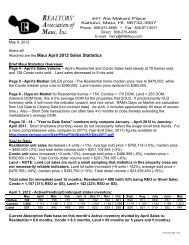

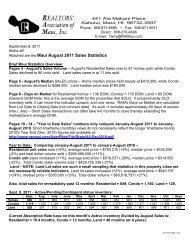

October 26, 2012 - REALTORS® Association of Maui, Inc.

October 26, 2012 - REALTORS® Association of Maui, Inc.

October 26, 2012 - REALTORS® Association of Maui, Inc.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>October</strong> <strong>26</strong>, <strong>2012</strong><br />

prepared for the<br />

Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong><br />

King Kamehameha Golf Club<br />

by Paul H. Brewbaker, Ph.D.<br />

TZ Economics, Kailua, Hawaii<br />

July 13, <strong>2012</strong><br />

Copyright <strong>2012</strong><br />

Paul H. Brewbaker, Ph.D.

Be careful what you wish for<br />

• In August 2005 I spoke to the Kauai Board <strong>of</strong> Realtors<br />

• I had all new data courtesy <strong>of</strong> Hawaii Information Service, their MLS provider<br />

• I get just as good <strong>Maui</strong> data from Terry Tolman at RAM—good enough to dig deep<br />

• My message on Kauai in 2005: it’s over, you just had your best year, prices are<br />

going to peak in the next 12 months and then you will become the living dead<br />

• Oops!<br />

• Angry Realtor® ladies harangued me from the front row, bracelets jangling:<br />

“but when, when will prices start rising again?!?”<br />

• To quiet them I said: <strong>October</strong> <strong>26</strong>, <strong>2012</strong> ...and they all put it in their Palm Treos<br />

• Oops.<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

1

Oahu, <strong>Maui</strong> single-family median sales prices: at<br />

quarterly frequency, recovery appears in the last year<br />

800<br />

Quarterly, 000$, s.a. (log scale)<br />

400<br />

<strong>Maui</strong><br />

Oahu<br />

Recessions shaded<br />

200<br />

2000 2002 2004 2006 2008 2010 <strong>2012</strong><br />

Sources:<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, Honolulu Board <strong>of</strong> Realtors; seasonal adjustment and trend extraction by TZE<br />

2

Oahu, <strong>Maui</strong> single-family median sales prices: at<br />

monthly frequency, recovery appears in the last year<br />

800<br />

Monthly, 000$, s.a. (log scale)<br />

400<br />

<strong>Maui</strong><br />

Oahu<br />

Recessions shaded<br />

200<br />

2000 2002 2004 2006 2008 2010 <strong>2012</strong><br />

Sources:<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, Honolulu Board <strong>of</strong> Realtors; seasonal adjustment and trend extraction by TZE<br />

3

<strong>Maui</strong> economic data<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

4

<strong>Maui</strong> non-agricultural payroll employment (jobs)<br />

75<br />

Monthly, 000, s.a. (log scale)<br />

70<br />

65<br />

60<br />

55<br />

50<br />

45<br />

90 95 00 05 10<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hawaii DLIR, Hawaii DBEDT; seasonal adjustment and calculation <strong>of</strong> generalized autoregressive conditional<br />

heteroskedasticity annualized standard deviations <strong>of</strong> the log change in payroll employment by TZ Economics<br />

5

Great Recession = beat-down; 9/11 = Black Swan:<br />

<strong>Maui</strong> nonagricultural job count conditional volatility<br />

.07<br />

9/11<br />

.06<br />

91:09<br />

09:11<br />

.05<br />

.04<br />

The Great<br />

Recession<br />

(cluster)<br />

.03<br />

.02<br />

.01<br />

.00<br />

90 95 00 05 10<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hawaii DLIR, Hawaii DBEDT; seasonal adjustment and calculation <strong>of</strong> generalized autoregressive conditional<br />

heteroskedasticity annualized standard deviations <strong>of</strong> the log change in payroll employment by TZ Economics<br />

6

<strong>Maui</strong> visitor arrivals since the 1980s:<br />

rebuilding from the loss <strong>of</strong> Aloha Airlines, ATA<br />

Thousands, s.a. (log scale)<br />

200<br />

180<br />

Recessions shaded<br />

80<br />

160<br />

40<br />

140<br />

120<br />

9/11<br />

Aloha<br />

Aloha<br />

20<br />

90 95 00 05 10<br />

Domestic<br />

90 95 00 05 10<br />

International<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hawaii Tourism Authority, Hawaii DBEDT; seasonal adjustment by TZ Economics<br />

7

<strong>Maui</strong> monthly visitor arrivals, seasonally-adjusted<br />

adjusted<br />

220<br />

Recessions shaded<br />

Thousands (log scale)<br />

200<br />

180<br />

160<br />

Aloha<br />

Aloha<br />

140<br />

9/11<br />

00 02 04 06 08 10 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hawaii Tourism Authority, Hawaii DBEDT; seasonal adjustment by TZ Economics<br />

8

<strong>Maui</strong> monthly visitor arrivals and payroll<br />

employment exhibit strong co-movement<br />

Thousands (log scale)<br />

76<br />

72<br />

68<br />

64<br />

60<br />

Visitor arrivals (right scale)<br />

Non-ag jobs (left)<br />

Recessions shaded<br />

9/11<br />

Jobs<br />

Aloha<br />

Aloha<br />

Arrivals<br />

240<br />

220<br />

200<br />

180<br />

160<br />

140<br />

Thousands (log scale)<br />

56<br />

00 02 04 06 08 10 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hawaii DLIR, Tourism Authority, Hawaii DBEDT; seasonal adjustment by TZ Economics<br />

9

<strong>Maui</strong> nonagricultural payroll employment<br />

Thousands (log scale)<br />

Private (right scale)<br />

Public (left)<br />

10.5<br />

10.0<br />

9.5<br />

9.0<br />

8.5<br />

Recession shaded<br />

64<br />

60<br />

56<br />

52<br />

Thousands (log scale)<br />

8.0<br />

02 03 04 05 06 07 08 09 10 11 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hawaii DLIR, Hawaii DBEDT; seasonal adjustment by TZ Economics<br />

