Scania Annual Report 2011

Scania Annual Report 2011 Scania Annual Report 2011

112 notes to the consolidated financial statements NOTE 16 Equity, continued The share capital of Scania AB consists of 400,000,000 Series A shares outstanding with voting rights of one vote per share and 400,000,000 Series B shares outstanding with voting rights of 1/10 vote per share. A and B shares carry the same right to a portion of the company’s assets and profit. The nominal value of both A and B shares is SEK 2.50 per share. All shares are fully paid and no shares are reserved for transfer of ownership. No shares are held by the company itself or its subsidiaries. Contributed equity consists of a statutory reserve contributed by the owners of Scania AB when it became a limited company in 1995. The hedge reserve consists of the change in market value of commercial cash flow hedging instruments in cases where hedge accountin g is applied according to IAS 39, “Financial Instruments: Recognition and Measurement”. The currency translation reserve arises when translating net asset s outside Sweden according to the current method of accounting. The currency translation reserve also includes currency rate differences related to monetary items for businesses outside Sweden deemed to be a part of the company’s net investment. The negative exchange rate difference of SEK –719 m. arose as a result of the Swedish krona’s appreciation against currencies important to Scania. The exchange rate differences were mainly due to the krona’s appreciation against the Brazilian real. Retained earnings consist not only of accrued profits but also of the change in pension liability attributable to changes in actuarial gains and losses etc. recognised in “Total other comprehensive income”. Regardin g changes in actuarial assumptions, see also Note 17, “Provisions for pensions and similar commitments”. The Parent Company’s dividend related to 2010 was SEK 4,000 m., equivalent to SEK 5.00 per share. The proposed dividend related to 2011 is SEK 4,000 m., equivalent to SEK 5.00 per share. Non-controlling interest refers to the share of equity that belongs to external interests without a controlling influence in certain subsidiaries of the Scania Group. The equity of the Scania Group consists of the sum of equity attribut able to Scania’s shareholders and equity attributable to noncontrolling interests. At year-end 2011, the Group’s equity totalled SEK 34,512 m. (30,036). According to the Group’s Financial Policy, the Group’s financial position shall meet the requirements of the business objectives it has established. At present, this is deemed to presuppose a financial position equivalent to the requirements for obtaining at least an A– credit rating from the most important rating institutions. In order to maintain the necessary capital structure, the Group may adjust the amount of its dividend to shareholders, distribute capital to the shareholders or sell assets and thereby reduce debt. Financial Services includes twelve companies that are subject to oversight by national financial inspection authorities. In some countries, Scania must comply with local capital adequacy requirements. During 2011, these units met their capital adequacy requirements. The Group’s Financial Policy contains targets for key ratios related to the Group’s financial position. These coincide with the ratios used by credit rating institutions. Scania’s credit rating according to Standard and Poor’s at the end of 2011 was for: • long-term borrowing: A– • outlook: Stable • short-term borrowing: A–2 • short-term borrowing, Sweden: K–1. Reconciliation of change in number of shares outstanding 2011 2010 2009 Number of A shares outstanding, 1 January 400,000,000 400,000,000 400,000,000 Number of A shares outstanding, 31 December 400,000,000 400,000,000 400,000,000 Number of B shares outstanding, 1 January 400,000,000 400,000,000 400,000,000 Number of B shares outstanding, 31 December 400,000,000 400,000,000 400,000,000 Total number of shares, 31 December 800,000,000 800,000,000 800,000,000 financial reports Scania 2011

