Sustainability Report 2012 - Generali Versicherung AG

Sustainability Report 2012 - Generali Versicherung AG Sustainability Report 2012 - Generali Versicherung AG

Change in numberof complaints received 2009-20122010/20092011/2010 2012/201127.0% 20.6% 8.5%The data for the Czech Republic do not include informationrelating to Generali Pojišt'ovna, which is not available.In 2012, the number of complaints received by the Group’sinsurance companies increased by 8.5%, continuing theupward trend of last two years, but to a much lower extent.The incidence of complaints received is 20.5 for every 10,000policies taken out, which is reduced to 10.8 if we consideronly accepted complaints, i.e. those for which the validity ofthe complaint has been acknowledged. It should be notedthat, while recording an increase of 14.1% over the previousyear, accepted complaints account for a little over half of thosesubmitted (52.8%). Furthermore, although growing at an overalllevel, the number of complaints received in some countries hasdeclined sharply during the year: 37.8% in Austria and 10.7%in France.Accepted complaints are highly concentrated in geographicalterms: 80.8% of them relate to Germany where, in addition toclaims, dissatisfaction/malfunction reports are also recorded.Therefore, in the case of Germany and also in Spain, the increase in complaints is not mainly due to growing customerdissatisfaction, but rather to the increased openness of companies to listening and trying to resolve the problems andinefficiencies reported by clients.In the majority of cases (93%), complaints are made by the policyholder/insured party, while only 7% of complaints aremade by the injured party/beneficiary.Considering the main reasons for complaints, over half (57.6%; 71.8% in Germany) relate to administrative activities,mainly due to shortcomings in the service provided, difficulties experienced by clients in understanding the contractualdocumentation and/or statements, and excessively long processing times. 29% of complaints relate to settlements,where grievances were primarily due to payment delays or what were perceived to be insufficient amounts reimbursed.Settlements represent the area with the majority of dissatisfied clients in Switzerland (94.8%), Spain (64.2%), Italy (59.6%)and France (57.1%) while, in Austria, only 1.8% of complaints relate to that area. Overall, the underwriting area received thefewest complaints (13.4% of the total, with a peak of 42.1% in Austria and 35.8% in France), relating mainly to inefficienciesin the service offered by the sales staff and client expectations of products not being met.Insurance disputesAs at 31 December 2012, in the countries in the Sustainability Report area, the Group was involved in 152,495 disputesrelating to its insurance business, all of which are currently in different phases of resolution. The number of disputesincludes passive litigation, in which the Generali Group companies are the defendants, and cases where Group companieshave initiated proceedings.Passive insurance disputesCountry Number of disputes Value of disputes (thousand euros)2011 2012 2011 2012Italy 54,230 57,943 3,054,803 3,176,344Austria 2,944 2,944 117,057 127,456Czech Republic 1,838 1,889 89,199 85,250France 3,845 3,600 254,116 233,169Germany 13,870 13,742 261,651 351,118Spain 18,460 20,950 265,688 267,587Switzerland 153 129 34,179 35,012TOTAL 95,340 101,197 4,076,692 4,275,937The number of pending passive disputes, totalling 101,197, increased by 6.1%, mainly due to motor insurance disputes (accountingfor 65.7%) and, to a lesser extent, general liability risks (21%).In the motor LoB, an increase of 8.3% was recorded, while disputes relating to general liability risks decreased by 2.9%.With regard to the value of disputes, herein taken to be the amount requested by claimants, there was an overall increase of 4.9%due to the increase in general liability risks (+4.5%) while the value of disputes related to the motor LoB fell by 3.3%.102 | Assicurazioni Generali - Sustainability Report 2012

