Maximun exposure to credit risk(Million euros)Spa<strong>in</strong> Eurasia Mexico31-12-12 31-12-11 31-12-10SouthAmericaThe UnitedStatesCorportateActivitiesTotalGroupTotalGroupGross credit risk (drawn) 229,290 41,960 39,542 53,672 41,505 1,158 407,126 400,709 384,069Customer lend<strong>in</strong>g (gross) 210,828 30,228 38,995 48,728 37,136 1,804 367,719 361,310 348,253Cont<strong>in</strong>gent liabilities 18,463 11,732 547 4,944 4,369 (646) 39,407 39,398 35,816Market activity 50,878 7,608 28,504 16,230 9,125 42,344 154,689 134,937 129,398Credit entities 12,463 2,327 4,808 3,332 1,368 2,224 26,522 26,107 23,636Fixed <strong>in</strong>come 25,275 5,280 22,460 10,107 7,263 40,120 110,505 88,621 88,081Derivatives 13,141 - 1,235 2,792 494 - 17,662 20,209 17,680Undrawn facilitites 27,241 16,769 13,366 6,521 22,157 168 86,223 88,978 86,790Maximum exposure to credit risk 307,410 66,337 81,412 76,424 72,787 43,669 648,039 624,624 600,257TotalGroup16 <strong>BBVA</strong> Group. Maximum exposure to credit riskDistribution by type of risk(31-12-<strong>2012</strong>)<strong>BBVA</strong> Group. Gross exposure to credit riskDistribution by bus<strong>in</strong>ess area(31-12-<strong>2012</strong>)17Undrawn facilities 13.3%South America 10.2%Credit risk 62.8%Spa<strong>in</strong> 56.3%Loans 56.7%Cont<strong>in</strong>gent liabilities 6.1%Market activity 23.9%Eurasia 10.3%Mexico 9.7%The United States 13.2%Exposure: 648,039 million eurosCredit risk: 407,126 million euros18<strong>BBVA</strong> Group. Exposure to customer lend<strong>in</strong>g (gross). Distribution by portfolio(31-12-<strong>2012</strong>)Global customers 13.3%Residential mortgages 28.9%Public sector 8.7%Individuals 39.7%Corporate and bus<strong>in</strong>ess 38.3%Consumer f<strong>in</strong>ance 7.5%Credit cards 3.4%Credit risk: 367,719 million euros102 Risk management

