Directors' Remuneration Report - Chemring Group PLC

Directors' Remuneration Report - Chemring Group PLC

Directors' Remuneration Report - Chemring Group PLC

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

4Business overview5Statement by the ChairmanThe <strong>Group</strong> has pursued a strategy of combiningsignificant organic growth from its existing businesseswith a successful programme of acquisitions which havecontributed further to the <strong>Group</strong>’s growth.Highlights• Revenue up 25% to £745.3 million• Underlying operating profit* up 3% to£141.8 million• Underlying profit before tax* up 6% to£125.6 million• Underlying earnings per share* up 5%at 52.1p• Profit before tax £90.8 million• Basic earnings per share 39.8p• Total dividend per share for the year up25% at 14.8pKey informationUnderlying profit before tax*£125.6m+6%Underlying earnings per share*52.1p+5%Dividend per ordinary share14.8p+25%* Before non-underlying items (see Note 6)<strong>Chemring</strong> produced another year of growthin profits and earnings, although both wereaffected in the last month by a slippage ofdeliveries into the current financial year.Revenue was £745.3 million, an increaseof 25%, and this generated an underlyingoperating profit* of £141.8 million, up 3%.Underlying profit before tax* increased by6% to £125.6 million, producing underlyingearnings per share* of 52.1p, 5% abovelast year. The Board is recommending afinal dividend of 10.8p per share whichwill provide a full year dividend of 14.8p,an increase of 25% over last year.The order intake for the <strong>Group</strong> was£819.1 million, which was slightly lowerthan last year. We saw strong order bookgrowth in our Counter-IED and Munitionsbusinesses, which was offset by a downturnin orders received in the Countermeasuresand Pyrotechnics divisions. These twodivisions suffered from reduced customerdemand, which was driven, in the main,by government fiscal and budgetarycontrols. The closing order book reached£878.3 million, which was 9% above last year.In July the <strong>Group</strong> acquired the DetectionSystems business of General DynamicsArmament and Technical Products for atotal cash consideration of £56.1 million.The business, which is now operating as<strong>Chemring</strong> Detection Systems, Inc., is a USleader in chemical and biological threatdetection and has an advanced capability instand-off detection of improvised explosivedevices. The acquisition greatly enhancesthe capabilities of our Counter-IED division,and has already made a good contributionto the <strong>Group</strong>’s earnings.Balance sheet, cash flow and debtThe <strong>Group</strong> generated an underlyingoperating cash flow* of £124.6 million,which was 88% of underlying operatingprofit*. At the end of the year, net debtwas £262.7 million compared with£307.5 million last year.In April 2011, approximately £112 millionof new equity was raised in order to fundtwo potential acquisitions. We went aheadwith the purchase of <strong>Chemring</strong> DetectionSystems but did not, in the end, proceedwith the other potential opportunity, asfurther investigation indicated that it wouldnot generate sufficient value. In the lightof this, the Board has reviewed the balancesheet to determine the appropriate levelsof debt and gearing for the <strong>Group</strong> in thefuture. We have taken a cautious view in thelight of the world’s economic and financialuncertainties and will continue reducingdebt levels when appropriate. However, wehave also concluded that we should considerreturning surplus capital to shareholderswhilst maintaining the strength of thebalance sheet. Accordingly, we will seekapproval at the forthcoming Annual GeneralMeeting to renew our authority to buy backshares, when it is considered appropriate,over the course of the next year. We wouldonly expect to exercise this authority for abuyback of up to £50 million of shares.The Board also considered its long termdividend policy as part of this balance sheetreview. For many years, the <strong>Group</strong> hasadopted a policy of maintaining dividendcover at around four times. With our strongannual cash generation, we believe it wouldbe appropriate to reduce the cover to threetimes over the next year. As part of thismove, the proposed total dividend for 2011will be covered 3.5 times by underlying aftertax earnings*, compared with 4.2 timeslast year.<strong>Group</strong> strategyOver a number of years, the <strong>Group</strong>has pursued a strategy of combiningsignificant organic growth from its existingbusinesses with a successful programme ofacquisitions which have contributed furtherto the <strong>Group</strong>’s growth. This has enabled usto develop new products and technologies,and utilise our market positions to exploitopportunities. The acquisitions haveusually been relatively modest in size,but have demonstrated a strong potentialfor expansion. Whilst there are noneplanned at the current time, we operate inmarkets where consolidation may becomeattractive, and we will therefore continueto consider opportunities when they ariseand pursue them only if there is a clearopportunity to enhance shareholder value.We see long term growth coming from ourexisting businesses but there will be timeswhen acquisitions may be appropriate tosupplement and enhance our portfolio.Board of directorsDuring the year, there have been somechanges in the composition of the Board.Two new directors were appointed during2011. Sarah Ellard, who has been headof the <strong>Group</strong>’s legal affairs for fourteenyears, joined the Board in October asLegal Director. On 1 November 2011,Vanda Murray, who has a number ofnon-executive appointments, was appointedto the Board as a non-executive director.I welcome them both to the Board.David Evans, who has been a director since1988, first as Chief Executive and for thelast seven years as a non-executive director,has indicated his intention to retire fromthe Board at the Annual General Meetingin March. During his time with the <strong>Group</strong>,David has made a major contribution to itsdevelopment, and I would like to take theopportunity to thank him on behalf of theBoard and wish him well in the future.DividendsIn line with the revised long term dividendpolicy outlined above, the Board isrecommending a final dividend for theyear of 10.8p (2010: 8.4p). With the interimdividend paid of 4p (2010: 3.4p), this gives atotal dividend for 2011 of 14.8p (2010: 11.8p),an increase of 25%. The dividend is covered3.5 times by underlying after tax earnings*,and with a solid balance sheet and cashflow, the <strong>Group</strong> remains well positioned toincrease its return to shareholders.ProspectsDuring the last year, many governmentshave struggled with increasing deficits andlower economic growth. This has affecteddefence procurement, leading to volumereductions and delays. The continuingproblems of the Eurozone and the impactof possible sequestration in the US indicatethat our traditional markets will not be anyeasier this year. We continue to pursueour policy of reducing our dependence onthese markets, and will actively seek morebusiness from elsewhere. It is encouragingto note that 44% of today’s order bookemanates from these non-NATO markets,compared with 33% at the same timelast year. We see further good growthprospects in these markets and will pursuethe opportunities they offer. I am confidentthat we have the products, the managementand technological skills to achieve ourobjectives and provide the foundation forsteady growth.P C F HicksonChairman24 January 2012Business overview Corporate governance Financial statements Other information<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011

