N° 2005-09 Juin 2005 Guillaume Daudin* Jean-Luc Gaffard ...

N° 2005-09 Juin 2005 Guillaume Daudin* Jean-Luc Gaffard ... N° 2005-09 Juin 2005 Guillaume Daudin* Jean-Luc Gaffard ...

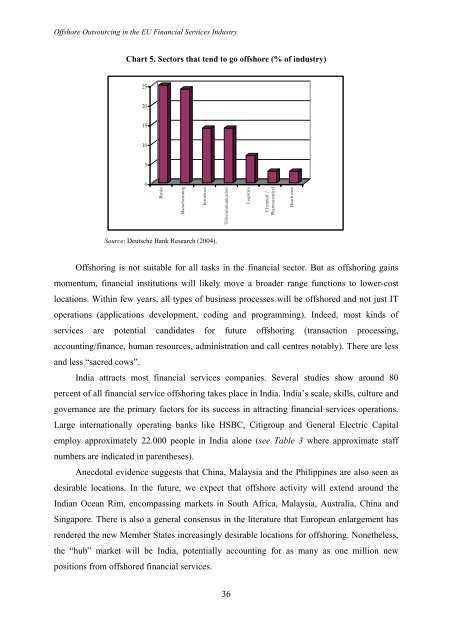

Offshore Outsourcing in the EU Financial Services IndustryChart 5. Sectors that tend to go offshore (% of industry)2520151050BanksManufacturingInsuranceTelecommunicationLogisticsChemical /PharmaceuticalHeath careSource: Deutsche Bank Research (2004).Offshoring is not suitable for all tasks in the financial sector. But as offshoring gainsmomentum, financial institutions will likely move a broader range functions to lower-costlocations. Within few years, all types of business processes will be offshored and not just IToperations (applications development, coding and programming). Indeed, most kinds ofservices are potential candidates for future offshoring (transaction processing,accounting/finance, human resources, administration and call centres notably). There are lessand less “sacred cows”.India attracts most financial services companies. Several studies show around 80percent of all financial service offshoring takes place in India. India’s scale, skills, culture andgovernance are the primary factors for its success in attracting financial services operations.Large internationally operating banks like HSBC, Citigroup and General Electric Capitalemploy approximately 22.000 people in India alone (see Table 3 where approximate staffnumbers are indicated in parentheses).Anecdotal evidence suggests that China, Malaysia and the Philippines are also seen asdesirable locations. In the future, we expect that offshore activity will extend around theIndian Ocean Rim, encompassing markets in South Africa, Malaysia, Australia, China andSingapore. There is also a general consensus in the literature that European enlargement hasrendered the new Member States increasingly desirable locations for offshoring. Nonetheless,the “hub” market will be India, potentially accounting for as many as one million newpositions from offshored financial services.36

Georges PujalsTable 3. Financial services companies in India (2003)ABN Amro (+ 300) American Express (+ 1.000)Axa (380) Citigroup (3.000)Deutsche Bank (500) General Electric Capital (11.000)HSBC (2.000) JP Morgan Chase (480)Mellon Financial (240) Merrill Lynch (350)Standard Chartered (3.000)Source: Deloitte Research (2004).According to a report 10 by Deloitte Research (2004), offshoring will continue to growthroughout this decade. The report estimated the percentage of global financial servicescompanies with offshore facilities grew to 67 percent in 2003 compared with 29 percent in2002, along with an estimated 500 percent increase in offshore jobs. By the year 2010, morethan one-fifth of the financial services industry’s global cost base will have shifted offshoreaccording to the survey. Meanwhile, the 100 largest financial institutions in the world – thosewith market capitalization exceeding $10 billion – will have moved nearly US $ 400 billion oftheir cost base offshore, reducing costs by 37 percent for each process relocated and savingeach firm on average a little below US $ 1.5 billion annually. By the end of 2005, itanticipated around US $ 210 billion of the cost base will be offshore with average costsavings to be over US $ 700 million for the largest 100. The report noted that the percentagefor large firms was significantly higher than for small firms 11 and also indicated thatincreasingly firms are setting up their own operations offshore (“captive” offshoring),distinguishing this trend from the growth of outsourcing.Deloitte Research (2003) also estimated that US $ 356 billion of operating expenses (or2 million people) would be relocated offshore in the global financial services industry withinthe next five years.10 Deloitte’s second annual offshore survey The Titans Take Hold, 2004. The survey is based on responses from43 financial institutions based in seven countries and included 13 of the 25 financial institutions in the world bymarket capitalization.11 80 percent of the world’s largest financial institutions (i.e., those with market capitalization exceeding US $10 billion) are already working offshore, with less than 20 percent keeping everything at home. For smallercompanies, the number are split 50:50 between those offshore and those staying home. That disparity creates asignificant cost advantage for the larger institutions and the gap is likely to get wider.37

