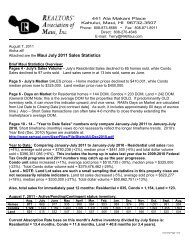

125 page Presentation - REALTORS® Association of Maui, Inc.

125 page Presentation - REALTORS® Association of Maui, Inc.

125 page Presentation - REALTORS® Association of Maui, Inc.

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Prepared for the<br />

Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong><br />

July 8, 2011<br />

by Paul H. Brewbaker,<br />

Principal, TZ Economics<br />

<strong>Maui</strong> Housing: Double-Dip?<br />

Dip?<br />

Single-dip, and this is IT!<br />

Copyright 2011<br />

Paul H. Brewbaker, Ph.D.

Where is Hawaii in the cycle?<br />

Slide copyright 2011, TZ Economics<br />

1

Extracting the underlying trend from seasonally-<br />

adjusted data clearly reveals recession/recovery cycle<br />

Monthly, in million $, s.a., (log scale)<br />

140<br />

120<br />

100<br />

80<br />

GE tax (right scale)<br />

WH on wages (left)<br />

U.S. recessions shaded<br />

200<br />

100<br />

Monthly, in million $, s.a., (log scale)<br />

00 02 04 06 08 10<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DoTAX, DBEDT; smoothing using Hodrick-Prescott filter by TZE<br />

2

Extracting the signal from the noise (through May):<br />

Hawaii general fund revenue is in cyclical recovery*<br />

Monthly in million $, s.a., log scale<br />

400<br />

300<br />

200<br />

*So stop acting like it isn’t<br />

02 03 04 05 06 07 08 09 10 11 12<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT, DLIR; seasonal adjustment using Census X-12 ARIMA filter and Hodrick-Prescott filter extraction<br />

<strong>of</strong> private employment trend by TZE<br />

3

Home price indexes: long-term housing returns are<br />

equated by arbitrage, but supply constraints<br />

amplify Hawaii’s s valuation cycle<br />

Index, 1985Q1 = 100, s.a., log scale<br />

400<br />

200<br />

100<br />

50<br />

Hawaii<br />

Iowa<br />

Colorado<br />

U.S. recessions shaded<br />

80 85 90 95 00 05 10 15<br />

Restricting development only<br />

increases the amplitude <strong>of</strong><br />

the home price valuation<br />

cycle and makes life better for<br />

high net-worth real estate<br />

investors who can carry<br />

wealth through the trough<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Housing Finance Agency (http://www.fhfa.gov/Default.aspx?Page=87) from sales prices and<br />

appraisals; seasonal adjustment, index rebasing and regression by TZ Economics<br />

4

The cycle in production (homebuilding)—new new units—Hawaii<br />

and U.S.; is there such a glut <strong>of</strong> housing in Hawaii?<br />

4.0<br />

4.0<br />

Quarterly, thousand units, s.a., log scale<br />

2.0<br />

1.0<br />

0.5<br />

Hawaii<br />

U.S.<br />

2.0<br />

1.0<br />

0.5<br />

80 85 90 95 00 05 10 15<br />

Quarterly, million units, s.a.a.r., log scale<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Bank <strong>of</strong> St. Louis (http://research.stlouisfed.org/fred2/series/HOUST/downloaddata?cid=32302),<br />

Hawaii DBEDT, County Building Departments; seasonal adjustment and trend extract <strong>of</strong> Hawaii data by TZE<br />

5

Make the appropriate macroeconomic comparisons<br />

across space and time: what stands out?<br />

• This is not the mainland (duh) so don’t act as if everything that happens<br />

there matters here<br />

• Which is more relevant to Hawaii: the NBC Nightly News (KHNL TV) or<br />

the news from NHK Tokyo (Hawaii Public Television)? Which gets more<br />

viewers?<br />

• Hawaii’s economic experience is dichotomous: Oahu and the Neighbor<br />

Islands have had different Great Recession outcomes<br />

Slide copyright 2011, TZ Economics<br />

6

Real Hawaii personal income indexed to last three<br />

cyclical peaks: this recession was not Hawaii’s s worst<br />

110<br />

P T<br />

Index, cyclical peak = 100 (log scale)<br />

105<br />

100<br />

95<br />

90<br />

Peak 1980<br />

Peak 1993<br />

Peak 2007<br />

US peak(07)<br />

Great Recession<br />

(t − 2) (t − 1) t 0<br />

(t + 1) (t + 2)<br />

Years<br />

Current<br />

recovery<br />

so-so<br />

Slide copyright 2011, TZ Economics<br />

Sources:<br />

BEA, BLS ; deflation and indexation by TZE<br />

7

Real personal income by county (indexed to 2007<br />

level—no 2010 data yet) Neighbor Islands hurting<br />

102<br />

Index, 2007 = 100, log scale<br />

100<br />

98<br />

96<br />

94<br />

<strong>Maui</strong><br />

OAHU<br />

U.S.<br />

HAWAII<br />

KAUAI<br />

MAUI<br />

92<br />

05 06 07 08 09 10<br />

Sources:<br />

BEA, BLS ; deflation and indexation by TZE<br />

Slide copyright 2011, TZ Economics<br />

8

Hawaii private sector jobs: recovery is proceeding…<br />

520<br />

P T<br />

Thousands, s.a., log scale<br />

510<br />

500<br />

490<br />

480<br />

470<br />

460<br />

2.7% Quarterly<br />

annualized growth<br />

<strong>of</strong> trend component<br />

(actual data: 2.6%)<br />

2.4% Semiannual<br />

annualized growth<br />

<strong>of</strong> trend component<br />

(actual data: 2.7%)<br />

450<br />

U.S. recession shaded<br />

04 05 06 07 08 09 10 11<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT, DLIR; seasonal adjustment using Census X-12 ARIMA filter and Hodrick-Prescott filter extraction<br />

<strong>of</strong> private employment trend by TZE<br />

9

…but only on Oahu: total private + public jobs<br />

⇒ Neighbor Islands are not participating<br />

Oahu (right scale)<br />

180<br />

Neighbor Isle (left)<br />

P T<br />

460<br />

Thousands, s.a., log scale<br />

175<br />

170<br />

165<br />

160<br />

155<br />

450<br />

440<br />

430<br />

420<br />

Thousands, s.a., log scale<br />

150<br />

U.S. recession shaded<br />

03 04 05 06 07 08 09 10 11 12<br />

410<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT, DLIR; seasonal adjustment using Census X-12 ARIMA filter and Hodrick-Prescott filter extraction<br />

<strong>of</strong> private employment trend by TZE<br />

10

Monthly unemployment rates:<br />

Oahu its own private Idaho<br />

Thousands, s.a., log scale<br />

12<br />

10<br />

8<br />

6<br />

4<br />

2<br />

U.S.<br />

Neighbor Isle<br />

Statewide<br />

Oahu<br />

P T<br />

9.1% U.S.<br />

8.4% Neighbor Isle<br />

5.9% Statewide (5.6% BLS)<br />

4.9% Oahu<br />

0<br />

U.S. recessions shaded<br />

04 05 06 07 08 09 10 11<br />

Slide copyright 2011, TZ Economics<br />

Sources: U.S. BLS, Hawaii DBEDT, DLIR; seasonal adjustment <strong>of</strong> Hawaii data using Census X-12 ARIMA filter by TZE<br />

11

The business cycle varies across time and space<br />

• The Great Recession was the worst U.S. recession since the Great<br />

Depression<br />

• The Great Recession was not the worst Hawaii recession<br />

• Hawaii’s early-1980s recession(s) was (were) deeper<br />

• Hawaii’s early-1990s recession was longer<br />

• Hawaii’s dot.com recession <strong>of</strong> 2001 wasn’t<br />

• Hawaii’s private sector jobs recovery is underway<br />

• Hawaii’s public sector job los was a deliberate “9/11” event<br />

• By a variety <strong>of</strong> measures Oahu is in far better shape than the mainland<br />

and the Neighbor Island essentially are the mainland<br />

Waiting for labor shortages and until after there is no inventory is too long<br />

Slide copyright 2011, TZ Economics<br />

12

A diversion: double-dips dips in the news<br />

Slide copyright 2011, TZ Economics<br />

13

Yikes!<br />

Scary headline!<br />

Slide copyright 2011, TZ Economics<br />

Source: Newsmax Wires (May 31, 2011), http://www.newsmax.com/Headline/housing-economy-foreclosuresrecession/2011/05/31/id/398297<br />