10

<strong>Maui</strong> unemployment rate<br />

10<br />

8<br />

Recessions shaded<br />

Aloha<br />

Aloha<br />

Percent, s.a.<br />

6<br />

4<br />

9/11<br />

2<br />

0<br />

00 02 04 06 08 10 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Bureau <strong>of</strong> Labor Statistics, U.S. Department <strong>of</strong> Labor, Hawaii DLIR, Hawaii DBEDT; data through May <strong>2012</strong>,<br />

seasonal adjustment <strong>of</strong> Hawaii data by TZE<br />

11

U.S. and Hawaii unemployment rates<br />

12<br />

Recessions shaded<br />

Percent, s.a.<br />

10<br />

8<br />

6<br />

4<br />

U.S. average<br />

Neighbor Islands<br />

Oahu<br />

Neighbor Isles<br />

like mainland<br />

2<br />

0<br />

Neighbor Isles<br />

like Oahu<br />

00 02 04 06 08 10 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Bureau <strong>of</strong> Labor Statistics, U.S. Department <strong>of</strong> Labor, Hawaii DLIR, Hawaii DBEDT; data through May <strong>2012</strong>,<br />

seasonal adjustment <strong>of</strong> Hawaii data by TZE<br />

12

Kauai monthly real nonresidential building permits<br />

100<br />

Recessions shaded<br />

Million 2011 dollars, log scale<br />

10<br />

BOH data<br />

DBEDT data<br />

1<br />

75 80 85 90 95 00 05 10<br />

Sources:<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Bank <strong>of</strong> Hawaii, Hawaii DBEDT, U.S. Bureau <strong>of</strong> the Census; deflation and Hodrick-Prescott filter by TZE<br />

13

<strong>Maui</strong> monthly real residential building permit values<br />

Recessions shaded<br />

Million 2011 dollars, log scale<br />

100<br />

10<br />

BOH data<br />

DBEDT data<br />

1<br />

75 80 85 90 95 00 05 10<br />

Sources:<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Bank <strong>of</strong> Hawaii, Hawaii DBEDT, U.S. Bureau <strong>of</strong> the Census; deflation and Hodrick-Prescott filter by TZE<br />

14

Quarterly new housing units authorized<br />

by building permit: no glut any time soon<br />

000 units, s.a., log scale<br />

1.0<br />

0.1<br />

Oahu, Hawaii, Kauai (right scale)<br />

<strong>Maui</strong> units (left scale)<br />

Recessions shaded<br />

Recessions shaded<br />

4<br />

3<br />

2<br />

1<br />

0<br />

000 units, s.a., log scale<br />

80 85 90 95 00 05 10 15<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources:<br />

Bank <strong>of</strong> Hawaii, Hawaii DBEDT; deflation and Hodrick-Prescott filter by TZE<br />

15

<strong>Maui</strong> existing home sales volumes<br />

Recessions shaded<br />

Monthly units, s.a. (log scale)<br />

160<br />

80<br />

40<br />

Condominium<br />

Single-family<br />

00 02 04 06 08 10 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources:<br />

Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, Hawaii DBEDT; seasonal adjustment by TZE<br />

16

<strong>Maui</strong> existing home sales volumes<br />

1000<br />

Recessions shaded<br />

Quarterly units, s.a. (log scale)<br />

100<br />

Condominium<br />

Single-family<br />

10<br />

80 85 90 95 00 05 10<br />

Sources:<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, Hawaii DBEDT, UHERO, Prudential Locations; seasonal adjustment by TZE<br />

17

<strong>Maui</strong> existing home sales median prices<br />

800<br />

Recessions shaded<br />

Quarterly units, s.a. (log scale)<br />

400<br />

200<br />

100<br />

Single-family<br />

Condominium<br />

95 00 05 10<br />

Sources:<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, Hawaii DBEDT, UHERO, Prudential Locations; seasonal adjustment by TZE<br />

18

Mythbusters: : the jobless [sic] recovery<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

19

Honolulu Star-Advertiser (July 14, 2011) http://www.staradvertiser.com/business/20110714__Jobless_recovery_persists_in_Hawaii.html

Nonagricultural payroll recovery:<br />

not fast enough is not the same as not at all<br />

Thousand jobs, s.a. (log scale)<br />

640<br />

620<br />

600<br />

580<br />

560<br />

540<br />

520<br />

P T<br />

Jobless<br />

recovery<br />

2001-2003<br />

U.S. recessions shaded;<br />

Vertical line is 9/11<br />

P T<br />

Up: the new down<br />

2010-<strong>2012</strong><br />

U.S. (right scale)<br />

Hawaii (left)<br />

00 02 04 06 08 10 12<br />

140<br />

136<br />

132<br />

128<br />

124<br />

Million jobs, s.a. (log scale)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hawaii DLIR and DBEDT, U.S. Bureau <strong>of</strong> Labor Statistics; national data through May <strong>2012</strong>, seasonal adjustment <strong>of</strong><br />

Hawaii data through April <strong>2012</strong> by TZE<br />

21

Nonagricultural payrolls: Neighbor Islands took a<br />

bigger hit than Oahu, now are slowly re-accelerating<br />

Monthly jobs in 000 (s.a.) log scale<br />

175<br />

170<br />

165<br />

160<br />

155<br />

150<br />

145<br />

U.S. recession shaded<br />

Neighbor<br />

Isles<br />

−10%<br />

P T<br />

Oahu (right scale)<br />

Neighbor Isles (left)<br />

Oahu −5.5%<br />

460<br />

450<br />

440<br />

430<br />

420<br />

410<br />

400<br />

Monthly jobs in 000 (s.a.) log scale<br />

05 06 07 08 09 10 11 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hawaii DLIR, Hawaii DBEDT; seasonal adjustment by TZ Economics<br />

22

Index <strong>of</strong> real GDP: peak quarter = 1.000<br />

U.S. real GDP indexed to cyclical peaks:<br />

recession ended 3 years ago<br />

1.100Previous 10 recessions*<br />

1.050<br />

1.000<br />

0.950<br />

0.900<br />

Great Recession 2008-09<br />

2007Q4<br />

Recession<br />

Recovery<br />

<strong>2012</strong>Q1P<br />

2006 2007 2008 2009 2010 2011 <strong>2012</strong> 2013<br />

*Recessions since World War II—averages aligned to peak quarter <strong>of</strong> each business cycle and to 2007Q4<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Pr<strong>of</strong>essor Robert Hall, Stanford University and Chair, NBER Dating Committee; Bureau <strong>of</strong> Economic Analysis,<br />

U.S. Department <strong>of</strong> Commerce; includes <strong>2012</strong>Q1P data and NABE forecasts though 2013Q4<br />

