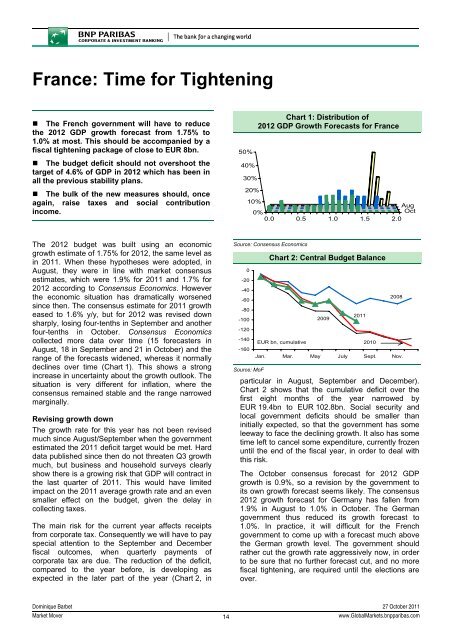

France: Time for Tightening• The French government will have to reducethe 2012 GDP growth forecast from 1.75% to1.0% at most. This should be accompanied by afiscal tightening package of close to EUR 8bn.• The budget deficit should not overshoot thetarget of 4.6% of GDP in 2012 which has been inall the previous stability plans.• The bulk of the new measures should, onceagain, raise taxes and social contributionincome.50%40%30%20%Chart 1: Distribution of2012 GDP Growth Forecasts for France10%Aug0%Oct0.0 0.5 1.0 1.5 2.0The 2012 budget was built using an economicgrowth estimate of 1.75% for 2012, the same level asin 2011. When these hypotheses were adopted, inAugust, they were in line with market consensusestimates, which were 1.9% for 2011 and 1.7% for2012 according to Consensus Economics. Howeverthe economic situation has dramatically worsenedsince then. The consensus estimate for 2011 growtheased to 1.6% y/y, but for 2012 was revised downsharply, losing four-tenths in September and anotherfour-tenths in October. Consensus Economicscollected more data over time (15 forecasters inAugust, 18 in September and 21 in October) and therange of the forecasts widened, whereas it normallydeclines over time (Chart 1). This shows a strongincrease in uncertainty about the growth outlook. Thesituation is very different for inflation, where theconsensus remained stable and the range narrowedmarginally.Revising growth downThe growth rate for this year has not been revisedmuch since August/September when the governmentestimated the 2011 deficit target would be met. Harddata published since then do not threaten Q3 growthmuch, but business and household surveys clearlyshow there is a growing risk that GDP will contract inthe last quarter of 2011. This would have limitedimpact on the 2011 average growth rate and an evensmaller effect on the budget, given the delay incollecting taxes.The main risk for the current year affects receiptsfrom corporate tax. Consequently we will have to payspecial attention to the September and Decemberfiscal outcomes, when quarterly payments ofcorporate tax are due. The reduction of the deficit,compared to the year before, is developing asexpected in the later part of the year (Chart 2, inSource: Consensus Economics0-20-40-60-80-100-120-140-160Source: MoFChart 2: Central Budget Balance20092011EUR bn, cumulative 20102008Jan. Mar. May July Sept. Nov.particular in August, September and December).Chart 2 shows that the cumulative deficit over thefirst eight months of the year narrowed byEUR 19.4bn to EUR 102.8bn. Social security andlocal government deficits should be smaller thaninitially expected, so that the government has someleeway to face the declining growth. It also has sometime left to cancel some expenditure, currently frozenuntil the end of the fiscal year, in order to deal withthis risk.The October consensus forecast for 2012 GDPgrowth is 0.9%, so a revision by the government toits own growth forecast seems likely. The consensus2012 growth forecast for Germany has fallen from1.9% in August to 1.0% in October. The Germangovernment thus reduced its growth forecast to1.0%. In practice, it will difficult for the Frenchgovernment to come up with a forecast much abovethe German growth level. The government shouldrather cut the growth rate aggressively now, in orderto be sure that no further forecast cut, and no morefiscal tightening, are required until the elections areover.Dominique Barbet 27 October 2011<strong>Market</strong> <strong>Mover</strong>14www.Global<strong>Market</strong>s.bnpparibas.com