14

On the<br />

home<br />

front<br />

Honolulu Star-Advertiser (July 8, 2011)<br />

http://www.staradvertiser.com/news/20110708_<br />

Oahu_home_sales_relapse.html<br />

Slide copyright 2011, TZ Economics<br />

15

Logistic growth function, k = 100, r = 0.10 and r = 1.9<br />

120<br />

100<br />

80<br />

Crunchy-granola bliss<br />

120<br />

100<br />

80<br />

x(t)<br />

60<br />

x(t)<br />

60<br />

40<br />

40<br />

20<br />

0<br />

r = 0.10<br />

20<br />

r = 1.9<br />

0<br />

1 21 41 61 81 101 121<br />

1 21 41 61<br />

t (time)<br />

t (time)<br />

A population with a carrying capacity <strong>of</strong> k = 100 growing at a logistic<br />

growth rate <strong>of</strong> 10%, converges smoothly (left panel); a higher intrinsic<br />

growth rate yields more rapid, oscillatory convergence (right panel).<br />

Slide copyright 2011, TZ Economics<br />

16

A made-up asset price trajectory displaying oscillatory<br />

convergence—higher<br />

“intensity” implies “wobbliness”<br />

p(t) (thousand $)<br />

650<br />

600<br />

550<br />

500<br />

450<br />

400<br />

350<br />

Period 1 equilibrium price: $350,000<br />

Period n equilibrium price: $600,000*<br />

(for example, assume that purchasing<br />

power limits the median household’s<br />

“carrying capacity” to the latter price)<br />

Oahu median<br />

SF home prices<br />

300<br />

*Uses Micros<strong>of</strong>t Excel’s built-in graphics<br />

smoothing algorithm applied to a logistic<br />

growth function with intrinsic growth rate<br />

<strong>of</strong> 1.5 and carrying capacity <strong>of</strong> 600<br />

0 5 10<br />

t (years)<br />

Slide copyright 2011, TZ Economics<br />

17

Look familiar? Oahu single-family median home<br />

prices from 2003 through May 2011<br />

700<br />

Thousand $, s.a., log scale<br />

650<br />

600<br />

550<br />

500<br />

450<br />

400<br />

“Double-dip?” or<br />

oscillatory<br />

convergence?<br />

350<br />

03 04 05 06 07 08 09 10 11<br />

Slide copyright 2011, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors; seasonal adjustment using Census X-12 filter and Hodrick-Prescott filter trend<br />

extraction by TZ Economics<br />

18

More complex asset price adjustment paths: an<br />

overshooting model <strong>of</strong> asset price decline<br />

Simulated asset price dynamics in a model<br />

<strong>of</strong> “slow-moving capital” by Darrel Duffie<br />

“The key implication is that supply or demand shocks must be absorbed on<br />

short notice by a limited set <strong>of</strong> investors. The risk aversion or limited<br />

capital <strong>of</strong> the currently available investors, including intermediaries, leads<br />

them to require a price concession in order to absorb the supply or demand<br />

shock. They plan to ‘lay <strong>of</strong>f’ the associated risk over time as other<br />

investors become available. As a result, the initial price impact is followed<br />

by a price reversal that may occur over an extended period <strong>of</strong> time.”<br />

Slide copyright 2011, TZ Economics<br />

Source: Darrell Duffie, “Asset Price Dynamics with Slow-Moving Capital” Journal <strong>of</strong> Finance vol. 65 no. 4 (August 2010)<br />

pp 1239-1267 (http://www.darrellduffie.com/uploads/pubs/DuffieAFAPresidentialAddress2010.pdf)<br />

19

Meltdown after 2006: overshooting plus oscillation<br />

in S&P Case-Shiller<br />

home price indexes<br />

280<br />

January 2000 = 100 s.a., log scale<br />

240<br />

200<br />

160<br />

120<br />

Los Angeles<br />

San Diego<br />

San Francisco<br />

Las Vegas<br />

LAX<br />

SAN<br />

SFO<br />

LAS<br />

Is this a “double-dip?”<br />

or is this overshooting<br />

followed by oscillatory<br />

convergence?<br />

This is Vegas, baby<br />

80<br />

03 04 05 06 07 08 09 10 11<br />

Slide copyright 2011, TZ Economics<br />

Sources: Standard & Poor’s; seasonal adjustment using Census X-12 filter by TZ Economics<br />

20

S&P 500 daily closing values:<br />

post-Lehman overshooting,<br />

uneven recovery<br />

1600<br />

1400<br />

Lehman Brothers collapses<br />

(September 15, 2008)<br />

Index, 1941-43 = 10<br />

1200<br />

1000<br />

800<br />

600<br />

NBER recession shaded<br />

(March 9, 2009)<br />

2007 2008 2009 2010 2011<br />

Slide copyright 2011, TZ Economics<br />

Sources: Standard & Poor’s, Federal Reserve Bank <strong>of</strong> St. Louis; daily closing data through June 22, 2011<br />

21

Intra-day S&P 500 May 6, 2010 “Flash Crash”<br />

time domain: intraday<br />

−8.5%<br />

Slide copyright 2011, TZ Economics<br />

Source: http://www.marketoracle.co.uk/images/2010/Jun/flash-crash-4-2.jpg<br />

22

Kauai visitor arrivals, hurricane Iniki etc.,<br />

time domain: half a decade<br />

160<br />

Monthly in thousands, s.a., log scale<br />

80<br />

40<br />

20<br />

Gulf<br />

War<br />

Iniki<br />

Iraqnaphobia*<br />

9/11 90 92 94 96 98 00 02 04<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT; Bank <strong>of</strong> Hawaii; *semantic mahalo to Diane Swonk, Mesirow Finance<br />

23

Hawaii international arrivals variation in monthly<br />

standard deviations under four exogenous shocks<br />

“3-6 months” “3-6 months”<br />

2<br />

Kobe<br />

2<br />

1<br />

0<br />

-1<br />

Gulf War<br />

1<br />

0<br />

-1<br />

SARS<br />

9/11<br />

-2<br />

-2<br />

-3<br />

-3<br />

Early-1990s: rising arrivals trend<br />

q 0<br />

q 1<br />

q 2<br />

q 3<br />

q 0<br />

q 1<br />

q 2<br />

q 3<br />

Early-2000s: falling arrivals trend<br />

Slide copyright 2011, TZ Economics<br />

Sources: Arrivals data published by HTA and DBEDT; interval standard deviation estimates relative to 4.5–year trends<br />

by TZ Economics<br />

24

Hawaii daily passenger arrivals on flights from<br />

Japan—difference from this year to last<br />

Thousands per day, net<br />

(2011 minus 2010)<br />

2<br />

1<br />

0<br />

-1<br />

-2<br />

-3<br />

Sendai seismic<br />

event (March 11)<br />

-4<br />

10.12 11.01 11.02 11.03 11.04 11.05 11.06<br />

Slide copyright 2011, TZ Economics<br />

Source: Hawaii DBEDT; calculations on daily passenger counts by TZ Economics through June 7, 2011<br />

25

Double-dip your home price<br />

• A “double-dip” in asset valuations could just be somebody’s way <strong>of</strong><br />

scaring the crap out <strong>of</strong> you so you’ll “tune in tomorrow”*<br />

• Or it could be the norm—complexity<br />

• You’re surrounded by exogenous impulses<br />

• These shocks generate complex paths: overshooting, oscillation, many<br />

different convergence trajectories from one equilibrium to another<br />

• Asset price dynamics—for stocks, bonds, commodities, houses—all<br />

exhibit these movements; it’s happening right now<br />

*See NBC Nightly News, Friday, July 8, 2011: http://www.msnbc.msn.com/id/3032619/vp/43691544#43691544<br />

(fast-forward to 1:11 in the clip)<br />

Slide copyright 2011, TZ Economics<br />

26

Two decades <strong>of</strong> Oahu home prices: under the cycle<br />

lie varying forcing factors and complex dynamics<br />

• Long-term home prices gravitate to an appreciate trend dictated by longrun<br />

returns in alternative asset classes (via arbitrage—capital and<br />

occupants are both mobile)<br />

• Each valuation cycle has its own character; each cycle is associated<br />

with a particular asset price adjustment path from one equilibrium<br />

“before the boom” to another equilibrium “after the boom”<br />

• A variety <strong>of</strong> complex trajectories are possible, in the same market in<br />

different cycles, or in different markets in the same cycle (even when all<br />

markets face the same constellation <strong>of</strong> macroeconomic drivers)<br />

Slide copyright 2011, TZ Economics<br />

27

Long run Oahu SF home prices: arbitrage to risk-<br />

free asset return plus a risk premium and expected<br />

inflation premium (higher pre-1980, lower post-1980)<br />

1000<br />

Annual in thousand $, s.a. (log scale)<br />

100<br />

Know your inflation history: a trend break in<br />

U.S. inflationary momentum in 1980, when<br />

monetary policy regime change was initiated<br />

by Jimmy Carter’s appointment <strong>of</strong> Paul Volker<br />

Oahu mean SF price<br />

Trend pre-1980<br />

Trend post-1980<br />

1960 1970 1980 1990 2000 2010 2020<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT, TZ Economics; regressions <strong>of</strong> natural logs <strong>of</strong> mean home prices on time trend 1958-1983 and<br />