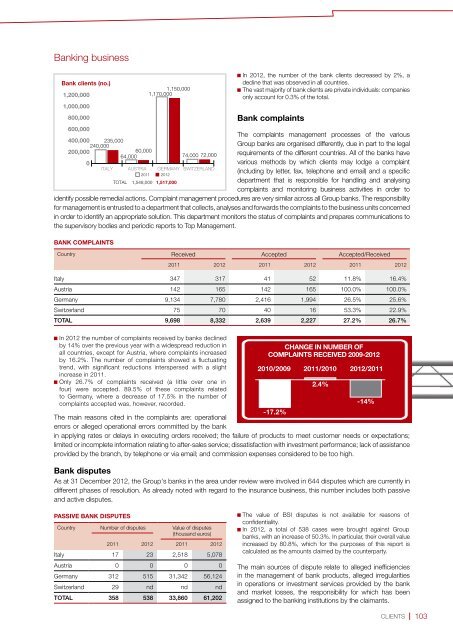

Banking businessBank clients (no.)1,200,0001,000,000800,000600,000400,000200,0000240,000235,000 60,00064,0001,170,0001,150,00074,000 72,000ITALY AUSTRIA GERMANY SWITZERLAND2011 2012TOTAL1,548,000 1,517,000In 2012, the number of the bank clients decreased by 2%, adecline that was observed in all countries.The vast majority of bank clients are private individuals: companiesonly account for 0.3% of the total.complaints and monitoring business activities in order toidentify possible remedial actions. Complaint management procedures are very similar across all Group banks. The responsibilityfor management is entrusted to a department that collects, analyses and forwards the complaints to the business units concernedin order to identify an appropriate solution. This department monitors the status of complaints and prepares communications tothe supervisory bodies and periodic reports to Top Management.Bank complaintsBank complaintsThe complaints management processes of the variousGroup banks are organised differently, due in part to the legalrequirements of the different countries. All of the banks havevarious methods by which clients may lodge a complaint(including by letter, fax, telephone and email) and a specificdepartment that is responsible for handling and analysingCountry Received Accepted Accepted/Received2011 2012 2011 2012 2011 2012Italy 347 317 41 52 11.8% 16.4%Austria 142 165 142 165 100.0% 100.0%Germany 9,134 7,780 2,416 1,994 26.5% 25.6%Switzerland 75 70 40 16 53.3% 22.9%TOTAL 9,698 8,332 2,639 2,227 27.2% 26.7%In 2012 the number of complaints received by banks declinedby 14% over the previous year with a widespread reduction inall countries, except for Austria, where complaints increasedby 16.2%. The number of complaints showed a fluctuatingtrend, with significant reductions interspersed with a slightincrease in 2011.Only 26.7% of complaints received (a little over one infour) were accepted. 89.5% of these complaints relatedto Germany, where a decrease of 17.5% in the number ofcomplaints accepted was, however, recorded.Change in number ofcomplaints received 2009-20122010/20092011/2010 2012/2011-17.2%The main reasons cited in the complaints are: operationalerrors or alleged operational errors committed by the bankin applying rates or delays in executing orders received; the failure of products to meet customer needs or expectations;limited or incomplete information relating to after-sales service; dissatisfaction with investment performance; lack of assistanceprovided by the branch, by telephone or via email; and commission expenses considered to be too high.Bank disputesAs at 31 December 2012, the Group's banks in the area under review were involved in 644 disputes which are currently indifferent phases of resolution. As already noted with regard to the insurance business, this number includes both passiveand active disputes.2.4%-14%Passive bank disputesCountry Number of disputes Value of disputes(thousand euros)2011 2012 2011 2012Italy 17 23 2,518 5,078Austria 0 0 0 0Germany 312 515 31,342 56,124Switzerland 29 nd nd ndTOTAL 358 538 33,860 61,202The value of BSI disputes is not available for reasons ofconfidentiality.In 2012, a total of 538 cases were brought against Groupbanks, with an increase of 50.3%. In particular, their overall valueincreased by 80.8%, which for the purposes of this report iscalculated as the amounts claimed by the counterparty.The main sources of dispute relate to alleged inefficienciesin the management of bank products, alleged irregularitiesin operations or investment services provided by the bankand market losses, the responsibility for which has beenassigned to the banking institutions by the claimants.CLIENTS | 103

