Bayesian Inference in the Seemingly Unrelated Regressions Model

Bayesian Inference in the Seemingly Unrelated Regressions Model

Bayesian Inference in the Seemingly Unrelated Regressions Model

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

3<br />

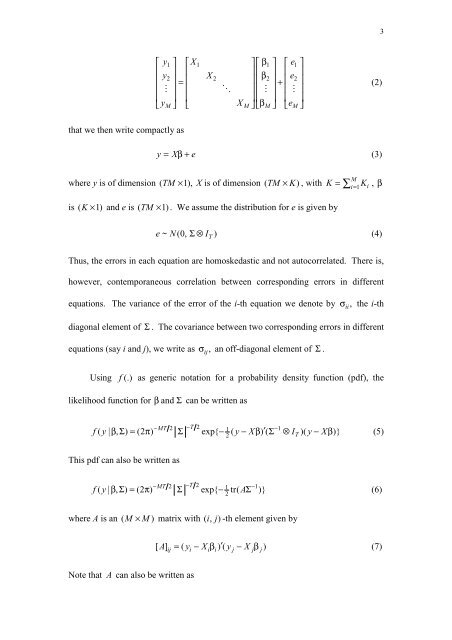

⎡ y1 ⎤ ⎡X1 ⎤⎡β1 ⎤ ⎡ e1<br />

⎤<br />

⎢<br />

y<br />

⎥ ⎢<br />

2 X<br />

⎥⎢<br />

2 β<br />

⎥ ⎢<br />

2 e<br />

⎥<br />

⎢ ⎥<br />

2<br />

= ⎢ ⎥⎢ ⎥+<br />

⎢ ⎥<br />

⎢ ! ⎥ ⎢ " ⎥⎢ ! ⎥ ⎢ ! ⎥<br />

⎢ ⎥ ⎢ ⎥⎢ ⎥ ⎢ ⎥<br />

y X β e<br />

⎣ M⎦ ⎣ M⎦⎣ M⎦ ⎣ M⎦<br />

(2)<br />

that we <strong>the</strong>n write compactly as<br />

y = Xβ<br />

+ e<br />

(3)<br />

where y is of dimension ( TM × 1), X is of dimension ( TM × K)<br />

, with K = ∑ i=<br />

1 Ki<br />

, β<br />

is ( K × 1) and e is ( TM × 1) . We assume <strong>the</strong> distribution for e is given by<br />

M<br />

e~ N(0, Σ⊗ I T )<br />

(4)<br />

Thus, <strong>the</strong> errors <strong>in</strong> each equation are homoskedastic and not autocorrelated. There is,<br />

however, contemporaneous correlation between correspond<strong>in</strong>g errors <strong>in</strong> different<br />

equations. The variance of <strong>the</strong> error of <strong>the</strong> i-th equation we denote by σ ii,<br />

<strong>the</strong> i-th<br />

diagonal element of Σ . The covariance between two correspond<strong>in</strong>g errors <strong>in</strong> different<br />

equations (say i and j), we write as σ ij,<br />

an off-diagonal element of Σ .<br />

Us<strong>in</strong>g f (.) as generic notation for a probability density function (pdf), <strong>the</strong><br />

likelihood function for<br />

β and Σ can be written as<br />

−MT<br />

2 −T<br />

2 1<br />

−1<br />

′<br />

2<br />

f( y| β, Σ ) = (2 π) Σ exp{ − ( y− Xβ) ( Σ ⊗I )( y− Xβ )} (5)<br />

T<br />

This pdf can also be written as<br />

−MT<br />

2 −T<br />

2 1 −1<br />

A<br />

2<br />

f( y| βΣ , ) = (2 π) Σ exp{ − tr( Σ )}<br />

(6)<br />

where A is an ( M × M)<br />

matrix with ( i, j)<br />

-th element given by<br />

[ A] = ( y − X β )( ′ y − X β )<br />

(7)<br />

ij i i i j j j<br />

Note that A can also be written as