8Business overview9Review by the Chief ExecutivecontinuedI would like to extend my personal thanks to allmembers of staff for their personal achievementsand hard work during the year.AcquisitionsThe <strong>Group</strong> made only one acquisition duringthe year. In July 2011, the <strong>Group</strong> completedthe acquisition of the Detection Systemsoperations and certain related assets ofGeneral Dynamics Armament and TechnicalProducts, a subsidiary of General DynamicsCorporation, for a cash consideration of$90 million (£56 million).The business, now renamed <strong>Chemring</strong>Detection Systems, Inc. (CDS), is based inCharlotte, North Carolina. It is a US leaderin chemical and biological threat detectionand has advanced capability in the stand-offdetection of improvised explosive devices.CDS is the incumbent supplier for two majorUS military vehicle-mounted detectionprogrammes: the Joint Biological PointDetection System (JBPDS) and the JointService Lightweight Stand-off ChemicalAgent Detector (JSLSCAD). In addition,its products include a stand-off IED andexplosives detector and the Juno hand-heldchemical detector.The acquisition substantially enhancesour Counter-IED business activities withleading-edge US technology for biological,chemical and stand-off explosive detection.It provides a complementary capabilityto our existing subsidiaries, NIITEK and<strong>Chemring</strong> EOD, and will help us expand ourgrowing global market position.During the summer, we were in discussionswith a third party regarding a significantacquisition that would have made a majorimpact to our market position. However,the restructuring required to deliver thefull benefit was considerable, and wefelt that the vendor’s valuation of thebusiness was too high. Although we are nolonger pursuing this opportunity, the corestrategy of the <strong>Group</strong> remains focused onorganic growth that is augmented by smallbolt-on acquisitions.ElectronicsIn line with the <strong>Group</strong>’s strategy, electronics,including electronic countermeasuresand IED detection systems, is of growingimportance across our four marketsegments. With the acquisition of <strong>Chemring</strong>Detection Systems and Roke, we havesignificantly enhanced our capabilities in<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011electronic systems design, development andintegration. In 2011, electronics contributed40% of the <strong>Group</strong> revenue, and this isexpected to grow to 50% over the next fiveyears. These electronic capabilities are infive niche areas:• Initiation – delays, sequencing andsafety/arming• Detection – radar and infra-redstand-off technologies• Electronic warfare – interception ofcommunications and electronic attack• Electronic countermeasures – activejamming systems• Network protection – legal interceptand anomaly detectionRoke has become a strategic Europeancentre-of-excellence for product andtechnology development of electronicsystems. It is heavily engaged in the systemengineering and software development ofour CENTURION countermeasure launcher;it is designing low-cost, active-jammingtechnology for our air and naval expendablemarkets; and it has completed the design ofour new SPLINTER hand-held mine detector.In 2011, Roke was given the QueensAward for Innovation for its RESOLVEmodular, man-portable, electronicwarfare system for the exploitation andsuppression of hostile communicationequipment. RESOLVE is now in service withthe UK Ministry of Defence and a numberof customers in the global export market.Roke has produced and demonstrated avehicle-mounted RESOLVE capability, andthere is strong interest from Europe and theMiddle East in vehicle-mounted surveillancesystems for dedicated electronicsurveillance applications.Research and developmentOur strategy for future growth continues torely on technology leadership and the rapiddevelopment of new products that meetthe changing needs of our customers anddisplace those of our competitors. Our totalexpenditure on research and developmentgrew by 74% to £59.6 million, whichrepresents 8% of the total <strong>Group</strong> revenue.Internally-funded research and developmentgrew by 56% to £21.2 million, reflecting thestrategic emphasis we continue to placeon product innovation. Our long-termpartnership with Cranfield Universitycontinues to expand, and we now havesixteen programmes running across areas ofinterest relevant to all four of our divisions.Roke now represents our largestconcentration of research and developmentexpenditure, with around 50% of the totalfunding directed at electronic rather thanenergetic products and technology.Capital investmentCapital investment in the year grew by 19%to £48.6 million, which represents nearly7% of <strong>Group</strong> revenue. £19.7 million of theinvestment relates to the continuing buildof the new countermeasures manufacturingfacilities at Salisbury in the UK and at Larain Australia. The UK facility has not yetbeen completed and has been delayed bytechnical issues with the safety criticalsoftware. These have recently beenresolved, and initial production is scheduledfor the end of 2012. Better progress hasbeen made on the facility in Australia, andthe first locally manufactured flares wereproduced in 2011. Low rate initial productionis scheduled for March 2012, but it will takeat least another six months to work up tofull volume manufacture.A second principal area of investmentwas associated with the developmentof our <strong>Chemring</strong> Energetics facility inScotland, where we spent £4.7 millionon the completion of four facilities:the primary explosives facility for themanufacture of detonators and initiators;the plastic explosives pressing facility forthe manufacture of demolition stores;the Meccanite expansion facility for themanufacture of propellants; and the highexplosive pressing facility for warheadmanufacture. All of these facilities providenew manufacturing capabilities to the siteand the capacity to meet the substantialgrowth in revenue that is expected inthe future.Staff and employeesAt the end of 2011, the <strong>Group</strong> employed atotal of 4,679 people, 396 (9%) higher thanthe previous year end, although 109 of themwere associated with our latest acquisition,<strong>Chemring</strong> Detection Systems. In addition,the year end figure included a significantnumber of short-term contractors engagedwithin our UK operations during the lastquarter of the financial year. Excludingthese contractors reduces the year-on-yeargrowth to around 4%. 1,798 employees(38%) are located within the UK and 2,047employees (44%) are located in the US.I would like to extend my personal thanksto all members of staff for their personalachievements and hard work during theyear. The Board understands how importantour employees are to the success of thisfast-changing business.Future prospectsMarket conditionsDuring 2011, the defence market facedgreater uncertainty than in previousyears, with the Eurozone crisis andEuropean government deficit reductionprogrammes continuing to have anegative impact on defence budgets.Most of our European customers continueto delay their annual procurements bysix months, and are looking for reducedvolumes of consumables to save money.The UK Ministry of Defence, in particular,has substantially reduced its procurementof flares and decoys for the protection ofhelicopters and transport aircraft.The UK defence market continues to bechallenging, with a contracting budget,significant changes to procurementstructures, and substantial reductionsin personnel. The impact of last year’sStrategic Defence & Security Review hasgradually become clear but the structuralreforms proposed by Lord Levene are onlyjust starting to get underway. Of particularimportance to the defence industry is therestructuring of the acquisition organisation,which may cause a significant disruption tothe future procurement process whilst it isbeing implemented. A number of options forreform have been submitted to Ministers buta decision is unlikely to be announced untilthe middle of 2012.However, it is the US market that has beenfar more challenging during the past year.No agreement was reached between thePresident and Congress on the size andconstitution of the FY2011 budget, andContinuing Resolution funding of theUS government continued all the waythrough the first half of our financial year.This mechanism maintains the funding forthe government employees but prohibitsnew programme starts or increases infunding compared to the previous year.The Pentagon was hesitant to release fundsfor procurement until the full year budgetwas known, as they were concerned aboutthe number of programmes that would haveto be adjusted. The majority of our annualcontracts were delayed into the secondhalf of the year, reducing the opportunityfor early deliveries from these contracts.Revenues from our US businesses were,therefore, heavily second-half weightedand greatly increased the risk of slippageinto 2012.The US government started its 2012financial year with further ContinuingResolutions, and there was a real threatthat a twelve month Continuing Resolutionmight be adopted. This would have had asignificant effect on the timing of annualcontract placement, resulting in a strongerthan usual second-half bias to our revenues,and a risk that sales would slip past October2012. However, in late December, the USFY2012 base defence budget was approvedat $520 billion, and the Overseas ContingentOperations (OCO) budget, which fundspeacekeeping operations in Afghanistan,was set at $115 billion. The funding containsa substantial year-on-year reduction inexpendable countermeasures that willaffect the <strong>Group</strong>, but this appears to beoffset by opportunities in counter-IEDand chemical/biological threat detection,and by strong growth in importantniche product areas, such as demolitionstores, pyrotechnics and mediumcalibre