- Page 1 and 2: COMPETITION FROM EMERGING COUNTRIES

- Page 3 and 4: Competition from Emerging Countries

- Page 5 and 6: I. OFFSHORE RELOCATIONS AND EMERGIN

- Page 7 and 8: Guillaume Daudin and Sandrine Levas

- Page 9 and 10: Guillaume Daudin and Sandrine Levas

- Page 11 and 12: Guillaume Daudin and Sandrine Levas

- Page 13 and 14: Guillaume Daudin and Sandrine Levas

- Page 15 and 16: Guillaume Daudin and Sandrine Levas

- Page 17 and 18: Guillaume Daudin and Sandrine Levas

- Page 19 and 20: Guillaume Daudin and Sandrine Levas

- Page 21 and 22: Guillaume Daudin and Sandrine Levas

- Page 23 and 24: Guillaume Daudin and Sandrine Levas

- Page 25 and 26: Guillaume Daudin and Sandrine Levas

- Page 27 and 28: II. OFFSHORE OUTSOURCING IN THE EU

- Page 29 and 30: Georges PujalsConcerning Europe, th

- Page 31 and 32: Georges Pujalsable to reduce costs)

- Page 33 and 34: Georges Pujals“Offshoring” - th

- Page 35: Georges Pujalsthe number of electro

- Page 39 and 40: Georges PujalsOffshoring was initia

- Page 41 and 42: Georges PujalsChart 8. Relative imp

- Page 43 and 44: Georges PujalsAll those categories

- Page 45 and 46: Georges PujalsChart 11. Supervisors

- Page 47 and 48: Georges Pujalsoutsourcing should th

- Page 49 and 50: Georges PujalsMcKinsey Global Insti

- Page 51 and 52: International Relocation and Deindu

- Page 53 and 54: International Relocation and Deindu

- Page 55 and 56: International Relocation and Deindu

- Page 57 and 58: International Relocation and Deindu

- Page 59 and 60: International Relocation and Deindu

- Page 61 and 62: International Relocation and Deindu

- Page 63 and 64: Relocation: What Matters? Competiti

- Page 65 and 66: Relocation: What Matters? Competiti

- Page 67 and 68: Relocation: What Matters? Competiti

- Page 69 and 70: Relocation: What Matters? Competiti

- Page 71 and 72: Relocation: What Matters? Competiti

- Page 73: Relocation: What Matters? Competiti

- Page 78: Jean-Luc Gaffard and Michel Quéré

Offshore Outsourcing in the EU Financial Services IndustryChart 5. Sectors that tend to go offshore (% of industry)2520151050BanksManufacturingInsuranceTelecommunicationLogisticsChemical /PharmaceuticalHeath careSource: Deutsche Bank Research (2004).Offshoring is not suitable for all tasks in the financial sector. But as offshoring gainsmomentum, financial institutions will likely move a broader range functions to lower-costlocations. Within few years, all types of business processes will be offshored and not just IToperations (applications development, coding and programming). Indeed, most kinds ofservices are potential candidates for future offshoring (transaction processing,accounting/finance, human resources, administration and call centres notably). There are lessand less “sacred cows”.India attracts most financial services companies. Several studies show around 80percent of all financial service offshoring takes place in India. India’s scale, skills, culture andgovernance are the primary factors for its success in attracting financial services operations.Large internationally operating banks like HSBC, Citigroup and General Electric Capitalemploy approximately 22.000 people in India alone (see Table 3 where approximate staffnumbers are indicated in parentheses).Anecdotal evidence suggests that China, Malaysia and the Philippines are also seen asdesirable locations. In the future, we expect that offshore activity will extend around theIndian Ocean Rim, encompassing markets in South Africa, Malaysia, Australia, China andSingapore. There is also a general consensus in the literature that European enlargement hasrendered the new Member States increasingly desirable locations for offshoring. Nonetheless,the “hub” market will be India, potentially accounting for as many as one million newpositions from offshored financial services.36