23

Distribution <strong>of</strong> annual U.S. real GDP growth<br />

forecasts in the May <strong>2012</strong> NABE survey<br />

5<br />

Percent change and<br />

geometric mean<br />

5<br />

4<br />

<strong>2012</strong> forecast: 2.37%<br />

4<br />

2013 forecast: 2.68%*<br />

3<br />

3<br />

2<br />

2<br />

1<br />

1<br />

0<br />

0 5 10 15 20<br />

0<br />

0 5 10 15 20<br />

<strong>2012</strong> 2013<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: National <strong>Association</strong> for Business Economics (public summary at http://www.nabe.com/publib/macsum.html);<br />

histograms and mean calculations by TZE<br />

24

U.S. real GDP growth NABE forecasts May <strong>2012</strong><br />

P T<br />

Percent change, quarterly, annualized<br />

4<br />

0<br />

-4<br />

-8<br />

Recession shaded<br />

Actual<br />

NABE May <strong>2012</strong><br />

Top five forecasts<br />

Bottom five forecasts<br />

06 07 08 09 10 11 12 13 14<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: BEA (http://www.bea.gov/national/index.htm#gdp); NABE Outlook “Subpar Recovery Exists; Forecasters Expect<br />

Improvement in <strong>2012</strong>,” (May 21, <strong>2012</strong>) (http://www.nabe.com/publib/macsum.html)<br />

25

Federal Reserve core PCE inflation and real GDP<br />

growth rate projections released in June <strong>2012</strong><br />

Central tendencies and ranges FOMC<br />

meeting participants’ projections for PCE<br />

inflation <strong>2012</strong>-14 and over the longer run<br />

Central tendencies and ranges FOMC meeting<br />

participants’ projections for real GDP growth<br />

rate <strong>2012</strong>-14 and over the longer run<br />

Percent Percent<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Board minutes <strong>of</strong> the Federal Open Market Committee meeting June 20, <strong>2012</strong><br />

(http://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl<strong>2012</strong>0620.pdf)<br />

<strong>26</strong>

Federal Reserve economic outlook June <strong>2012</strong>:<br />

2% longer run forecast consistent with policy goal<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Board Members and Federal Reserve Bank Presidents (advance release with FOMC minutes)<br />

(June 20, <strong>2012</strong>) (http://www.federalreserve.gov/monetarypolicy/files/fomcprojtabl<strong>2012</strong>0620.pdf)<br />

27

What the Fed wants to avoid with an explicit inflation<br />

target: misinterpretation <strong>of</strong> inflation risk (like before)<br />

10<br />

January 1994: FOMC begins raising the fed funds target;<br />

no announcement, no forecast, no statement <strong>of</strong> strategy,<br />

markets over-reacted to inflation risk (bond sell-<strong>of</strong>f)<br />

8<br />

6<br />

Percent<br />

4<br />

2<br />

Recession shaded<br />

0<br />

89 90 91 92 93 94 95 96<br />

After the 1990-91 (Gulf War) recession<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Board (http://www.federalreserve.gov/releases/h15/current/)<br />

28

Treasury yields in early-2000s had series <strong>of</strong> “false<br />

starts” before Fed removed monetary policy<br />

accommodation at a “measured pace”<br />

7<br />

Percent<br />

6<br />

5<br />

4<br />

3<br />

2<br />

1<br />

0<br />

Recession shaded<br />

98 99 00 01 02 03 04 05<br />

Even before the Fed<br />

finished easing in<br />

2003, and despite<br />

explicit fed funds<br />

announcements, longterm<br />

bond yields<br />

experienced a bumpy<br />

transition and return to<br />

LR equilibrium as the<br />

Fed removed policy<br />

accommodation,<br />

2004-2006<br />

After the 2001 (dot.com) recession<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Board (http://www.federalreserve.gov/releases/h15/current/)<br />

29

Treasury yields now are guided by explicit statements<br />

<strong>of</strong> Fed policy goals and long-run<br />

equilibria<br />

Percent<br />

6<br />

5<br />

4<br />

3<br />

Recession shaded<br />

QE1<br />

QE21<br />

Operation Twist<br />

Now the Federal Open<br />

Market Committee<br />

(FOMC) tells you their<br />

short-term forecast,<br />

longer-term steadystate<br />

equilibrium<br />

expectations and<br />

policy goals<br />

2<br />

1<br />

0<br />

06 07 08 09 10 11 12 13 14 15 16<br />

Fed funds target rate<br />

trajectory implied by<br />

FOMC participants’<br />

own forecasts<br />

After the 2007-09 Great Recession<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Board (http://www.federalreserve.gov/releases/h15/current/;<br />

http://www.federalreserve.gov/monetarypolicy/files/fomcminutes<strong>2012</strong>0125.pdf)<br />

30

Year-end end fed funds rate forecast distributions<br />

(FOMC, June 20, <strong>2012</strong>) and weighted averages<br />

Percent (in 25 b.p. increments)<br />

5.0<br />

5.0<br />

5.0<br />

5.0<br />

4.0<br />

4.0<br />

4.0<br />

4.0<br />

LR: 4.105%<br />

3.0<br />

3.0<br />

3.0<br />

3.0<br />

2.0<br />

2.0<br />

2.0<br />

2.0<br />

1.0<br />

<strong>2012</strong>: 0.303%<br />

1.0<br />

2013: 0.513%<br />

1.0<br />

2014: 1.105%<br />

1.0<br />

0.0<br />

0 5 10 15<br />

0.0<br />

0 5 10 15<br />

0.0<br />

0 5 10 15<br />

0.0<br />

0 5 10 15<br />

Number <strong>of</strong> forecasts for each rate level in 25 basis point increments (bar length),<br />

and means<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Board (http://www.federalreserve.gov/monetarypolicy/files/fomcminutes<strong>2012</strong>0125.pdf)<br />

