MARKET MOVER - BNP PARIBAS - Investment Services India

MARKET MOVER - BNP PARIBAS - Investment Services India

MARKET MOVER - BNP PARIBAS - Investment Services India

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

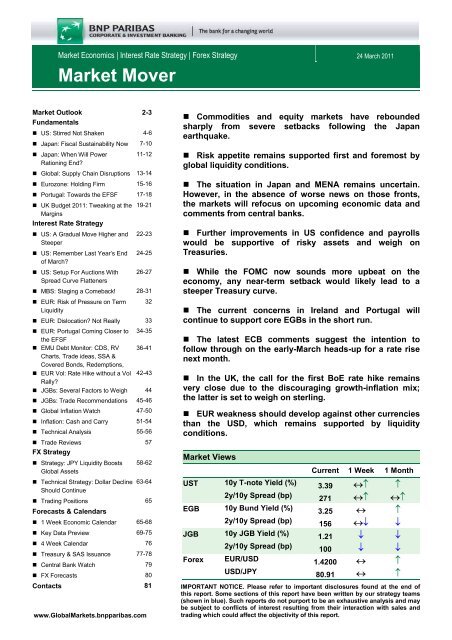

Market Economics | Interest Rate Strategy | Forex Strategy 24 March 2011<br />

Market Mover<br />

Market Outlook 2-3<br />

Fundamentals<br />

• US: Stirred Not Shaken 4-6<br />

• Japan: Fiscal Sustainability Now 7-10<br />

• Japan: When Will Power 11-12<br />

Rationing End?<br />

• Global: Supply Chain Disruptions 13-14<br />

• Eurozone: Holding Firm 15-16<br />

• Portugal: Towards the EFSF 17-18<br />

• UK Budget 2011: Tweaking at the 19-21<br />

Margins<br />

Interest Rate Strategy<br />

• US: A Gradual Move Higher and 22-23<br />

Steeper<br />

• US: Remember Last Year’s End 24-25<br />

of March?<br />

• US: Setup For Auctions With 26-27<br />

Spread Curve Flatteners<br />

• MBS: Staging a Comeback! 28-31<br />

• EUR: Risk of Pressure on Term 32<br />

Liquidity<br />

• EUR: Dislocation? Not Really 33<br />

• EUR: Portugal Coming Closer to 34-35<br />

the EFSF<br />

• EMU Debt Monitor: CDS, RV 36-41<br />

Charts, Trade ideas, SSA &<br />

Covered Bonds, Redemptions,<br />

• EUR Vol: Rate Hike without a Vol 42-43<br />

Rally?<br />

• JGBs: Several Factors to Weigh 44<br />

• JGBs: Trade Recommendations 45-46<br />

• Global Inflation Watch 47-50<br />

• Inflation: Cash and Carry 51-54<br />

• Technical Analysis 55-56<br />

• Trade Reviews 57<br />

FX Strategy<br />

• Strategy: JPY Liquidity Boosts 58-62<br />

Global Assets<br />

• Technical Strategy: Dollar Decline 63-64<br />

Should Continue<br />

• Trading Positions 65<br />

Forecasts & Calendars<br />

• 1 Week Economic Calendar 65-68<br />

• Key Data Preview 69-75<br />

• 4 Week Calendar 76<br />

• Treasury & SAS Issuance 77-78<br />

• Central Bank Watch 79<br />

• FX Forecasts 80<br />

Contacts 81<br />

www.GlobalMarkets.bnpparibas.com<br />

• Commodities and equity markets have rebounded<br />

sharply from severe setbacks following the Japan<br />

earthquake.<br />

• Risk appetite remains supported first and foremost by<br />

global liquidity conditions.<br />

• The situation in Japan and MENA remains uncertain.<br />

However, in the absence of worse news on those fronts,<br />

the markets will refocus on upcoming economic data and<br />

comments from central banks.<br />

• Further improvements in US confidence and payrolls<br />

would be supportive of risky assets and weigh on<br />

Treasuries.<br />

• While the FOMC now sounds more upbeat on the<br />

economy, any near-term setback would likely lead to a<br />

steeper Treasury curve.<br />

• The current concerns in Ireland and Portugal will<br />

continue to support core EGBs in the short run.<br />

• The latest ECB comments suggest the intention to<br />

follow through on the early-March heads-up for a rate rise<br />

next month.<br />

• In the UK, the call for the first BoE rate hike remains<br />

very close due to the discouraging growth-inflation mix;<br />

the latter is set to weigh on sterling.<br />

• EUR weakness should develop against other currencies<br />

than the USD, which remains supported by liquidity<br />

conditions.<br />

Market Views<br />

UST 10y T-note Yield (%)<br />

2y/10y Spread (bp)<br />

EGB 10y Bund Yield (%)<br />

2y/10y Spread (bp)<br />

JGB 10y JGB Yield (%)<br />

2y/10y Spread (bp)<br />

Forex<br />

EUR/USD<br />

USD/JPY<br />

Current 1 Week 1 Month<br />

3.39 ↔↑ ↑<br />

271 ↔↑ ↔↑<br />

3.25 ↔ ↑<br />

156 ↔↓ ↓<br />

1.21 ↓ ↓<br />

100 ↓ ↓<br />

1.4200 ↔ ↑<br />

80.91 ↔ ↑<br />

IMPORTANT NOTICE. Please refer to important disclosures found at the end of<br />

this report. Some sections of this report have been written by our strategy teams<br />

(shown in blue). Such reports do not purport to be an exhaustive analysis and may<br />

be subject to conflicts of interest resulting from their interaction with sales and<br />

trading which could affect the objectivity of this report.

Market Outlook<br />

The panic mode did not<br />

last long but a number of<br />

risks remain<br />

Upcoming US payrolls and<br />

confidence report will be<br />

key for Treasuries<br />

Last week’s risk-off period proved to be short lived. Markets have partly – for<br />

some assets, fully – reversed the post-Japan earthquake flight-to-quality<br />

move. Though the situation in Japan and MENA remains uncertain, global<br />

liquidity conditions continue to support risk appetite. After a jump into the 30<br />

area, the VIX index has moved back below 20.<br />

In the US, we remain cautiously bearish on Treasuries, firmly sticking with<br />

our view that yields may gradually rise in the coming months. However, the<br />

short-term picture will prove challenging due to global risk events spooking<br />

markets. It’s worth noting that this week’s Fed buybacks have been met with<br />

more aggressive selling than usual.<br />

We expect the upcoming US payroll (1 April) growth to be solid but<br />

unspectacular (180k). Consumer confidence (29 March) has been very<br />

sensitive to external developments and the impact on stock and oil prices.<br />

This effect is not over but the FOMC has only recently improved its<br />

assessment of the economic situation. It is unlikely to change its assessment<br />

unless confidence effects become broader based and sustained.<br />

Upcoming confidence and payrolls reports to impact risk appetite<br />

1600<br />

1500<br />

1400<br />

1300<br />

1200<br />

1100<br />

1000<br />

900<br />

800<br />

700<br />

600<br />

Consum er Confidence (RHS)<br />

S&P 500<br />

99 00 01 02 03 04 05 06 07 08 09 10<br />

150<br />

140<br />

130<br />

120<br />

110<br />

100<br />

90<br />

80<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

Increasing tensions on<br />

Portugal and Ireland…<br />

…are supporting core<br />

markets…<br />

Source: Reuters EcoWin Pro<br />

In Europe, the near-term focus is on the EU summit (today and tomorrow),<br />

with spreads having widened at the periphery. In Portugal, with the<br />

government failing to secure passage of its latest round of austerity<br />

measures in the lower house, the Prime Minister resigned. The probability of<br />

a bailout for Portugal (which we have long considered inevitable) has risen,<br />

but the current situation is very fluid. The path from where are today to<br />

assistance being provided by the IMF and the EU remains unclear.<br />

Irish bond yields have hit 10%, indicating that markets are pricing in<br />

insolvency risks. Ireland is more significant than Portugal in that its oversized<br />

banking sector can create significant negative spillovers when it runs into<br />

trouble. Spain, which had seen an impressive decline of its CDS spreads<br />

since January, has been alarmed by rating agencies considering<br />

downgrades of its banks.<br />

All this is happening as core countries see their room for manoeuvre and<br />

strike a deal reduced by populist trends. In Germany, Chancellor Merkel will<br />

have to renegotiate the funding of the ESM as the compromise reached at<br />

the last Summit and follow-up FinMin meeting has run into opposition even<br />

from lawmakers of parties that back her. In Finland, the 17 April general<br />

election may see the populist party 'True Fins' triumphing.<br />

Signs of stress have so far been limited outside Portugal and Ireland but<br />

current concerns will support core EGBs. The lack of resteepening of the<br />

Cyril Beuzit 24 March 2011<br />

Market Mover<br />

2<br />

www.GlobalMarkets.bnpparibas.com

…are supporting core<br />

markets…<br />

…and weighing on the<br />

euro<br />

benchmark curve shows that, if markets are taking into account potential<br />

risks, they are not as concerned as they were before. At this juncture, this<br />

context may prevail in coming days, offering core markets some support but<br />

not fuelling a strong bullish tone. We retain our constructive view on core<br />