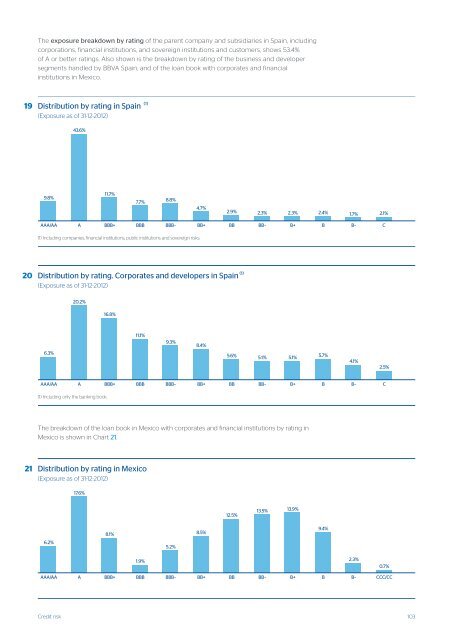

The exposure breakdown by rat<strong>in</strong>g of the parent company and subsidiaries <strong>in</strong> Spa<strong>in</strong>, <strong>in</strong>clud<strong>in</strong>gcorporations, f<strong>in</strong>ancial <strong>in</strong>stitutions, and sovereign <strong>in</strong>stitutions and customers, shows 53.4%of A or better rat<strong>in</strong>gs. Also shown is the breakdown by rat<strong>in</strong>g of the bus<strong>in</strong>ess and developersegments handled by <strong>BBVA</strong> Spa<strong>in</strong>, and of the loan book with corporates and f<strong>in</strong>ancial<strong>in</strong>stitutions <strong>in</strong> Mexico.19 Distribution by rat<strong>in</strong>g <strong>in</strong> Spa<strong>in</strong> (1)(Exposure as of 31-12-<strong>2012</strong>)43.6%9.8%11.7%7.7%8.8%4.7%2.9% 2.3% 2.3% 2.4%1.7%2.1%AAA/AA A BBB+ BBB BBB– BB+ BB BB– B+BB–C(1) Includ<strong>in</strong>g companies, f<strong>in</strong>ancial <strong>in</strong>stitutions, public <strong>in</strong>stitutions and sovereign risks.20 Distribution by rat<strong>in</strong>g. Corporates and developers <strong>in</strong> Spa<strong>in</strong> (1)(Exposure as of 31-12-<strong>2012</strong>)20.2%16.8%11.1%9.3%8.4%6.3%5.6% 5.1% 5.1%5.7%4.1%2.5%AAA/AA A BBB+ BBB BBB– BB+ BB BB– B+BB–C(1) Includ<strong>in</strong>g only the bank<strong>in</strong>g book.The breakdown of the loan book <strong>in</strong> Mexico with corporates and f<strong>in</strong>ancial <strong>in</strong>stitutions by rat<strong>in</strong>g <strong>in</strong>Mexico is shown <strong>in</strong> Chart 21.21 Distribution by rat<strong>in</strong>g <strong>in</strong> Mexico(Exposure as of 31-12-<strong>2012</strong>)17.6%12.5%13.5% 13.9%8.1%8.5%9.4%6.2%5.2%1.9%AAA/AA A BBB+ BBB BBB– BB+ BB BB– B+B2.3%B–0.7%CCC/CCCredit risk103

- Page 2 and 3:

BBVA Group Highlights

- Page 4 and 5:

“ In 2012 the Group generateda ne

- Page 6:

2

- Page 9 and 10:

Letter from the Chairman 5

- Page 11 and 12:

All this is the result of a strateg

- Page 13 and 14:

1 As the main expression of t

- Page 15 and 16:

Our communication in 2012 has conti

- Page 17 and 18:

Brand management in 2012 was highly

- Page 19 and 20:

BBVA Board CommitteesIn order to be

- Page 21 and 22:

• Across-the-board operational co

- Page 23 and 24:

Primary stakeholdersIntroduction: t

- Page 25 and 26:

BBVA earnings figures presented in

- Page 28 and 29:

High liquidity ofBBVA shareBBVA is

- Page 30 and 31:

Management modelA model of peoplema

- Page 32 and 33:

To sum up, the combination of the a

- Page 35 and 36:

South AmericaIn 2012, a common syst

- Page 37 and 38:

Number of claims filed at the Banki

- Page 39 and 40:

Environmentand BBVA positioningThe

- Page 41 and 42:

the measures taken to correct imbal

- Page 44 and 45:

The easing of financial tensions in

- Page 46 and 47:

Positioning of BBVA GroupBBVA conti

- Page 48 and 49:

20 2. A business model based on th

- Page 50 and 51:

- Innovate with teams dedicated exc

- Page 52 and 53:

25 In short, this banking model

- Page 54 and 55:

