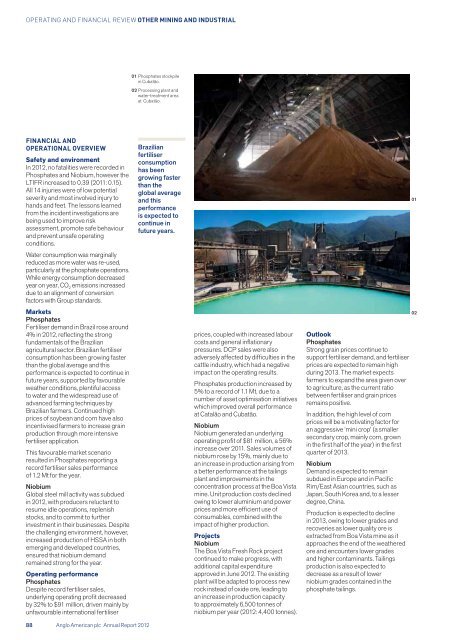

OPERATING AND FINANCIAL REVIEW OTHER MINING AND INDUSTRIAL01 Phosphates stockpilein Cubatão.02 Processing plant andwater-treatment areaat Cubatão.FINANCIAL ANDOPERATIONAL OVERVIEWSafety and environmentIn <strong>2012</strong>, no fatalities were recorded inPhosphates and Niobium, however theLTIFR increased to 0.39 (2011: 0.15).All 14 injuries were of low potentialseverity and most involved injury tohands and feet. The lessons learnedfrom the incident investigations arebeing used to improve riskassessment, promote safe behaviourand prevent unsafe operatingconditions.Water consumption was marginallyreduced as more water was re-used,particularly at the phosphate operations.While energy consumption decreasedyear on year, CO 2 emissions increaseddue to an alignment of conversionfactors with Group standards.MarketsPhosphatesFertiliser demand in Brazil rose around4% in <strong>2012</strong>, reflecting the strongfundamentals of the Brazilianagricultural sector. Brazilian fertiliserconsumption has been growing fasterthan the global average and thisperformance is expected to continue infuture years, supported by favourableweather conditions, plentiful accessto water and the widespread use ofadvanced farming techniques byBrazilian farmers. Continued highprices of soybean and corn have alsoincentivised farmers to increase grainproduction through more intensivefertiliser application.This favourable market scenarioresulted in Phosphates reporting arecord fertiliser sales performanceof 1.2 Mt for the year.NiobiumGlobal steel mill activity was subduedin <strong>2012</strong>, with producers reluctant toresume idle operations, replenishstocks, and to commit to furtherinvestment in their businesses. Despitethe challenging environment, however,increased production of HSSA in bothemerging and developed countries,ensured that niobium demandremained strong for the year.Operating performancePhosphatesDespite record fertiliser sales,underlying operating profit decreasedby 32% to $91 million, driven mainly byunfavourable international fertiliserBrazilianfertiliserconsumptionhas beengrowing fasterthan theglobal averageand thisperformanceis expected tocontinue infuture years.prices, coupled with increased labourcosts and general inflationarypressures. DCP sales were alsoadversely affected by difficulties in thecattle industry, which had a negativeimpact on the operating results.Phosphates production increased by5% to a record of 1.1 Mt, due to anumber of asset optimisation initiativeswhich improved overall performanceat Catalão and Cubatão.NiobiumNiobium generated an underlyingoperating profit of $81 million, a 56%increase over 2011. Sales volumes ofniobium rose by 15%, mainly due toan increase in production arising froma better performance at the tailingsplant and improvements in theconcentration process at the Boa Vistamine. Unit production costs declinedowing to lower aluminium and powerprices and more efficient use ofconsumables, combined with theimpact of higher production.ProjectsNiobiumThe Boa Vista Fresh Rock projectcontinued to make progress, withadditional capital expenditureapproved in June <strong>2012</strong>. The existingplant will be adapted to process newrock instead of oxide ore, leading toan increase in production capacityto approximately 6,500 tonnes ofniobium per year (<strong>2012</strong>: 4,400 tonnes).OutlookPhosphatesStrong grain prices continue tosupport fertiliser demand, and fertiliserprices are expected to remain highduring 2013. The market expectsfarmers to expand the area given overto agriculture, as the current ratiobetween fertiliser and grain pricesremains positive.In addition, the high level of cornprices will be a motivating factor foran aggressive ‘mini crop’ (a smallersecondary crop, mainly corn, grownin the first half of the year) in the firstquarter of 2013.NiobiumDemand is expected to remainsubdued in Europe and in PacificRim/East Asian countries, such asJapan, South Korea and, to a lesserdegree, China.Production is expected to declinein 2013, owing to lower grades andrecoveries as lower quality ore isextracted from Boa Vista mine as itapproaches the end of the weatheredore and encounters lower gradesand higher contaminants. Tailingsproduction is also expected todecrease as a result of lowerniobium grades contained in thephosphate tailings.010288 <strong>Anglo</strong> <strong>American</strong> plc <strong>Annual</strong> <strong>Report</strong> <strong>2012</strong>