EGBs and recommend trading from the long side.<br />

On spreads, it is worth noting that the market's assessment of risks is less<br />

elevated than it has been. This means that risk aversion could rise<br />

significantly if risks extend further. We see room for spreads to widen in the<br />

near term. This may prevent the flattening from developing significantly and<br />

exposes the back end of the curve to resteepening risks.<br />

The latest eurozone news is not good for the euro. However, global liquidity<br />

conditions have become even more supportive with the BoJ bumping<br />

liquidity into money markets and pushing this liquidity via JPY weakening<br />

intervention into global markets. Even in the US, recent housing market<br />

weakness has pushed back early rate-hike speculation. Strong liquidity<br />

conditions will keep asset prices supported and the USD on the back foot for<br />

the moment. This implies that EUR weakness should develop against other<br />

currencies than the USD. We recommend selling EURSEK, EURNOK and<br />

AUDEUR.<br />

Ireland and Portugal under the spotlight<br />

7<br />

6<br />

10 -Y ea r G ove rnm en t<br />

Bond Yield Spreads vs Germ any (% )<br />

Ireland<br />

5<br />

Portugal<br />

4<br />

3<br />

Spain<br />

2<br />

1<br />

0<br />

Jul<br />

Sep Nov Jan<br />

09<br />

Ita ly<br />

Mar May Jul Sep Nov Jan<br />

10<br />

Mar<br />

11<br />

Close call on the BoE due to<br />

the poor growth-inflation mix<br />

JGBs to remain well<br />

supported into the new<br />

fiscal year<br />

Source: Reuters EcoWin Pro<br />

In the UK, the timing of the first BoE rate hike remains a very close call. The<br />

worsening in the latest inflation data, coupled with confirmation from the BoE<br />

minutes that the MPC expects CPI inflation to exceed 5% y/y, reinforces the<br />

case for a rate hike at the May meeting. However, the minutes also showed<br />

that the committee is sensitive to news on the consumer and uncertainty<br />

about the durability of the recovery in activity indicators. We stand by our call<br />

for a hike at the May meeting, given the worsening news on inflation.<br />

Nonetheless, the increased risk of weaker activity data has made us more<br />

nervous.<br />

Sterling may have seen most of its rally. The advance since January was<br />

backed by rising nominal interest rate differentials while real yields have<br />