ammunition.Details of the US FY2013 budgetshould be announced in February 2012.US Department of Defense guidance hasfocused on a base budget of $523 billionand OCO funding of $83 billion, which isa 5% reduction on this year. However,President Obama recently announced thathe was looking for $263 billion of cutsover the next five years against the FY20111World Economic Outlook, September 2011 published by the International Monetary Fundbaseline, which equates to a base budget of$517 billion. If implemented, the US budgetwill reduce by 6% in FY2013 and thenreturn to slow growth of a few per cent eachyear thereafter.However, the 2011 Budget Control Act,passed in the US in August 2011, containsa “sequestration” clause that willautomatically reduce US defence spendingby a further $54.7 billion per year andthreatens to reduce the FY2013 base budgetto $465 billion. This will be very difficult toachieve without cancellation of importantmajor programmes and may lead to seriouscutbacks in all aspects of procurement.Although Congress has started to makeplans to repeal the sequestration clause,the President has threatened to vetoany attempts by Congress to blockthe automatic spending cuts. There is,therefore, considerable continuinguncertainty about the US market.Non-NATO markets, on the other hand,remain buoyant with more attractiveeconomic growth rates and lower fiscaldeficits. The International MonetaryFund 1 forecasts that real Gross DomesticProduct in India/Asia will grow by 7.5%,Latin America by 3.9% and in the MiddleEast by 3.6%. Defence spending in theseregions continues to strengthen andthey represent a very attractive marketfor the <strong>Group</strong>. Customers are looking toupgrade their products to near-NATOstandards, to develop local manufacturing,and to eventually develop an indigenousdesign capability. The <strong>Group</strong> is findingconsiderable opportunities in all four ofour market segments, but the specialistcapabilities that we have in direct fireammunition, in particular, are proving tobe a significant attraction.Counter-IEDOur HMDS ground penetrating radarcontinues to operate successfully duringcounter-IED operations in Afghanistan andhas saved the lives of many US and coalitionsoldiers. During 2011, NIITEK delivered77 HMDS systems to the US Army takingthe number of systems supplied to over240. Negotiations with the US Army for amulti-year sustainment contract, coveringsystems, spares and support and potentially<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011Business overview Corporate governance Financial statements Other information

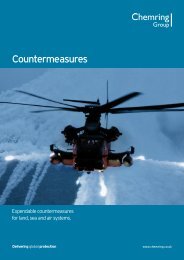

10Business overview11Review by the Chief ExecutivecontinuedThe Board anticipates that organic growth willcontinue at a similar rate to that achieved in 2011.worth in excess of $500 million, has beenunderway for many months, and thecontract is expected to be received by theend of the second quarter. This will supportthe operation of the HMDS fleet untilwithdrawal from Afghanistan in 2015.Good progress has also been made indeveloping the export market for HMDS.Agreement has been reached with MBDAItaly to provide the Italian Army with amodified ground penetrating radar systemto go on the Calife pushed trailer and theIVECO VTMM multi-role tactical vehicle.Full development will be completed in 2012and production is expected in 2012 and2013. The Australian Defence Force hasalso selected HMDS for its counter-IEDoperations, and is looking to procuresystems through the US Foreign MilitarySales channels.The US Army’s acquisition of anext-generation IED detection system,involving more advanced multi-sensortechnology and data fusion, will probablytake place in 2013, and they have confirmedthat they expect to purchase in excess of500 systems over a five year period.In 2012, the US Army will take the Milestone Cdecision to start full rate productionof the nuclear, biological and chemicalreconnaissance vehicle – Stryker Suite. Anadditional 100 vehicles will be built in 2012and a further 50 in 2013. This will boostdemand for both the biological (JBPDS)and chemical detection systems (JSLSCAD)supplied by our new subsidiary, <strong>Chemring</strong>Detection Systems, and will generate goodgrowth over the next few years.The <strong>Group</strong> has also continued work on acustomer-funded development programmefor stand-off explosives detection. Threesystems were manufactured and deliveredfor early user testing during 2011. Additionalwork is expected in 2012 to continue earlyuser testing, to complete a productionreadiness phase of the current generationsystem, and to work on a next generationsystem for vehicle-mounted applicationswith on-the-move capability.The qualification of our range of insensitivedemolition stores is making good progress,and considerable export interest has beengenerated, both within and outside NATO,by our SABREX flexible linear cuttingcharge. The global market for productsused to “defeat” the threat remainssteady at £300 million, and representsan important area for future growth. Theaward of the multi-year APOBS contract to<strong>Chemring</strong> Ordnance by the US Army wasa strong endorsement of the investmentin technology and facilities. Technologytransfer of our next generation demolitionstores to the US should help capture asizable share of the global market.The order book for our Counter-IED divisionwas £127.1 million at the end of the year,28% higher than the previous year.The growth has been driven by the APOBScontract. The HMDS multi-year sustainmentcontract has taken many months tonegotiate, and the delay is reflected in thereducing order book. The delayed timingof the new contract will impact revenuesat NIITEK in 2012. However, revenue from<strong>Chemring</strong> Detection Systems will offset thisreduction, and overall, the Board expectsgood growth from this segment in 2012.CountermeasuresIn Afghanistan, the total NATO deploymentis still 130,000 troops. However, coalitionforces have announced their intention towithdraw their troops by 2015, starting witha reduction of nearly 40,000 by the end of2012. In anticipation of this withdrawal and,under pressure from budget constraints,most of our customers have cut backsignificantly on the purchase of flaresand decoys needed for the protectionof helicopters and transport aircraft. Acombination of reductions in the volumesordered and delays in order placement isquickly reducing the current stock piles.Further reductions are anticipated in 2012,which will take production on some decoysdown to a minimum sustainable level.The major growth in expendablecountermeasures over the next five yearswill, however, be associated with thesupply of flares and countermeasures toprotect fast jets. These are principallyused in operations against sophisticatedopponents, where war stocks need to be inplace for high volume usage during intensebattle conditions. Two aircraft, Typhoonand the F-35 Joint Strike Fighter (JSF), willdominate the market over the next ten tofifteen year period. A technical problemwith the dispenser, manufactured by athird party, has delayed volume productionof the Typhoon units, and we are still inlow rate initial production with the JSFflare set. With the approval of the USgovernment, <strong>Chemring</strong> Australia has beenidentified as a second source supplier forJSF countermeasures and, after the USDepartment of Defense qualifies productionin Australia, will compete with Kilgore for ashare of the long-term production.Another major area of growth over thenext few years is naval countermeasures.These are designed to protect shipsagainst incoming missiles, particularly incircumstances when rapid-fire gun systemscannot be used, such as in shallow waternext to other friendly vessels. During 2011,the <strong>Group</strong> completed development of arange of new payloads to meet the changingthreat and is now starting to manufacturethese next generation products. The <strong>Group</strong>has also purchased, from Lockheed Martin,the manufacturing assets and intellectualproperty for certain legacy US navalrounds. Our new designs and the detailedknowledge of current US in-service roundswill position us strongly for a new US Navyprocurement programme which will runfrom 2013 onwards.The <strong>Group</strong> has also made good progressin the development of its new trainablelauncher system, Centurion. A series ofland-based firing demonstrations weresuccessfully undertaken last year, anda fully operational prototype is now inmanufacture. Discussions with the RoyalNavy on sea trials are underway, and theItalian Navy has recently expressed stronginterest in undertaking an extended seatrial of the system on one of their SanAntonio Landing Platform Dock vessels.Considerable interest has been shown bya number of US, Middle East, Far East