AMAPÁAmapá generated an underlyingoperating profit of $54 million,a decrease of $66 million on theprior year.Production increased significantly,in line with planned ramp up andalso due to higher mass recovery inthe beneficiation plant as a result ofthe plant’s improved stability. Theoperation is now at design productioncapacity. Higher sales were alsoachieved following fewer delaysassociated with transportable moisturelimits. Transhipment at Trinidad andTobago from smaller capacityHandymax to the larger capacityCapesize vessels for onward shipmentto the Middle and Far East wassuccessfully implemented in thesecond half of <strong>2012</strong>.The favourable impact of improvedproduction and higher sales, however,was more than offset by a sharpdecrease in prices during <strong>2012</strong>, thoughtight cost control and improvedoperating efficiencies, partlycompensated their effect. Underlyingoperating profit also benefited fromthe reversal of penalty provisions,which were in place at the end of 2011,as a result of contract renegotiations.Regrettably, one fatality occurredat Amapá iron ore system in Brazilduring <strong>2012</strong>. The LTIFR hasimproved over the past six years,and encouragingly, the severity ofinjuries also continues to decline.On 4 January 2013, <strong>Anglo</strong> <strong>American</strong>announced an agreement to sell its70% interest in Amapá to ZaminFerrous Ltd. The transaction is subjectto regulatory approval and is expectedto complete in 2013. We have alwaysmaintained that we did not envisageholding our interest in Amapá over thelong term and, in July <strong>2012</strong>, reportedthat we had transferred responsibilityfor Amapá to our Other Mining andIndustrial business unit and stated thatwe were exploring the possibility ofdivesting our interest.<strong>Anglo</strong> <strong>American</strong> has transformed theoperational performance of Amapásince acquisition in 2008, increasingannual production from 1.2 Mt in 2008to 6.1 Mt in <strong>2012</strong>.TARMACTarmac reported an underlyingoperating profit of $73 million,compared with a loss of $38 millionin 2011. Tarmac’s underlying EBITDAwas $148 million, 44% higher thanin 2011.Quarry materialsThe business’ profitability was athigher levels than last year, mainly asa result of the operation being treatedas ‘held for sale’ from the end of July<strong>2012</strong>, and the subsequent cessationof recorded depreciation. There hasbeen a decline in asphalt volumes, withfew major road schemes commencingin <strong>2012</strong> as a result of the UKgovernment’s austerity measures.Private-sector growth remainedmuted throughout the year, thuskeeping pressure on ready-mixconcrete prices and volumes, but wasoffset in part by the resilient centralLondon market. A continued focuson maximising the use of substitutefuel and recycled asphalt materialsis helping to mitigate the impact ofrising hydrocarbon costs and tosupport margins.On 7 January 2013, <strong>Anglo</strong> <strong>American</strong>and Lafarge announced thecompletion of their 50:50 joint venturewhich will combine their cement,aggregates, ready-mix concrete,asphalt and asphalt surfacing,maintenance services, and wasteservices businesses in the UK. Thejoint venture will be known as LafargeTarmac. Completion of the LafargeTarmac joint venture followed finalclearance from the UK CompetitionCommission, predicated on thecompleted sale of a portfolio of Tarmacand Lafarge construction materialsoperations in the UK, which alsooccurred on 7 January 2013.Building productsPerformance was affected bythe continued general economicdownturn, compounded by disruptionto building activity followingunseasonal wet weather duringthe summer months.The weak building products marketresulted in a highly competitivepricing environment affecting salesvolumes, although cost reductionprojects and improvements inoperating efficiencies are helpingto mitigate some of the impact.In early 2013,<strong>Anglo</strong> <strong>American</strong>and Lafargeannouncedthe completionof their 50:50joint venture.A number of initiatives continue to bedeveloped to ensure improved longerterm performance, but the short termremains difficult owing to the prevailingweak market conditions.SCAW METALSScaw Metals experienced a 32%increase in underlying operating profitto $49 million for the 11 months toend November <strong>2012</strong> compared withthe full year 2011, mainly as a resultof the company being treated as‘held for sale’ from 24 April <strong>2012</strong>,and the subsequent cessation ofrecorded depreciation.Cast Products showed a markedimprovement, owing to firm demandacross all segments and a reductionin costs following the closure of aloss making foundry in the prior year.Grinding Media reported a decreasein underlying operating profit as aresult of lower demand from themining sector owing to industrialaction in the second half of <strong>2012</strong>.This business is expected to recoveras mining operations revert to fullproduction. The performance ofWire Rod Products suffered as aconsequence of a decline in miningactivity, but nevertheless reportedstable earnings. Demand forconstruction products remainedweak, but in spite of this the RolledProducts business, through costcontainment measures andoperational improvements, wasable to minimise its losses.Total production of steel productswas 611,600 tonnes for the 11 monthsto end November <strong>2012</strong>, a decreaseof 9.7% over the full year 2011.On 24 April <strong>2012</strong>, <strong>Anglo</strong> <strong>American</strong>announced the sale of its interestin Scaw South Africa to an investmentconsortium led by the IndustrialDevelopment Corporation ofSouth Africa and the Group’spartners in Scaw South Africa,being Izingwe Holdings (Pty)Limited, Shanduka Resources (Pty)Limited and the Southern PalaceGroup of Companies (Pty) Limited.On 23 November, the sale ofScaw South Africa and relatedcompanies completed for a totalconsideration of ZAR3.4 billion($440 million) on a cash- anddebt-free basis as announced.Operating and financial review<strong>Anglo</strong> <strong>American</strong> plc <strong>Annual</strong> <strong>Report</strong> <strong>2012</strong> 89

![English PDF [ 189KB ] - Anglo American](https://img.yumpu.com/50470814/1/184x260/english-pdf-189kb-anglo-american.jpg?quality=85)

![pdf [ 595KB ] - Anglo American](https://img.yumpu.com/49420483/1/184x260/pdf-595kb-anglo-american.jpg?quality=85)

![pdf [ 1.1MB ] - Anglo American](https://img.yumpu.com/49057963/1/190x240/pdf-11mb-anglo-american.jpg?quality=85)