- Page 2 and 3:

TABLE OF CONTENTSLIST OF ABBREVIATI

- Page 4 and 5:

11.8 RECOMMENDATIONS ..............

- Page 6 and 7:

LIST OF TABLESTable 1: Cases of Non

- Page 8 and 9: NORMOSPsPOSAPPLPPL (India)ProLitter

- Page 10 and 11: These problems are addressed in the

- Page 12 and 13: xxi.The report considers developmen

- Page 14 and 15: 1.3.8. Determine whether all money

- Page 16 and 17: 1.4.9. The CRC derived considerable

- Page 18 and 19: 2.3 SUBMISSION BY THE DEPARTMENT OF

- Page 20 and 21: Aspects of Intellectual Property Ri

- Page 22 and 23: (1) Subject to the provisions of th

- Page 24 and 25: Copyright Tribunal or an arbitrator

- Page 26 and 27: society, the South African Recordin

- Page 28 and 29: 3.2.14. With the liquidation of SAR

- Page 30 and 31: the final rate or rates to be appli

- Page 32 and 33: (a)that payment is to be made to th

- Page 34 and 35: information as to their use to enab

- Page 36 and 37: The WCT and WPPT oblige members to

- Page 38 and 39: Once the handset technology changed

- Page 40 and 41: 4.3.16. In 2009, in what was coined

- Page 42 and 43: 4.4.6. In exchange for the above li

- Page 44 and 45: operators are licensed by NORM to p

- Page 46 and 47: 5.2 FUNCTIONING OF COLLECTING SOCIE

- Page 48 and 49: the grant of licences. Article 17 o

- Page 50 and 51: 6.1.3. The CRC’s assessment of th

- Page 52 and 53: 6.3.3. SAMPRA should be given one y

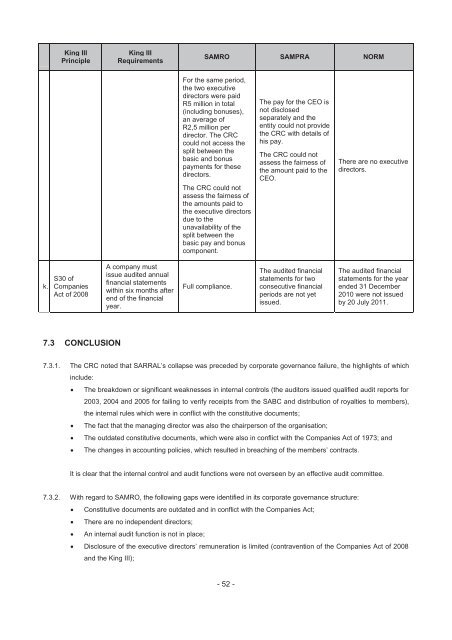

- Page 54 and 55: Corporate Governance GapsKing II Re

- Page 56 and 57: King IIIPrincipleKing IIIRequiremen

- Page 60 and 61: 8 COLLECTION OF MUSIC ROYALTIES8.1

- Page 62 and 63: 8.1.4.2. Needletime royalties are n

- Page 64 and 65: 8.1.7.4. For the past five years, V

- Page 66 and 67: PRS (UK)SPRE (FRANCE)SUISA(SWITZERL

- Page 68 and 69: DetailsPerformance RightsSound Reco

- Page 70 and 71: 8.2.7 Comparative Study Performed b

- Page 72 and 73: y a collecting society. A rights ho

- Page 74 and 75: agency, its rights being derived fr

- Page 76 and 77: Mr Robinson said DALRO assumed the

- Page 78 and 79: 10.1.6. The distribution to publish

- Page 80 and 81: 10.4.4. Most of the other collectin

- Page 82 and 83: 10.6.3.4. South African English-lis

- Page 84 and 85: 10.10 CONTRACTUAL RELATIONSHIPS BET

- Page 86 and 87: 10.12.2. The Regulations should rec

- Page 88 and 89: licence that the licensee comply wi

- Page 90 and 91: 11.4.6. The details of ICASA’s ta

- Page 92 and 93: RecommendationsTimelines for Recomm

- Page 94 and 95: enterprises. There was a suggestion

- Page 96 and 97: Copyright as it relates to copyrigh

- Page 98 and 99: 13.4 DEPARTMENT OF ARTS AND CULTURE

- Page 100 and 101: Table 28: Comparative Study’s Key

- Page 102 and 103: KEY ITEMS BRAZIL FRANCE INDIA NORWA

- Page 104 and 105: KEY ITEMS BRAZIL FRANCE INDIA NORWA

- Page 106 and 107: about 30%, which is the highest amo

- Page 108 and 109:

15.1.3. The Copyright Tribunal’s

- Page 110 and 111:

15.1.20. Local music content requir

- Page 112 and 113:

for the selected artists. The outco

- Page 114 and 115:

King III Report by Institute of Dir

- Page 116 and 117:

Paranagua Pedro, “Strategies to I

- Page 118 and 119:

Copyright Amendment Act of 1984Copy

- Page 120 and 121:

APPENDIX 1(B): SUMMARY OF ORAL REPR

- Page 122 and 123:

Due to the fact that the existing c

- Page 124 and 125:

Mr BrottelProtection of copyright m

- Page 126 and 127:

1.1.3. LIST OF ENTITIES VISITED AND

- Page 128 and 129:

In the 2009 Annual Report of ABRAMU

- Page 130 and 131:

The implementation of this law led

- Page 132 and 133:

ecordings. In respect of audio-visu

- Page 134 and 135:

In 1995, ECAD distributed 72% of it

- Page 136 and 137:

niches in the market to ensure fair

- Page 138 and 139:

Proprietary rights allow authors to

- Page 140 and 141:

International royalty distribution

- Page 142 and 143:

3.2. Relevant LegislationsThe prese

- Page 144 and 145:

IPRS uses the standard tariffs in r

- Page 146 and 147:

Ad-hoc workshops on copyright are c

- Page 148 and 149:

meaningful living out of their crea

- Page 150 and 151:

4.1.3. LICENSING AND LEGAL REGIMESI

- Page 152 and 153:

Ballet teachers; Teachers in the fi

- Page 154 and 155:

It was founded in 1928 by the Norwe

- Page 156 and 157:

6.2. STRUCTURE OF COLLECTING SOCIET

- Page 158 and 159:

6.5. COLLECTION OF MUSIC ROYALTIEST

- Page 160 and 161:

1957, when the Managing Director of

- Page 162 and 163:

16.4.14 SWISSPERFORM: CHF4 millionI

- Page 164 and 165:

Cross-border licensing of digital r

- Page 166 and 167:

algorithm could be used to determin

- Page 168 and 169:

Collecting societies in the UK all

- Page 170 and 171:

APPENDIX 3: RECOMMENDATIONS BY MITT

- Page 172 and 173:

1.PREAMBLEThe Music Industry Task T

- Page 174 and 175:

The environment in which the music

- Page 176 and 177:

3.1.3 IMPLEMENTATION AND ACCESSION

- Page 178 and 179:

In this regard, the Minister should

- Page 180 and 181:

3.5.6 OMBUDSMANThe music industry s

- Page 182 and 183:

RECOMMENDATION 23:The MITT recommen

- Page 184 and 185:

The MITT further recommends that DA

- Page 186 and 187:

APPENDIX 4A: EXTRACTS FROM COPYRIGH

- Page 188 and 189:

(f)(g)doing, in relation to an adap

- Page 190 and 191:

(i)requiring notice of any intended

- Page 192 and 193:

(b)any organization claiming to be

- Page 194 and 195:

PERFORMERS’ PROTECTION ACTNO. 11

- Page 196 and 197:

the parties may agree to refer the

- Page 198 and 199:

- 192 -

- Page 200 and 201:

- 194 -

- Page 202 and 203:

- 196 -

- Page 204 and 205:

- 198 -

- Page 206 and 207:

ANNEXURE 5: COPY OF SARRAL’S CONT

- Page 208 and 209:

- 202 -

- Page 210 and 211:

ANNEXURE 6: SARRAL’S AUDIT REPORT

- Page 212 and 213:

- 206 -

- Page 214 and 215:

TERMS OF REFERENCESNO’SREQUIREMEN

- Page 216 and 217:

TERMS OF REFERENCESNO’SREQUIREMEN

- Page 218 and 219:

TERMS OF REFERENCESNO’SREQUIREMEN

- Page 220 and 221:

TERMS OF REFERENCESNO’SREQUIREMEN

- Page 222 and 223:

TERMS OF REFERENCESNO’SREQUIREMEN

- Page 224:

- 218 -