andSouth American customers.The order book for our Countermeasuresdivision decreased by 12% to £234.0 millionduring 2011. Although this is normally areliable lead indicator of trends over thenext twelve months, it does not take intoaccount the high level of backlog at Kilgoreor the delays in order placement caused bythe US government’s Continuing Resolutionfunding. Strong growth in deliveries ofdecoys for combat aircraft programmesare, therefore, expected to compensate forthe reduction in demand for those used onhelicopters and transport aircraft, and astable level of revenue can be expected forthis segment.PyrotechnicsThere continues to be strong interestin illuminating payloads for use inpeacekeeping operations. We havedeveloped a family of “white light” and“black light” payloads for the full range ofmortar calibres, large calibre ammunitionand for low signature, hand-held rocketsthat can be used by individual soldiers.These are all expected to enter into volumemanufacture during 2012 and 2013.We have also completed the initialdevelopment of a payload for thereplacement of white phosphorous insmoke/screening payloads. A 120mmspotting round has completed developmentand will be qualified by the US Army in 2012for sale to Middle East customers under theForeign Military Sales programme.The overall order book for the Pyrotechnicsdivision reduced by 16% to £145.5 million,with large reductions in the smoke,illumination and training parts of the market.However, the Pyrotechnics order book hasa much shorter coverage, and the openingorder book does not adequately characterisethe scale of in-for-out orders that make upthe full year performance. Lower demandfor training and aircraft safety productsis expected in 2012 but further growth inrevenues for smoke, illumination and spaceproducts means that revenues approaching2010 levels can be expected.MunitionsThe naval ammunition market continues togrow, principally driven by the number of76mm guns fitted to new naval ships. Thereis considerable interest in our products fromMiddle East and South American customers.A live-firing demonstration is planned inItaly to demonstrate its capability againstpirate boats or fast attack craft to a numberof Middle East customers.The Middle East and South America are alsogrowing markets for our 90mm, 105mm and115mm ammunition. In particular, the CMI90mm Mk8 gun is often fitted to the LAVsprevalent in these regions, and offers the<strong>Group</strong> a substantial opportunity to developnew customer relationships and markets.Discussions are also underway with theBrazilian government for the supply of90mm ammunition for the 400 new IVECOLAVs which they are planning to acquireover the next ten years.The <strong>Group</strong> is under contract with GeneralDynamics Land Systems, Canada for thesupply of vehicle-based 120mm mortarsystems for sale under a US Foreign MilitarySales programme. System deliverieswill commence in 2012 and will involveproduction testing by the US Army during2012 and 2013, using Mecar suppliedammunition. New inspection requirementsfrom the US government have delayedthe expected delivery programme and themajority of deliveries are now scheduledfor 2013. Annual ammunition contracts arethen expected.The order book for the Munitions divisiongrew by 39% to £371.7 million in 2011, withstrong growth in both the land and navalprime contract markets. Growth in 2012revenues is expected to be good, albeit ata lower rate than would be implied by theincrease in the opening order book.Non-NATO growthThe <strong>Group</strong> sells to a wide variety of militarycustomers in 80 countries around theworld. Over the last four years, revenuesfrom non-NATO customers have grownby 360% and now represent 29% ofthe <strong>Group</strong> revenue. Economic growthand lower fiscal deficits offer attractivemarkets for companies willing to quicklydevelop new products for their specificneeds, to establish local entities, transferthe technology for local manufacture, anddevelop over the long term the capabilityto incrementally upgrade products forthe future.We believe that we are well-positioned todevelop our non-NATO business to 40%of <strong>Group</strong> revenue over the next five to tenyears. Our niche ammunition products haveprovided the foundation for negotiations ina number of countries but interest is alsohigh in our countermeasures, counter-IEDand electronics technologies.During 2011, we announced that we hadreached agreement with the Hinduja <strong>Group</strong>to form a joint venture in India. Initially,the focus has been on a marketing jointventure, which will be pursuing a number ofmajor opportunities during 2012. However,we expect to obtain Indian governmentapproval for a defence manufacturing jointventure in due course, which will addressthe full range of the <strong>Group</strong>’s products andtechnologies. Similar discussions withpotential joint venture partners are takingplace in Saudi Arabia and Brazil, and the<strong>Group</strong> expects to announce more detailedinformation later in the year.OutlookOver the next two years, the NATO marketwill face considerable uncertainties andrevenues will be constrained by governmentdeficit reduction actions. Non-NATOmarkets, on the other hand, still offer goodgrowth prospects but the timescales forsuccessful implementation often take sometime. Over the short term, therefore, theBoard anticipates that organic growth willcontinue at a similar rate to that achievedin 2011.In the medium term, there are goodopportunities in all four of our businesssegments. The <strong>Group</strong> focuses on shortterm developments of products thatmatch important and constantly changingcustomer needs. This agility and its widebreadth of technology allows the <strong>Group</strong> totarget a number of well-funded, specialistniches and growth in market share at theexpense of weaker competitors.D J PriceChief Executive24 January 2012Business overview Corporate governance Financial statements Other information<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011

12Business overview13Our strategyOur strategy is to develop and build on ourcore competencies in energetic materials andelectronics for sensors, electronic warfareand network protection.VisionOur vision is to be the leading producer ofprotection systems and energetic productsfor the global defence marketCounter-IEDEstablish technologyleadership• Become the world leader inIED, chemical and biologicalthreat detection• Maintain technological leadin ground penetrating radarand counter-IED jamming• Become world leader inIED neutralisation anddemolition storesPyrotechnicsDisplace weak competitors• Establish undisputedworld lead• Develop new products totransform user operationsEstablishtechnologyleadershipCounter-IEDMaintainmarketshareCountermeasuresCountermeasures<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011Maintain market share• Exploit lead in specialmaterial, spectral andthrusted flares• Develop a market lead innaval launchers and decoys• Become the worldleader in dismountedand vehicle electronicwarfare equipment• Establish niche positionin network protectionMunitionsDevelop niche prime position• Become a leading primecontractor for non-NATO• Become a supplier ofchoice for NATO primesDisplaceweakcompetitorsPyrotechnicsDevelopniche primepositionsMunitions<strong>Group</strong> strategyThe <strong>Group</strong> strategy is focused on our four market segments –Counter-IED, Countermeasures, Pyrotechnics and Munitions.With the growing importance of electronics throughout ourbusiness, our future vision statement includes a broader definitionof “protection systems”, including electronic countermeasuresand IED detection systems.Our core strategy over the next five years is to develop and buildon our key core competencies:• Energetic materials – We will focus on products where we canexploit our extensive knowledge and expertise in explosive,pyrotechnic and pyrophoric materials. We will addressniche, highly profitable markets with significant value-addedmanufacture/assembly where barriers to entry are high. We willexploit the commonality of technology and design expertise togenerate a broad centre-of-expertise that can be maintainedover the long-term future.