31

Nominal and real U.S. Treasury yields<br />

5<br />

Jul 06<br />

4<br />

Jul 07<br />

Jul 08<br />

3<br />

2<br />

Jul 2007<br />

Jul 2006<br />

3<br />

Jul 09<br />

Jul 10<br />

1<br />

Jul 2009<br />

Jul 2008<br />

2<br />

1<br />

Jul 11<br />

June <strong>2012</strong><br />

0<br />

-1<br />

Jul 2010<br />

Jul 2011<br />

June <strong>2012</strong><br />

0<br />

FF<br />

1-yr<br />

2-yr<br />

3-yr<br />

5-yr<br />

7-yr<br />

10-yr<br />

20-yr<br />

30-yr<br />

-2<br />

FF<br />

1-yr<br />

2-yr<br />

3-yr<br />

5-yr<br />

7-yr<br />

10-yr<br />

20-yr<br />

30-yr<br />

U.S. Treasury yield curve<br />

Treasury inflation-protected securities<br />

(TIPS) yield curve<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

32

Long-term inflation expectations: difference<br />

between nominal and real U.S. Treasury yields<br />

3<br />

Percentage points, difference<br />

between nominal U.S. Treasury<br />

yields and real (TIPS) yields<br />

2<br />

1<br />

0<br />

-1<br />

Jul 06/07/08/11<br />

June <strong>2012</strong><br />

Jul 09/10<br />

Feb 2009<br />

Nov 2008<br />

2.0% PCE<br />

deflator goal<br />

1.2-1.7% PCE<br />

deflator <strong>2012</strong><br />

FOMC forecast<br />

central tendency<br />

-2<br />

FF<br />

1-yr<br />

2-yr<br />

3-yr<br />

5-yr<br />

7-yr<br />

10-yr<br />

20-yr<br />

30-yr<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Board (H.15 constant maturity yields); calculations by TZE through June <strong>2012</strong>, inflation risk<br />

premium is 15-20 b.p. (See http://www.federalreserve.gov/pubs/feds/<strong>2012</strong>/<strong>2012</strong>06/<strong>2012</strong>06pap.pdf)<br />

33

Still waiting for the double-dip?<br />

dip?<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

34

Spring (May) 2011: double-dip dip headlines keep<br />

double-dip dip recession fears alive and investors scared<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: web sites as illustrated (all from the end <strong>of</strong> May 2011)<br />

35

“Overshooting” models <strong>of</strong> asset price dynamics<br />

Simulated asset price dynamics in<br />

a model <strong>of</strong> “slow-moving capital”<br />

P t<br />

Sound effect:<br />

“boy-yoy-yoy-yoy-yoing”<br />

P 0<br />

P T<br />

t 0<br />

Time<br />

“The key implication is that supply or demand shocks must be<br />

absorbed on short notice by a limited set <strong>of</strong> investors. The risk<br />

aversion or limited capital <strong>of</strong> the currently available investors,<br />

including intermediaries, leads them to require a price concession in<br />

order to absorb the supply or demand shock. They plan to ‘lay <strong>of</strong>f’<br />

the associated risk over time as other investors become available.<br />

As a result, the initial price impact is followed by a price reversal that<br />

may occur over an extended period <strong>of</strong> time.”<br />

Simulated asset price dynamics in<br />

a logistic growth model<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Darrell Duffie, “Asset Price Dynamics with Slow-Moving Capital” Journal <strong>of</strong> Finance vol. 65 no. 4 (August 2010) pp 1239-<br />

1<strong>26</strong>7 (http://www.darrellduffie.com/uploads/pubs/DuffieAFAPresidentialAddress2010.pdf); TZ Economics calculations<br />

36

S&P 500 Index: overshooting + oscillation after<br />

Congressional FAIL (Aug. 3, 2011; Nov. 23, 2011)<br />

1500<br />

1400<br />

1941-43 = 10 (log scale)<br />

1300<br />

1200<br />

1100<br />

Supercommittee FAIL<br />

Trading range prior to<br />

the August 3, 2011<br />

federal debt ceiling<br />

“deadline”<br />

1000<br />

Overshooting + oscillation<br />

after Aug. 3, 2011* FAIL <strong>of</strong><br />

Congress to commit to<br />

long-term deficit reduction<br />

11:1 11:2 11:3 11:4 12:1 12:2<br />

*Federal debt ceiling “deadline”<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Standard & Poor’s, Federal Reserve Bank <strong>of</strong> St. Louis; daily closing data through June 21, <strong>2012</strong><br />

37

S&P Case-Shiller<br />

price indexes (“relative(<br />

to Jan 2000”):<br />

“double-dip” is overshooting + oscillation<br />

P T<br />

January 2000 = 100, s.a., log scale<br />

200<br />

100<br />

Denver<br />

Los Angeles<br />

San Diego<br />

San Francisco<br />

Denver (relatively stable)<br />

Phoenix<br />

Las Vegas<br />

U.S. recession shaded<br />

2006 2007 2008 2009 2010 2011 <strong>2012</strong><br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Standard & Poor’s; seasonal adjustment using Census X-12 filter by TZ Economics<br />

38

Median CA existing single-family home prices:<br />

“double-dip” or “overshooting + oscillation?”<br />

Quarterly, thousand $, s.a. (log scale)<br />

900<br />

800<br />

700<br />

600<br />

500<br />

400<br />

300<br />

U.S. recession shaded<br />

P T<br />

Oahu (Honolulu) its own private Idaho<br />

San Jose, Sunnyvale, Santa Clara<br />

Anaheim, Santa Ana, Irvine<br />

San Francisco, Oakland, Fremont<br />

San Diego, Carlsbad, San Marcos<br />

Los Angeles, Long Beach, Santa Ana<br />

05 06 07 08 09 10 11 12 13<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors, National <strong>Association</strong> <strong>of</strong> Realtors; seasonal adjustment by TZE using Census X-12<br />

ARIMA filter, data through first quarter <strong>2012</strong><br />

39

Oahu housing market most stable—relatively<br />

relatively—<strong>of</strong><br />

Hawaii Islands and many mainland urban markets<br />

800<br />

700<br />

600<br />

Oahu<br />

800<br />

700<br />

600<br />

Orange Co., CA<br />

500<br />

500<br />

400<br />

800<br />

05 06 07 08 09 10 11 12<br />

400<br />

800<br />

05 06 07 08 09 10 11 12<br />

700<br />

700<br />

600<br />

500<br />

<strong>Maui</strong><br />

600<br />

500<br />

Kauai<br />

400<br />

05 06 07 08 09 10 11 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors, Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, National <strong>Association</strong> <strong>of</strong> Realtors, Kauai Board <strong>of</strong><br />

Realtors / Hawaii Information Service; seasonal adjustment by TZE using Census X-12 ARIMA filter<br />

400<br />

05 06 07 08 09 10 11 12<br />

40

Oahu median single-family home prices returning to<br />

the upper end <strong>of</strong> “the zone,” 2005-<strong>2012</strong><br />

<strong>2012</strong><br />

700<br />

600<br />

Thousand dollars, log scale<br />

500<br />

400<br />

300<br />

92 94 96 98 00 02 04 06 08 10 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors; TZ Economics<br />