- Page 53 and 54: In Italy and France, when returning

- Page 55 and 56: normally have the option, often gua

- Page 57 and 58: HEALTH AND SAFETY IN THEWORKPLACETh

- Page 59 and 60: Emirates, the Philippines, Guatemal

- Page 61 and 62: SIZE AND CHARACTERISTICS OF THE WOR

- Page 63 and 64: On average, a third (33.4%) of posi

- Page 65 and 66: Workforce by age bracket2011 2012 2

- Page 67 and 68: Labour disputesNumber and value of

- Page 69 and 70: To foster greater staff involvement

- Page 71 and 72: Committedto innovation anddiversifi

- Page 73 and 74: SIZE AND CHARACTERISTICS OFTHE SALE

- Page 75 and 76: DIRECT CHANNELS, with no intermedia

- Page 77 and 78: Satisfaction surveys on services pr

- Page 79 and 80: Along with thecommitment to strengt

- Page 81 and 82: FINANCIAL AND SUSTAINABILITY PERFOR

- Page 83 and 84: RatingRating agencyRating*A.M.BestA

- Page 85: Main meetings with analysts and inv

- Page 88 and 89: PRODUCT POLICIESCustomer loyalty is

- Page 90 and 91: Products with particular environmen

- Page 92 and 93: Over the last few years, various ro

- Page 94 and 95: • fill out questionnaires with a

- Page 96 and 97: of pre-packaged solutions. As part

- Page 98 and 99: Surveys on servicesGERMANYOnline su

- Page 100 and 101: Percentage of clients by age bracke

- Page 102 and 103: Change in number of claims2009-2012

- Page 106 and 107: SUPPLIERSKarolinen Karee, Munich, G

- Page 108 and 109: Relationships with contractual part

- Page 110 and 111: SIZE AND CHARACTERISTICSOF SUPPLIER

- Page 112 and 113: COMMUNITYOld-Aged Survey, Germania1

- Page 114 and 115: GUIDELINES FOR COMMUNITYINITIATIVES

- Page 116 and 117: For example, in 2012 the Generali E

- Page 118 and 119: Cultural areaWith a view to promoti

- Page 120 and 121: Sports areaGenerali regards sport a

- Page 122 and 123: ENVIRONMENT ANDCLIMATE CHANGEOilsee

- Page 124 and 125: In order to pursue the abovemention

- Page 126 and 127: DIRECT ENVIRONMENTAL IMPACTThe data

- Page 128 and 129: Electricity quota from renewable so

- Page 130 and 131: PaperPaper consumption3530252015105

- Page 132 and 133: WaterWater consumption (m 3 )-0.4%3

- Page 134 and 135: In all countries, IT waste, compris

- Page 136 and 137: Flight kilometres travelled by empl

- Page 138 and 139: The increase in exposure to climate

- Page 140 and 141: EXPENDITURES AND INVESTMENTSFOR ENV

- Page 142 and 143: ENVIRONMENTAL RANKINGGenerali’s a

- Page 145 and 146: CONTENTINDEXParis - France

- Page 147 and 148: REPORTEDGLOBALCOMPACTPRINCIPLESCROS

- Page 149 and 150: GLOBALREPORTED COMPACTPRINCIPLESful

- Page 151 and 152: REPORTEDGLOBALCOMPACTPRINCIPLESCROS

- Page 153: GLOBALREPORTED COMPACTCROSS-REFEREN

Banking businessBank clients (no.)1,200,0001,000,000800,000600,000400,000200,0000240,000235,000 60,00064,0001,170,0001,150,00074,000 72,000ITALY AUSTRIA GERMANY SWITZERLAND2011 <strong>2012</strong>TOTAL1,548,000 1,517,000In <strong>2012</strong>, the number of the bank clients decreased by 2%, adecline that was observed in all countries.The vast majority of bank clients are private individuals: companiesonly account for 0.3% of the total.complaints and monitoring business activities in order toidentify possible remedial actions. Complaint management procedures are very similar across all Group banks. The responsibilityfor management is entrusted to a department that collects, analyses and forwards the complaints to the business units concernedin order to identify an appropriate solution. This department monitors the status of complaints and prepares communications tothe supervisory bodies and periodic reports to Top Management.Bank complaintsBank complaintsThe complaints management processes of the variousGroup banks are organised differently, due in part to the legalrequirements of the different countries. All of the banks havevarious methods by which clients may lodge a complaint(including by letter, fax, telephone and email) and a specificdepartment that is responsible for handling and analysingCountry Received Accepted Accepted/Received2011 <strong>2012</strong> 2011 <strong>2012</strong> 2011 <strong>2012</strong>Italy 347 317 41 52 11.8% 16.4%Austria 142 165 142 165 100.0% 100.0%Germany 9,134 7,780 2,416 1,994 26.5% 25.6%Switzerland 75 70 40 16 53.3% 22.9%TOTAL 9,698 8,332 2,639 2,227 27.2% 26.7%In <strong>2012</strong> the number of complaints received by banks declinedby 14% over the previous year with a widespread reduction inall countries, except for Austria, where complaints increasedby 16.2%. The number of complaints showed a fluctuatingtrend, with significant reductions interspersed with a slightincrease in 2011.Only 26.7% of complaints received (a little over one infour) were accepted. 89.5% of these complaints relatedto Germany, where a decrease of 17.5% in the number ofcomplaints accepted was, however, recorded.Change in number ofcomplaints received 2009-<strong>2012</strong>2010/20092011/2010 <strong>2012</strong>/2011-17.2%The main reasons cited in the complaints are: operationalerrors or alleged operational errors committed by the bankin applying rates or delays in executing orders received; the failure of products to meet customer needs or expectations;limited or incomplete information relating to after-sales service; dissatisfaction with investment performance; lack of assistanceprovided by the branch, by telephone or via email; and commission expenses considered to be too high.Bank disputesAs at 31 December <strong>2012</strong>, the Group's banks in the area under review were involved in 644 disputes which are currently indifferent phases of resolution. As already noted with regard to the insurance business, this number includes both passiveand active disputes.2.4%-14%Passive bank disputesCountry Number of disputes Value of disputes(thousand euros)2011 <strong>2012</strong> 2011 <strong>2012</strong>Italy 17 23 2,518 5,078Austria 0 0 0 0Germany 312 515 31,342 56,124Switzerland 29 nd nd ndTOTAL 358 538 33,860 61,202The value of BSI disputes is not available for reasons ofconfidentiality.In <strong>2012</strong>, a total of 538 cases were brought against Groupbanks, with an increase of 50.3%. In particular, their overall valueincreased by 80.8%, which for the purposes of this report iscalculated as the amounts claimed by the counterparty.The main sources of dispute relate to alleged inefficienciesin the management of bank products, alleged irregularitiesin operations or investment services provided by the bankand market losses, the responsibility for which has beenassigned to the banking institutions by the claimants.CLIENTS | 103