BHRUT annual report 2009 - Barking Havering and Redbridge ...

BHRUT annual report 2009 - Barking Havering and Redbridge ...

BHRUT annual report 2009 - Barking Havering and Redbridge ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Annual Report & Accounts <strong>2009</strong>-2010<br />

79<br />

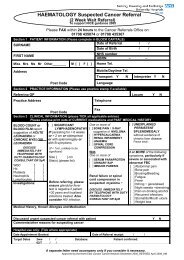

39.2 Capital cost absorption rate<br />

The trust was required to absorb the cost of capital at<br />

a rate of 3.5% of forecast average relevant net assets.<br />

The rate is calculated as the percentage that dividends<br />

paid on public dividend capital, totalling for <strong>2009</strong>/10<br />

£4549k, bearing to the actual average relevant net<br />

assets of £129,978k, that is 3.5% (2008/09 3.1%)<br />

From <strong>2009</strong>/10 the dividend payable on public dividend<br />

capital is based on the actual (rather than forecast)<br />

average relevant net assets <strong>and</strong> therefore the actual<br />

capital cost absorption rate is automatically 3.5%.<br />

39.3 External financing<br />

The Trust is given an external financing limit which it is permitted to undershoot<br />

<strong>2009</strong>/10 2008/09<br />

£000 £000<br />

External financing limit (22,374) (20,388)<br />

Cash flow financing (14,098) 13,441<br />

Finance leases taken out in the year 2,026 0<br />

Other capital receipts 0 0<br />

External financing requirement (12,072) 13,441<br />

Undershoot/(overshoot) (10,302) (33,829)<br />

The EFL is set by the Department of Health <strong>and</strong><br />

determines how much (or less) cash than that<br />

generated by its activites the Trust can spend in a year.<br />

It is initially set at planning stage early in the year. The<br />

Trust's EFL was based on its original planned deficit of<br />

£24.7m, which would have led to a cash requirement<br />

of £11.7m, allowing for non-cash items such as<br />

impairments <strong>and</strong> depreciation plus capital expenditure.<br />

The out-turn was a deficit of £56.2m, which with<br />

non-cash items gives a cash requirement of £25.6m,<br />

some £13.9m more than planned. Within the year, the<br />

Trust received Public Dividend Captial of £5.0m, which<br />

was covered by an EFL adjustment, leaving £8.9m<br />

uncovered. In year, London SHA did recognise the<br />

causes of the Trust's financial pressures <strong>and</strong> increased<br />

the Trust's planned deficit from £24.7m to £54.1m.<br />

£18m of this increase was due to non-cash items such<br />

as unforeseen fixed asset impairments, the remaining<br />

£11.4m requiring cash. Although the increased deficit<br />

was supported by the SHA, the DH did not adjust the<br />

Trust's EFL. Overshooting the EFL means that the Trust<br />

has used more cash in year than the DH intended; it<br />

does not give rise to a present or future liability to the<br />

DH.<br />

Annual Accounts

![[4] Biopsy Leaflet.pub - Barking, Havering and Redbridge University ...](https://img.yumpu.com/51285530/1/190x134/4-biopsy-leafletpub-barking-havering-and-redbridge-university-.jpg?quality=85)