2. …reflected ingross income…28

- Page 56 and 57: Risk under controlBBVA NPAs versusp

- Page 58 and 59: Business areasSpainStrong franchise

- Page 60 and 61: EurasiaAn area ofgrowth andpositive

- Page 62 and 63: South AmericaBusiness activity(Year

- Page 64 and 65: In short, abusinesstransformationre

- Page 67 and 68: Group financialinformation65 Earnin

- Page 69 and 70: EarningsIn 2012, BBVA Group reporte

- Page 71 and 72: Consolidated income statement: quar

- Page 73 and 74: • Resilience in Spain, in a conte

- Page 75 and 76: allocations to the deposit guarante

- Page 77 and 78: 8 • Maintain its leadership p

- Page 79 and 80: 13 Provisions and othersCumulativ

- Page 81 and 82: Lastly, earnings per share (EPS) fr

- Page 83 and 84: In short, a year in which there has

- Page 85 and 86: 20 Lastly, non-performing loans ha

- Page 87 and 88: Off-balance-sheet customer funds st

- Page 89 and 90: Capital baseThe main highlight in 2

- Page 91 and 92: 26 RatingsIn 2012, BBVA’s ratin

- Page 93 and 94: Risk management90 Global Risk Manag

- Page 95 and 96: Integration of risks andoverall ris

- Page 97 and 98: Credit riskCredit risk quantificati

- Page 99 and 100: Behavioral scoring is used to revie

- Page 101 and 102: The economic cycle in PDThe current

- Page 103 and 104: 13LGD for Autos Finanzia, BBVA Spai

- Page 105: The portfolio model and concentrati

- Page 109 and 110: 22 Real-estate exposure and coverag

- Page 111 and 112: ConcentrationExcluding sovereign ri

- Page 113 and 114: 27 BBVA Group. Net NPA entries(Mill

- Page 115 and 116: Structural risksStructural interest

- Page 117 and 118: Interest rate risk measurement is s

- Page 119 and 120: Structural risk in the equity portf

- Page 121 and 122: BBVA continues working to improve a

- Page 123 and 124: Credit risk in market activitiesThe

- Page 125 and 126: Operational riskOperational risk is

- Page 127 and 128: Operational risk management in the

- Page 129 and 130: Reputational riskThis is another ty

- Page 131 and 132: The economic capital of the Pension

- Page 133 and 134: Categories of financing and advice

- Page 135 and 136: Business areas135 Spain149 Eurasia1

- Page 137 and 138: Furthermore, as usual in the case o

- Page 139 and 140: SpainIncome statement(Million euros

- Page 141 and 142: • On July 20, the Government requ

- Page 143 and 144: 3 Spain. Efficiency ratio versus pe

- Page 145 and 146: These lines axes of action will con

- Page 147 and 148: 10 Spain. Operating income(Million

- Page 149 and 150: - Creation of a SICAV module on the

- Page 151 and 152: As of 31-Dec-2012, BBVA Seguros has

- Page 153 and 154: EurasiaIncome statement(Million eur

- Page 155 and 156: Management prioritiesIn 2012, the E

- Page 157 and 158:

17 Eurasia. Efficiency(Million euro

- Page 159 and 160:

• The above, together with the hi

- Page 161 and 162:

Highlights• The Bank has been rec

- Page 163 and 164:

MexicoIncome statement(Million euro

- Page 165 and 166:

area has been positive year-on-year

- Page 167 and 168:

30 Mexico. Consumer finance plus cr

- Page 169 and 170:

The increase of operating expenses

- Page 171 and 172:

As a result of the above, the net a

- Page 173 and 174:

government employees and tax collec

- Page 175 and 176:

South AmericaIncome statement(Milli

- Page 177 and 178:

advancing together with economic ac

- Page 179 and 180:

43 South America. Net attributable

- Page 181 and 182:

Grupo BBVA. Business share ranking

- Page 183 and 184:

Colombia Peru Venezuela2012 ∆%

- Page 185 and 186:

The macroeconomic and competitive e

- Page 187 and 188:

VenezuelaIn 2012, the growth of the

- Page 189 and 190:

By companies, Seguros Argentina, fo

- Page 191 and 192:

Significant ratios(Percentage)The U

- Page 193 and 194:

opportunities in key markets throug

- Page 195 and 196:

51 The United States. NPA and cover

- Page 197 and 198:

The area was able to successfully m

- Page 199 and 200:

HighlightsThe most relevant awards

- Page 201 and 202:

Definition of the aggregateCorporat

- Page 203 and 204:

held by retail investors. The conve

- Page 205 and 206:

Additional information:Corporate &

- Page 207 and 208:

greater efficiency, cost control an

- Page 209 and 210:

The trend in operating expenses sho

- Page 211 and 212:

Main Corporate Finance transactions

- Page 213 and 214:

Corporate LendingCorporate Lending

- Page 215 and 216:

In Latin America, the funding of Li

- Page 217 and 218:

In Mexico, Global Markets maintains

- Page 219 and 220:

Supplementaryinformation216 Consoli

- Page 221 and 222:

IFRS (Bank of Spain’s Circular 4/

- Page 223:

JapanTokyoFukoku Seimei Bldg. 12 th