been declining. The discouraging growth-inflation mix suggests that real<br />

yields will stay low. Domestic demand weakness is likely as real income<br />

weakens. Unless the UK experiences a productivity growth boost – of which<br />

we have seen no evidence to date – real income will remain depressed,<br />

undermining sterling in the medium term.<br />

In Japan, equities plunged and JGB futures were bought up in the wake of<br />

11 March. With the help of emergency quantitative easing by the Bank of<br />

Japan and coordinated FX intervention, things seems to be calming<br />

somewhat. However, the headline risk remains high. Flight-to-quality<br />

considerations and the worsening economic outlook are likely to dominate<br />

sentiment in the near term.<br />

Cyril Beuzit 24 March 2011<br />

Market Mover<br />

3<br />

www.GlobalMarkets.bnpparibas.com

US: Stirred Not Shaken<br />

• The events in Japan are likely to produce a<br />

noticeable dip and recovery in US GDP growth<br />

in 2011. Limitations in supply will disrupt sales<br />

of autos and electronics.<br />

Chart 1: Share of Japan in US Trade<br />

• We forecast a slowing in GDP growth to<br />

1.5% in Q2 q/q saar from 2.3% in Q1. We then<br />

think consumers and businesses will make up<br />

for lost time in H2, with GDP accelerating to<br />

3.0% in Q3 and 4.0% in Q4.<br />

• Overall, the events in Japan are expected to<br />

reduce GDP growth by 0.2pp in 2011 while the<br />

rebound from the disaster should add 0.1pp in<br />

2012.<br />

• Japan is a relatively minor trading partner<br />

for the US, accounting for around 4.8% of all<br />

exports and 6% of imports. Japan plays a more<br />

significant role in the auto and advanced<br />

technology industries, where it accounts for<br />

13% and 7% of imports respectively.<br />

Source: Reuters EcoWin Pro<br />

Chart 2: Japanese Motor Vehicles and Parts<br />

Imports as % US Total Imported Vehicles and<br />

Parts<br />

• Most of the impact of the Japanese<br />

earthquake on the US economy is temporary in<br />

nature and comes from supply-chain<br />

disruptions.<br />

• However, it is a supply shock that is likely to<br />

add to global inflationary pressures, which will<br />

sap a little from final demand growth on<br />

balance.<br />

• The wild card continues to be any hit to<br />

consumer and business confidence which could<br />

take a larger toll on international activity.<br />

• There are few implications for US monetary<br />

or fiscal policy, which will continue to be driven<br />

by domestic concerns.<br />

Source: Reuters EcoWin Pro<br />

Chart 3: Auto Inventories on Hand Allow for a<br />

Decent Month of Sales in March<br />

A preliminary assessment of the impact of events<br />

in Japan on US economic growth suggests<br />

significant near-term supply chain disruptions<br />

The massive earthquake in Japan has wrought<br />

devastating human consequences in the world’s third<br />

largest economy. The rest of the world has looked on<br />

with sympathy and sadness as the Japanese bravely<br />

deal with the aftermath. The reaction in financial<br />

markets has swung between depression and<br />

euphoria.<br />

The reality is that the actual impact on economic<br />

activity inside and outside Japan will take time to<br />

Source: Reuters EcoWin Pro<br />

assess. The best we can do is think clearly through<br />

the likely chain of events in coming months.<br />

Our economists in Japan estimate that the hit to GDP<br />

growth in Japan in 2011 will be close to 3pp relative<br />

Julia Coronado/Yelena Shulyatyeva 24 March 2011<br />

Market Mover<br />

4<br />

www.GlobalMarkets.bnpparibas.com

to their pre-earthquake forecast, followed by a boost<br />

in 2012 as reconstruction activity gathers<br />

momentum. The reduction in growth comes from: the<br />

direct destruction of productive capacity in the<br />

affected regions; a disruption in production across<br />

Japan owing to limitations in power supply; increased<br />

risk aversion; and a decline in sentiment among<br />

household and businesses.<br />

The near-term disruptions to production have the<br />

most direct near-term implications for the rest of the<br />

world through supply-chain effects. While Japan has<br />

not been a driver of global growth for some time, it is<br />

still a source for key inputs in the automotive and<br />

electronics industry.<br />

Despite the restarting of some production featured in<br />

recent headlines, our Japan economists suggest that<br />

many large industrial companies continue to deal<br />

with disruptive shortages and limitations that will not<br />

be resolved easily in the near term. We simply need<br />

to wait and see how disruptive reduced production<br />

proves to be to the global supply chain.<br />

We look for a modest reduction in US economic<br />

growth in 2011 but a notable impact on the<br />

contour over the year<br />

Japan’s importance as a US trading partner has<br />

steadily declined in recent years (Chart 1). The<br />

country currently accounts for just 4.8% of all exports<br />

and 6% of imports. A reduction in domestic demand<br />

in Japan will likely translate into only a small<br />

reduction in the growth of US exports. Imports are<br />

also likely to be disrupted owing to production<br />

interruptions, with the impact concentrated on autos<br />

and electronics.<br />

The role of Japan is still quite significant in the motor<br />

vehicle industry as Japanese motor vehicle parts<br />

account for 13% of the US’s total imported motor<br />

vehicles and parts (Chart 2). The impact on auto<br />

availability will go beyond reduced availability of<br />

Japanese vehicles. For example, General Motors<br />

has announced the shutdown of plants in the US and<br />

Europe owing to reduced availability of Japanese<br />

parts.<br />

Auto parts are often model-specific, making it difficult<br />

to shift to other suppliers at short notice. The nearterm<br />

impact on auto sales will be mitigated by<br />

inventories on hand. The severity of the impact will<br />

therefore depend on how long the disruptions to<br />

Japanese production persist.<br />

US auto sales for March will be released next week<br />

and are likely to be largely unaffected by the<br />

interruptions in auto production following the<br />

Japanese earthquake. Auto sales had risen above<br />

13mn units saar in February on aggressive pricing<br />

Chart 4: Auto Pricing May Dampen Sales<br />

Source: Reuters EcoWin Pro<br />

Source: Reuters EcoWin Pro<br />

Chart 5: High Tech<br />

and improved consumer confidence and most<br />

analysts are looking for a March reading near<br />

February’s. Automakers have healthy levels of<br />

inventory on hand and can easily meet near-term<br />

demand (Chart 3). Beginning in April, US consumers<br />

are likely to see reduced model availability. Ward’s<br />

Automotive, a leading industry research organisation,<br />

suggested that supply limitations “almost certainly<br />

will put the brakes on April incentives, which will<br />

likely drive out price-conscious buyers who recently<br />

returned to the market”. It is looking for the pace of<br />

sales to drop “dramatically” in April, with continued<br />

sub-par sales likely to persist for a number of<br />

months. Demand for autos will be hurt by three<br />

factors:<br />

• Reduced availability of certain makes and<br />

models will reduce sales as some consumers will<br />

be unwilling to substitute to other models and will<br />

prefer to wait. Some substitution will likely occur,<br />

a development that could favour domestic<br />

producers, but such substitution is likely to be<br />

less than one for one.<br />

• The second factor hurting sales will be firmer<br />

pricing. With severe supply shortages,<br />

automakers will simply not need to offer the<br />

Julia Coronado/Yelena Shulyatyeva 24 March 2011<br />

Market Mover<br />

5<br />

www.GlobalMarkets.bnpparibas.com

aggressive incentives they have rolled out of late<br />

to clear their inventories. We expect an impact<br />

on pricing similar to what we saw during the<br />

bankruptcy of two of the big three US<br />

automakers (Chart 4). During that episode, the<br />

lack of positive profit margins led to firmer prices<br />

as automakers simply did not have the capacity<br />

to compete on price. This was a significant factor<br />

keeping sales subdued as consumers can simply<br />

extend the life of their current vehicle in many<br />

cases and wait for better pricing to return.<br />

• The third factor that will crimp sales is soaring<br />

gasoline prices. Japan specialises in the<br />

production of fuel-efficient models and engines.<br />

The lack of availability of these models and<br />

higher retail prices will be hitting just as gasoline<br />

prices will be reaching levels not seen since<br />

2008.<br />

Many consumers are likely to simply wait and see<br />

how these factors evolve before committing to a<br />

significant auto purchase.<br />

Autos and other durable goods have a powerful<br />

impact on consumer spending growth. The<br />

acceleration in consumption from 2.4% q/q saar in<br />

Q3 to 4.1% was entirely accounted for by a 21%<br />

surge in durables spending. Even if we were to see<br />

auto sales return to their Q4 2010 average of 12.4mn<br />

units in Q2 2011 from what is likely to be an average<br />

13.1mn pace in Q1, we could see a flat reading on<br />

consumer spending growth.<br />

We have reduced our forecast of real growth in<br />

consumption to 1.0% q/q saar. Consumer and<br />

business electronics are expected to be affected by<br />

some lack of availability in Q2 as well, and overall<br />

growth will suffer from a drag from inventories.<br />

Partially offsetting these factors should be a boost<br />

from trade as imports sag. On balance, the aftermath<br />

of the Japanese earthquake should bring a dip to<br />

1.5% q/q saar in US GDP growth in Q2 2011. This<br />

will be reflected broadly across economic indicators<br />

including the ISM indices, consumer confidence and<br />

retail sales.<br />

We then expect consumers and businesses to make<br />

up for lost time in spending and restocking in H2<br />

2011, with growth accelerating to 3.0% in Q3 and<br />

4.0% in Q4. The wild card will be how well business<br />

and consumer confidence hold up. We do expect<br />

some softening in the pace of hiring in Q2 but for the<br />

labour market to stay on a solid track. The labour<br />

market will be key to how markets interpret any<br />

sluggish numbers on activity.<br />

Policymakers are likely to continue along a<br />

gradual path toward normalisation<br />

In our baseline scenario, the US economy is stirred<br />

but not shaken. As in 2010, global events will lead to<br />

a soft patch from which the US economy will recover.<br />

Last year, the soft patch was accompanied by an<br />

aggressive accommodation from the Fed.<br />

However, this year, we expect the Fed to continue<br />

along its path toward gradual removal of policy<br />

accommodation. We think the Fed will end QE2 in<br />

June and hold the balance sheet steady by<br />

reinvesting the roll-off of the mortgage portfolio<br />

through at least September before allowing a gradual<br />

shrinking of the balance sheet and beginning a<br />

soaking up of excess reserves through reverse repos<br />

and the term deposit facility in early 2012. We<br />

continue to think the first rate hike will come in June<br />

2012.<br />

The US economy is clearly in a better place than<br />

when we hit the soft patch last year, and global and<br />

domestic inflationary pressures point to the need for<br />

a gradual normalisaton of policy. Of course,<br />

uncertainties abound and the Fed will remain nimble<br />

– although the potential for inflation to be a<br />

constraining factor has risen.<br />

Julia Coronado/Yelena Shulyatyeva 24 March 2011<br />

Market Mover<br />

6<br />

www.GlobalMarkets.bnpparibas.com

Japan: Fiscal Sustainability Now<br />

• If the financial markets were seriously<br />

worried about fiscal sustainability, the long-term<br />

interest rate would be rising and the yen<br />

weakening. <br />

• But in the week after the earthquake/tsunami<br />

term rates fell, the yen strengthened and share<br />

prices tumbled.<br />

• That subdued term rates and yen<br />

appreciation can coexist with the huge public<br />

debt is because Japan has succumbed to<br />

deflationary equilibrium, whereby funds<br />

continue to flow towards ‘safe’ assets.<br />

• But the earthquake disaster could bring<br />

forward the time when the debt reaches critical<br />

mass.<br />

• The most effective way to ensure that<br />

financing reconstruction does not trigger a<br />

fiscal crisis is for the government to<br />

concurrently announce plans for reconstruction<br />

and plans for long-term fiscal restructuring. The<br />

government should also give up on its favoured<br />

projects such as generous child benefits and rechannel<br />

that funding towards reconstruction.<br />

• There is a danger that the BoJ will be<br />

pressed into supplying funds for reconstruction.<br />

If the financial markets believe the BoJ is<br />

monetising the debt, deflationary equilibrium<br />

may be replaced by soaring inflation, surging<br />

term rates and a tanking yen.<br />

Chart 1: Japan's Share of Global Production of<br />

IT Electronics (%, 2009)<br />

IT Solution Service 9%<br />

Communications equipment<br />

Computers and data terminals<br />

Other electronic devices<br />

Semiconductors<br />

Dis play devices<br />

Electronic parts<br />

AV equipment<br />

Source: JEITA, <strong>BNP</strong> Paribas<br />

14%<br />

20%<br />

22%<br />

22%<br />

23%<br />

40%<br />

44%<br />

Japan's share<br />

(includes overseas<br />

production)<br />

Others<br />

0% 20% 40% 60% 80% 100%<br />

Chart 2: Combined Central and Local<br />

Government Debt (% of GDP, FY)<br />

200<br />

180<br />

160<br />

140<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10<br />

Source: Cabinet Office, <strong>BNP</strong> Paribas ** FY 2010 is our estimate.<br />