1976-2010.<br />

28

In the 1990s, median Oahu condo and SF home<br />

prices fell: possible convergence paths generated<br />

by a logistic model (see Appendix 1)<br />

200<br />

150<br />

100<br />

50<br />

Calibrated to early-<br />

1990s Oahu condo<br />

price movements<br />

200<br />

150<br />

100<br />

50<br />

400<br />

350<br />

300<br />

250<br />

200<br />

Calibrated to early-<br />

1990s Oahu SF home<br />

price movements<br />

400<br />

350<br />

300<br />

250<br />

200<br />

Slide copyright 2011, TZ Economics<br />

29

The actual 1990s Oahu path: smooth compression<br />

220<br />

200<br />

180<br />

160<br />

140<br />

120<br />

Thousand $, s,a, (log scale)<br />

Thousand $, s,a, (log scale)<br />

400<br />

380<br />

360<br />

340<br />

320<br />

300<br />

280<br />

100<br />

End <strong>of</strong> U.S. recession shaded<br />

91 92 93 94 95 96 97 98 99 00<br />

260<br />

End <strong>of</strong> U.S. recession shaded<br />

91 92 93 94 95 96 97 98 99 00<br />

Median condo price<br />

Median single-family home price<br />

Slide copyright 2011, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors, Standard & Poor’s; seasonal adjustment using Census X-12 ARIMA filter and trend<br />

extraction using Hodrick-Prescott filter by TZE<br />

30

Median Oahu home prices: mid-1990s sag,<br />

2000s overshoot and oscillation<br />

700<br />

Thousand $, s.a. (log scale)<br />

400<br />

200<br />

Single-family (right scale)<br />

Condominium (left)<br />

600<br />

500<br />

400<br />

300<br />

200<br />

Thousand $, s.a. (log scale)<br />

U.S. recessions shaded<br />

100<br />

90 95 00 05 10<br />

Slide copyright 2011, TZ Economics<br />

Sources: Harvey Shapiro, Honolulu Board <strong>of</strong> Realtors; recession dates are NBER cyclical turning points (peak-trough);<br />

seasonal adjustment by TZE using Census X-12 ARIMA filter<br />

31

Median Oahu home prices: mid-1990s sag,<br />

2000s overshoot and oscillation<br />

700<br />

Thousand $, s.a. (log scale)<br />

400<br />

200<br />

After the 1994 Fed<br />

tightening: smooth<br />

convergence to lower<br />

equilibrium prices<br />

Late in the 2000s housing<br />

“bubble:” overshooting,<br />

oscillatory convergence<br />

600<br />

500<br />

400<br />

300<br />

Thousand $, s.a. (log scale)<br />

100<br />

90 95 00 05 10<br />

Slide copyright 2011, TZ Economics<br />

Sources: Harvey Shapiro, Honolulu Board <strong>of</strong> Realtors; recession dates are NBER cyclical turning points (peak-trough);<br />

seasonal adjustment by TZE using Census X-12 ARIMA filter<br />

32

This cycle’s s median existing single-family home<br />

prices: “double-dip” or overshooting + oscillation?<br />

900<br />

Quarterly, thousand $, s.a. (log scale)<br />

800<br />

700<br />

600<br />

500<br />

400<br />

300<br />

U.S. recession shaded<br />

2005 2006 2007 2008 2009 2010 2011<br />

San Jose, Sunnyvale, Santa Clara<br />

Oahu<br />

Anaheim, Santa Ana, Irvine<br />

San Francisco, Oakland, Fremont<br />

<strong>Maui</strong><br />

Los Angeles, Long Beach, Santa Ana<br />

San Diego, Carlsbad, San Marcos<br />

Slide copyright 2011, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors, Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, National <strong>Association</strong> <strong>of</strong> Realtors; seasonal<br />

adjustment by TZE using Census X-12 ARIMA filter<br />

33

All these markets faced the same interest rates,<br />

homebuyer tax credits; each has unique price path<br />

900<br />

800<br />

700<br />

600<br />

500<br />

Oahu<br />

900<br />

800<br />

700<br />

600<br />

500<br />

400<br />

400<br />

Orange County, CA<br />

800<br />

06 07 08 09 10 11 12<br />

800<br />

06 07 08 09 10 11 12<br />

700<br />

700<br />

600<br />

600<br />

San Diego<br />

500<br />

<strong>Maui</strong><br />

500<br />

400<br />

400<br />

300<br />

05 06 07 08 09 10 11 12<br />

300<br />

05 06 07 08 09 10 11 12<br />

Slide copyright 2011, TZ Economics<br />

34

<strong>Maui</strong> existing single-family home sales median prices<br />

now smoothly converging to the low- to mid-$400ks<br />

800<br />

Monthly, thousand $, s.a. (log scale)<br />

400<br />

200<br />

1995 2000 2005 2010 2015<br />

Pau by 2013? By<br />

“October 26, 2012?”<br />

Slide copyright 2011, TZ Economics<br />

Sources: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>; seasonal adjustment using Census X-12 ARIMA filter and trend extraction using<br />

Hodrick-Prescott filter by TZE<br />

35

<strong>Maui</strong> existing single-family home sales price<br />

distribution shifted to the left since the cyclical peak<br />

700<br />

Number <strong>of</strong> sales<br />

in $250,000 increments<br />

600<br />

500<br />

400<br />

300<br />

200<br />

100<br />

2006<br />

2010<br />

0<br />

0.0 0.5 1.0 1.5 2.0 2.5 3.0<br />

Million dollars<br />

Slide copyright 2011, TZ Economics<br />

Sources: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>; histogram generation by TZ Economics<br />

36

<strong>Maui</strong> existing-home days on market: not so much a<br />

glut <strong>of</strong> supply* as lackluster absorption<br />

Lehman<br />

Monthly, days, s.a. (log scale)<br />

200<br />

100<br />

Single-family<br />

Condominium<br />

Condo<br />

Single-family<br />

Recessions shaded<br />

02 04 06 08 10 12<br />

*Even with all those #@*^& foreclosures!<br />

Slide copyright 2011, TZ Economics<br />

Sources: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>; seasonal adjustment using Census X-12 ARIMA filter and trend extraction using<br />

Hodrick-Prescott filter by TZE<br />

37

<strong>Maui</strong> macroeconomic indicators: insufficient “lift, lift,”<br />

and self-inflicted wounds (“we(<br />

meant to do that”)<br />

• The legacy <strong>of</strong> the 2008 Aloha Airlines and ATA shutdowns still is felt in<br />

the relative lack <strong>of</strong> scheduled air seats to <strong>Maui</strong> from the mainland, and<br />

reduced interisland lift (Wiki: “Stackelberg competition”)*<br />

• Good timing on that fiscal austerity: no public job growth to complement<br />

the utter lack <strong>of</strong> private job growth<br />

• Unemployment rates are falling partly (largely?) because the labor force<br />

(the denominator in the unemployment rate) is shrinking as workers<br />

leave <strong>Maui</strong> (<strong>of</strong> course, they also came to <strong>Maui</strong>)<br />

• That wacky “workforce housing” ordinance is the gift that keeps on<br />

giving: x percent <strong>of</strong> zero is still zero<br />

• Hey, anti-Superferry n00bs: great job! Big, big help on the economy<br />

there. You’re doing a great job protecting the environment by checking<br />

all that luggage that comes into <strong>Maui</strong>…what’s that? you only check the<br />

luggage leaving <strong>Maui</strong>? Boy, you guys must really be concerned about<br />

the environment. Yo: pono this.<br />

Slide copyright 2011, TZ Economics<br />

* http://en.wikipedia.org/wiki/Stackelberg_competition<br />

38

<strong>Maui</strong> total visitor arrivals through May 2011<br />

Monthly in thousands, s.a. (log scale)<br />

240<br />

220<br />

200<br />

180<br />

160<br />

140<br />

Desert<br />

Storm<br />

Recessions shaded<br />

9/11<br />

Aloha<br />

Lehman<br />

Sendai + weak spring travel<br />

demand (higher oil prices /<br />

air fares)<br />

90 95 00 05 10<br />

Sources:<br />

Slide copyright 2011, TZ Economics<br />

Hawaii Tourism Authority, Hawaii DBEDT; seasonal adjustment using Census X-12 ARIMA filter and trend<br />

extraction using Hodrick-Prescott filter by TZE<br />

39

<strong>Maui</strong> payroll employment: no recovery yet<br />

Monthly in thousands, s.a. (log scale)<br />

75<br />

70<br />

65<br />

60<br />

55<br />

50<br />

45<br />

Recessions shaded<br />

9/11<br />

1995 2000 2005 2010<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DLIR, DBEDT; seasonal adjustment using Census X-12 ARIMA filter by TZE<br />

40

Both private and public employment<br />

on <strong>Maui</strong> stagnant since 2009<br />

Monthly 000, s.a. (log scale)<br />

10.4<br />

10.0<br />

9.6<br />

9.2<br />

8.8<br />

8.4<br />

8.0<br />

66<br />

64<br />

62<br />

60<br />

58<br />

56<br />

54<br />

Private (right scale)<br />

Public (left scale)<br />

Recession shaded<br />

03 04 05 06 07 08 09 10 11 12<br />

Monthly 000, s.a. (log scale)<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DLIR, DBEDT; seasonal adjustment using Census X-12 ARIMA filter by TZE<br />

41

<strong>Maui</strong> unemployment rate<br />

Monthly, percent, s.a.<br />

10<br />

9<br />

8<br />

7<br />

6<br />

5<br />

4<br />

3<br />

2<br />

Recessions shaded<br />

1<br />

90 95 00 05 10<br />

Decrease partly<br />

attributable to labor<br />

force exit (outmigration<br />

back to<br />

Oahu or mainland)<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DLIR, DBEDT; seasonal adjustment using Census X-12 ARIMA filter by TZE<br />