In September, we estimated 2012 French growtharound 1.0% (see "French 2012 Deficit: In Control",in <strong>Market</strong> <strong>Mover</strong>, 29 September 2011). We also saidthen the government would not only have to reduceits growth forecast, but would also have to implementnew austerity measures to keep the deficit, as ashare of GDP, at the same level. We estimated thenthat around EUR 8bn of new measures would berequired. At present the risks to our growth forecastare on the downside.The measures to stabilise the deficitConsensus Economics also shows that, despite thelower growth, the deficit forecast remained extremelyflat (Chart 3). Economists clearly share our view thatthe government will toughen its fiscal policy to copewith slower growth, as the president and governmentmembers have already said loud and clear. Thisbudgetary policy may also explain why lower growth,which goes hand in hand with a higherunemployment rate forecast and lower wageincrease expectations, does not result in modificationof the inflation forecast. Most analysts probablyexpect fiscal measures to push prices a little higher.However, we can't say whether this refers to thefiscal measures already announced late August andin the draft budget late September, or whetheranalysts expect more adverse fiscal news in thefuture.The government has already announced the easiestand most obvious measures, so the new austeritypackage will be more difficult to put together. Thefact that 2012 is the main election year naturallycomplicates the decision-making process. Thepolitical factor is the main reason we are notexpecting a hike in VAT, although this wouldgenerate the highest income gain (theoreticallyEUR 6bn for 1pp hike in the standard rate andEUR 3bn for the same increase in the reduced rate).A VAT hike, six months before the elections, wouldbe very risky politically. The election factor also limitsthe potential for further indirect tax hikes onconsumption.Opinion polls also indicate that people are lesswilling to accept spending cuts than tax hikes;probably because most people also want tax rises tohit the wealthy, i.e. not them. Potential savings onspending are limited, and these should be usedpreferably around year-end as a last minute lifeline incase of unexpected bad news at that time.We believe the bulk of fiscal tightening will, onceagain, come from a reduction in breaks on taxes andsocial charges (known as "niches fiscales etsociales"). An interesting insight of what could beannounced is provided by the MoF report, prepared1.91.71.51.31.10.90.7Chart 3: Major Consensus Forecastsfor France in 2012 (mean)15 forecasters 18 forecasters 21 forecastersAugust September OctoberSource: Consensus EconomicsCPI (% y/y)GDP (% y/y)Budget Def(% of GDP, RHS)in June 2011, which analysed 385 different schemes,amounting to a total of EUR 96bn. The report gaveeach of them an efficiency (or inefficiency) rating(see "France: The Deficit Target is the Priority", in<strong>Market</strong> <strong>Mover</strong>, 1 September 2011). As much asEUR 10.7bn of the tax breaks were deemedeconomically inefficient and another EUR 27.1bnwere not efficient enough.A large part (EUR 9.8bn) of the least effectivemeasures affect income tax: a modification decidednow would only affect 2013 fiscal income, not the2012 fiscal year. Some of the least efficientmeasures were already reduced or cancelled earlierthis year. Consequently the main source of incomefor 2012 lies with social contributions. The reportmentions EUR 3.1bn of inefficient cuts in socialcontribution and another EUR 9.4bn have a poorefficiency rating. This is where the bulk of theausterity measures can be found.Asset salesThe government may also be willing to increaseasset sales, although the financial context does notlook favourable for restarting the privatisationprogramme. However, the government may try to sellreal estate, buildings and land, since these priceshave not declined much. More immaterial assetsmay also be sold; the current budget includes theproceeds of the sale of radio bands for mobilephones.Since August, the tax increases already announcedamount to EUR 10.5bn or 0.5% of GDP. Another0.3pp to 0.4pp should be presented by the year-end.Given the measures announced in 2010, for thefiscal year 2012, the total tightening from incomeshould reach 1.0pp of GDP. Expenditure restraintswould also reduce the structural deficit by about0.6pp of GDP. With low growth mechanically adding0.5% to the deficit, the 2012 initial target of 4.6% ofGDP should be respected.5.45.25.04.84.64.44.2Dominique Barbet 27 October 2011<strong>Market</strong> <strong>Mover</strong>15www.Global<strong>Market</strong>s.bnpparibas.com