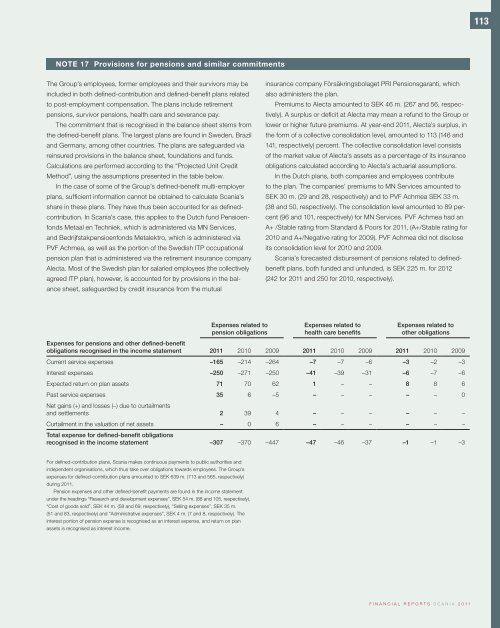

113 NOTE 17 Provisions for pensions and similar commitments The Group’s employees, former employees and their survivors may be included in both defined-contribution and defined-benefit plans related to post-employment compensation. The plans include retirement pension s, survivor pensions, health care and severance pay. The commitment that is recognised in the balance sheet stems from the defined-benefit plans. The largest plans are found in Sweden, Brazi l and Germany, among other countries. The plans are safeguarded via reinsured provisions in the balance sheet, foundations and funds. Calcula tions are performed according to the “Projected Unit Credit Method”, using the assumptions presented in the table below. In the case of some of the Group’s defined-benefit multi-employer plans, sufficient information cannot be obtained to calculate Scania’s share in these plans. They have thus been accounted for as definedcontribution. In Scania’s case, this applies to the Dutch fund Pensioenfonds Metaal en Techniek, which is administered via MN Services, and Bedrijfstakpensioenfonds Metalektro, which is administered via PVF Achmea, as well as the portion of the Swedish ITP occupational pension plan that is administered via the retirement insurance company Alecta. Most of the Swedish plan for salaried employees (the collectively agreed ITP plan), however, is accounted for by provisions in the balance sheet, safeguarded by credit insurance from the mutual insurance company Försäkringsbolaget PRI Pensionsgaranti, which also administers the plan. Premiums to Alecta amounted to SEK 46 m. (267 and 56, respectively). A surplus or deficit at Alecta may mean a refund to the Group or lower or higher future premiums. At year-end 2011, Alecta’s surplus, in the form of a collective consolidation level, amounted to 113 (146 and 141, respectively) percent. The collective consolidation level consists of the market value of Alecta’s assets as a percentage of its insurance obligations calculated according to Alecta’s actuarial assumptions. In the Dutch plans, both companies and employees contribute to the plan. The companies’ premiums to MN Services amounted to SEK 30 m. (29 and 28, respectively) and to PVF Achmea SEK 33 m. (38 and 50, respec tively). The consolidation level amounted to 89 percent (96 and 101, respectively) for MN Services. PVF Achmea had an A+ /Stable ratin g from Standard & Poors for 2011, (A+/Stable rating for 2010 and A+/Negative rating for 2009). PVF Achmea did not disclose its consolidation level for 2010 and 2009. Scania’s forecasted disbursement of pensions related to definedbenefit plans, both funded and unfunded, is SEK 225 m. for 2012 (242 for 2011 and 250 for 2010, respectively). Expenses related to pension obligations Expenses related to health care benefits Expenses related to other obligations Expenses for pensions and other defined-benefit obligations recognised in the income statement 2011 2010 2009 2011 2010 2009 2011 2010 2009 Current service expenses –165 –214 –264 –7 –7 –6 –3 –2 –3 Interest expenses –250 –271 –250 –41 –39 –31 –6 –7 –6 Expected return on plan assets 71 70 62 1 – – 8 8 6 Past service expenses 35 6 –5 – – – – – 0 Net gains (+) and losses (–) due to curtailments and settlements 2 39 4 – – – – – – Curtailment in the valuation of net assets – 0 6 – – – – – – Total expense for defined-benefit obligations recognised in the income statement –307 –370 –447 –47 –46 –37 –1 –1 –3 For defined-contribution plans, Scania makes continuous payments to public authorities and independent organisations, which thus take over obligations towards employees. The Group’s expenses for defined-contribution plans amounted to SEK 639 m. (713 and 565, respectively) during 2011. Pension expenses and other defined-benefit payments are found in the income statement under the headings “Research and development expenses”, SEK 54 m. (88 and 105, respectively), “Cost of goods sold”, SEK 44 m. (58 and 69, respectively), “Selling expenses”, SEK 35 m. (51 and 83, respectively) and “Administrative expenses”, SEK 4 m. (7 and 8, respectively). The interes t portion of pension expense is recognised as an interest expense, and return on plan assets is recognised as interest income. financial reports Scania 2011