41

Unraveling <strong>of</strong> median single-family home prices on<br />

two Neighbor Islands: that was the bottom<br />

Quarterly, thousand $, s.a. (log scale)<br />

800<br />

700<br />

600<br />

500<br />

400<br />

U.S. recession shaded<br />

<strong>Maui</strong><br />

Kauai<br />

Kauai*<br />

<strong>Maui</strong><br />

05 06 07 08 09 10 11 12 13<br />

*April-May <strong>2012</strong><br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, Hawaii Information Service; seasonal adjustment by TZE using Census X-12<br />

ARIMA filter<br />

42

Three relevant trade-<strong>of</strong>fs: inverse relationships<br />

between three pairs <strong>of</strong> variables provide guidance<br />

Honolulu inflation vs. unemployment<br />

• “Supply shocks” from recent energy impulses (Arab Spring, Japan seismic shock),<br />

unemployment falling from over 6.5% to 5.5%, while core inflation rebounds from<br />

near zero to 2% (plus energy boost), consistent with historical recovery transitions<br />

Real hotel room rate appreciation vs. hotel vacancy rates (1 minus occupancy)<br />

• Consistent with historical pattern, breakout above 73% occupancy from below<br />

implies return to real rates <strong>of</strong> appreciation, rising real yields<br />

Rates <strong>of</strong> home price appreciation vs. months <strong>of</strong> MLS inventory remaining<br />

• Transition from 12 months (2008) to 4 months (<strong>2012</strong>) remaining implies an<br />

acceleration <strong>of</strong> home price increase this year to range <strong>of</strong> 5-10%, rising<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

43

Trade-<strong>of</strong>fs, 1976-2011, between Hawaii inflation and<br />

unemployment (and Fed’s s target inflation zone)<br />

Hawaii’s<br />

Phillips Curve<br />

12<br />

8<br />

With oil and other supply shocks (1974, 1979),<br />

and high “unanchored” inflation expectations<br />

Inflation (%)<br />

4<br />

FOMC goal: 2%<br />

PCE inflation<br />

0<br />

Trade-<strong>of</strong>f 1983-1998<br />

-4<br />

Forecast<br />

Trade-<strong>of</strong>f since 1998<br />

0 2 4 6 8 10<br />

Unemployment (%)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Bureau <strong>of</strong> Labor Statistics, U.S. Department <strong>of</strong> Labor, Hawaii DBEDT and DLIR; all calculations by TZE<br />

44

Recent events: supply shocks since the recession<br />

Oahu inflation and unemployment data, 1998-2011<br />

Inflation (%)<br />

pˆ<br />

t<br />

8<br />

6<br />

2006<br />

Assumed long-term nonaccelerating<br />

inflation<br />

equilibrium:<br />

*<br />

( pˆ<br />

)<br />

* t , ut<br />

4<br />

2007<br />

2008<br />

2011<br />

*<br />

ˆ t p<br />

2<br />

2010<br />

Post-recession petroleum<br />

inflation, financial frictions<br />

(Hawaii Clean Energy Policy?)<br />

0<br />

2009<br />

-2<br />

1998<br />

1 2 3 4 5 6 7<br />

Unemployment (%)<br />

*<br />

u t<br />

u t<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Bureau <strong>of</strong> Labor Statistics, US Department <strong>of</strong> Labor; calculations by TZE<br />

45

Low-sulfur petroleum price benchmark:<br />

North Sea (Europe) Brent crude oil<br />

160<br />

P T<br />

Monthly, dollars/barrel (log scale)<br />

80<br />

40<br />

U.S. recession shaded<br />

05 06 07 08 09 10 11 12<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Federal Reserve Bank <strong>of</strong> St. Louis<br />

(http://research.stlouisfed.org/fred2/series/MCOILWTICO/downloaddata?cid=32217)<br />

46

Historical quarterly trade-<strong>of</strong>fs, 1978-2011,<br />

between Hawaii hotel room real rate<br />

movements and hotel vacancy rates<br />

15<br />

Real room rate changes (% y-o-y)<br />

10<br />

5<br />

0<br />

-5<br />

-10<br />

-15<br />

.10 .15 .20 .25 .30 .35 .40 .45<br />

Think <strong>of</strong> it as a trade-<strong>of</strong>f between<br />

appreciation (in real room rates)<br />

and unemployment (<strong>of</strong> hotel rooms)<br />

Hotel vacancy rate (%)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hospitality Advisors LLC, Hawaii DBEDT, U.S. Bureau <strong>of</strong> Labor Statistics; regression by TZE<br />

47

Hawaii hotel room real rates and vacancy:<br />

more aggressive yield recapture in last few years<br />

15<br />

Realroom ratechanges(%y-o-y)<br />

10<br />

end-2011<br />

5<br />

0<br />

-5<br />

-10<br />

2009Q3<br />

-15<br />

.10 .15 .20 .25 .30 .35 .40 .45<br />

Hotel vacancy rate (%)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Hospitality Advisors LLC, Hawaii DBEDT, U.S. Bureau <strong>of</strong> Labor Statistics; regression by TZE<br />

48

Trade-<strong>of</strong>fs, 1994-2011, between Oahu SF home price<br />

movements and months <strong>of</strong> inventory remaining<br />

The Sklarz Curve<br />

% change P(single-family)<br />

40<br />

30<br />

20<br />

10<br />

0<br />

-10<br />

Again, think <strong>of</strong> it as a trade-<strong>of</strong>f<br />

between inflation (in home prices)<br />

and unemployment (<strong>of</strong> houses)<br />

Shaded intersection: <strong>2012</strong> forecast<br />

-20<br />

0 4 8 12 16 20 24<br />

Months <strong>of</strong> inventory (-5)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors; regression by TZE as anticipated in as anticipated in Norm Miller and Mike Sklarz,<br />

“A Note on Leading Indicators <strong>of</strong> House Price Trends,” Journal <strong>of</strong> Real Estate Research 1:1 (Fall 1986) pp. 99-109<br />

49

Trade-<strong>of</strong>fs between Oahu SF prices and inventory<br />

remaining: you just missed the first year<br />

%change P(single-family)<br />

40<br />

30<br />

20<br />

10<br />

0<br />

-10<br />

Spring <strong>2012</strong><br />

Summer 2009<br />

Brewbaker says the<br />

recession is over?<br />

-20<br />

0 4 8 12 16 20 24<br />

Summer 2011<br />

“Double dip” fetishism<br />

Months <strong>of</strong> inventory (-5)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors; regression by TZE as anticipated in as anticipated in Norm Miller and Mike Sklarz,<br />

“A Note on Leading Indicators <strong>of</strong> House Price Trends,” Journal <strong>of</strong> Real Estate Research 1:1 (Fall 1986) pp. 99-109<br />