• Electronics for sensors, electronic warfare and networkprotection – A growing proportion of our business will bebased on high integrity, high-speed electronics for detectingand analysing threats as well as enabling a timely response.Many of these electronic systems will be network-based.Organic strategyOur organic growth strategy is based on two elements:• Geographic expansion outside NATO• New product developmentOur geographic strategy is to establish a strong localmanufacturing presence in the world’s leading defence spendingcountries and to export vigorously around the world. We havebusinesses in the US and Europe’s top five spending countries(UK, Germany, France, Italy and Spain), and export to over 80countries around the world. As the emphasis of global defencespending migrates from NATO to the Middle East, Far East andSouth America, we will develop our presence in these regions.We are in the process of establishing joint ventures in India,Saudi Arabia and Brazil.Top 15 defence spending countries$ billion150100500698Joint venture targetsUSAChinaUKFranceRussiaJapanSaudi ArabiaGermanyIndiaItalyBrazilSouth KoreaAustraliaCanadaTurkeySecondly, we will maintain a strong focus on developingworld-leading products. As a growing proportion of our businessis based on advanced electronics, we have developed parallelenergetics and electronics technology strategies.Our energetics technology strategy is focused on materialstechnology and applications engineering in five key areas:• Explosive materials – We will develop and optimise materialformulations to improve their performance and safety.• Warheads – We will build a lead in missile warheads and will offerinsensitive munitions (IM) variants of our ammunition products.• Propellants – We will develop a new generation of lowvulnerability ammunition (LOVA) propellants and will build acapability in composite rocket motors.• Pyrotechnic countermeasures and illumination – We will maintainour world lead in air countermeasures and will develop a fullrange of spectrally-optimised pyrotechnic payloads.• Pyrotechnic obscurants – We will lead development of safer,multi-spectral smokes and less-lethal technologies.Our electronics technology strategy builds on our leadership inkey niches:• Initiation – Is the interface to energetic products, and we willextend the application of electronics to improve the performanceof our munitions and pyrotechnic products.• Detection – We will maintain our lead in stand-off threatdetection technologies and will enhance these with sensor fusionand advanced algorithm development.• Electronic warfare (EW) – We will extend our lead in man-portableelectronic intelligence equipment, and will developvehicle-mounted variants of our products.• Electronic countermeasures – We will establish a world leadin active off-board decoys, and will develop a step-change inportable counter-IED jammers.• Network protection – We will apply our leading capability in fastelectronic hardware to lawful intercept applications and theprotection of wirelessly networked military systems.We will maintain an underpinning technology base to enable a cycleof rapid product development and technology insertion throughinternal research and partnerships with universities, researchinstitutions and technology companies. Where we cannot quicklydevelop critical capabilities and technologies organically, we willsupplement this with targeted acquisitions.Acquisition strategyAcquisitions have been an important element of the recent growthof the business. The successful completion of eighteen acquisitionsover the last six years has broadened our capabilities, diversifiedour segmental and geographic activities, and has directlycontributed to the overall growth of the <strong>Group</strong>.Revenue growth 2005–2011£ million80070060050040030020010002005 OrganicgrowthAcquisitivegrowth*Foreignexchange*Acquisitive growth comprisesFull year revenue of prior year acquisitionsRevenue contribution of businesses acquired in the year2011Our strategy for acquisitions is to continue to target opportunitieswhich add capability, technology and market access. We will exploitsynergies from such acquisitions by creating centres-of-excellence,investing in new products and selling our products though ourworldwide channels to market.We intend to maintain a balance of acquisition investment across allour segments, markets and technologies.Our acquisition investments over the last six years can be analysedas follows:Total investment on acquisitions 2005–2011 c.£480 millionGeographical spreadUK 22%Europe 23%USA 55%Electronic warfareGround troops using the Queen’s Awardwinning RESOLVE systemBusiness activityPyrotechnics 39%Munitions 31%Counter-IED 24%Countermeasures 6%<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011Business overview Corporate governance Financial statements Other information

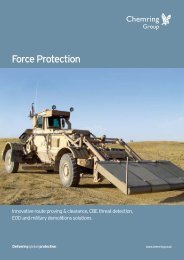

14Business overview15Counter – IEDThe closing order book for Counter-IED was £127 million,up 28% on 2010, and a clear indicator of continued revenuegrowth in 2012.Highlights in 2011• Revenue 46% higher than 2010• NIITEK delivered 77 complete HMDSand range of spares, increasing itsrevenue by 24%• Acquisition of <strong>Chemring</strong> DetectionSystems provides world-leadingcapability in chemical andbiological detection• <strong>Chemring</strong> Ordnance won USproduction contract for Anti-PersonnelObstacle Breaching System (APOBS),worth up to $150 million• Closing order book for Counter-IEDwas £127 million, up 28% on 2010Key informationOrders£207mRevenue£168mOperating profit£32mOperating margin19%StrategyOur strategy is to become the world leaderin the global counter-IED (improvisedexplosive device) market with hightechnology products to detect, disable anddefeat the threat posed by IEDs, as wellas chemical and biological agents. We willinvest in advanced sensor technologyfor the detection of explosive, biological,chemical and nuclear threats, as well asthe data fusion necessary to deliver highreliability detection performance. We willalso develop portable wide-band adaptivejamming capabilities to disable remotelycontrolled devices, and will develop andqualify advanced technology disruptors andthe full range of safer demolition stores todefeat them.AnalysisThe global market for counter-IEDequipment is estimated to be £3 billion.Our revenue in 2011 was £168 million,46% higher than the previous year, whichequates to a market share of 6%. The<strong>Group</strong>’s strongest focus is on detectionsystems, and revenue from this part of thebusiness increased by 51% to £149 million,representing a 25% market share of this keyhigh technology area. Our success has beendriven by the demand from the US Army forhighly effective ground penetrating radar(GPR). In July, the acquisition of <strong>Chemring</strong>Detection Systems was completed and,in the last four months of the financialyear, the business contributed £15 millionof revenue.The closing order book for Counter-IEDwas £127 million, up 28% on 2010, and aclear indicator of continued revenue growthin 2012.Activities during the yearDetectThe detection of IEDs continued todominate the activities of our Counter-IEDdivision during the year, with continuedgrowth at NIITEK in support of the HuskyMounted Detection System (HMDS) groundpenetrating radars currently deployed inAfghanistan. During 2011, NIITEK delivered77 complete radar systems, over 2,700radar panels, and a wide variety of sparesfor operational maintenance in-theatre,generating an increase in revenue of 24%compared with the previous year.In the middle of the year, a system upgradewas introduced to all new HMDS radarsystems. This upgrade provided greatersensitivity and a higher ground clearancemount to minimise panel damage duringtransit. A remote-controlled version ofthe Husky system was also deployed toAfghanistan and is currently undergoingoperational evaluation.NIITEK also won a contract from theUS Army for a Talon-based GPR systemwith an embedded metal detector coil.The system has successfully completedUS trials and safety testing. It is expectedto start operational evaluation during2012 and production should commenceshortly thereafter.Roke has been funded by the UK Ministryof Defence to develop a family of newhand-held detector systems, calledSPLINTER. An early prototype system wasdeployed to Afghanistan during the yearand the results achieved were describedas “very encouraging”. A fully functionalproduct has recently been completed and arapid qualification programme is expectedin 2012.The acquisition of <strong>Chemring</strong> DetectionSystems provides the <strong>Group</strong> with aworld-leading capability in chemical andbiological detection, as it is the incumbentsupplier for two major US militaryvehicle-mounted detection programmes:the Joint Biological Point Detection System(JBPDS) and the Joint Service LightweightStand-off Chemical Agent Detector(JSLSCAD). <strong>Chemring</strong> Detection Systemscontinued its customer-funded developmentprogramme during the year and movedon to Phase 3 of the Biological DetectionSystem Upgrade Program. These updateswill be implemented into new productionsystems, as well as retrofitted into existingfield units.