Doubts about Japan’s fiscal sustainability<br />

The massive earthquake/tsunamis that hit northern<br />

Japan on 11 March struck just as we were returning<br />

from the global forecasting meeting in New York. Our<br />

flight, in fact, was making its final approach to Narita<br />

Airport. However, after circling Narita several times,<br />

an announcement was made that we would be<br />

diverted to Nagoya. After landing at Nagoya, we<br />

were kept in the plane for roughly two hours, during<br />

which time we were inundated via BlackBerry with<br />

concerned messages from colleagues and clients.<br />

Beyond inquiries about our condition, we were<br />

repeatedly asked what the disaster (the Fukushima<br />

power station crisis was not yet known) meant for the<br />

Japanese economy and, especially, Japan’s already<br />

precarious fiscal condition. Questions included:<br />

Would the budget deficit swell even more if the<br />

disaster caused the economy to contract sharply,<br />

reducing tax receipts? Will the Kan administration<br />

have to forgo finalising plans in June for reforming<br />

social security, the single greatest cause of Japan’s<br />

chronic budget deficits? Will fiscal reform be further<br />

put off if the economy is weakened by the<br />

earthquake? Will the public debt snowball from the<br />

massive cost of reconstruction? With the public debt<br />

already at 180% of GDP, how will government<br />

spending on reconstruction be financed? With so<br />

many concerns about the fiscal ramifications of the<br />

earthquake, we address these concerns in this report.<br />

Disaster was actually followed by falling term<br />

rates, yen appreciation and weak share prices<br />

If the financial markets were seriously worried about<br />

the sustainability of Japan’s public debt, long-term<br />

interest rates would be rising and the yen weakening.<br />

But, contrary to the fears of some, what actually<br />

happened is that the week after the disaster saw<br />

Ryutaro Kono 24 March 2011<br />

Market Mover<br />

7<br />

www.GlobalMarkets.bnpparibas.com

term rates falling, the yen strengthening and share<br />

prices tumbling.<br />

Chart 3: Corporate Growth Expectations (real<br />

growth rate, %)<br />

While the drop in term rates, like the plunge in share<br />

prices, can be attributed to the market discounting<br />

economic deterioration from the earthquake, the<br />

yen’s strength – the cause of weak share prices<br />

owing to the damage to exporters’ earnings – could<br />

seem incongruent.<br />

7.0<br />

6.0<br />

5.0<br />

4.0<br />

3- Year Ahead<br />

5- Year Ahead<br />

Mechanism behind the yen’s appreciation<br />

As often evident in the financial markets, whenever<br />

uncertainties increase, there is a tendency to avoid<br />

risk assets in favour of safe assets. So did the<br />

disaster prompt a shift away from foreign currency<br />

and foreign-currency denominated assets with their<br />

relatively high risk in favour of the relative safety of<br />

the yen?<br />

Rampant speculation of such yen repatriation (by<br />

Japanese insurers to procure cash for payouts to<br />

policyholders, by Japanese banks to prepare for<br />

withdrawals, by corporations to prepare for<br />

emergencies) is deemed a cause of the yen’s recent<br />

appreciation.<br />

Whether there actually was massive repatriation or<br />

not is unclear but, in behavioural economics, what is<br />

important is the narrative justifying long positions on<br />

the yen – which act to bring about the expected yen<br />

appreciation.<br />

Will term rates remain subdued, even as the debt<br />

steadily grows?<br />

Even in the bond market, growing preference for safe<br />

assts (or speculation thereof) owing to heightened<br />

uncertainties, and not just bleak prospects for the<br />

economy, drove investors to buy government debt.<br />

Seeing how the cost of reconstruction will inevitably<br />

add to Japan’s already-huge public debt, will doubts<br />

of fiscal sustainability at some point prompt investors<br />

to dump JGBs and the yen?<br />

Disconnect with Japan’s public debt<br />

There has long been a disconnect between Japan’s<br />

huge public debt and the trends in prices, the yen<br />

and term rates. For a country such as Japan, with its<br />

dangerously high public debt, one would normally<br />

expect to find a tanking currency, soaring interest<br />

rates and high inflation. Instead what we have is yen<br />

appreciation, subdued interest rates and deflation.<br />

As pointed out in previous reports, this is because<br />

funds continue to flow towards government bonds, as<br />

private sector demand for funding has not revived<br />

owing to continued deflationary expectations and the<br />

dim prospects for economic growth. In other words,<br />

government debt can be smoothly absorbed because<br />

3.0<br />

2.0<br />

1.0<br />

0.0<br />

74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10<br />

Source: Cabinet office, <strong>BNP</strong> Paribas<br />

540<br />

520<br />

500<br />

480<br />

460<br />

440<br />

420<br />

Chart 4: Nominal GDP (CY, JPY trn)<br />

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10<br />

Source: Cabinet office, <strong>BNP</strong> Paribas<br />

private demand for funds is falling faster than debt<br />

issuance is increasing.<br />

Why subdued term rates and yen appreciation<br />

coexist with the huge public debt<br />

Because of lacklustre growth and deflation, tax<br />

receipts are not rising and the debt continues to<br />

expand. But the same lacklustre growth and deflation<br />

also keeps the long-term interest rate steady at low<br />

levels, thereby preventing Japan’s fiscal meltdown.<br />

Keeping the interest rate down is imperative for the<br />

authorities and market participants. A rising interest<br />

rate (for whatever reason) would cause debt<br />

servicing costs to soar, thereby increasing the risk<br />

that the debt will snowball out of control. Indeed, it<br />

seems as though Japan is choosing to forgo<br />

escaping from deflation and lacklustre growth in<br />

order to avoid a fiscal meltdown. As pointed out in<br />

earlier reports, because Japan has succumbed to a<br />

deflationary equilibrium of falling prices, super-low<br />

interest rates and weak growth, it is possible for<br />

subdued term rates and yen appreciation to coexist<br />

with the huge public debt.<br />

Ryutaro Kono 24 March 2011<br />

Market Mover<br />

8<br />

www.GlobalMarkets.bnpparibas.com

Bubble for safe assets creates deflationary<br />

equilibrium<br />

But the problem is that deflationary equilibrium is not<br />

a stable equilibrium and so will not last indefinitely.<br />

When the debt finally reaches critical mass,<br />

adjustments will begin in the form of a drop in real<br />

value and deflationary equilibrium will then be<br />

transformed into a new equilibrium.<br />

While some may feel that deflationary equilibrium<br />

can go on forever, the fact that that is not so<br />

becomes clear when we realise that the excessive<br />

preference for ‘safe’ assets (currency and<br />

government bonds) fostered by deflationary<br />

equilibrium has created a bubble for safe assets.<br />

Currently, owing to deflation, the real value at home<br />

and abroad of both the bonds issued by the<br />

government and the cash issued by the BoJ<br />

continues to rise. But the fact that these assets –<br />

ultimately only government-issued scraps of paper –<br />

acquire such added value makes them a kind of<br />

bubble. It is due to this bubble for the yen and<br />

government bonds that the yen strengthens, the term<br />

interest rate stays low and prices fall.<br />

Collapse of deflationary equilibrium<br />

Bubbles do not last, so when the bubble for safe<br />

assets bursts the reverse will occur. In other words,<br />

there will be a surge in inflation, tumbling bond prices<br />

(= soaring long-term interest rates) and yen<br />

depreciation. JGBs and the currency will revert to<br />

their pre-bubble price levels.<br />

While the severity of the adjustments will depend on<br />

the size of the bubble, if matters proceed to the point<br />

of critical mass for Japan’s public debt, the likely<br />

result will be higher inflation, a collapse in bond<br />

prices and huge currency depreciation.<br />

Deflationary equilibrium erodes the tax base<br />

We can also imagine the following. If the public debt<br />

is not reined in through rising inflation, tumbling bond<br />

prices and yen depreciation, then it could be adjusted<br />

using the proper means of tax increases and<br />

spending cuts. Unfortunately, the persistence of<br />

deflationary expectations and dim prospects for<br />

economic growth that keep private demand for funds<br />

stagnant also indicate that nominal GDP growth, the<br />

broadest measure of the tax base, will continue to<br />

shrink.<br />

Thus, with deflationary equilibrium eroding the tax<br />

base, it is unlikely that the public debt can be repaid<br />

through future tax receipts and spending cuts.<br />

Disaster could further swell safe-asset bubble<br />

If the current disaster has increased investor<br />

preference for ‘safe’ assets, the safe-asset bubble<br />

can be further inflated – bringing ever closer the<br />

moment of critical mass for the public debt. The<br />