50

The Sklarz Curve during the last housing<br />

cycle—trough to trough (1999-2011)<br />

40<br />

40<br />

%chng P(single-family) y-o-y<br />

30<br />

20<br />

10<br />

0<br />

-10<br />

Single-family<br />

%chng P(condominium) y-o-y<br />

30<br />

20<br />

10<br />

0<br />

-10<br />

Condominium<br />

-20<br />

0 4 8 12 16<br />

-20<br />

0 4 8 12 16<br />

Months <strong>of</strong> inventory remaining (-5)<br />

Months <strong>of</strong> inventory remaining (-5)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Honolulu Board <strong>of</strong> Realtors (raw data); seasonal adjustment using Census X-12 ARIMA filter, regressions on<br />

natural log <strong>of</strong> months <strong>of</strong> inventory remaining (lagged 5 months) by TZE through April <strong>2012</strong><br />

51

<strong>Maui</strong> single-family home days on market<br />

200<br />

Recessions shaded<br />

180<br />

160<br />

Days<br />

140<br />

120<br />

100<br />

80<br />

2000 2002 2004 2006 2008 2010 <strong>2012</strong><br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong><br />

52

<strong>Maui</strong> SF days on market seasonality (right)<br />

and underlying trend (left); data through June <strong>2012</strong><br />

200<br />

180<br />

1.2<br />

160<br />

1.1<br />

140<br />

120<br />

1.0<br />

100<br />

0.9<br />

80<br />

2000 2002 2004 2006 2008 2010 <strong>2012</strong><br />

<strong>Maui</strong> single-family days on market (s.a.)<br />

and underlying trend through April<br />

00 01 02 03 04 05 06 07 08 09 10 11 12<br />

<strong>Maui</strong> single-family days on market<br />

seasonal adjustment factors (avg. = 1)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>; seasonal adjustment by TZE<br />

53

Sklarz Curve, RAM version: use “days on market”<br />

60<br />

Single-family pricechange (%)<br />

40<br />

20<br />

0<br />

-20<br />

Prices rising<br />

Prices falling<br />

-40<br />

80 100 120 140 160 180 200<br />

Days on market (trend) (-5 months)<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>; regression by TZE<br />

54

Toxicity: learning from mortgage delinquency<br />

• The Great Recession, concluding the sub-prime mortgage lending-driven housing<br />

“bubble” that preceded it, had legacy <strong>of</strong> wide geographic delinquency variation<br />

• Great Recession notable for anomalous spike in serious delinquency<br />

• Setting up a comparison: house price movements, delinquency changes<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

55

U.S. delinquency rate on single-family residential<br />

mortgages, domestic <strong>of</strong>fices <strong>of</strong> commercial banks<br />

12<br />

Recessions shaded<br />

10<br />

Percent, s.a.<br />

8<br />

6<br />

4<br />

2<br />

0<br />

1995 2000 2005 2010<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Bank <strong>of</strong> St. Louis (http://research.stlouisfed.org/fred2/series/DRSFRMACBS); graphic by TZE<br />

56

Mortgage delinquency rate by county in Hawaii:<br />

first mortgages, home equity loans and lines<br />

14<br />

Percent <strong>of</strong> loans, at year end<br />

12<br />

10<br />

8<br />

6<br />

4<br />

2<br />

Recessions shaded<br />

Big Island<br />

Kauai<br />

<strong>Maui</strong><br />

Oahu<br />

0<br />

2000 2002 2004 2006 2008 2010 <strong>2012</strong><br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Federal Reserve Bank <strong>of</strong> New York (http://data.newyorkfed.org/creditconditions/); graphic by TZE<br />

57

Hawaii mortgage delinquency rates<br />

4<br />

Percent <strong>of</strong> mortgages outstanding<br />

3<br />

2<br />

1<br />

U.S. recessions shaded<br />

30-59 days delinquent<br />

90+ days delinquent<br />

90+<br />

30+<br />

“Sub-prime”<br />

financial crisis<br />

notable for sharp<br />

increase in<br />

longer-term<br />

mortgage<br />

delinquency<br />

rates<br />

0<br />

1980 1985 1990 1995 2000 2005 2010<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Regressions and seasonal adjustment by TZE; data from Mortgage Bankers <strong>Association</strong>, TZE<br />

58

Mortgage delinquency near cyclical peak (2010Q3)<br />

≥90 days past due by county (darker is higher)<br />

22.7 Dade, FL<br />

18.3 Broward, FL<br />

15.9 Palm Beach, FL<br />

15.6 Clark, NV<br />

13.6 Riverside, CA<br />

13.2 San Joaquin<br />

12.8 San Bernadino, CA<br />

11.4 Bronx, NY<br />

10.1 Maricopa, AZ<br />

9.4 Sacramento, CA<br />

9.1 Contra Costa, CA<br />

8.8 Los Angeles, CA<br />

8.2 Hawaii, HI<br />

7.6 <strong>Maui</strong>, HI<br />

7.6 San Diego, HI<br />

6.9 Orange, CA<br />

5.9 Santa Clara, CA<br />

5.3 U.S. average<br />

4.5 Kauai, HI<br />

3.7 San Francisco, CA<br />

3.4 Honolulu, HI<br />

1.8 Dane, WI<br />

1.0 Cherry, NE<br />

0.0 Todd, SD<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Federal Reserve Bank <strong>of</strong> New York based on credit-reporting agency TransUnion LLC’s Trend Data database<br />