<strong>Chemring</strong> Detection Systems also launcheda commercially available variant of theJSLSCAD. This product provides groundplatforms, fixed sites and shipboardinstallations with state-of-the-art remotechemical agent detection capabilities.A recent test demonstrated its ability todetect stimulants out to a full 5km range.A first export contract has been receivedfrom a Far East country, and strong interesthas been expressed by a number of MiddleEast customers.<strong>Chemring</strong> Detection Systems also continuedwork in 2011 on a customer-fundeddevelopment for the Lightguard stand-offexplosives detector. Three systems werefabricated and delivered for early usertesting. Additional work is expected in2012 to continue user testing, to complete aproduction readiness phase of the currentgeneration system, and to work on a nextgeneration system for vehicle-mountedapplications with on-the-move capability.DefeatIn June 2011, our US subsidiary <strong>Chemring</strong>Ordnance won a highly competitive contractto produce the MK7 MOD 2 Anti-PersonnelObstacle Breaching System (APOBS) for theUS Army and Marine Corps. The contractis for three years and is worth up to$150 million. The APOBS is a self-contained,one-shot, expendable linear demolitioncharge, which can be transported anddeployed by a two person team. Thesystem is capable of safely clearing afootpath through anti-personnel mines andmulti-strand wire obstacles. This contractaward expands our position in the USdemolition stores market. A new productionfacility, to assemble the product, is nownearing completion.This year has seen the successfuldevelopment and qualification of a newgeneration of Bangalore Torpedo undercontract from the UK Ministry of Defence.Although the concept of the BangaloreTorpedo is over 100 years old, ourdevelopment has produced a substantialimprovement in performance whilstensuring that it meets the criteria for aninsensitive munition.The development of the SABREX flexiblelinear cutting charge has continuedthroughout the year with final design,to meet the underwater performancerequirements, being achieved in thesummer. A commercial qualificationprogramme, to meet the needs of ourexport and commercial customers, hascommenced, and UK qualification willfollow in summer 2012. A number of exportcustomers have already placed orders andthere continues to be strong interest in theproduct from all parts of the global market.Our business units and companies<strong>Chemring</strong> Energetics UK LtdSpecialises in the design andmanufacture of energetic materials,detonators, and demolition stores.<strong>Chemring</strong> EOD Ltd (UK)Manufactures a range of products fordetection, assessment and neutralisationof threats from improvised explosivedevices and unexploded ordnance.<strong>Chemring</strong> Ordnance, Inc. (USA)Supplies Anti-Personnel ObstacleBreaching System (APOBS), arocket-deployed mine clearance system,to the US Army.<strong>Chemring</strong> Detection Systems, Inc. (USA)Leading US developer and supplier ofvehicle-mounted chemical and biologicaldetection systems for the US Army.Non-Intrusive Inspection Technology,Inc. (USA)The leading manufacturer ofvehicle-mounted ground penetratingradar mine detection systems.Roke Manor Research Ltd (UK)A world-class developer of electroniccountermeasures and threat detectiontechnologies.Chemical/biological detectionJUNO hand held detector in useOur productsDetect• Vehicle-mounted IED detection systems• Chemical and biological detectionsystems• Stand-off IED detectors• Remote IED inspection equipment• Under-vehicle surveillance systemsDisable• Electronic countermeasuresDefeat• Remote initiators• Detonators• Explosive charges• Minefield breaching systems• Recoilless de-armers/disruptorsBusiness overview Corporate governance Financial statements Other information<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011

18Business overview19PyrotechnicsIn September, <strong>Chemring</strong> Ordnance won two new marinepyrotechnic production contracts, worth up to $31 million,from the US Navy.Highlights in 2011• US Army declared the M992 “blacklight” illumination round produced by<strong>Chemring</strong> Ordnance as one of its topten inventions• <strong>Chemring</strong> Energetics UK selected todeliver components associated with theemergency oxygen deployment systemfor the Boeing 787• <strong>Chemring</strong> Energetic Devices completedinitial deliveries of its Joint CombinedAircraft Systems Testers (JCAST), fortesting life-support systems for F-16and F-22 aircraftKey informationOrders£107mRevenue£140mOperating profit£32mOperating margin23%StrategyOur strategy is to become the worldleader in pyrotechnics, through focusedinvestment in new products that displaceexisting incumbents and which better meetour customers’ requirements and transformtheir operational capabilities. We intend toexpand our activities in the space sectorby developing improved products forinitiation, stage separation, and satelliteand sub-system deployment for military andcommercial customers. This will address theUS, European and emerging internationalmarkets. We intend to expand our safetysystems activities, both in military andcivil aircraft.AnalysisThe global market for pyrotechnics iscurrently estimated to be £1.6 billion.Our revenue in 2010 was £140 million,which is 18% lower than the previous yearand represents a reduction in global marketshare to 9%. The majority of this declinewas driven by reduced sales of smoke andillumination products, which were 25% lowerthan the previous year. Sales of trainingand simulation products were down 5%,reflecting reduced European sales whichwere partially offset by increased deliveriesof US training grenades.The closing order book was £145 million,down 16% on the previous year due todelayed order placement from many of ourcustomers. However, demand is recoveringin this sector and revenues are expected torecover to pre-2011 levels.Activities during the yearSmoke and illuminationThe <strong>Group</strong> continues to focus on thedevelopment of advance “blacklight” andvisible illumination payloads for a widevariety of ordnance rounds and missiles.During the year, volume production wasstarted on 105mm ammunition payloadsand this has generated considerableinterest with the US Army. A number ofair-launched products are also underdevelopment and should enter productionin the next few years.Production of US 40mm pyrotechnicrounds slowed in 2011, when the US Armytook six months to hold the competitionfor the 40mm prime contract coveringthe next five years. This extended periodforced re-qualification of all productionlines, and the Army decided to give priorityto its non-pyrotechnic requirements.Production is restarting in 2012 with goodvolumes for M662 Red Star and M992Blacklight rounds. In September, theUS Army declared the M992 was one of itstop ten award-winning inventions.Mecar has completed the initial developmentof a 120mm mortar spotting round, whichis used to improve long-range firingaccuracy as well as operator and forwardobserver training. This new product uses aproprietary composition that replaces theconventional white phosphorus payload. In2012, Mecar will also develop an infra-redand visible light screening round for towedand turreted 120mm mortar systems.In September, <strong>Chemring</strong> Ordnance wontwo new marine pyrotechnic productioncontracts, worth up to $31 million, from theUS Navy. The first was for Mk 140 seriesday/night signals that are launched fromsubmarines to signal surface vessels oraircraft. The second was for the MK124day/night pyrotechnic marking signal, ahand-held device utilised by the US Navyand US Air Force aircrew in air and searescue and recovery operations. Thesenew contracts establish <strong>Chemring</strong> asone of the largest suppliers of submarinelocation markers.TrainingIn 2010, <strong>Chemring</strong> Ordnance upgradedthe M228 training grenade to incorporatethe confidence clip fitted to live grenadesused by the US Army to prevent accidentalremoval of the firing pin. During 2011, theautomated production line was increasedto 20 units per minute and over two millionunits were made. The company also passedseveral pre-qualification tests for a nextgeneration pyrotechnic simulator, whichprovides a safe and realistic visible effectto orientate air and ground personnel tothe launch of a MANPADS surface-to-airmissile. The MANPADS simulator will beutilised to train personnel involved in rotarywing close air support and UAV operations.Safety systems<strong>Chemring</strong> Energetics UK has been selectedby BE Aerospace to deliver componentsassociated with the emergency oxygendeployment system for the Boeing 787.The initial components have been deliveredas part of the qualification programme forthe system, and we have signed a long-termagreement with BE Aerospace to deliverthese components over an extended period.We are also supporting proposals for anemergency oxygen delivery system