downturn in the long-term interest rate could be a<br />

manifestation of further weakening of growth<br />

expectations.<br />

That said, reconstruction should trigger public-sector<br />

demand for funds over the intermediate term. Usually,<br />

when a nation’s capital stock is destroyed by war or<br />

disaster, the potential GDP level falls, while the<br />

potential growth rate itself is bolstered by<br />

reconstruction. Growth expectations could, therefore,<br />

pick up and the long-term interest rate could also rise<br />

somewhat.<br />

Critical mass for public debt brought forward<br />

The recent disaster has also created huge supply<br />

constraints for the Japanese economy. The disasterinduced<br />

economic contractions, therefore, do not<br />

only reflect weakened aggregate demand but also<br />

large-scale supply constraints brought about by the<br />

emergence of bottlenecks.<br />

Thus, it is possible that inflationary expectations<br />

could get the upper hand over deflationary<br />

expectations, resulting in higher long-term interest<br />

rates. If so, it might not be soon but the disaster<br />

could bring forward the time when the debt reaches<br />

critical mass.<br />

How to finance reconstruction<br />

Seeing how the public debt is a virtual time bomb<br />

with a fuse of unknown length, how should the<br />

country finance reconstruction? Some might feel that<br />

debt financing of reconstruction would not be a big<br />

problem provided it is an emergency one-off that is<br />

clearly predicated on repayment via future tax<br />

receipts. Such a view seems reasonable.<br />

But the government in its budget for FY 2010 and<br />

planned budget for FY 2011 already relies heavily on<br />

issuing debt to finance new permanent spending<br />

programmes. So the public may not readily support<br />

one-time emergency financing unless the authorities<br />

can fully explain it.<br />

Pork-barrel spending in the name of<br />

reconstruction cannot be allowed<br />

Care must be taken to ensure that reconstruction<br />

spending in the name of disaster relief does not<br />

include unrelated pork-barrel spending. For instance,<br />

after the Lehman shock, the authorities spent a huge<br />

amount of taxpayers’ money on coping with a ‘oncein-a-century<br />

crisis’, but those outlays included a lot of<br />

pork. So if a source of financing cannot be clearly<br />

secured, the government should forgo its child<br />

allowances and toll road reductions – budgetary<br />

items that the opposition parties adamantly oppose –<br />

and re-channel that funding toward reconstruction<br />

Ryutaro Kono 24 March 2011<br />

Market Mover<br />

9<br />

www.GlobalMarkets.bnpparibas.com

(revenue worth JPY 3.5 trillion could be secured by<br />

forgoing the DPJ’s favoured projects).<br />

Can’t plans for reconstruction and fiscal reform<br />

be concurrently announced?<br />

Of course, if the government announces its plans for<br />

reconstruction and long-term fiscal restructuring<br />

simultaneously, the market would not harbour doubts<br />

about Japan’s fiscal sustainability. Announcing both<br />

together would be the most effective way to ensure<br />

that the unveiling of one policy to counter a crisis<br />

(reconstruction) does not trigger another crisis (fiscal<br />

meltdown).<br />

If doubts about fiscal sustainability mount, the<br />

financial system will inevitably be shaken owing to<br />

the huge JGB holdings of most domestic financial<br />

institutions. Some might question the feasibility of<br />

realising credible plans for fiscal reform at this time of<br />

crisis. However, the very fact that this is the worst<br />

crisis since WWII should make it possible for<br />

politicians of all stripes to put aside their partisan<br />

differences and work together for the good of the<br />

country.<br />

Danger of financing by BoJ<br />

In closing, we want to express our concern that the<br />

BoJ could be pressed into supplying funds to finance<br />

reconstruction. On 14 March, the BoJ moved to<br />

double the size of its outright asset purchasing<br />

programme introduced last October. Thus, in the<br />

event the government issues bonds to pay for<br />

reconstruction, we suspect that some might feel that<br />

the BoJ should support this by buying such debt.<br />

Seeing how Japan faces a national emergency, more<br />

and more politicians would probably concur. (The<br />

media, in fact, are already suggesting this kind of<br />

BoJ cooperation.)<br />

Consequences of monetisation<br />

Regardless of the label, government bonds are<br />

government bonds and the purchasing of same by<br />

the central bank constitutes monetisation.<br />

Monetisation could cause bonds and the currency to<br />

lose value, resulting in high inflation, soaring term<br />

interest rates and a plunging yen. History has shown<br />

that, all too often in Japan, emergency measures end<br />

up morphing into routine policy. Voters should not<br />

forget that the BoJ started underwriting government<br />

debt during the Great Depression as an emergency<br />

measure. Of course, our concerns will be groundless<br />

if reconstruction is undertaken alongside a credible<br />

package of fiscal reforms.<br />

Without credible fiscal reform, support from the BoJ<br />

would be very dangerous. If the financial markets<br />

believe the BoJ is monetising the debt, deflationary<br />

equilibrium will instantly end – to be replaced by<br />

soaring inflation, surging term rates and a tanking<br />

yen. We must not let policies to counter one crisis<br />

create conditions for another.<br />

Ryutaro Kono 24 March 2011<br />

Market Mover<br />

10<br />

www.GlobalMarkets.bnpparibas.com

Japan: When Will Power Rationing End?<br />

• Japan is in for two more quarters of<br />

contraction, triggered not by the usual demand<br />

shock but by supply constraints.<br />

• Tepco’s power generation for the Kanto<br />

area, down 25%, will constrain the supply of<br />

goods and services in areas unaffected by the<br />

earthquake. Meanwhile, the disrupting of supply<br />

chains has put manufacturing at risk of grinding<br />

to a halt.<br />

• Whether or not the blackouts will really end<br />

in April is key. According to our calculations,<br />

the recovery of two of Tepco’s four damaged<br />

thermal power plants by April should allow<br />

electrical capacity to cover demand in May and<br />

June. This suggests rationing could indeed end<br />

as scheduled.<br />

• But demand for power will again exceed<br />

capacity in the summer and winter. Tepco is<br />

striving to cope by acquiring gas turbine power<br />

generation systems, which should help alleviate<br />

the power shortage in Q3.<br />

Economic slowdown will be due to supply shock<br />

Because of the bottleneck of insufficient electrical<br />

power and disrupted supply chains, Japan is in for<br />

two more quarters of negative growth (-4.0%<br />

annualised in Q1 2011 and -10.0% in Q2 on our<br />

forecasts). While weakening national sentiment will<br />

certainly weigh on aggregate demand, the economic<br />

slowdown this time will largely be due to supply<br />

constraints. In this sense, the slowdown will be like<br />

none in recent memory in that it will not be triggered<br />

by a demand shock.<br />

Supply constraint of insufficient power<br />

For starters, beyond the damage to production<br />

activities in the quake-hit Tohoku region, the supply<br />

of goods and services in the Kanto region – the<br />

economic heart of the country comprising the<br />

prefectures of Tokyo, Ibaraki, Tochigi, Gunma,<br />

Saitama, Chiba, Kanagawa, Yamanashi, and part of<br />

Shizuoka – will be severely constrained by the<br />

diminished supply of electricity.<br />

Power generation by Tepco (the company supplying<br />

the Kanto region) is down roughly 25%, meaning<br />

daytime rolling blackouts on weekdays will have to<br />

continue. This imposes a great burden on factory<br />

operations as production lines have to be shut down<br />

each time blackouts occur, and some companies<br />

have suspended operations entirely as quality would<br />

be affected by momentarily stopping operations.<br />

Chart 1: Expected Power Demand in Tepco's<br />

Service Area (million kW)<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

March<br />

April<br />

May<br />

June<br />

July<br />

August<br />

Source: Tepco, <strong>BNP</strong> Paribas<br />

Note: Expected power demand is average for last two years.<br />

Chart 2: Expected Power Demand versus Power<br />

Capacity (million kW)<br />

70<br />

60<br />

50<br />

40<br />

30<br />

20<br />

10<br />

0<br />

March<br />

April<br />

May<br />

June<br />

July<br />

August<br />

Some factories in the area affected by power<br />

rationing thus remain inoperative all day long. That<br />

said, because companies can regulate their<br />

operations as they deem fit, including running<br />

production lines at night when power demand<br />

declines, and department stores and other retailers<br />

also have leeway to adjust their operating hours, the<br />

damage to economic activity might be limited.<br />

Disrupted supply chains stall manufacturing<br />

Manufacturing in particular, with its well-developed<br />

and tightly managed supply chains, is at risk of<br />

grinding to a halt if supplies run out. This could<br />