(http://data.newyorkfed.org/creditconditionsmap/)<br />

59

Foreclosures as a percent <strong>of</strong> housing units by state<br />

0.333<br />

0.328<br />

0.319<br />

0.309<br />

0.308<br />

0.202 0.294<br />

0.193<br />

0.189<br />

0.169<br />

0.149<br />

0.148<br />

0.134<br />

0.133<br />

0.117<br />

0.115<br />

0.115<br />

0.112<br />

0.112<br />

0.110<br />

0.096<br />

0.093<br />

0.091<br />

0.087<br />

0.085<br />

0.00 0.10 0.20 0.30<br />

Georgia<br />

Arizona<br />

Nevada<br />

California<br />

Illinois<br />

Florida<br />

Ohio<br />

Michigan<br />

South Carolina<br />

Utah<br />

Wisconsin<br />

Colorado<br />

Indiana<br />

Delaware<br />

Idaho<br />

Texas<br />

New<br />

Oregon<br />

Kansas<br />

Minnesota<br />

Iowa<br />

Missouri<br />

Tennessee<br />

Louisiana<br />

Massachusetts<br />

Washington<br />

Kentucky<br />

Virginia<br />

New Mexico<br />

Oklahoma<br />

Pennsylvania<br />

Rhode Island<br />

North<br />

Maryland<br />

Connecticut<br />

Alaska<br />

Alabama<br />

Nebraska<br />

New Jersey<br />

Hawaii<br />

New York<br />

Wyoming<br />

Mississippi<br />

South Dakota<br />

Arkansas<br />

Montana<br />

Maine<br />

West Virginia<br />

North Dakota<br />

Vermont<br />

0.085<br />

0.084<br />

0.084<br />

0.083<br />

0.077<br />

0.077<br />

0.076<br />

0.074<br />

0.073<br />

0.072<br />

0.067<br />

0.066<br />

0.054<br />

0.053<br />

0.051<br />

0.043<br />

0.041<br />

0.037<br />

0.035<br />

0.031<br />

0.029<br />

0.015<br />

0.011<br />

0.007<br />

0.007<br />

Sources: Realty Trac (http://www.realtytrac.com/trendcenter/), data for May <strong>2012</strong>; graphic by TZE<br />

0.00 0.10 0.20 0.30<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

60

Using trend data: the inverse relationship between<br />

changes in home prices and delinquency rates<br />

appears cyclically in diagonal, flattened orbits<br />

Percent change in single-family prices<br />

25<br />

20<br />

15<br />

10<br />

5<br />

0<br />

-5<br />

-10<br />

2004<br />

1987<br />

1980s<br />

<strong>2012</strong>Q1<br />

1992<br />

1997<br />

2010<br />

1 2 3 4 5 6 7<br />

Delinquent as percent <strong>of</strong> all loans<br />

Prices rising<br />

Prices falling<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Data sources: Prudential Locations, UHERO, Mortgage Bankers <strong>Association</strong>, Guy Sakamoto (Bank <strong>of</strong> Hawaii); all<br />

calculations by TZE<br />

61

Digging deeper into linkages:<br />

house price movements and delinquency changes<br />

• Rising prices are associated with falling delinquencies (up to lags, etc.)<br />

• In cyclical markets, rising phase <strong>of</strong> house price cycle has similar inverse<br />

relationship with falling phase <strong>of</strong> mortgage delinquency cycle (up to lags)<br />

• Some evidence that price deceleration raises the pace <strong>of</strong> increase in delinquency<br />

(i.e. prices rising at a decreasing rate <strong>of</strong> increase can precede delinquency rise<br />

• Complex nonlinearity actually masks underlying orbit—embedding inverse<br />

relationship—in delinquency-price change space<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

62

Trends, cycles and bubbles<br />

• We’ve got all three—simultaneously<br />

• Arbitrage and factor mobility (capital, labor, technology) implies convergence to<br />

common trend in long-run home price appreciation<br />

• Cycles are not bubbles, and presence <strong>of</strong> the former is neither necessary nor<br />

sufficient for the latter<br />

• Hawaii has had more cyclical housing valuations since early-statehood (1960s)<br />

• Many microeconomic factors distinguish regional performance differences even in<br />

shared macroeconomic environment<br />

• Looking for signs <strong>of</strong> cyclical upswing, indications <strong>of</strong> its imminence<br />

• Remember: Hawaii peak for sales 2005, peak for values 2006—six years ago<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

63

Average Oahu single-family and condominium<br />

existing home sales prices<br />

Thousand dollars, log scale<br />

1000<br />

100<br />

Single-family<br />

Condominium<br />

10<br />

Recessions shaded<br />

1960 1970 1980 1990 2000 2010 2020<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Sources: Honolulu Board <strong>of</strong> Realtors; TZ Economics<br />

64

Remarkably, until the sub-primehousing<br />

bubble,<br />

longer-term trends were roughly equivalent<br />

Indexes, s.a. (1987 = 100), logs<br />

400<br />

200<br />

100<br />

Oahu (median prices)<br />

Las Vegas (Case-Shiller)<br />

Regressions <strong>of</strong> the<br />

natural logarithm <strong>of</strong> the<br />

two price indexes on a<br />

constant and a time<br />

trend, Oahu (1980-<br />

2011) and Las Vegas<br />

(1987-2004)<br />

U.S. recessions shaded<br />

50<br />

80 85 90 95 00 05 10<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Standard & Poor’s, Honolulu Board <strong>of</strong> Realtors, TZE database; seasonal adjustment using Census X-12 ARIMA<br />

filter and regressions by TZE<br />

65

Bubblicious housing markets like Phoenix<br />

will have to re-establish establish long-term trend<br />

No longer log-linear<br />

S&P Case-Shiller home price index<br />

January 2000 = 100.0 (log scale)<br />

200<br />

100<br />

Bubblicious<br />

Overshoot<br />

Oscillation<br />

?<br />

50<br />

U.S. recessions shaded<br />

1995 2000 2005 2010<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Standard & Poor’s (http://www.standardandpoors.com/indices/sp-case-shiller-home-priceindices/en/us/?indexId=spusa-cashpidff--p-us----);<br />

seasonal adjustment by TZE<br />

66

Some longer-term trajectories probably displaced,<br />

but largely unbroken (Hawaii vs. Iowa)<br />

800<br />

Index, 1985Q1 = 100, s.a., log scale<br />

400<br />

200<br />

100<br />

Hawaii<br />

Iowa<br />

Hawaii 1983-2011*<br />

Iowa 1988-2006<br />

Geographic constraints and<br />

regulatory constraints are why<br />

Hawaii has cycles <strong>of</strong> large<br />

amplitude and Iowa doesn’t:<br />

restricting development only<br />

increases the amplitude <strong>of</strong> the<br />

home price valuation cycle<br />

50<br />

75 80 85 90 95 00 05 10 15<br />

*Regressions <strong>of</strong> the natural logarithm <strong>of</strong> individual state FHFA indexes on a time trend<br />

Sources: Federal Housing Finance Agency (http://www.fhfa.gov/Default.aspx?Page=87) from sales prices and<br />

appraisals; seasonal adjustment, index rebasing and regression by TZ Economics<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

67

Long-term median home price movements: despite<br />

idiosyncrasies, arbitrage constrains co-movement<br />

800<br />

U.S. recessions shaded<br />

Thousand dollars, s.a., logs<br />

400<br />

200<br />

100<br />

Japan<br />

Bubble<br />

<strong>Maui</strong><br />

Oahu<br />

Orange County, CA<br />

50<br />

75 80 85 90 95 00 05 10<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, Honolulu Board <strong>of</strong> Realtors, Prudential Locations, National <strong>Association</strong> <strong>of</strong> Realtors,<br />