on theAirbus 350.In early September, <strong>Chemring</strong> EnergeticDevices completed initial deliveries of itsJoint Combined Aircraft Systems Testers(JCAST), which are used to test oxygensystems, helmets, noise reduction headsetsand chemical defence systems on F-16 andF-22 aircraft. These testers were used bythe US Air Force to assess the quality ofthe oxygen systems that grounded theF-22 fleet during 2011. Each of the F-22squadrons now has an onsite test capability.We are also under contract to provideadditional systems to the US Air Force AirCombat Command for its F-16 units in 2012,and have started working with the Air Forceon defining the modifications necessary toservice the multi-national F-35 Joint StrikeFighter programme.SpaceOur commercial launch and satellitesegment continues to grow, and defencecustomers are combining their requirementswith the commercial side to realise costsavings. The constant need for weather,navigation and increased communicationsbandwidth will have a positive impact onthis marketplace. The market is becomingmore global with both Europe and Asiaincreasing their rate of launches, and inorder to exploit this change, Hi-Shear and<strong>Chemring</strong> Energetics UK have entered intoan agreement to expand <strong>Chemring</strong>’s spacepresence in Europe. We are solidifying ourrelationship with both ANA and Mitsubishiin Japan, and we have begun to explorerelationships in India.Our business units and companies<strong>Chemring</strong> Australia Pty LtdSupplies a range of pyrotechnics, militarytraining and marine safety products.<strong>Chemring</strong> Defence (Europe)Centre-of-excellence for the design,development and production of smoke andillumination pyrotechnics and payloads formilitary, OEM and safety customers.<strong>Chemring</strong> Energetics UK LtdA leading supplier of rocket motors,canopy cutting cords and pyromechanismsfor safety and aircrew egress.<strong>Chemring</strong> Energetic Devices, Inc. (USA)Supplier of pyrotechnic andelectromechanical systems for space,safety and military training applications.<strong>Chemring</strong> Marine Ltd (UK)The world’s leading supplier of marinedistress signals to commercial andleisure markets, under the brand namesPains Wessex and Comet.<strong>Chemring</strong> Ordnance, Inc. (USA)Leading US manufacturer of militarytraining pyrotechnics and pyrotechnicrounds for 40mm grenade launchers.Hi-Shear Technology Corporation (USA)Leading supplier of space qualifiedinitiators and low shock satelliteseparation systems, and a range ofpyromechanisms for aircrew egress.Troop concealmentTraining with smoke grenadesOur productsSpace and satellite launch• Initiators• Separation sub-systems• Thrusters and actuatorsTraining• Pyrotechnics and launchersSmoke and illumination• Military smokes, flares and rockets• Distraction and screening products• Pyrotechnic payloads• Commercial marine pyrotechnics• Submarine distress signalsSafety systems• Rocket motors• Canopy cutting charges• Cartridge actuated devicesBusiness overview Corporate governance Financial statements Other information<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011

20Business overview21MunitionsThe closing order book for the Munitions divisionwas £372 million, an increase of 39% on theprevious year.Highlights in 2011• Revenue up 104% on 2010• Large calibre ammunition sales grewstrongly with revenues up 198%• New microwave fuze, jointly developedwith Oto Melara, recently completedNATO qualification• Continued growth in demand for40mm grenades, with a 200% increasein production• Closing order book for Munitionswas £372 million, an increase of 39%on 2010Key informationOrders£349mRevenue£237mOperating profit£41mOperating margin17%StrategyOur principal strategy is to develop ourposition as a niche prime contractorof specialist ammunition products forEuropean and non-NATO markets. We willbuild on our world-leading position in navalammunition, our growing strength in thesupply of ammunition for light armouredvehicles (LAVs), and our broad range ofmortar and 40mm grenade products.We will focus on new product developmentand investment in facilities that will allowus to expand our presence in a growinginternational market. We intend to buildour position as a key strategic supplierof energetic material components andsub-systems to the key prime contractorsfor ammunition and missiles in Europeand the US. This will be achieved bydeveloping and qualifying componentsfor next generation weapon systems,displacing poorly performing incumbents onlegacy products, investment in automatedmanufacturing facilities, and by furthercomplementary acquisitions wherethere is a clear opportunity to enhanceshareholder value.AnalysisThe global market for ammunition,excluding small calibre, is estimated tobe £4 billion. Our total revenue in 2011was £237 million, a 104% increase on theprevious year and equating to a marketshare of 6%. Our highest growth comesfrom the sale of ammunition for LAVs,which increased by 198% to £158 million ofrevenue. Naval ammunition sales increasedby 122% to £20 million, as deliveriesof 76mm ammunition started to rampupwards. The global market for munitionscomponents is estimated to be £2 billion.In 2011, our revenue from componentswas £58 million, representing 24% of ourtotal Munitions revenue, an increase of8% compared with the previous year andequating to a market share of 3%.The closing order book for the Munitionsdivision was £372 million, an increase of39% on the previous year, and a clearindication of further growth in 2012.About 71% of the order book is fromnon-NATO customers.Activities during the yearNaval76mm naval ammunition continued to bein demand during the year, with productionvolumes up 83% to 13,000 rounds. Therehas been strong interest from many of ournaval customers in Europe, the Middle East,the Far East and South America. A newmicrowave fuze, jointly developed withOto Melara, has recently completed NATOqualification and a live-firing demonstrationfor a number of Middle East customers isscheduled to take place shortly in Italy.LandOur sales of large calibre ammunition grewstrongly during the year with revenuesup 198% for Middle East and Far Eastcustomers. Demand for advanced 90mmand 105mm ammunition for LAVs hascontinued to increase with more and morenon-NATO countries upgrading their fleetsto make them more effective. Demand for81mm and 120mmm mortar products alsoincreased and we recently signed our firstcontract with an important Middle EastNavy customer.Demand for our range of 40mm grenadeshas also continued to grow, with a 200%increase in production volumes forAustralian and Middle East customers.Our US subsidiary, <strong>Chemring</strong> Ordnance,continues to develop, qualify, and fieldadvanced products for the US market andthis year we qualified a family of extendedrange, low velocity rounds and the nextgeneration door-breaching round used byspecial forces for forced entry operations.Components and sub-systemsDemand for our high performance, highreliability components and sub-systemscontinues to grow with increased sales toboth US and European prime contractors.During the year, there was a substantialincrease in the deliveries of warheads toMBDA for use on their Sea Viper air defencemissile, that protects the UK’s Daring classdestroyers. There was also strong growth insales of fuzing and safety/arming systemsthat initiate warheads and rocket motorswith over 20,000 ordnance fuzes deliveredto Far East customers.The <strong>Group</strong> also manufactures criticalcomponents of fuzing systems usedin a large number of US missiles andammunition rounds. A new 25mm airburstround, called the XM-25, was qualifiedduring the year and then evaluated in thefield by US Special Forces. Highly automatedmanufacturing systems will be set upduring 2012 to handle the start of full rateproduction in 2014.Our business units and companies<strong>Chemring</strong> Energetics UK LtdA leading supplier of detonators,actuators, rocket motors, high explosivefilling and pyromechanical sub-assemblies.<strong>Chemring</strong> Energetic Devices, Inc. (USA)Manufactures a range of materials,components and sub-systems for leadingmissile and ammunition prime contractors.<strong>Chemring</strong> Military Products, Inc. (USA)Provides load, assemble, packand procurement services to theUS government and prime contractors.<strong>Chemring</strong> Nobel AS (Norway)Manufactures niche energeticmaterials with insensitive munitions(IM) characteristics for munition andoil-field applications.<strong>Chemring</strong> Ordnance, Inc. (USA)Niche supplier of 40mm grenadeammunition.Hi-Shear Technology Corporation (USA)Develops advanced sub-systemsfor ballistic missile defence andtactical weapons.Mecar S.A. (Belgium)A niche supplier of medium andlarge calibre ammunition for lightarmoured vehicles.Simmel Difesa S.p.A. (Italy)A leading supplier of naval ammunition,advanced fuzing technology andmissile components.105mm tank ammunition105mm MGS Stryker BCT vehicleOur productsNaval ammunition• Medium and large calibre ammunitionLand forces ammunition• Medium and large calibre ammunition• 40mm grenades• Mortar ammunitionComponents• Propellants and rocket motors• Fuze and safe/arm units• Pyromechanisms and actuators• Energetic materialsBusiness overview Corporate governance Financial statements Other information<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011

