INDIA'S NAPHTHA TRADE OUTLOOK - CMT Conferences

INDIA'S NAPHTHA TRADE OUTLOOK - CMT Conferences INDIA'S NAPHTHA TRADE OUTLOOK - CMT Conferences

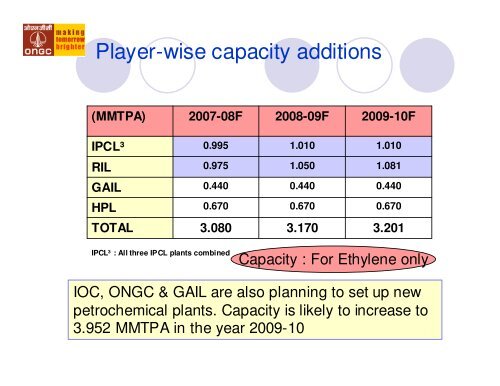

Player-wise capacity additions(MMTPA)2007-08F2008-09F2009-10FIPCL³0.9951.0101.010RIL0.9751.0501.081GAIL0.4400.4400.440HPL0.6700.6700.670TOTAL3.0803.1703.201IPCL³ : All three IPCL plants combinedCapacity : For Ethylene onlyIOC, ONGC & GAIL are also planning to set up newpetrochemical plants. Capacity is likely to increase to3.952 MMTPA in the year 2009-10

Production forecast(MMTPA)2006-07E2007-08F2008-09F2009-10FCAGREthylene2.8102.9613.5673.7498.1Propylene2.1342.2492.6692.7447.8hdPE1.2501.3001.5501.7488.0ldPE0.2050.2050.2050.2051.0lldPE0.5900.6100.7700.8388.0PP1.8001.9502.4002.5708.0

- Page 1 and 2: 6th Petchem Feedstock Asia/China Co

- Page 3 and 4: India’s Economic Scenario

- Page 5 and 6: Structure of India Economy5040Servi

- Page 7 and 8: India GDP (PPP)4.03.53.02.52.01.51.

- Page 9 and 10: Key Social and Economic Indicators2

- Page 11 and 12: Refinery Capacity (mmt)1998-991999-

- Page 13 and 14: INDIA’S PETROCHEMICALINDUSTRY

- Page 15 and 16: Petrochemical Industry Expansion !M

- Page 17 and 18: Ethylene Capacity today….HPL, Hal

- Page 19 and 20: Net trade position in petrochemical

- Page 21: Import - Export Scenario2005-06IMPO

- Page 25 and 26: Surplus / Deficit forecast(MMTPA)20

- Page 27 and 28: Ethylene Sectoral: Growth(KTPA)2004

- Page 29 and 30: hdPE Sectoral: Growth(KTPA)2004-052

- Page 31 and 32: Feedstock DetailsIn MMTPAIPCLBaroda

- Page 33 and 34: INDIA’S NAPHTHA TRADEOUTLOOK

- Page 35 and 36: Introduction Naphtha business is gl

- Page 37 and 38: Consumption(MMTPA)04-0505-0606-07EP

- Page 39 and 40: Sales to Fertilizer SectorFeedstock

- Page 41 and 42: Domestic Prices01-0202-0303-0404-05

- Page 43 and 44: DOMESTIC DEMAND

- Page 45 and 46: Overview of the Indian Economy Visi

- Page 47 and 48: Working Age Population747270IndiaCh

- Page 49 and 50: Retail On the Demand Front Brand co

- Page 51 and 52: Automobile India is a sourcing hub

- Page 53 and 54: ProductionMMTPA2006-07E2007-08F2008

- Page 55 and 56: Demand & Supply : Naphtha• From 2

- Page 57 and 58: Export The surplus production of Na

- Page 59 and 60: ExportDFRC:Through DFRC the Exporte

- Page 61 and 62: Naphtha Exports by PSUQty(MMT2002-0

- Page 63 and 64: Import Import of Naphtha is continu

- Page 65 and 66: Conclusion

- Page 67 and 68: Conclusion Naphtha consumption is i

Player-wise capacity additions(MMTPA)2007-08F2008-09F2009-10FIPCL³0.9951.0101.010RIL0.9751.0501.081GAIL0.4400.4400.440HPL0.6700.6700.670TOTAL3.0803.1703.201IPCL³ : All three IPCL plants combinedCapacity : For Ethylene onlyIOC, ONGC & GAIL are also planning to set up newpetrochemical plants. Capacity is likely to increase to3.952 MMTPA in the year 2009-10