Auto Dealerships - Audit Technique Guide - Uncle Fed's Tax*Board

Auto Dealerships - Audit Technique Guide - Uncle Fed's Tax*Board Auto Dealerships - Audit Technique Guide - Uncle Fed's Tax*Board

Chapter 9 Alternative LIFO for Auto Dealers As you were reading the chapter regarding the LIFO Method of Inventory Valuation, it probably occurred to you that LIFO computations are complex. To simplify the dollar-value computation for auto dealerships, Rev. Proc. 92-79, 1992-2 C.B. 457, Alternative LIFO Method, was published, superseded by Rev. Proc. 97-36, I.R.B. 1997-33, 14 (July 31, 1997). In general, the Alternative LIFO Method is a comprehensive dollar-value, link-chain LIFO method of accounting that encompasses several LIFO sub-methods and may only be used by an automobile dealer engaged in the trade or business of retail sales of new automobiles or new lightduty trucks to value its inventory of new automobiles and new light-duty trucks. The Alternative LIFO Method is designed to simplify the dollar value computations of automobile dealers. It does this by not requiring comparability adjustments from one year to the next. Under the authority of Treas. Reg. section 1.446-1(c)(2)(ii), the Commissioner will waive strict adherence of Treas. Reg. section 1.472-8 comparability requirement in applying the Alternative LIFO Method provided that a taxpayer complies with the requirements stated in the revenue procedure. Summary of Rules The Alternative LIFO Method is available to any automobile dealer engaged in the business of retail sales of new automobiles or new light-duty trucks for its LIFO inventories of new automobiles and new light-duty trucks. Light-duty trucks are trucks with a gross vehicle weight of 14,000 pounds or less, which are also referred to as class 1, 2, or 3 trucks. Discussion of pertinent areas of this revenue procedure are summarized in the following paragraphs. LIFO Pools The revenue procedure was not intended to change the pooling rules and all rules in effect prior to Rev. Proc. 92-79 remain in effect. All new automobiles and demonstrators (regardless of manufacturer) must be included in one LIFO pool and all new light trucks and demonstrators (regardless of manufacturer) must be included in another separate LIFO pool. Section 4.02(1) states that pools must be established for each "separate trade or business." There is little guidance on just what constitutes a separate trade or business. However, certain factors such as the location of multiple franchises, whether there is separate management, personnel and recordkeeping functions at each location can be used to determine whether each franchise is a separate trade or business. 9-1

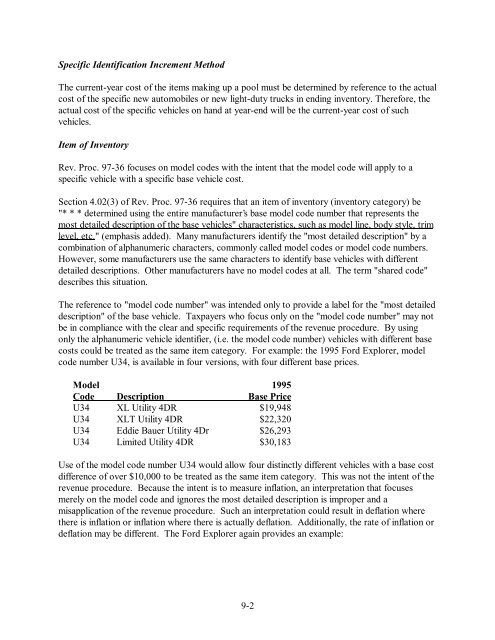

Specific Identification Increment Method The current-year cost of the items making up a pool must be determined by reference to the actual cost of the specific new automobiles or new light-duty trucks in ending inventory. Therefore, the actual cost of the specific vehicles on hand at year-end will be the current-year cost of such vehicles. Item of Inventory Rev. Proc. 97-36 focuses on model codes with the intent that the model code will apply to a specific vehicle with a specific base vehicle cost. Section 4.02(3) of Rev. Proc. 97-36 requires that an item of inventory (inventory category) be "* * * determined using the entire manufacturer’s base model code number that represents the most detailed description of the base vehicles" characteristics, such as model line, body style, trim level, etc." (emphasis added). Many manufacturers identify the "most detailed description" by a combination of alphanumeric characters, commonly called model codes or model code numbers. However, some manufacturers use the same characters to identify base vehicles with different detailed descriptions. Other manufacturers have no model codes at all. The term "shared code" describes this situation. The reference to "model code number" was intended only to provide a label for the "most detailed description" of the base vehicle. Taxpayers who focus only on the "model code number" may not be in compliance with the clear and specific requirements of the revenue procedure. By using only the alphanumeric vehicle identifier, (i.e. the model code number) vehicles with different base costs could be treated as the same item category. For example: the 1995 Ford Explorer, model code number U34, is available in four versions, with four different base prices. Model 1995 Code Description Base Price U34 XL Utility 4DR $19,948 U34 XLT Utility 4DR $22,320 U34 Eddie Bauer Utility 4Dr $26,293 U34 Limited Utility 4DR $30,183 Use of the model code number U34 would allow four distinctly different vehicles with a base cost difference of over $10,000 to be treated as the same item category. This was not the intent of the revenue procedure. Because the intent is to measure inflation, an interpretation that focuses merely on the model code and ignores the most detailed description is improper and a misapplication of the revenue procedure. Such an interpretation could result in deflation where there is inflation or inflation where there is actually deflation. Additionally, the rate of inflation or deflation may be different. The Ford Explorer again provides an example: 9-2