22Business overview23Review by the Finance DirectorUnderlying profit before tax* was up 6% to £125.6 million,and underlying profit after tax* was up 10% to £96.8 million.Financial highlights• Revenue up 25% to £745.3 million• Underlying profit before tax* up 6% to£125.6 million• Net finance expense down 14% to£16.3 million• Underlying operating cash flow of£124.6 million, representing an88% conversion from underlyingoperating profit*• £150.1 million of undrawn borrowingfacilities at the year endKey informationUnderlying operating profit*£141.8m+3%Research and development expenditure£59.6m+74%Divisional operating margin20%* Before non-underlying items (see Note 6)#The 2010 figures have been restated to reflect thereclassification of certain items from underlyingcosts to non-underlying costs (see Note 6)~ Organic growth at constant US dollar excludesgrowth from contracts and customers acquired withRoke, Mecar and <strong>Chemring</strong> Detection SystemsResultsAn analysis of the underlying results is set out below:Total revenue 745.3 597.1Divisional operating profit 151.8 147.9Unallocated corporate costs (10.0) (10.4)Underlying operating profit 141.8 137.5Share of post-tax results of associate 0.1 0.1Finance income 0.1 0.5Finance expense (16.4) (19.4)Underlying profit before tax 125.6 118.7Tax on underlying profit before tax (28.8) (30.7)Underlying profit after tax 96.8 88.0Total revenue was £745.3 million (2010: £597.1 million), an increase of 25%. Revenuearising from the acquisition of <strong>Chemring</strong> Detection Systems in 2011 was £14.6 million, 2%of the increase. Organic revenue growth ~ was 9%. Roke and Mecar, which were acquiredin September 2010, contributed 17% of the <strong>Group</strong> revenue increase. During the year, theUS dollar depreciated against sterling, which reduced the reported sterling revenues ofUS subsidiaries by £15.1 million, equivalent to 3%.An analysis of revenue and divisional operating profit* by segment is set out below:Underlyingoperatingprofit*£m2011UnderlyingoperatingmarginDivisionRevenueRevenue£m£mCounter-IED 167.6 31.9 19% 114.9 28.1 25%Countermeasures 200.8 46.7 23% 196.3 58.8 30%Pyrotechnics 139.9 32.4 23% 170.0 40.1 24%Munitions 237.0 40.8 17% 115.9 20.9 18%Divisional results 745.3 151.8 20% 597.1 147.9 25%2011£mUnderlyingoperatingprofit* #£m2010£m2010UnderlyingoperatingmarginCounter-IED revenue increased 46% to £167.6 million, due to increased revenue atNIITEK for HMDS spares and support, together with a £14.6 million contribution from<strong>Chemring</strong> Detection Systems. Operating margins reduced to 19%, largely due to pricingpressure on NIITEK’s products. <strong>Chemring</strong> Detection Systems’ 15% margin also dilutedthe overall margin for this segment.Countermeasures revenue grew by 3% but underlying operating profit* reduced 21%,largely due to lower demand for decoys at Alloy Surfaces, which was only partially offsetby revenue from Roke at a lower margin of 10%.Pyrotechnics revenue decreased 18% to £139.9 million and underlying operatingprofit* decreased 19% to £32.4 million, principally due to lower demand for 81mmillumination products.Munitions grew the most, with revenue increasing 104% to£237.0 million following a strong second half performance fromMecar. Mecar’s margin grew to 10% in the second half from anegative margin at the half year.Unallocated corporate costs were £10.0 million, slightly down on2010. In 2010, two non-recurring cost items, which netted out at£1.9 million (£4.3 million charge, £2.4 million credit) were includedin unallocated corporate costs but with the reformatting of theIncome Statement this year these items have now been reclassifiedas non-underlying items in order to be consistent year-on-year.The impact of this reclassification is an increase in underlyingoperating profit* for 2010 to £137.5 million from £135.6 million,although divisional operating profits are unchanged.Total underlying operating profit* was £141.8 million(2010: £137.5 million), an increase of 3%. Underlying operatingprofit* generated by <strong>Chemring</strong> Detection Systems was £2.2 million.Roke and Mecar contributed £9.0 million. The impact of thedepreciation of the US dollar against sterling reduced the USsubsidiaries’ reported sterling profits in 2011 by £3.6 million.Without this depreciation, growth in total underlying operatingprofit* in 2011 would have been 6%.Total underlying operation margin* reduced to 19% from 23% lastyear. Approximately half this reduction is attributable to lowermargins at Alloy Surfaces and NIITEK, with the other half reflectingthe impact of acquired businesses with lower margins than the<strong>Group</strong> average.Finance income in the year was £0.1 million (2010: £0.5 million).Finance expense for the year was £16.4 million (2010: £19.4 million),a decrease of 15%. Included within finance expense is £0.7 million(2010: £1.2 million) for retirement benefit obligations. Net financeexpense was covered 8.7 times (2010: 7.3 times) by underlyingoperating profits.Underlying profit before tax* was £125.6 million(2010: £118.7 million # ), an increase of 6%.Tax on underlying profit before tax* was £28.8 million(2010: £30.7 million), representing an underlying rate of 23%(2010: 26%). The reduction in the tax rate arises from theutilisation of research and development tax credits across the<strong>Group</strong>, particularly at Roke, together with the partial utilisationof tax losses within our European businesses which had notpreviously been recognised.Underlying profit after tax* was £96.8 million(2010: £88.0 million # ), an increase of 10%.Analysis of non-underlying itemsThe Board monitors underlying operating profit and underlyingprofit before tax for reporting purposes so as to not distortyear-on-year comparisons, hence certain items are classed asnon-underlying as set out below:2011£m2010 #£mAcquisition related costs 5.7 6.7Restructuring and incident costs 7.2 4.3Provision release – (2.4)(Gain)/loss on fair value movements on derivatives (2.4) 4.0Intangible amortisation arising frombusiness combinations 24.3 17.0Total non-underlying items 34.8 29.6Acquisition related costs include the external costs incurredin acquiring businesses in 2010 and 2011, together with costsassociated with an aborted bid and the establishment ofjoint ventures.In 2011, the restructuring and incident costs related to theclosure of Plant 3 at Alloy Surfaces (£1.1 million) and the start-upof production at Mecar following the incident that occurred inSeptember 2010 (£2.3 million). At the end of October 2011, theBoard decided to exit some loss-making munitions product lines inthe US, and in addition to minor losses, a provision has also beenmade for excess inventory and fixed assets (£3.8 million).In 2010, the restructuring and incident costs included therestructuring of the <strong>Group</strong>’s UK Counter-IED business at a costof £1.5 million. As a result, one of the two sites out of which itoperated was closed. Also, there were two separate incidents thatstopped production at the Kilgore Flares facility in Tennessee andMecar in Belgium. As a result of these incidents, £2.8 million ofnon-recurring costs were incurred in respect of the write-off ofdamaged stock and destroyed assets.During 2010, part of the provision held in respect of theenvironmental liabilities associated with the <strong>Chemring</strong> EnergeticDevices site in Illinois was released, following a third partyassessment of the provision. This resulted in a £2.4 millionnon-recurring credit to the Income Statement.A gain on derivatives of £2.4 million arose this year, due largely tothe movement in the sterling/dollar exchange rate during the year.Intangible amortisation arising from business combinationsincreased in the year, with a full year amortisation of assetsacquired with the Mecar and Roke acquisitions, and fourmonths’ amortisation arising from the acquisition of <strong>Chemring</strong>Detection Systems.Business overview Corporate governance Financial statements Other information<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011<strong>Chemring</strong> <strong>Group</strong> <strong>PLC</strong> <strong>Report</strong> and Accounts 2011