- Page 64 and 65: 62 Risks and risk management Produc

- Page 66 and 67: 64 CORPORATE GOVERNANCE REPORT owne

- Page 68 and 69: 66 CORPORATE GOVERNANCE REPORT The

- Page 70 and 71: 68 CORPORATE GOVERNANCE REPORT by t

- Page 72 and 73: 70 BOARD OF DIRECTORS Board of Dire

- Page 74 and 75: 72 EXECUTIVE BOARD AND CORPORATE UN

- Page 76 and 77: financial reports Amounts in tables

- Page 78 and 79: 76 group financial review Group fin

- Page 80 and 81: 78 group financial review During 20

- Page 82 and 83: 80 consolidated income statements C

- Page 84 and 85: 82 consolidated balance sheets Cons

- Page 86 and 87: 84 Consolidated statement of change

- Page 88 and 89: 86 notes to the consolidated financ

- Page 90 and 91: 88 notes to the consolidated financ

- Page 92 and 93: 90 notes to the consolidated financ

- Page 94 and 95: 92 notes to the consolidated financ

- Page 96 and 97: 94 notes to the consolidated financ

- Page 98 and 99: 96 notes to the consolidated financ

- Page 100 and 101: 98 notes to the consolidated financ

- Page 102 and 103: 100 notes to the consolidated finan

- Page 104 and 105: 102 notes to the consolidated finan

- Page 106 and 107: 104 notes to the consolidated finan

- Page 108 and 109: 106 notes to the consolidated finan

- Page 110 and 111: 108 notes to the consolidated finan

- Page 112 and 113: 110 notes to the consolidated finan

- Page 116 and 117: 114 notes to the consolidated finan

- Page 118 and 119: 116 notes to the consolidated finan

- Page 120 and 121: 118 notes to the consolidated finan

- Page 122 and 123: 120 notes to the consolidated finan

- Page 124 and 125: 122 notes to the consolidated finan

- Page 126 and 127: 124 notes to the consolidated finan

- Page 128 and 129: 126 notes to the consolidated finan

- Page 130 and 131: 128 notes to the consolidated finan

- Page 132 and 133: 130 notes to the consolidated finan

- Page 134 and 135: 132 notes to the consolidated finan

- Page 136 and 137: 134 notes to the consolidated finan

- Page 138 and 139: 136 notes to the consolidated finan

- Page 140 and 141: 138 parent company financial statem

- Page 142 and 143: 140 notes to the parent company fin

- Page 144 and 145: 142 proposed guidelines for salary

- Page 146 and 147: 144 audit report Audit Report TRANS

- Page 148 and 149: 146 quarterly data Quarterly data,

- Page 150 and 151: 148 key financial ratios and figure

- Page 152 and 153: 150 multi-year statistical review M

- Page 154 and 155: 152 The Annual Report contains forw

- Page 156: Scania AB (publ), SE-151 87 Södert

113<br />

NOTE 17 Provisions for pensions and similar commitments<br />

The Group’s employees, former employees and their survivors may be<br />

included in both defined-contribution and defined-benefit plans related<br />

to post-employment compensation. The plans include retirement<br />

pension s, survivor pensions, health care and severance pay.<br />

The commitment that is recognised in the balance sheet stems from<br />

the defined-benefit plans. The largest plans are found in Sweden, Brazi l<br />

and Germany, among other countries. The plans are safeguarded via<br />

reinsured provisions in the balance sheet, foundations and funds.<br />

Calcula tions are performed according to the “Projected Unit Credit<br />

Method”, using the assumptions presented in the table below.<br />

In the case of some of the Group’s defined-benefit multi-employer<br />

plans, sufficient information cannot be obtained to calculate <strong>Scania</strong>’s<br />

share in these plans. They have thus been accounted for as definedcontribution.<br />