42

<strong>Maui</strong> new housing units authorized by permit:<br />

demand-constrained or supply-constrained?<br />

Quarterly units, s.a. (log scale)<br />

1000<br />

100<br />

Recessions shaded<br />

1,500 per<br />

year<br />

10<br />

75 80 85 90 95 00 05 10<br />

< 300 per year?<br />

How’s that workforce housing<br />

ordinance working out?<br />

Slide copyright 2011, TZ Economics<br />

Sources: <strong>Maui</strong> County Building Department, Hawaii DBEDT; seasonal adjustment using Census X-12 ARIMA filter and<br />

trend extraction using Hodrick-Prescott filter by TZE<br />

43

<strong>Maui</strong> total real private building permit values<br />

Monthly in million 2006$, s.a. (log scale)<br />

100<br />

10<br />

Lehman<br />

Back To The Future<br />

75 80 85 90 95 00 05 10 15<br />

Slide copyright 2011, TZ Economics<br />

Sources: <strong>Maui</strong> County Building Department, Hawaii DBEDT; seasonal adjustment using Census X-12 ARIMA filter and<br />

trend extraction using Hodrick-Prescott filter by TZE<br />

44

The challenges for <strong>Maui</strong><br />

• Overhang <strong>of</strong> distressed properties, delinquencies with mainland<br />

borrowers and lenders; foreclosure logjam and idiotic Act 48*<br />

• Rising absorption <strong>of</strong> existing inventory driven by low valuations is<br />

vulnerable to incipient interest rate normalization, exogenous<br />

“headwinds” on investor expectations (energy shocks; ge<strong>of</strong>inancial risks)<br />

• Supply side constraints: <strong>Maui</strong> still has that wacky housing ordinance—<br />

growth-management policy when there is no growth<br />

• Air capacity: domestic lift back to the 1990s (“No Aloha”)<br />

• Otherwise, macro-fundamentally: <strong>Maui</strong> unemployment in 2012 will be<br />

the same as it was in 1997—the beginning <strong>of</strong> the last great decade<br />

• Demographic challenge: that late-1990s 50-something investor is now<br />

70 years old and ran her last triathlon when Kimo was <strong>Maui</strong> Mayor<br />

(define “active lifestyle” for Baby Boomers in the 20-teens)<br />

• What does <strong>Maui</strong> <strong>of</strong>fer for skaters, gamers, and WoW addicts?<br />

Slide copyright 2011, TZ Economics<br />

* In the Q&A somebody asked about Act 48. I had no answer. I looked it up. My answer: Whiskey Tango Foxtrot.<br />

45

Pau<br />

Slide copyright 2011, TZ Economics<br />

46

Appendix 1: a simple model <strong>of</strong> asset price movements<br />

Slide copyright 2011, TZ Economics<br />

47

An example from the bio-economics <strong>of</strong> growth with<br />

a capacity constraint—the the logistic growth function<br />

Ever hear someone say that tourism in Hawaii risks exceeding the islands’ “carrying<br />

capacity?” What are they talking about? Consider the logistic growth function.<br />

Assume the environment has a carrying capacity <strong>of</strong> “100,” a natural limit on how much<br />

a biological population can grow: k = 100 . Assume that the intrinsic growth rate <strong>of</strong> the<br />

population is the parameter r. The relationship between population next year x ( t +1)<br />

and today’s population x ( t)<br />

is:<br />

( t) ⎞ ⎟⎠<br />

⎛ x<br />

∆ x ≡ [ x( t + 1 ) − x( t)<br />

] = rx()<br />

t ⎜1<br />

− ,<br />

⎝ k<br />

If the population xt<br />

can be defined in continuous time, this is:<br />

dx ⎛ x ⎞<br />

≡ = ⎜ −<br />

t<br />

x& rxt 1 ⎟ .<br />

dt ⎝ k ⎠<br />

Now, solve for x () t , for all t , as a function <strong>of</strong> r , k , and ( 0)<br />

x ( x at time t = 0 ).<br />

Slide copyright 2011, TZ Economics<br />

48

Logistic growth function*, k = 100, r = 0.10 and r = 1.9<br />

120<br />

100<br />

80<br />

Crunchy-granola bliss<br />

120<br />

100<br />

80<br />

x(t)<br />

60<br />

x(t)<br />

60<br />

40<br />

40<br />

20<br />

0<br />

r = 0.10<br />

20<br />

r = 1.9<br />

0<br />

1 21 41 61 81 101 121<br />

1 21 41 61<br />

t (time)<br />

t (time)<br />

A population with a carrying capacity <strong>of</strong> k = 100 growing at a logistic<br />

growth rate <strong>of</strong> 10%, converges smoothly (left panel); a higher intrinsic<br />

growth rate yields more rapid, oscillatory convergence (right panel).<br />

Slide copyright 2011, TZ Economics<br />

*This slide is a replicate <strong>of</strong> slide 16<br />

49

Logistic growth function, k = 100, r = 2.1 and r = 2.8<br />

x(t)<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

r = 2.1<br />

20<br />

r = 2.8<br />

0<br />

1 21 41 61 81 101 121<br />

1 21 41 61 81 101 121<br />

t (time)<br />

t (time)<br />

Really high intrinsic growth rates (r) generate complexity: rapid<br />

convergence to k followed by bifurcation (left panel) or by chaotic<br />

motion (right panel)—deterministic, not stochastic movement!<br />

x(t)<br />

140<br />

120<br />

100<br />

80<br />

60<br />

40<br />

Slide copyright 2011, TZ Economics<br />

50

Appendix 2: mortgage delinquency<br />

Slide copyright 2011, TZ Economics<br />

51

Despite surge, Hawaii mortgage delinquency now<br />

subsiding as home prices prices settle<br />

Percent <strong>of</strong> mortgages outstanding, s.a.<br />

4<br />

3<br />

2<br />

1<br />

0<br />

Hawaii home prices (right)<br />

30 days past due (left)<br />

90 days past due (left)<br />

U.S. recessions shaded<br />

Data<br />

puka<br />

75 80 85 90 95 00 05 10<br />

800<br />

400<br />

200<br />

100<br />

50<br />

Index, 1980Q1 = 100, s.a. (log scale)<br />

Sources:<br />

Slide copyright 2011, TZ Economics<br />

Federal Housing Finance Agency, Mortgage Bankers, <strong>Association</strong>, Guy Sakamoto—Bank <strong>of</strong> Hawaii; seasonal<br />

adjustment by TZE<br />

52

Rank percent <strong>of</strong> loans<br />

90+ days<br />

past due<br />

Foreclosure<br />

inventory<br />

Serious delinquency<br />

rankings by state<br />

1 Florida 4.59 14.38<br />

2 Nevada 6.65 9.32<br />

3New Jersey 3.48 7.74<br />

4 Illinois 3.70 6.77<br />

5New York 3.77 5.33<br />

6 Arizona 4.23 4.81<br />

7 California 4.84 3.97<br />

8 Ohio 3.57 5.09<br />

9 Rhode Island 3.92 4.53<br />

10 Indiana 3.42 4.89<br />

11 Maryland 4.77 3.52<br />

12 Maine 2.78 5.48<br />

13 Georgia 4.64 3.43<br />

14 Mississippi 4.59 3.41<br />

15 Michigan 4.16 3.74<br />

16 Connecticut 3.31 4.36<br />

17 Delaware 2.94 4.29<br />

18 Hawaii 2.64 4.57<br />

19 South Carolina 3.15 4.04<br />

20 Louisiana 3.24 3.92<br />

21 Massachusetts 3.54 3.32<br />

4%<br />

3<br />

2<br />

1<br />

0<br />

Prices (right)<br />

30+ days (left)<br />

90+ days (left)<br />

Index, 1980Q1 = 100,<br />

s.a. (log scale)<br />

540<br />

520<br />

2006 2007 2008 2009 2010 2011<br />

Hawaii home price index and delinquency<br />

500<br />

480<br />

460<br />

440<br />

Slide copyright 2011, TZ Economics<br />

Sources:<br />

Federal Housing Finance Agency, Mortgage Bankers, <strong>Association</strong>, Guy Sakamoto—Bank <strong>of</strong> Hawaii; seasonal<br />

adjustment by TZE<br />

53

Mortgage delinquency varies widely:<br />

≥90 days past due by county (darker is higher)<br />

22.7 Dade, FL<br />

18.3 Broward, FL<br />

15.9 Palm Beach, FL<br />

15.6 Clark, NV<br />

13.6 Riverside, CA<br />

13.2 San Joaquin<br />

12.8 San Bernadino, CA<br />

11.4 Bronx, NY<br />

10.1 Maricopa, AZ<br />

9.4 Sacramento, CA<br />

9.1 Contra Costa, CA<br />

8.8 Los Angeles, CA<br />

8.2 Hawaii, HI<br />

7.6 <strong>Maui</strong>, HI<br />

7.6 San Diego, HI<br />

6.9 Orange, CA<br />

5.9 Santa Clara, CA<br />

5.3 U.S. average<br />

4.5 Kauai, HI<br />

3.7 San Francisco, CA<br />

3.4 Honolulu, HI<br />

1.8 Dane, WI<br />

1.0 Cherry, NE<br />

0.0 Todd, SD<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Bank <strong>of</strong> New York based on credit-reporting agency TransUnion LLC’s Trend Data database<br />