constrain economic activity in areas and sectors not<br />

affected by power rationing. Of course, with effort<br />

and ingenuity in finding new suppliers and/or shifting<br />

production to unaffected areas, the problems of<br />

bottlenecks and disrupted supply chains can be<br />

September<br />

September<br />

October<br />

October<br />

November<br />

November<br />

December<br />

Shortage<br />

December<br />

January<br />

January<br />

Power capacity<br />

Source: Tepco, <strong>BNP</strong> Paribas<br />

Note: Expected capacity is based on Tepco estimates and other sources.<br />

February<br />

February<br />

Ryutaro Kono/ Makiko Fukuda 24 March 2011<br />

Market Mover<br />

11<br />

www.GlobalMarkets.bnpparibas.com

overcome, but it will take time before conditions<br />

return to normal.<br />

End of power rationing should allow a return to<br />

growth in Q3<br />

The Kanto area did not sustain significant earthquake<br />

or tsunami damage, so infrastructure and capital<br />

stock are essentially intact. Thus, economic activity<br />

in the area should quickly return to normal levels<br />

once the rolling blackouts end. Tepco has indicated<br />

that its rolling blackouts will stop at the end of April.<br />

If this turns out to be the case, we believe the<br />

economy will return to growth in Q3 (5.9%<br />

annualised in Q3, 10.5% in Q4 and 1.9% in Q1 2012)<br />

on the back of reconstruction demand. But owing to<br />

the expected contractions in Q1 and Q2, growth in<br />

2011 overall will be negative: our forecast is -0.9%.<br />

Will blackouts really end in April?<br />

Whether the blackouts will really end in April or not<br />

depends on the state of power generation at that<br />

time. Currently, four of Tepco’s thermal power plants<br />

are out of operation: Hirono plant in Fukushima,<br />

Hitachinaka and Kashima plants in Ibaraki, and<br />

Higashi Ohgishima plant in Kanagawa. According to<br />

Tepco, operations should resume at Higashi<br />

Ohgishima in March and at the Kashima plant in April.<br />

Damage at the other two plants was more extensive<br />

so repairing them will take more time.<br />

Based on Tepco’s maximum capacity and estimates<br />

of likely demand (past two-year average), the return<br />

to operations by the Higashi Ohgishima plant will<br />

mean that the electricity shortage in April won’t be as<br />

bad as in March. Nevertheless, shortages will still<br />

exist, making continued rationing necessary.<br />

In May and June, assuming the plants in Higashi<br />

Ohgishima and Kashima are generating at maximum<br />

capacity, generation should just cover expected<br />

demand. Thus, there is a good chance that rolling<br />

blackouts will indeed end in April.<br />

Power shortages likely in summertime<br />

The problem, however, is summertime electric<br />

consumption (Q3), when usage of power soars<br />

alongside rising temperatures. On our calculations,<br />

Tepco’s likely maximum capacity of 4.7 million kW<br />

will be exceeded by estimated demand of 5.7 million<br />

kW in July-August and 5.1 million kW in September.<br />

That means some form of rationing will probably<br />

have to resume. So unless something is done to<br />

cope with summertime demand for air conditioning,<br />

economic activity could again be constrained in Q3.<br />

What is more, demand for heating from December<br />

onwards could trigger another round of power<br />

shortages. Based on our calculation of Tepco’s<br />

capacity, we believe supply could be greater than<br />

first thought in Q2 but slightly less in Q3.<br />

Chart 3: Tepco’s Expected Power Demand and<br />

Power Capacity (million kW)<br />

*Electric sales<br />

(billion kw)<br />

*Electric<br />

demand<br />

*Expected<br />

capacity<br />

Shortage<br />

March 237.3 50.1 34.0 -16.1<br />

April 243.0 42.9 40.0 -2.9<br />

May 222.7 43.0 44.0 1.0<br />

June 218.7 45.9 46.0 0.1<br />

July 257.6 57.3 47.0 -10.3<br />

August 277.7 56.9 47.0 -9.9<br />

September 286.8 51.1 47.0 -4.1<br />

October 229.4 42.3 47.0 4.7<br />

November 222.0 47.4 47.0 -0.4<br />

December 229.1 48.9 47.0 -1.9<br />

January 263.8 51.3 47.0 -4.3<br />

February 50.3 47.0 -3.3<br />

Source: Tepco, <strong>BNP</strong> Paribas<br />

Note: *Electric sales: Figures for 2010, forecasts for 2011.<br />

* Expected power demand is average for last two years.<br />

* Expected capacity is based on Tepco estimates and other sources.<br />

Chart 4: Tepco's Suspended Power Operations<br />

Location<br />

Total<br />

capacity<br />

(million kW) (Share)<br />

Termal power<br />

Fukushima<br />

3.8 (5.9%)<br />

Ibaraki<br />

1.0 (1.6%)<br />

Ibaraki<br />

4.4 (6.8%)<br />

Kanagawa<br />

2.0 (3.1%)<br />

Nuclear power<br />

Fukushima<br />

4.3 (6.6%)<br />

Fukushima<br />

4.4 (6.8%)<br />

Total 19.9 (30.8%)<br />

Tepco's total maximum capacity 64.5<br />

Source: Tepco, <strong>BNP</strong> Paribas<br />

Tepco to acquire new gas turbine power<br />

generation systems<br />

Meanwhile, Tepco has announced plans to acquire<br />

gas turbine power generation systems to ease the<br />

electricity shortage expected this summer. If the new<br />

systems are those that generate 300k kW, setting up<br />

the new power stations should be easy they should<br />

only take a few months to construct. Bringing these<br />

systems online should help alleviate the power<br />

shortage in Q3.<br />

Power cannot be transferred throughout Japan<br />

If power could be transferred from parts of Japan<br />

unaffected by the disaster, the electricity shortage in<br />

the Kanto area could be eased. Unfortunately, this is<br />

easier said than done because AC power<br />

frequencies are not the same throughout the country<br />

(Japan is the only country to use both 50Hz and<br />

60Hz). In Japan, the western part of the country<br />

(Kansai area and west) uses 60Hz and the eastern<br />

part (Kanto area and east) uses 50Hz.<br />

While there are a several substations that can<br />

convert between frequencies and transfer electricity<br />

from Kansai to Kanto, their capacity to do so is<br />

limited to only 1-1.2 million kilowatts; the shortfall is<br />

10 times that.<br />

Ryutaro Kono/ Makiko Fukuda 24 March 2011<br />

Market Mover<br />

12<br />

www.GlobalMarkets.bnpparibas.com

Global: Supply Chain Disruptions<br />

• We present below stories on supply-chain<br />

disruptions caused by the Japan earthquake<br />

which have appeared in the media since 11<br />

March.<br />

• Although some companies have resumed<br />

production in Japan, the impact of the disaster<br />

will be longer lasting for others.<br />

note, as the stories below show, some companies<br />

have resumed their operations over the past week or<br />

started to boost production in the factories located in<br />

unaffected areas in Japan. However, there is also<br />

evidence that that the negative impact of the<br />

earthquake will be long-lasting for some other<br />

companies, with some saying that they are<br />

considering temporarily shifting production overseas.<br />

• In the rest of the world, supply chain<br />

disruption is causing delays or cuts to<br />

production and poses upside risks to prices.<br />

Following Japan’s earthquake/tsunami on 11 March,<br />

one of the major concerns is the impact of these<br />

events on global economic activity. In the last issue<br />

of Market Mover (17 March 2011), the economics<br />

team published a number of articles assessing the<br />

economic impact of the developments in Japan on<br />

other parts of the world.<br />

In this piece, we focus on the anecdotal evidence of<br />

the effects on the supply chain. The earthquake and<br />

the tsunami have caused significant disruptions to<br />

the power supply and logistics generally in Japan.<br />

Given Japan is a key supplier of hi-tech products,<br />

this points to possible spillovers to other economies<br />

being considerable.<br />

In the box below, we present some stories that have<br />

appeared in the media over the past two weeks<br />

regarding the impact of the Japanese events on the<br />

supply chain, production and prices. On a positive<br />

In the rest of the world, there is evidence that supply<br />

chain disruption is causing delays or cuts to<br />

production. The decisions of some car manufacturers<br />

to cut output of vehicles in the US and Europe (or<br />

discussions on doing so) are just some to quote. On<br />

the prices front, there are already concerns that<br />

supply disruptions could drive prices of key<br />

technology parts and consumer electronic goods<br />

higher.<br />

Overall, anecdotal evidence supports our view that<br />

this is a shock to supply as well as demand, for the<br />

rest of the world. Supply chain disruptions look<br />

severe and greater than for past natural disasters.<br />

Supply disruptions may lead to some substitution for<br />

other countries’ products (which in itself suggests the<br />

negative impact on global growth would be reduced).<br />

However, such disruptions are affecting the ability of<br />

companies elsewhere to produce goods. It is difficult<br />

to gauge the magnitude of these at this stage, but the<br />

direct and indirect effects of the Japanese<br />

earthquake will reduce global growth this year in our<br />

view.<br />

Box 1: Anectodal Evidence of the Impact of Japan Quake on Supply Chain and Production<br />

