Annual report 2004 (PDF, 4141 kB) - Unicredit Bank

Annual report 2004 (PDF, 4141 kB) - Unicredit Bank

Annual report 2004 (PDF, 4141 kB) - Unicredit Bank

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

In <strong>2004</strong> and 2003, the <strong>Bank</strong> did not restructure any of its receivables from banks. In <strong>2004</strong> and<br />

2003 the <strong>Bank</strong> classified all claims from banks as standard.<br />

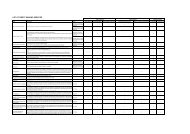

5 DUE FROM CUSTOMERS<br />

31 December <strong>2004</strong><br />

CZK m<br />

31 December 2003<br />

CZK m<br />

Public sector 98 72<br />

Financial sector 863 1 421<br />

Non-financial sector - legal persons 20 873 19 567<br />

Physical persons 3 307 2 158<br />

25 141 23 218<br />

Allowance for impaired loans (Note 10) - 621 - 432<br />

24 520 22 786<br />

In addition to the allowance for impaired loans the <strong>Bank</strong> has reflected a general provision<br />

for loans of CZK 256 million at 31 December <strong>2004</strong> (31 December 2003: CZK 410 million).<br />

This provision has to be utilised or written back to income by 31 December 2005 (Note 2(p),<br />

Note 10).<br />

The <strong>Bank</strong> restructured CZK 159 million of its loans and receivables in <strong>2004</strong> (31 December<br />

2003: CZK 134 million). Loans and other receivables are considered as restructured in case<br />

that the <strong>Bank</strong> grants relief to clients because it is likely that the <strong>Bank</strong> would incur losses if<br />

acting otherwise. Roll-over of a short-term loan is not considered to be restructuring of the<br />

loan in the case where the client has fulfilled all requirements of loan agreements.<br />

As at 31 December <strong>2004</strong> the <strong>Bank</strong> led syndicate loans of CZK 167 million (31 December<br />

2003: CZK 167 million).<br />

(a)<br />

Quality of loan portfolio<br />

Loans are categorised in accordance with the definitions issued by the CNB in five categories<br />

(standard, watch, substandard, doubtful, loss). Impaired loans include substandard, doubtful<br />

and loss loans and represent total outstanding principal and accrued interest receivable with<br />

service payments overdue more than 90 days or other defaults in contractual terms<br />

or financial performance. Watch loans are usually overdue between 30 – 90 days or other<br />

risks characteristic are presented. Administration of impaired receivables, including their<br />

recovery, is performed by a separate department in the <strong>Bank</strong>.The <strong>Bank</strong> does not apply<br />

a portfolio approach to the categorisation of receivables. Each receivable is considered<br />

individually, as is also the case for the creation of provisions.<br />

26