(http://data.newyorkfed.org/creditconditionsmap/)<br />

54

Appendix 3: housing and monetary policy<br />

Slide copyright 2011, TZ Economics<br />

55

Housing and monetary policy:<br />

an exit strategy for the Federal Reserve?<br />

• That was then and this is now: one big change since the 1990s is that<br />

the Fed now contemporaneously announces policy shifts and articulates<br />

forward-looking language to help agents anticipate future policy<br />

• In 1994, unanticipated Fed tightening did not clarify the extent <strong>of</strong> inflation<br />

risk, it actually aggravated the perception <strong>of</strong> inflation risk, causing an<br />

increase in real long-term interest rates<br />

• [The subsequent 1999 tightening—post-LTCM—partly was intended to<br />

deflect “irrational exuberance” fueling an equity asset pricing bubble; it<br />

too raised real long-term interest rates]<br />

• The 2004 Fed tightening was articulated—“accommodation can be<br />

removed at a pace that is likely to be measured”—it did not aggravate<br />

inflation expectations and had no adverse real interest rate impacts<br />

• The end <strong>of</strong> QE2 (June 30, 2011) and start <strong>of</strong> Fed tightening (2012?)<br />

cannot occur until after medium-term Treasury yields rise somewhat<br />

(with adverse effects partly <strong>of</strong>fset by narrowing mortgage spreads)<br />

possibly exerting drag on a revival <strong>of</strong> housing investment<br />

Slide copyright 2011, TZ Economics<br />

56

Fed funds rate increases (1994>, end-1998>, 2004>):<br />

the first two “unannounced;<br />

unannounced;” the last “transparent”<br />

9<br />

Percent<br />

8<br />

7<br />

6<br />

5<br />

4<br />

Each arrow between<br />

vertical lines denotes<br />

periods during which<br />

the Federal Open<br />

Market Committee<br />

(FOMC) was raising<br />

its target for the<br />

overnight interbank<br />

lending rate, the socalled<br />

fed funds rate.<br />

3<br />

2<br />

1<br />

U.S. recessions shaded<br />

0<br />

90 95 00 05 10<br />

Slide copyright 2011, TZ Economics<br />

Sources: Harvey Shapiro, Honolulu Board <strong>of</strong> Realtors; recession dates are NBER cyclical turning points (peak-trough);<br />

Fed tightening dates indicate major move in effective Fed Funds rate or target<br />

57

Risk premiums and real interest rates: 2004 Fed<br />

“transparency” kept real interest rates from jumping<br />

7<br />

6<br />

Mortgage spread (right scale)<br />

Real mortgage rate (left)<br />

LTCM<br />

Crisis<br />

3.5<br />

3.0<br />

2.5<br />

2.0<br />

1.5<br />

1.0<br />

Percentage points<br />

Percent<br />

5<br />

4<br />

3<br />

U.S. recessions shaded<br />

2<br />

90 95 00 05 10<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Board; recession dates are NBER cyclical turning points (peak-trough); Fed tightening dates<br />

indicate major move in effective Fed Funds rate or target<br />

58

Median <strong>Maui</strong> and San Diego home prices, Fed tightening (arrows):<br />

1994/1989 “surprises” ignored; 2004 announced The End Is Near<br />

<strong>Maui</strong> (median, right scale)<br />

San Diego (CS, left)<br />

800<br />

Index Jan 2000 = 100, s.a.<br />

(log scale)<br />

400<br />

200<br />

100<br />

400<br />

200<br />

Thousand $, s.a. (log scale)<br />

50<br />

U.S. recessions shaded<br />

94 96 98 00 02 04 06 08 10 12<br />

Slide copyright 2011, TZ Economics<br />

Sources: Realtor <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, Standard & Poors (seasonal adjustment by TZE); recession dates are NBER<br />

cyclical turning points (peak-trough); Fed tightening dates indicate move in effective Fed Funds rate target<br />

59

Monetary policy and the macroeconomic outlook<br />

• Monetary policy changes conditioned on actual economic performance<br />

• Talk is cheap: people now getting sound-bites predicting a “double-dip”<br />

recession are not a reflection <strong>of</strong> the majority view regarding the outlook<br />

• Examine the data—does the progress <strong>of</strong> economic reacceleration<br />

warrant a return to monetary policy normalcy? Eventually yes.<br />

• Before (1990s) when the Fed removed monetary policy accommodation<br />

it was a surprise, causing both long-term and short-term rates to rise<br />

• Now (2000s) the Fed removes accommodation transparently, leaving<br />

long-term rates relatively unchanged while short-term rates rise<br />

• Transparency means: we know their forecast, whether policy is<br />

conventional (Fed Funds target) or unconventional (quantitative easing)<br />

how much unconventional accommodation there will be (QE2) and when<br />

it will end (June 30), how long conventional accommodation may last<br />

(“an extended period”) and what conditions will warrant its removal.<br />

Slide copyright 2011, TZ Economics<br />

60

U.S. real GDP indexed to cyclical peaks<br />

Index <strong>of</strong> real GDP: peak quarter = 1.000<br />

1.050<br />

Previous 10 recessions*<br />

Carter/Reagan double-dip<br />

Great Recession<br />

1.000<br />

0.950<br />

-6 -4 -2 0 2 4 6 8 10 12 14<br />

Actual 2011Q1p real GDP<br />

*Recessions since World War II<br />

Slide copyright 2011, TZ Economics<br />

Source: Pr<strong>of</strong>essor Robert Hall, Stanford University and Chair, NBER Dating Committee; Bureau <strong>of</strong> Economic Analysis,<br />

U.S. Department <strong>of</strong> Commerce; includes 2011Q1P data and forecasts though 2011Q4<br />

61

October 2010 NABE real growth forecasts,<br />

with actual 2010 fourth quarter data<br />

Quarterly annualized growth in percent<br />

8<br />

4<br />

0<br />

-4<br />

-8<br />

Crisis<br />

begins<br />

NBER recession shaded<br />

P<br />

Lehman<br />

fails<br />

T<br />

Actual<br />

NABE Oct 2010<br />

Top 5<br />

Bottom 5<br />

NABE<br />

forecast<br />

published<br />

October 10,<br />

2010<br />

06 07 08 09 10 11<br />

Source:<br />

Slide copyright 2011, TZ Economics<br />

Bureau <strong>of</strong> Economic Analysis, National <strong>Association</strong> for Business Economics; advance 2010Q4 data released<br />

January 27, 2011 include revisions to prior quarters<br />

62

May 2011 NABE real growth forecasts,<br />

with actual 2011 first quarter data<br />

8<br />

P<br />

T<br />

Quarterly annualized growth in percent<br />

4<br />

0<br />

-4<br />

-8<br />

Crisis<br />

begins<br />

NBER recession shaded<br />

Lehman<br />

fails<br />

Actual<br />

NABE May 2011<br />

Top 5<br />

Bottom 5<br />

NABE<br />

forecast<br />

published<br />

May 16, 2011<br />

06 07 08 09 10 11 12<br />

Source:<br />

Bureau <strong>of</strong> Economic Analysis, National <strong>Association</strong> for Business Economics; preliminary 2011Q1 data<br />

released May 26, 2011 include revisions to prior quarters<br />

Slide copyright 2011, TZ Economics<br />

63

Federal Reserve real GDP growth projections<br />

released with the June 2011 FOMC statement<br />

Slide copyright 2011, TZ Economics<br />

Source: Federal Reserve Board minutes <strong>of</strong> the Federal Open Market Committee meeting January 25-26, 2011<br />

(http://www.federalreserve.gov/monetarypolicy/files/fomcminutes20110126.pdf)<br />

64

Quantitative easing and the Fed’s s balance sheet<br />

Securities<br />

Other assets<br />

SIFIs<br />

TALF<br />

Term Auction<br />

CP funding<br />

Central banks<br />

Lehman<br />

QE1<br />

QE2<br />

2.5<br />

2.0<br />

1.5<br />

1.0<br />

Treasury<br />

Currency<br />

Deposits<br />

Lehman<br />

QE1<br />

QE2<br />

2.5<br />

2.0<br />

1.5<br />

1.0<br />

0.5<br />

0.5<br />

0.0<br />

A-07 F-08 A-08 F-09 A-09 F-10 A-10 F-11<br />

Federal Reserve Assets<br />

0.0<br />

A-07 F-08 A-08 F-09 A-09 F-10 A-10 F-11<br />

Federal Reserve Liabilities<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Board (http://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm), balance<br />

sheet data through week <strong>of</strong> June 2, 2011; calculations by TZE<br />

65

Why quantitative easing? Lesson from the 1930s:<br />

<strong>of</strong>fset collapse <strong>of</strong> M1 money multiplier (m)(<br />

Lehman<br />

+ c<br />

m = 1 money multiplier<br />

r + e + c<br />

c = currency/deposit ratio<br />

e = excess reserves/deposit ratio<br />

r = required reserves/deposit ratio<br />

Slide copyright 2011, TZ Economics<br />

Source: Federal Reserve Bank <strong>of</strong> St. Louis (http://research.stlouisfed.org/fred2/series/MULT)<br />