TZE database; seasonal adjustment using Census X-12 ARIMA filter by TZE<br />

68

Finally: lessons from “higher-order moments”<br />

• The distribution <strong>of</strong> home prices tells a lot more than one might think.<br />

• A normal, “bell-shaped” home price distribution would be symmetric,<br />

characterized sufficiently by its first and second moments, the mean and the<br />

standard deviation—the mean and median would be equal (symmetry).<br />

• Actual home prices have an asymmetric distribution—”tilted”—with most<br />

transactions clustered around the median price (at which half the transactions are<br />

above and below) and a small number <strong>of</strong> high-end transactions in a long “tail.”<br />

• The “width” or dispersion <strong>of</strong> the distribution is characterized by its second<br />

moment, the standard deviation (graphed relative to the mean).<br />

• The “tilt” <strong>of</strong> the distribution is characterized by its third moment, its skewness<br />

• The density in the “tail” <strong>of</strong> the distribution is characterized by the fourth moment,<br />

kurtosis.<br />

• Home prices are typically skewed, with a long tail (so-called “leptokurtosis”)<br />

• Some evidence (e.g. Kauai) that higher-order moments—skewness, kurtosis—<br />

rise in the transition from stable to robust home price upward movement.<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

69

From the Kauai single-family data set:<br />

measures <strong>of</strong> central tendency, including the first moment <strong>of</strong><br />

the distribution <strong>of</strong> existing home sales prices<br />

Recessions shaded<br />

Thousand dollars, log scale<br />

800<br />

400<br />

200<br />

Mean (first moment)<br />

Median<br />

90 95 00 05 10 15<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Hawaii Information Service, West Hawaii and Hawaii Island Boards <strong>of</strong> Realtors; moment metrics calculated by TZE<br />

70

From the West Hawaii (Kona) single-family data set:<br />

measures <strong>of</strong> central tendency, including the first moment <strong>of</strong><br />

the distribution <strong>of</strong> existing home sales prices<br />

Thousand dollars, log scale<br />

800<br />

400<br />

200<br />

Mean (first moment)<br />

Median<br />

Recessions shaded<br />

90 95 00 05 10<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Hawaii Information Service, Kauai Board <strong>of</strong> Realtors; moment metrics calculated by TZE<br />

71

From the <strong>Maui</strong> single-family data set:<br />

measures <strong>of</strong> central tendency, including the first moment <strong>of</strong><br />

the distribution <strong>of</strong> existing home sales prices<br />

Thousand dollars, log scale<br />

800<br />

400<br />

200<br />

Mean (first moment)<br />

Median<br />

Recessions shaded<br />

1990 1995 2000 2005 2010 2015<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, moment metrics calculated by TZE<br />

72

From the West Hawaii (Kona) single-family data set:<br />

higher order moments <strong>of</strong> the distribution <strong>of</strong> prices—standard<br />

standard<br />

deviation (second), skewness (third) and kurtosis (fourth)<br />

16<br />

14<br />

Recessions shaded<br />

S.D./mean (x100) (right)<br />

Skewness (left scale)<br />

Kurtosis (right scale)<br />

350<br />

300<br />

12<br />

250<br />

10<br />

200<br />

8<br />

150<br />

6<br />

100<br />

4<br />

50<br />

2<br />

90 95 00 05 10<br />

0<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Hawaii Information Service, West Hawaii and Hawaii Island Boards <strong>of</strong> Realtors; moment metrics calculated by TZE<br />

73

From the Kauai single-family data set:<br />

higher order moments <strong>of</strong> the distribution <strong>of</strong> prices—standard<br />

standard<br />

deviation (second), skewness (third) and kurtosis (fourth)<br />

16<br />

14<br />

12<br />

S.D./mean (x100) (right scale)<br />

Skewness (left scale)<br />

Kurtosis (right scale)<br />

Recessions shaded<br />

350<br />

300<br />

250<br />

10<br />

8<br />

6<br />

4<br />

200<br />

150<br />

100<br />

50<br />

2<br />

0<br />

90 95 00 05 10 15<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Hawaii Information Service, Kauai Board <strong>of</strong> Realtors; moment metrics calculated by TZE<br />

74

From the <strong>Maui</strong> single-family data set:<br />

higher order moments <strong>of</strong> the distribution <strong>of</strong> prices—standard<br />

standard<br />

deviation (second), skewness (third) and kurtosis (fourth)<br />

14<br />

12<br />

S.D./mean (x100)(right)<br />

Skewness (left scale)<br />

Kurtosis (right scale)<br />

240<br />

200<br />

10<br />

160<br />

8<br />

120<br />

6<br />

80<br />

4<br />

40<br />

2<br />

Recessions shaded<br />

0<br />

1995 2000 2005 2010 2015<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

Source: Realtors <strong>Association</strong> <strong>of</strong> <strong>Maui</strong>, moment metrics calculated by TZE<br />

75

<strong>October</strong> <strong>26</strong>, <strong>2012</strong><br />

• The same cyclical factors interacting with long-term trends, <strong>of</strong>fshore arbitrage,<br />

and onshore macroeconomic fundamentals mattered in 2005 as in <strong>2012</strong><br />

• Different proportions, different mix, does not change the trend-cycle phenomenon<br />

• Hawaii’s home valuation cycle is rooted in microeconomic constraints on supply<br />

• Macroeconomics drives cyclical timing (frequency) and magnitude (amplitude)<br />

• In 2005 Kauai, <strong>Maui</strong> had reached points beyond which excessive bubbliciousness<br />

set the stage for more severe overshooting and oscillation, subsequently<br />

• <strong>Maui</strong> was not Phoenix, but it also was not Oahu—better than one, not the other<br />

• End <strong>of</strong> last housing cycle is reasonably on track to fulfill the expectation that,<br />

broadly-speaking, the 20-teens will exhibit <strong>Maui</strong> house price appreciation<br />

• If your 12-year old child thinks he or she is a teenager, then <strong>October</strong> <strong>26</strong>, <strong>2012</strong><br />

makes perfect sense as to when the next valuation cycle should emerge<br />

• Don’t wait until 2018 to “have that conversation”<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

76

Mahalo!<br />

Aloha!<br />

Paul H. Brewbaker, Ph.D.<br />

Principal, Economist<br />

TZ Economics<br />

606 Ululani St.<br />

Kailua, Hawaii 96734-4430<br />

4430<br />

paulbrewbaker@tzeconomics.com<br />

Slide copyright <strong>2012</strong>, TZ Economics<br />

77