

66916 Federal Register / Vol. 75, N

- Page 88 and 89:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 90 and 91:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 92 and 93:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 94 and 95:

66924 Federal Register / Vol. 75, N

- Page 96 and 97:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 98 and 99:

66928 Federal Register / Vol. 75, N

- Page 100 and 101:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 102 and 103:

66932 Federal Register / Vol. 75, N

- Page 104 and 105:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 106 and 107:

66936 Federal Register / Vol. 75, N

- Page 108 and 109:

66938 Federal Register / Vol. 75, N

- Page 110 and 111:

66940 Federal Register / Vol. 75, N

- Page 112 and 113:

66942 Federal Register / Vol. 75, N

- Page 114 and 115:

66944 Federal Register / Vol. 75, N

- Page 116 and 117:

66946 Federal Register / Vol. 75, N

- Page 118 and 119:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 120 and 121:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 122 and 123:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 124 and 125:

66954 Federal Register / Vol. 75, N

- Page 126 and 127:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 128 and 129:

66958 Federal Register / Vol. 75, N

- Page 130 and 131:

66960 Federal Register / Vol. 75, N

- Page 132 and 133:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 134 and 135:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 136 and 137:

WReier-Aviles on DSKGBLS3C1PROD wit

- Page 138 and 139:

66968 Federal Register / Vol. 75, N

- Page 140 and 141:

66970 Federal Register / Vol. 75, N

- Page 142 and 143:

66972 Federal Register / Vol. 75, N

- Page 144 and 145:

66974 Federal Register / Vol. 75, N