66

Monetary accommodation and interest rates after<br />

the Dot.com Recession and the Great Recession<br />

Percent<br />

7<br />

6<br />

P T<br />

“Under these circumstances<br />

policy accommodation can be<br />

removed at a pace that is<br />

likely to be measured.”<br />

Percent<br />

7<br />

6<br />

NBER recession shaded<br />

P T<br />

“economic conditions…are<br />

likely to warrant exceptionally<br />

low levels for the federal<br />

funds rate for an extended<br />

period.”<br />

5<br />

4<br />

10-y T-Note<br />

5<br />

4<br />

10-y T-Note<br />

3<br />

2<br />

Fed funds<br />

3<br />

2<br />

But<br />

when?<br />

1<br />

0<br />

NBER recession shaded<br />

99 00 01 02 03 04 05<br />

1<br />

0<br />

Fed funds<br />

06 07 08 09 10 11 12<br />

Dot.com<br />

Great<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Board, Federal Reserve Bank <strong>of</strong> St. Louis; TZ Economics<br />

67

U.S. Treasury (risk-free) constant-maturity yields:<br />

1990s Fed tightening shot long-term rates upward;<br />

2004 tightening was neutral w.r.t. . long-term rates<br />

Percent<br />

10<br />

8<br />

6<br />

4<br />

2<br />

Fed<br />

tightens<br />

Fed<br />

tightens<br />

Fed<br />

tightens<br />

NBER recessions shaded<br />

0<br />

90 95 00 05 10<br />

TY30<br />

TY20<br />

TY10<br />

TY7<br />

TY5<br />

TY3<br />

TY2<br />

TY1<br />

TMO6<br />

TMO3<br />

TMO1<br />

FEDF<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Board, Federal Reserve Bank <strong>of</strong> St. Louis; TZ Economics<br />

68

Recent U.S. Treasury (risk-free) constant-maturity yields<br />

6<br />

P T<br />

5<br />

4<br />

LR equilibrium?<br />

Percent<br />

3<br />

2<br />

1<br />

0<br />

NBER recession shaded<br />

06 07 08 09 10 11 12<br />

10-year<br />

7-year<br />

5-year<br />

Fed funds (overnight)<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Board, monthly data include June 20, 2011 observation; TZ Economics<br />

69

Nominal U.S. Treasury yield curves<br />

5<br />

Jul 06<br />

Jul 07<br />

4<br />

Percent<br />

3<br />

2<br />

Jul 08<br />

Jul 09<br />

Jul 10<br />

June 21, 2011<br />

1<br />

FF<br />

0<br />

1-yr<br />

2-yr<br />

3-yr<br />

5-yr<br />

7-yr<br />

10-yr<br />

20-yr<br />

30-yr<br />

Slide copyright 2011, TZ Economics<br />

Source: Federal Reserve Board (H.15 constant maturity yields); calculations by TZE through June 21, 2011<br />

70

FOMC Statement June 22, 2011:<br />

no easing, no tightening<br />

• “The economic recovery is continuing at a moderate pace, though<br />

somewhat more slowly than the Committee had expected”<br />

• “The slower pace <strong>of</strong> the recovery reflects in part factors that are likely to be<br />

temporary, including the damping effect <strong>of</strong> higher food and energy prices<br />

on consumer purchasing power and spending as well as supply chain<br />

disruptions associated with the tragic events in Japan”<br />

• “The Committee expects the pace <strong>of</strong> recovery to pick up over coming<br />

quarters and the unemployment rate to resume its gradual decline [and]<br />

that inflation will subside to levels at or below those consistent with the<br />

Committee's dual mandate”<br />

• “Economic conditions…are likely to warrant exceptionally low levels for the<br />

federal funds rate for an extended period.”<br />

• “The Committee will complete its purchases <strong>of</strong> $600 billion <strong>of</strong> longer-term<br />

Treasury securities by the end <strong>of</strong> this month and will maintain its existing<br />

policy <strong>of</strong> reinvesting principal payments from its securities holdings”<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Board (http://www.federalreserve.gov/newsevents/press/monetary/20110622a.htm)<br />

71

Notes from Bernanke’s s press conference<br />

June 22, 2011<br />

• The “burn-<strong>of</strong>f” in the Fed’s securities portfolio has been put on hold: QE2<br />

ends on June 30, and the balance sheet will remain stable for now<br />

(reinvesting principal and interest)<br />

• QE2 did achieve something: a reduction in the probability <strong>of</strong> expected<br />

deflation implied by TIPS yields<br />

• Not reinvesting principal and interest would be the first step in an exit from<br />

policy accommodation<br />

• No timetable for initiating the exit has been determined<br />

• The FOMC’s “extended period” is not intended to be deliberately opaque,<br />

but it cannot be said exactly how long it would be<br />

• Bernanke conjecture: the extended period would be “at least” two or three<br />

FOMC meetings, with the emphasis on at least<br />

• Other communication tools are available to indicate the direction <strong>of</strong> Fed<br />

policy and timetable for exit from monetary policy accommodation<br />

Slide copyright 2011, TZ Economics<br />

Sources: Federal Reserve Board (http://www.federalreserve.gov/monetarypolicy/fomcpresconf20110622.htm)<br />

72

Appendix 4: Inflation (no mo da kine?)<br />

• Remember the idea behind inflation targeting:<br />

• The real side <strong>of</strong> the economy will achieve employment goals if<br />

inflation risk can be diminished<br />

• Credible monetary policy-making increases the potency <strong>of</strong><br />

countercyclical fiscal and monetary policy tools (especially at the<br />

zero bound for nominal interest rates)—small doses suffice<br />

• In principle, keeping your eye on the prize involves low and stable<br />

core inflation<br />

• Now concluded, QE2 should be seen through the lens <strong>of</strong> incipient<br />

deflation: what do we learn from Japan’s Lost Decade? Don’t let<br />

deflationary expectations take root (the risk in summer 2010)<br />

• Talk is cheap: we can see expectations revealed in securities pricing<br />

Slide copyright 2011, TZ Economics<br />

73

Long-term inflation expectations implied by Treasury<br />

yields (including unobservable inflation risk premia)<br />

3<br />

Jul 06, 07, 08<br />

Percentage points, difference<br />

between nominal U.S. Treasury<br />

yields and real (TIPS) yields<br />

2<br />

1<br />

0<br />

-1<br />

June 21 2011<br />

Jul 09, 10<br />

Feb 2009<br />

Nov 2008<br />

e<br />

σ π<br />

= 0.5%<br />

≈ 1.5−2.0%<br />

“target”<br />

-2<br />

FF<br />

1-yr<br />

2-yr<br />

3-yr<br />

5-yr<br />

7-yr<br />

10-yr<br />

20-yr<br />

30-yr<br />

Slide copyright 2011, TZ Economics<br />

Source: Federal Reserve Board (H.15 constant maturity yields); calculations by TZE through June 21, 2011<br />

74

Federal Reserve economic projections<br />

Mistaken date published in original<br />

(actual release date June 22, 2011)<br />

Slide copyright 2011, TZ Economics<br />

Source: Federal Reserve Board (http://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl20110622.pdf)<br />

75

The spoiler: real crude petroleum spot prices<br />

(West Texas Intermediate)<br />

160<br />

Monthly, in April 2011 $/bbl (log scale)<br />

80<br />

40<br />

20<br />

50 60 70 80 90 00 10<br />

Slide copyright 2011, TZ Economics<br />

Source: Federal Reserve Bank <strong>of</strong> St. Louis (http://research.stlouisfed.org/fred2/series/MCOILWTICO?cid=32358); deflation<br />

using U.S. consumer price index for all urban consumers (CPI-U) by TZ Economics<br />

76

U.S. consumer price inflation rates<br />

6<br />

Monthly s.a. percent change y-o-y<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

-1<br />

-2<br />

NBER recessions shaded<br />

Headline<br />

Core<br />

Transitory commodity<br />

price-based impulse<br />

Transitory commodity<br />

price-based impulse<br />

Transitory commodity<br />

price-based impulse<br />

-3<br />

00 02 04 06 08 10<br />

Slide copyright 2011, TZ Economics<br />

Source: BLS, U.S. Department <strong>of</strong> Labor<br />

77

Honolulu inflation varies around the U.S. urban<br />

average over the business cycle (booms and busts)<br />

Semiannual; percent change y-o-y<br />

8<br />

6<br />

4<br />

2<br />

0<br />

Honolulu<br />

U.S. city average<br />

NBER recessions shaded<br />

-2<br />

85 90 95 00 05 10<br />

Slide copyright 2011, TZ Economics<br />

Source: BLS, U.S. Department <strong>of</strong> Labor<br />

78

Overall Oahu Phillips Curve 1983-2010:<br />

inverse relationship between inflation and unemployment<br />

Honolulu inflation rate (%)<br />

8<br />

6<br />

4<br />

2<br />

0<br />

Boom<br />

Semiannual data<br />

1983-2010<br />

Bust<br />

-2<br />

1 2 3 4 5 6 7 8<br />

Oahu unemployment rate (%)<br />

Slide copyright 2011, TZ Economics<br />

Source: Bureau <strong>of</strong> Labor Statistics, Hawaii DLIR; seasonal adjustment using Census X-12 ARIMA filter, regressions<br />

on natural log <strong>of</strong> contemporaneous unemployment rate by TZE<br />