Japan<br />

• The Samsung/Toshiba factory in Yokkaichi, which supplies over 40% of the world's NAND flash and DRAM chips, was<br />

stopped during the earthquake. But it is now back up and running. (14 March, electroiq.com)<br />

• The prospect of extended supply disruption caused by Japan's earthquake drove prices for key technology parts higher. (16<br />

March, canada.com)<br />

• Fuji Heavy Industries Ltd. said that it will soon restart production of some autoparts at Gunma Prefecture factories. (21 March,<br />

nikkei.com)<br />

• Toyota Motor Corp. is considering halting domestic production of completed vehicles within the week due to the difficulty of<br />

procuring parts in the wake of the earthquake. The automaker has yet to set a production schedule beyond 28 March, though<br />

it has resumed domestic production of parts for overseas use. (22 March, nikkei.com)<br />

• Sony Corp. said it has partially resumed production at a lithium-ion battery plant operated by Sony Energy Device Corp in<br />

quake-hit Tochigi Prefecture. But production lines will be suspended until 31 March at five plants. Sony said it will consider<br />

shifting production to overseas plants temporarily if the parts shortage continues. (22 March, nikkei.com)<br />

• Production has stopped at roughly 70% of domestic plants that produce zinc. (22 March, nikkei.com)<br />

• Hitachi Chemical Co., which controls more than 40% of the global market for a negative electrode material for Li-ion batteries,<br />

has been forced to halt operations at a plant in Ibaraki Prefecture. (22 March, nikkei.com)<br />

• Panasonic Corp said it has resumed operations at its Koriyama plant in Fukushima Prefecture. (23 March, nikkei.com)<br />

• Fujitsu Ltd. said it has resumed some operations at one of its chip-manufacturing factories in quake-struck northern Japan.<br />

(23 March, nikkei.com)<br />

Gizem Kara/Hiroshi Shiraishi/Mole Hau/Bricklin Dwyer 24 March 2011<br />

Market Mover<br />

13<br />

www.GlobalMarkets.bnpparibas.com

Asia Ex-Japan<br />

• Semiconductor makers in Taiwan face a "fight to get raw materials" as 50% of the world's silicon wafer stock comes from two<br />

Japanese firms, Shin-Etsu and Sumco Corp., both affected by the quake. (14 March, pcworld.com)<br />

• Taiwan-based digital camera makers Altek and Ability pointed out that they have already confirmed deliveries with their<br />

Japan-based upstream CCD suppliers and are currently seeing no shortages in short-term supply. However, longer term,<br />

suppliers could see issues from their own upstream material suppliers, as well as problems with transportation and power. (14<br />

March, digitimes.com)<br />

• Automobile production is continuing as usual at the three Toyota Motor Thailand (TMT) factories. (15 March,<br />

aseanaffairs.com)<br />

• STATS ChipPac said delivery schedules could be affected if the logistics pile-up in Japan drags on. (16 March,<br />

businesstimes.com)<br />

• "A prolonged abnormalcy in Japan will certainly affect the material supplies . . . as, incidentally, most of the electronics<br />

industry locators in the Philippines are Japanese-owned companies," Ernesto Santiago, Semiconductor and Electronics<br />

Industries in the Philippines Inc. President, said. (16 March, aseanaffairs.com)<br />

• Malaysian state oil firm Petronas said it will supply extra LNG to Japan after the earthquake forced the shutdown of several<br />

nuclear power plants, prompting increased demand for gas. (19 March, topix.com)<br />

• GM Korea Co. said that it will reduce production to prepare for a possible lack of automotive parts from Japan, following a<br />

similar decision by Renault SA's subsidiary in South Korea. (21 March, WSJ)<br />

• Chinese Dongfeng Automobile, which set up a joint venture with Nissan, imports most of its auto components from Japan. An<br />

insider said inventory will run out by end of March and production will be halted by then. (21 March, stock.591hx.com)<br />

• Chinese Shenzhen Success Electronics Co., which is a producer of LCD, imports LCD glass substrate, polarized glass and<br />

some electronic components from Japan. The company said the logistics bottleneck may affect the delivery schedule and that<br />

they can purchase polarized glass and other electronic components from South Korean, Taiwanese and mainland suppliers.<br />

(21 March, stock.591hx.com)<br />

• Chinese TCL corporation invests in a programme to produce liquid crystal panels. 80% of its manufacturing equipment relies<br />

on imports from a Japanese producer called AGC. Due to the disruption to Japanese logistics, the company said the whole<br />

program will be delayed. (21 March, stock.591hx.com)<br />

• Indonesian coal shipments to Japan are being redirected to China because of delays and damage at ports. (22 March,<br />

thejakartaglobe.com)<br />

• Local auto assemblers in Philippines are facing delays in their supplies of completely built-up vehicles and assembly parts<br />

from Japan. (22 March, mb.com)<br />

• US solar power companies are among those facing disruptions to supply. (14 March, Reuters)<br />

• Apple Inc.'s iPad 2 tablet may run into supply problems, as some hard-to-replace parts come from Japan. (18 March,<br />

nikkei.com)<br />

• General Motors has been forced to close its Shrevesport, Louisiana facility due to supply problems. (18 March,<br />

ewallstreeter.com)<br />

US<br />

• Boeing Co. officials said they are working out how to deal with possible airplane-parts shortages from suppliers in Japan. (18<br />

March, WSJ)<br />

• Caterpillar Inc. said disruptions in its supply chain in Japan could sporadically affect the company's assembly plants<br />

elsewhere in the world. (18 March, WSJ)<br />

• Honda is suspending May orders for Japan-made vehicles from U.S. dealers. (19 March, WSJ)<br />

Europe<br />

• The price of consumer electronic goods such as computers, mobile phones and DVDs could rise across the world due to<br />

shortage of electronic components from Japan. (16 March, guardian.co.uk)<br />

• The British arm of Honda said it was operating normally, although there are wider concerns in the industry about supply<br />

shortages. (16 March, guardian.co.uk)<br />

• Swedish group Ericsson said that although it expects its supply of components to be affected, it does not expect a material<br />

impact on its Q1 2011 sales. (16 March, supplychainstandard.com)<br />

• Peugeot has started to reduce production of diesel cars, due to a lack of Hitachi-made electronic components. However, the<br />

Hitachi factory has recently restarted production at a slow pace. (22 March, latribune.fr)<br />

• General Motors Co., Toyota Motor Corp. and PSA Peugeot-Citroën have cut or are making plans to curb output of thousands<br />

of vehicles in the US and Europe due to concerns about a shortage of critical parts made in Japan. (24 March, WSJ)<br />

