Estimation, Evaluation, and Selection of Actuarial Models

Estimation, Evaluation, and Selection of Actuarial Models

Estimation, Evaluation, and Selection of Actuarial Models

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

14 CHAPTER 2. MODEL ESTIMATION<br />

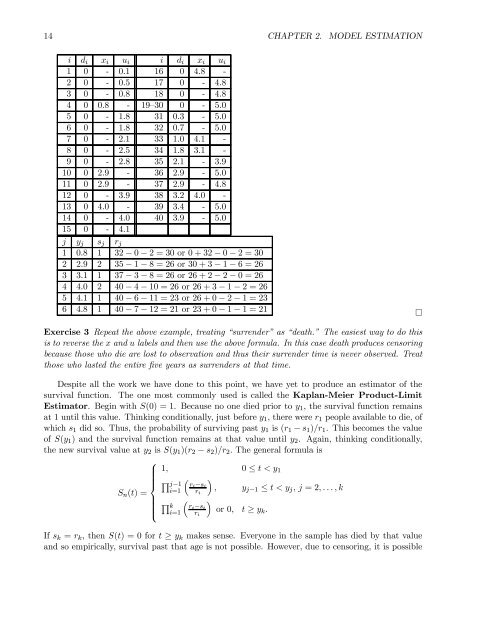

i d i x i u i i d i x i u i<br />

1 0 - 0.1 16 0 4.8 -<br />

2 0 - 0.5 17 0 - 4.8<br />

3 0 - 0.8 18 0 - 4.8<br />

4 0 0.8 - 19—30 0 - 5.0<br />

5 0 - 1.8 31 0.3 - 5.0<br />

6 0 - 1.8 32 0.7 - 5.0<br />

7 0 - 2.1 33 1.0 4.1 -<br />

8 0 - 2.5 34 1.8 3.1 -<br />

9 0 - 2.8 35 2.1 - 3.9<br />

10 0 2.9 - 36 2.9 - 5.0<br />

11 0 2.9 - 37 2.9 - 4.8<br />

12 0 - 3.9 38 3.2 4.0 -<br />

13 0 4.0 - 39 3.4 - 5.0<br />

14 0 - 4.0 40 3.9 - 5.0<br />

15 0 - 4.1<br />

j y j s j r j<br />

1 0.8 1 32 − 0 − 2=30or 0+32− 0 − 2=30<br />

2 2.9 2 35 − 1 − 8=26or 30 + 3 − 1 − 6=26<br />

3 3.1 1 37 − 3 − 8=26or 26 + 2 − 2 − 0=26<br />

4 4.0 2 40 − 4 − 10 = 26 or 26 + 3 − 1 − 2=26<br />

5 4.1 1 40 − 6 − 11 = 23 or 26 + 0 − 2 − 1=23<br />

6 4.8 1 40 − 7 − 12 = 21 or 23 + 0 − 1 − 1=21<br />

¤<br />

Exercise 3 Repeat the above example, treating “surrender” as “death.” The easiest way to do this<br />

is to reverse the x <strong>and</strong> u labels <strong>and</strong> then use the above formula. In this case death produces censoring<br />

because those who die are lost to observation <strong>and</strong> thus their surrender time is never observed. Treat<br />

those who lasted the entire fiveyearsassurrendersatthattime.<br />

Despitealltheworkwehavedonetothispoint,wehaveyettoproduceanestimator<strong>of</strong>the<br />

survival function. The one most commonly used is called the Kaplan-Meier Product-Limit<br />

Estimator. Begin with S(0) = 1. Because no one died prior to y 1 , the survival function remains<br />

at 1 until this value. Thinking conditionally, just before y 1 , there were r 1 people available to die, <strong>of</strong><br />

which s 1 did so. Thus, the probability <strong>of</strong> surviving past y 1 is (r 1 − s 1 )/r 1 .Thisbecomesthevalue<br />

<strong>of</strong> S(y 1 ) <strong>and</strong> the survival function remains at that value until y 2 . Again, thinking conditionally,<br />

the new survival value at y 2 is S(y 1 )(r 2 − s 2 )/r 2 . The general formula is<br />

⎧<br />

1, 0 ≤ t