79

Oahu Phillips Curves since the 1970s: decrease in<br />

long-term inflation expectations shifted curve down<br />

Honolulu inflation rate (%)<br />

8<br />

6<br />

4<br />

2<br />

0<br />

-2<br />

"Japan" 1983-98<br />

"Subprime" 1998-2009<br />

Phillips curves (fitted)<br />

1 2 3 4 5 6 7 8<br />

Regression <strong>of</strong> Honolulu inflation rate ( pˆ<br />

t<br />

)<br />

on the Oahu unemployment rate ( u ) at time t.<br />

pˆ<br />

[ ln( )]<br />

= 12.67574 − 6.22218⋅<br />

(1983-1998)<br />

(0.094243) (0.63310)<br />

2 = 0.763018<br />

t u t<br />

AdjR<br />

F = 96.59607<br />

D . W.<br />

= 0.786456<br />

pˆ<br />

[ ln( )]<br />

= 10.30540 − 5.83584 ⋅ (1998-2009)<br />

(0.994873) (0.732546)<br />

2 = 0.751378<br />

t u t<br />

AdjR<br />

F = 6.346547<br />

D . W.<br />

= 0.736671<br />

Oahu unemployment rate (%)<br />

Slide copyright 2011, TZ Economics<br />

Source: Bureau <strong>of</strong> Labor Statistics, Hawaii DLIR; seasonal adjustment using Census X-12 ARIMA filter, regressions<br />

on natural logs <strong>of</strong> contemporaneous unemployment rates by TZE<br />

80

Oahu Phillips Curve since early-1990s:<br />

commodity price shocks pushing out the trade-<strong>of</strong>f<br />

Inflation rate (%)<br />

6<br />

5<br />

4<br />

3<br />

2<br />

1<br />

π *<br />

Boom<br />

2008H1<br />

2008H2<br />

2010<br />

Assumed long-term<br />

non-accelerating<br />

inflation equilibrium:<br />

( π )<br />

* ,u *<br />

Volatile global petroleum<br />

and commodity prices over<br />

last two years have exerted<br />

transitory inflation impulses<br />

0<br />

-1<br />

u *<br />

Bust<br />

2009<br />

2 3 4 5 6<br />

Unemployment rate (%)<br />

Slide copyright 2011, TZ Economics<br />

Source: Bureau <strong>of</strong> Labor Statistics, US Department <strong>of</strong> Labor; calculations by TZE<br />

81

Another trade-<strong>of</strong>f: inverse relationship between Oahu<br />

house price change, inventory remaining (1994-2010)<br />

40<br />

Single-family<br />

40<br />

Condominium<br />

% chng P(single-family) y-o-y<br />

30<br />

20<br />

10<br />

0<br />

-10<br />

ˆ<br />

p H<br />

[ ln( ( −5)<br />

)]<br />

= 32.80695 −15.36972⋅<br />

MRI<br />

(1.61912) (0.82424)<br />

AdjR<br />

2 = 0.6514993<br />

F = 347.7148<br />

D . W.<br />

= 1.218097<br />

% chng P(condos) (y-o-y)<br />

30<br />

20<br />

10<br />

0<br />

-10<br />

ˆ<br />

p H<br />

[ ln( ( −5)<br />

)]<br />

= 39.11897 − 20.23304⋅<br />

MRI<br />

(1.48397) (0.96947)<br />

AdjR<br />

2 = 0.785419<br />

F = 435.5696<br />

D . W.<br />

= 1.545932<br />

-20<br />

0 4 8 12 16 20 24<br />

-20<br />

0 4 8 12 16 20 24<br />

Months <strong>of</strong> inventory remaining (lagged 5)<br />

Months <strong>of</strong> inventory remaining (lagged 5)<br />

Slide copyright 2011, TZ Economics<br />

Source: Honolulu Board <strong>of</strong> Realtors (raw data); seasonal adjustment using Census X-12 ARIMA filter, regressions on<br />

natural log <strong>of</strong> months <strong>of</strong> inventory remaining (lagged 5 months) by TZE<br />

82

Oahu months <strong>of</strong> inventory remaining,<br />

through May 2011<br />

Months, [inventory(t) / sales(t –1)], s.a.<br />

20<br />

16<br />

12<br />

8<br />

4<br />

0<br />

Condominium<br />

Single-family<br />

98 00 02 04 06 08 10<br />

Slide copyright 2011, TZ Economics<br />

Source: Honolulu Board <strong>of</strong> Realtors; seasonal adjustment by TZE<br />

83

Appendix 5: (for tourism) remember: markets have<br />

two sides and most shocks are transitory<br />

Slide copyright 2011, TZ Economics<br />

84

Recession (demand) and lift (supply):<br />

Hawaii monthly domestic visitor arrivals<br />

520<br />

480<br />

U.S. recession shaded<br />

P T<br />

Thousands, s.a., log scale<br />

440<br />

400<br />

360<br />

320<br />

Additional<br />

Aloha Airlines &<br />

lift 2010<br />

ATA shutdowns<br />

Lehman<br />

Brothers<br />

03 04 05 06 07 08 09 10 11 12<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT, HTA; seasonal adjustment using Census X-12 ARIMA filter by TZE<br />

85

Monthly air seats operated to Hawaii<br />

Thousands, s.a., log scale<br />

Domestic (right scale)<br />

International (left)<br />

260<br />

240<br />

220<br />

200<br />

180<br />

Aloha/ATA<br />

shutdown<br />

P T<br />

U.S. recession shaded<br />

04 05 06 07 08 09 10 11<br />

680<br />

640<br />

600<br />

560<br />

520<br />

480<br />

Thousands, s.a., log scale<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT, HTA; seasonal adjustment using Census X-12 ARIMA filter by TZE<br />

86

Hotel industry performance indicators<br />

U.S. recessions shaded<br />

80<br />

Constant 2010$, s.a., log scale<br />

220<br />

200<br />

180<br />

160<br />

140<br />

Occupancy (right scale)<br />

Real room rate (left)<br />

94 96 98 00 02 04 06 08 10 12<br />

70<br />

60<br />

Percent, s.a.<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hospitality Advisors LLC; seasonal adjustment using Census X-12 ARIMA filter by TZE<br />

87

Hawaii monthly international visitor arrivals:<br />

shocks matter but are transitory<br />

240<br />

200<br />

Thousands, s.a., log scale<br />

160<br />

120<br />

Y2K<br />

9/11<br />

SARS<br />

H1N1-A<br />

Sendai<br />

80<br />

00 02 04 06 08 10<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT, HTA; seasonal adjustment using Census X-12 ARIMA filter by TZE<br />

88

Conditional annualized quarterly seasonally-<br />

adjusted Japanese visitor arrivals volatility<br />

1.4<br />

1.2<br />

9/11<br />

1.0<br />

Before wars were broadcast live<br />

Gulf<br />

SARS<br />

0.8<br />

0.6<br />

0.4<br />

H1N1-A<br />

0.2<br />

0.0<br />

75 80 85 90 95 00 05 10<br />

Slide copyright 2011, TZ Economics<br />

Sources: Arrivals data originally published by HVB, later DBEDT, raw data source here is UHERO; seasonal adjustment<br />

and calculation <strong>of</strong> threshold autoregressive conditional heteroskedasticity standard deviations by TZE<br />

89

Pre-/post<br />

/post-Sendai daily passenger arrivals growth<br />

Hawaii daily arriving passenger counts<br />

growth rates in percent vs. comparable days <strong>of</strong> week, one year earlier<br />

Flight origin: Domestic Canada Japan Other<br />

January-February 9.1 no data 6.2 20.9<br />

March 1-10 8.1 - -6.3 40.4<br />

March 11-31 1.9 - −24.2 24.5<br />

April 1-11 4.2 - −25.2 34.9<br />

April 12-19 (pre-Easter) 17.8 - −29.4 49.6<br />

April 20-27 4.8 - −24.4 35.2<br />

April 28 - May 8* 3.6 - −15.4 43.8<br />

May 9-31 2.2 −22.3 39.7<br />

June to-date † -0.9 −18.4 38.4<br />

Post-Sendai † 3.7 - −22.6 36.2<br />

Shares (Jan-Mar 10) 75.7% 18.5% 5.8%<br />

*Golden Week in Japan<br />

† Through Tuesday, June 6 for domestic, Monday, June 7 for international<br />

Slide copyright 2011, TZ Economics<br />

Sources: Raw data from DBEDT (http://hawaii.gov/dbedt/info/economic/data_reports/special/daily-pax-update.xls);<br />

compilation <strong>of</strong> interval year-over-year growth rates by TZE<br />

90

Appendix 6: the investment cycle is bottoming<br />

Slide copyright 2011, TZ Economics<br />

91

Hawaii real private building permit values<br />

800<br />

Monthly, million 2010 $, s.a., log scale<br />

400<br />

200<br />

100<br />

50<br />

75 80 85 90 95 00 05 10<br />

Slide copyright 2011, TZ Economics<br />

Sources: Hawaii DBEDT, County building departments, Bureau <strong>of</strong> the Census; deflation, seasonal adjustment using<br />