- Page 31 and 32: c. Reconcile (2): Beginning Trial B

- Page 33 and 34: 3 Repair Order Sales 4 Parts Sales

- Page 35 and 36: Conclusion Although intimidating at

- Page 37 and 38: Chapter 5 Balance Sheet Why do we c

- Page 39 and 40: When an adjustment to a balance she

- Page 41 and 42: Part 2 Inventory Chapter 6 General

- Page 43 and 44: . Purchasing c. Handling, processin

- Page 45 and 46: dealerships use specific identifica

- Page 47 and 48: Chapter 7 LIFO Background Overview

- Page 49 and 50: A Short History of LIFO Application

- Page 51 and 52: improper inflation through unwarran

- Page 53 and 54: Introduction Chapter 8 Computing LI

- Page 55 and 56: The double extension index formula

- Page 57 and 58: as one item, there would probably n

- Page 59 and 60: (existing items) and non-comparable

- Page 61 and 62: The current-year costs that can be

- Page 63 and 64: Assuming the dealership elects LIFO

- Page 65 and 66: matching of revenues and costs. Thu

- Page 67 and 68: section 1.471-9. Both of these regu

- Page 69 and 70: providing to the credit subsidiary

- Page 71 and 72: Under elections made prior to Decem

- Page 73 and 74: Base Year Cost 9112 $224,000 You ha

- Page 75 and 76: BLS Sanity Check A simpler means to

- Page 77 and 78: CYC = Current Year Cost. This is th

- Page 79 and 80: Computation of 1993 Increment and R

- Page 81: This page intentionally left blank.

- Page 85 and 86: which may be identified by a unique

- Page 87 and 88: Step # 3 For each item category, ad

- Page 89 and 90: Step # 10 Compute the total cost of

- Page 91 and 92: 1991 Inventory Value at Current Yea

- Page 93 and 94: This page intentionally left blank.

- Page 95 and 96: Dealers may offer the contracts as

- Page 97 and 98: This page intentionally left blank.

- Page 99 and 100: 2. Principal/Obligor A principal is

- Page 101 and 102: Rev. Proc. 97-38 provided for an al

- Page 103 and 104: Contract Construction Generally, a

- Page 105 and 106: Rev. Proc. 97-27 provides the admin

- Page 107 and 108: The Court ruled that when the deale

- Page 109 and 110: Considerations for Forming a Produc

- Page 111 and 112: The Reinsurance Transaction To illu

- Page 113 and 114: insurance contract reinsured throug

- Page 115 and 116: (1979). The Service’s position is

- Page 117 and 118: While not all captive situations in

- Page 119 and 120: 3. IRC section 845 tax avoidance 4.

- Page 121 and 122: section, seemingly compliant arrang

- Page 123 and 124: 2. By owner A dealer may own dealer

- Page 125 and 126: Rules and Regulations Many rules re

- Page 127 and 128: This page intentionally left blank.

- Page 129 and 130: One of the assets specifically iden

- Page 131 and 132: Where a covenant may be enforced it

Specific Identification Increment Method<br />

The current-year cost of the items making up a pool must be determined by reference to the actual<br />

cost of the specific new automobiles or new light-duty trucks in ending inventory. Therefore, the<br />

actual cost of the specific vehicles on hand at year-end will be the current-year cost of such<br />

vehicles.<br />

Item of Inventory<br />

Rev. Proc. 97-36 focuses on model codes with the intent that the model code will apply to a<br />

specific vehicle with a specific base vehicle cost.<br />

Section 4.02(3) of Rev. Proc. 97-36 requires that an item of inventory (inventory category) be<br />

"* * * determined using the entire manufacturer’s base model code number that represents the<br />

most detailed description of the base vehicles" characteristics, such as model line, body style, trim<br />

level, etc." (emphasis added). Many manufacturers identify the "most detailed description" by a<br />

combination of alphanumeric characters, commonly called model codes or model code numbers.<br />

However, some manufacturers use the same characters to identify base vehicles with different<br />

detailed descriptions. Other manufacturers have no model codes at all. The term "shared code"<br />

describes this situation.<br />

The reference to "model code number" was intended only to provide a label for the "most detailed<br />

description" of the base vehicle. Taxpayers who focus only on the "model code number" may not<br />

be in compliance with the clear and specific requirements of the revenue procedure. By using<br />

only the alphanumeric vehicle identifier, (i.e. the model code number) vehicles with different base<br />

costs could be treated as the same item category. For example: the 1995 Ford Explorer, model<br />

code number U34, is available in four versions, with four different base prices.<br />

Model 1995<br />

Code Description Base Price<br />

U34 XL Utility 4DR $19,948<br />

U34 XLT Utility 4DR $22,320<br />

U34 Eddie Bauer Utility 4Dr $26,293<br />

U34 Limited Utility 4DR $30,183<br />

Use of the model code number U34 would allow four distinctly different vehicles with a base cost<br />

difference of over $10,000 to be treated as the same item category. This was not the intent of the<br />

revenue procedure. Because the intent is to measure inflation, an interpretation that focuses<br />

merely on the model code and ignores the most detailed description is improper and a<br />

misapplication of the revenue procedure. Such an interpretation could result in deflation where<br />

there is inflation or inflation where there is actually deflation. Additionally, the rate of inflation or<br />

deflation may be different. The Ford Explorer again provides an example:<br />

9-2