Source: The date and sources are in parentheses after each story.<br />

Gizem Kara/Hiroshi Shiraishi/Mole Hau/Bricklin Dwyer 24 March 2011<br />

Market Mover<br />

14<br />

www.GlobalMarkets.bnpparibas.com

Eurozone: Holding Firm<br />

• The sentiment surveys for March released to<br />

date show little adverse impact from the recent<br />

run of unfavourable news.<br />

• Regarding the spillovers from the problems<br />

in Japan, there may be lags until the disruption<br />

to supply chains becomes more evident.<br />

• Price developments in the surveys show a<br />

continuation of the elevation of input costs and<br />

further signs of pass-through.<br />

2.0<br />

1.5<br />

1.0<br />

0.5<br />

0.0<br />

-0.5<br />

-1.0<br />

Chart 1: French PMI & Growth<br />

Composite PMI:<br />

Output (RHS)<br />

70<br />

65<br />

60<br />

55<br />

50<br />

45<br />

40<br />

• In addition to the data flow, recent speeches<br />

suggest that the ECB is likely to follow through<br />

on its ‘heads up’ for a rate rise in early April.<br />

-1.5<br />

GDP % q/q<br />

35<br />

-2.0<br />

30<br />

98 99 00 01 02 03 04 05 06 07 08 09 10 11<br />

Source: Reuters EcoWin Pro<br />

Chart 2: German PMI & Growth<br />

Strong surveys…<br />

The recent run of surveys across a number of ‘core’<br />

eurozone countries have shown sentiment holding up<br />

remarkably well given the flow of adverse news over<br />

the last few weeks.<br />

2.0<br />

1.0<br />

0.0<br />

Composite PMI:<br />

Output (RHS)<br />

65<br />

60<br />

55<br />

50<br />

In France especially, the data have been remarkably<br />

strong. The monthly business sentiment index from<br />

INSEE rose by three points in March to 109, its<br />

highest level since March 2008. The sub-index of<br />

‘own company’ output expectations, which is typically<br />

a good guide to actual output growth trends, jumped<br />

from +17 to +25, its strongest level since late 2000.<br />

The sub-index of orders from overseas also rose<br />

strongly in March.<br />

Echoing the INSEE survey, the French 'flash' PMI for<br />

March also came in strong. The composite index for<br />

output rose from 59.0 to 59.6, a whisker away from<br />

its cycle peaks over the past decade (Chart 1). The<br />

PMI is a pretty good gauge of growth momentum but<br />

it has tended to over-state growth since the financial<br />

crisis. The PMIs for services (from 59.7 to 60.7) and<br />

for manufacturing (from 55.7 to 56.6) both showed<br />

improvement relative to February.<br />

…in the core of the eurozone…<br />

In big-picture terms, Germany's 'flash' PMI data for<br />

March were pretty similar. The composite PMI output<br />

index came in at 60.6, down a little from 60.9 in the<br />

prior month, but still consistent with unusually strong<br />

growth. As we have been stressing for a long while<br />

now, the 0.4% q/q rise in German GDP in Q4 last<br />

year was not representative of the underlying growth<br />

momentum in Germany. Our forecast for Q1 GDP is<br />

a q/q increase of 1%, more in line with the signals<br />

from the composite PMI (Chart 2).<br />

-1.0<br />

-2.0<br />

-3.0<br />

-4.0<br />

20<br />

98 99 00 01 02 03 04 05 06 07 08 09 10 11<br />

Source: Reuters EcoWin Pro<br />

GDP (% q/q)<br />

The German PMIs continue to highlight the broaderbased<br />

nature of the expansion, another recurring<br />

theme of our analysis. The services PMI rose to 60.1<br />

in March, not far short of its manufacturing sibling,<br />

which slipped to 60.9. The German economy is very<br />

sensitive to external developments but domestic<br />

demand is playing an increasingly important role in<br />

the strength of German growth.<br />

…with Germany’s labour market tightening<br />

A striking difference between Germany and other<br />

countries, including the US in particular, is the state<br />

of the labour market. The composite PMI’s sub-index<br />

for employment in Germany rose to a record high in<br />

March (of 57.4).<br />

The manufacturing PMI’s sub-index for employment<br />

is at an exceptionally high level. At 60.6 in March, it<br />

is indicative of a further strong rise in the demand for<br />

labour in the sector (Chart 3), at a time when labour<br />

shortages are already being reported.<br />

45<br />

40<br />

35<br />

30<br />

25<br />

Ken Wattret 24 March 2011<br />

Market Mover<br />

15<br />

www.GlobalMarkets.bnpparibas.com

Divergence continues<br />

At the eurozone level, the 'flash' PMI data for March<br />

showed activity across sectors is still very elevated<br />

but less spectacularly so than in France and<br />

Germany. This points to considerable divergence<br />

between the conditions in the core and periphery,<br />

which will be evident in the complete national<br />

breakdown of the PMI figures early next month.<br />

Despite the divergence, the eurozone service sector<br />

PMI for March was robust at 56.9, its highest level<br />

since August 2007. The manufacturing PMI, in<br />

contrast, slipped from 59.0 to 57.7 but this is a pretty<br />

strong reading nonetheless. Given the softening in<br />

the manufacturing data, the composite PMI for the<br />

eurozone lost some ground in March but at 57.5, it is<br />

still indicative of q/q GDP growth of at least twice the<br />

rate seen in Q4 last year (of 0.3%).<br />

Lagged effects<br />

In sum, there appears to be little disruption so far to<br />

the improvement in eurozone economic conditions<br />

which has been evident since last autumn. Note that<br />

the survey period for the PMI figures this month ran<br />

from 11 March onwards, the day of the earthquake in<br />

Japan, so the data ought to be an accurate reflection<br />

of activity trends.<br />

That said, it is too soon to conclude that there will be<br />

no disruption from developments in Japan. Lags may<br />

be an issue given the nature of the problem. The<br />

potential disruption to supply chains due to output<br />

shutdowns in Japan may take a while to show<br />

through as companies are able to use their existing<br />

inventory for the time being. Either way, the fact that<br />

the data remain so strong suggests that the damage<br />

to confidence from events in Japan, and in the MENA<br />

region, has been very limited to date.<br />

Price pressures<br />

The survey data on the activity side have reinforced<br />

the markets’ (and our own) belief that the ECB is<br />

likely to go ahead with its proposed policy tightening<br />

next month. The relationship between the composite<br />

PMI and policy changes is a pretty solid one and the<br />

PMI is clearly in the tightening zone (Chart 4). The<br />

same is true on the pricing side of the surveys.<br />

The input price sub-index of the eurozone composite<br />

PMI rose for the sixth straight month in March and is<br />

a whisker shy of its record highs. The output price<br />

sub-index went sideways in March but it too remains<br />

elevated by past standards. There has been only one<br />

month in the history of the series in which the output<br />

price sub-index of the PMI has been higher than its<br />

current level (in July 2008, when the ECB opted to<br />

hike rates with inflation well above target and inflation<br />

expectations high and rising).<br />

4<br />

3<br />

2<br />

1<br />

0<br />

-1<br />

-2<br />

-3<br />

-4<br />

-5<br />

-6<br />

Chart 3: German PMI & Employment<br />

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11<br />

Source: Reuters EcoWin Pro<br />

Employment in Industry (% y/y)<br />

Manufacturing PMI: Employment<br />

(RHS, 3Mth Lag)<br />

Chart 4: Composite PMI & Policy Changes<br />

0.50<br />

0.25<br />

0.00<br />

-0.25<br />

-0.50<br />

-0.75<br />

Change in Refi Rate (bp)<br />

-1.00<br />

35<br />

98 99 00 01 02 03 04 05 06 07 08 09 10 11<br />

Source: Reuters EcoWin Pro<br />

Composite PMI (RHS)<br />

The pricing surveys are particularly elevated in the<br />

manufacturing sector. While the input price sub-index<br />

slipped back a little in March, the level of 83.0 would<br />

have represented a record high in any other month<br />

but February. The manufacturing output price subindex,<br />

meanwhile, rose to yet another record high of<br />

61.4 in March, suggesting that there is some passthrough<br />

from higher input costs – a prominent cause<br />

for concern at the ECB.<br />

Rate rise on the cards<br />

The speeches from various ECB officials in the last<br />

few days have all pointed to the same conclusion.<br />

While the decision to raise rates has not yet formally<br />

been made, the assessment of the fundamentals in<br />

early March still applies.<br />

A common theme of some of the speeches has been<br />

the concern expressed over the potential adverse<br />

consequences of keeping interest rates too low for<br />

too long. This concern is unlikely to be extinguished<br />

by a sole 25bp rate rise, suggesting that the market<br />

is right to have re-priced in a series of hikes this year.<br />

The ECB staff inflation projections going forward are<br />

likely to support this conclusion.<br />

65<br />

60<br />

55<br />

50<br />

45<br />

40<br />

35<br />

30<br />

60<br />

55<br />

50<br />

45<br />

40<br />

Ken Wattret 24 March 2011<br />

Market Mover<br />

16<br />

www.GlobalMarkets.bnpparibas.com

Portugal: Towards the EFSF<br />

• The political crisis triggered by Mr Socrates’<br />

resignation makes it virtually inevitable that the<br />

country will have to seek external financial<br />

support.<br />

Chart 1: Net Financial Assets (% GDP)<br />

• However, this is complicated in the short<br />

term, as the caretaker government has not got<br />

the mandate to negotiate the terms of a possible<br />

bailout.<br />

• The ECB will probably come to the rescue<br />

but markets will remain nervous.<br />

• It is encouraging that Spanish paper has not<br />

been greatly affected by the Portuguese crisis.<br />

• But the crisis is still a reminder of the<br />

consolidation effort required in a number of<br />

countries will be very challenging from a<br />

political point of view.<br />