Census X-12 ARIMA filter and trend extract using Hodrick-Prescott filter by TZE<br />

92

Appendix 7: balance pragmatism against ideology,<br />

an illustration from federal fiscal imbalance<br />

Slide copyright 2011, TZ Economics<br />

93

Restoring federal fiscal balance<br />

“We do have to solve the fiscal situation and that’s probably going to take some compromise that’s a<br />

little hard to see right now. I think the real problem is that if one side wants no revenue increase in<br />

the form <strong>of</strong> tax increases then all future-oriented investment has to come out <strong>of</strong> some current<br />

program or redistributive part <strong>of</strong> the government’s operation, and those are Draconian choices.<br />

We should probably have increased taxes for a period <strong>of</strong> time to get past a deficit that we’ve created.<br />

We also don’t want to destroy whatever recovery we have, which is fragile. So there’s a debate<br />

going on about what the withdrawal rate should be.<br />

It’s encouraging that there’s serious debate going on about the fiscal situation now. …Even in<br />

Congress now, even if you think…it doesn’t look like a very well-organized debate, at least they’re<br />

debating something important…based on principles that various sides believe in, and that’s good. I<br />

mean, if this were a situation <strong>of</strong> not so benign neglect I think you and I would be very worried.<br />

I think there’s two streaks in America. We have an ideological streak, and I don’t mean that on one<br />

side or the other, both, and we have a pragmatic streak. And I think they come and go. We need<br />

this pragmatic streak to come out.”<br />

Michael Spence, recipient <strong>of</strong> the 2001 Nobel Memorial Price in Economic Sciences<br />

(with George Akerl<strong>of</strong> and Joseph Stiglitz)<br />

on Charlie Rose (May 27, 2011) http://www.charlierose.com/guest/view/7162<br />

Slide copyright 2011, TZ Economics<br />

94

Fiscal imbalance<br />

• The last time the discretionary portion <strong>of</strong> the federal budget imbalance was in<br />

full-employment surplus was before the 2001 recession<br />

• History suggests the probable zone <strong>of</strong> compromise for federal government<br />

receipts and outlays is 18-20% <strong>of</strong> GDP<br />

• Pragmatism requires that all available fiscal tools be used, whether for shortterm<br />

full-employment balance or long-term balance—e.g. Douglas Holtz-Eakins’<br />

(ex-CBO) social security fix:<br />

1. Raise the social security payroll tax<br />

2. <strong>Inc</strong>rease the retirement age<br />

3. Decrease social security benefits<br />

4. Means-test benefits<br />

5. Move the system toward hybrid accounts (SS + IRA/401k)<br />

• It’s impossible to get to full-employment federal budget balance without higher<br />

marginal tax rates, lower spending, and sacrifice <strong>of</strong> Sacred Cows*<br />

• It’s hard to argue that a reset to 2000 parameters would be a bad thing<br />

Slide copyright 2011, TZ Economics<br />

*like the tax deductibility <strong>of</strong> mortgage interest expense<br />

95

U.S. federal budget deficit as a percent <strong>of</strong> GDP<br />

4<br />

2<br />

Recessions shaded<br />

Percentage points<br />

0<br />

-2<br />

-4<br />

-6<br />

-8<br />

-10<br />

70 75 80 85 90 95 00 05 10 15<br />

Slide copyright 2011, TZ Economics<br />

Source: Congressional Budget Office, Budget and Economic Outlook Fiscal Years 2011 Through 2021<br />

(http://cbo.gov/ftpdocs/120xx/doc12039/BudgetTables[1].xls)<br />

96

Procyclical component <strong>of</strong> U.S. federal budget deficit<br />

attributable to automatic stabilizers as share <strong>of</strong> GDP<br />

2<br />

Automatic stabilizers<br />

Deficit without stabilizers<br />

Percentage points<br />

0<br />

-2<br />

-4<br />

-6<br />

-8<br />

Recessions shaded<br />

70 75 80 85 90 95 00 05 10 15<br />

Slide copyright 2011, TZ Economics<br />

Source: Congressional Budget Office, Budget and Economic Outlook Fiscal Years 2011 Through 2021<br />

(http://cbo.gov/ftpdocs/120xx/doc12039/BudgetTables[1].xls)<br />

97

Federal outlays as a percentage <strong>of</strong> GDP<br />

Slide copyright 2011, TZ Economics<br />

Source: Karl Case, Ray Fair and Sharon Oster, Principles <strong>of</strong> Macroeconomics, 10 th ed. (2012 forthcoming) Prentice Hall<br />

98

Federal personal income tax/taxable income (%)<br />

Slide copyright 2011, TZ Economics<br />

Source: Karl Case, Ray Fair and Sharon Oster, Principles <strong>of</strong> Macroeconomics, 10 th ed. (2012 forthcoming) Prentice Hall<br />

99

Federal government revenue and outlays<br />

as a percent <strong>of</strong> GDP through 2010<br />

26<br />

24<br />

Outlays<br />

Revenues<br />

Percent <strong>of</strong> GDP<br />

22<br />

20<br />

18<br />

I’m just going to guess<br />

that, pragmatically<br />

speaking, 18-20% is “it”<br />

16<br />

Vertical shaded areas denote recessions<br />

14<br />

70 75 80 85 90 95 00 05 10 15<br />

Slide copyright 2011, TZ Economics<br />

Source: Congressional Budget Office, Budget and Economic Outlook Fiscal Years 2011 Through 2021<br />

(http://cbo.gov/ftpdocs/120xx/doc12039/BudgetTables[1].xls)<br />

100

CBO projections were scary<br />

after and before Obama<br />

Slide copyright 2011, TZ Economics<br />

Source: Congressional Budget Office, Analysis <strong>of</strong> the President’s Budgetary Proposals for Fiscal Year 2012,<br />

http://www.cbo.gov/ftpdocs/121xx/doc12130/04-15-AnalysisPresidentsBudget.pdf<br />

101

Appendix 8: income distribution changes<br />

now confound U.S. economic policy options<br />

• The distribution <strong>of</strong> income in Hawaii and the U.S. has been widening<br />

since the mid- to late-20 th century<br />

• The rich are getting richer and the poor are getting richer (partly<br />

because technology is improving so fast)<br />

• But the rich have gotten richer way, way faster than everybody else<br />

• Implication: high income/high net worth households not only do not<br />

need a tax cut, they need to pay more in taxes<br />

Slide copyright 2011, TZ Economics<br />

102

U.S. income distribution 2007<br />

from the Survey <strong>of</strong> Consumer Finances<br />

%<br />

Histogram <strong>of</strong> the 2007 SCF income<br />

distribution (and <strong>of</strong> its smoothed<br />

kernel density estimates)<br />

<strong>Inc</strong>ome<br />

Slide copyright 2011, TZ Economics<br />

Source: Javier Diaz-Gimenez, Andy Glover and Jose-Victor Rios-Rull, “Facts on the Distributions <strong>of</strong> Earnings, <strong>Inc</strong>ome, and Wealth in the United States: 2007<br />

Update,” Federal Reserve Bank <strong>of</strong> Minneapolis Quarterly Review vol. 34, no. 1 (February 2011), pp. 2-31 http://www.minneapolisfed.org/research/qr/qr3411.pdf<br />

103

“The Hollowing Out <strong>of</strong> the Middle Class [sic]”<br />

Source: Mary C. Daly, “The ‘Shrinking’<br />

Middle Class?” FRBSF Economic Letter 97-<br />

07 (March 7, 1997)<br />

www.frbsf.org/econrsrch/wklyltr/el97-07.html<br />

A: 75 percent <strong>of</strong> the poverty line<br />

B: two times the poverty line<br />

C: five times the poverty line<br />

Economic<br />

mobility<br />

The “middle class” comprises families<br />

between B and C (2X to 5X poverty)<br />

92 percent <strong>of</strong> the loss in the middle class<br />

shifted higher, 7 percent shifted lower—the<br />

rise in income inequality occurred “through<br />

disproportionate increases in economic wellbeing,<br />

not through ‘immiserization.’”<br />

Slide copyright 2011, TZ Economics<br />

Note: definitional changes in the 2000 census prevented strict extension <strong>of</strong> these comparisons, but 2010 census data<br />

should permit renewed comparison, 1999-2009<br />

104

U.S. Lorenz Curves<br />

Cumulativeshare <strong>of</strong> household income (%)<br />

100<br />

80<br />

60<br />

40<br />

20<br />

0<br />

1967<br />

2009<br />

The Lorenz curve depicts the<br />

cumulative distribution function <strong>of</strong><br />

income, showing for each quintile<br />

<strong>of</strong> households (x-axis) the<br />

proportion <strong>of</strong> total income (y-axis)<br />

accruing cumulatively to those<br />

households. For example, for 2009<br />

3.4% <strong>of</strong> income was received by<br />

the lowest fifth <strong>of</strong> households in the<br />

U.S, and 8.6% was received by the<br />

second fifth. On the Lorenz curve,<br />

the lowest received 3.4% <strong>of</strong><br />

income and the two lowest<br />