In <strong>Scania</strong>’s case, this applies to the Dutch fund Pensioenfonds<br />

Metaal en Techniek, which is administered via MN Services,<br />

and Bedrijfstakpensioenfonds Metalektro, which is administered via<br />

PVF Achmea, as well as the portion of the Swedish ITP occupational<br />

pension plan that is administered via the retirement insurance company<br />

Alecta. Most of the Swedish plan for salaried employees (the collectively<br />

agreed ITP plan), however, is accounted for by provisions in the balance<br />

sheet, safeguarded by credit insurance from the mutual<br />

insurance company Försäkringsbolaget PRI Pensionsgaranti, which<br />

also administers the plan.<br />

Premiums to Alecta amounted to SEK 46 m. (267 and 56, respectively).<br />

A surplus or deficit at Alecta may mean a refund to the Group or<br />

lower or higher future premiums. At year-end <strong>2011</strong>, Alecta’s surplus, in<br />

the form of a collective consolidation level, amounted to 113 (146 and<br />

141, respectively) percent. The collective consolidation level consists<br />

of the market value of Alecta’s assets as a percentage of its insurance<br />

obligations calculated according to Alecta’s actuarial assumptions.<br />

In the Dutch plans, both companies and employees contribute<br />

to the plan. The companies’ premiums to MN Services amounted to<br />

SEK 30 m. (29 and 28, respectively) and to PVF Achmea SEK 33 m.<br />

(38 and 50, respec tively). The consolidation level amounted to 89 percent<br />

(96 and 101, respectively) for MN Services. PVF Achmea had an<br />

A+ /Stable ratin g from Standard & Poors for <strong>2011</strong>, (A+/Stable rating for<br />

2010 and A+/Negative rating for 2009). PVF Achmea did not disclose<br />

its consolidation level for 2010 and 2009.<br />

<strong>Scania</strong>’s forecasted disbursement of pensions related to definedbenefit<br />

plans, both funded and unfunded, is SEK 225 m. for 2012<br />

(242 for <strong>2011</strong> and 250 for 2010, respectively).<br />

Expenses related to<br />

pension obligations<br />

Expenses related to<br />

health care benefits<br />

Expenses related to<br />

other obligations<br />

Expenses for pensions and other defined-benefit<br />

obligations recognised in the income statement <strong>2011</strong> 2010 2009 <strong>2011</strong> 2010 2009 <strong>2011</strong> 2010 2009<br />

Current service expenses –165 –214 –264 –7 –7 –6 –3 –2 –3<br />

Interest expenses –250 –271 –250 –41 –39 –31 –6 –7 –6<br />

Expected return on plan assets 71 70 62 1 – – 8 8 6<br />

Past service expenses 35 6 –5 – – – – – 0<br />

Net gains (+) and losses (–) due to curtailments<br />

and settlements 2 39 4 – – – – – –<br />

Curtailment in the valuation of net assets – 0 6 – – – – – –<br />

Total expense for defined-benefit obligations<br />

recognised in the income statement –307 –370 –447 –47 –46 –37 –1 –1 –3<br />

For defined-contribution plans, <strong>Scania</strong> makes continuous payments to public authorities and<br />

independent organisations, which thus take over obligations towards employees. The Group’s<br />

expenses for defined-contribution plans amounted to SEK 639 m. (713 and 565, respectively)<br />

during <strong>2011</strong>.<br />

Pension expenses and other defined-benefit payments are found in the income statement<br />

under the headings “Research and development expenses”, SEK 54 m. (88 and 105, respectively),<br />

“Cost of goods sold”, SEK 44 m. (58 and 69, respectively), “Selling expenses”, SEK 35 m.<br />

(51 and 83, respectively) and “Administrative expenses”, SEK 4 m. (7 and 8, respectively). The<br />

interes t portion of pension expense is recognised as an interest expense, and return on plan<br />

assets is recognised as interest income.<br />

financial reports <strong>Scania</strong> <strong>2011</strong>