EUROPA - Introduction to the Mechanical and Electrical Engineering ...

EUROPA - Introduction to the Mechanical and Electrical Engineering ...

EUROPA - Introduction to the Mechanical and Electrical Engineering ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Institute for<br />

Economic Research<br />

at <strong>the</strong> University of Munich<br />

Poschingerstraße 5<br />

D-81679 Munich<br />

Telefon ++49-089-92 24 -(0)-1362<br />

Telefax ++49-89-9224-2362<br />

E-mail Vieweg@ifo.de<br />

_____________________________________________________________<br />

Industrial Branch Research<br />

<strong>Introduction</strong> <strong>to</strong> <strong>the</strong> <strong>Mechanical</strong> <strong>and</strong> <strong>Electrical</strong><br />

<strong>Engineering</strong> Sec<strong>to</strong>rs of new<br />

EU Member States<br />

Report <strong>to</strong> <strong>the</strong> project No ENTR/04/063<br />

Contrac<strong>to</strong>r:<br />

ifo Institute for Economic Research, Munich<br />

In co-operation with:<br />

VDMA, Frankfurt<br />

ZVEI, Frankfurt<br />

Munich, November, 2005

Institute for<br />

Economic Research<br />

at <strong>the</strong> University of Munich<br />

Poschingerstraße 5<br />

D-81679 Munich<br />

Telefon ++49-089-92 24 -(0)-1362<br />

Telefax ++49-89-9224-2362<br />

E-mail Vieweg@ifo.de<br />

_____________________________________________________________<br />

Industrial Branch Research<br />

<strong>Introduction</strong> <strong>to</strong> <strong>the</strong> <strong>Mechanical</strong> <strong>and</strong> <strong>Electrical</strong><br />

<strong>Engineering</strong> Sec<strong>to</strong>rs of new<br />

EU Member States<br />

Project Management:<br />

Hans-Gün<strong>the</strong>r Vieweg, Ifo Institute<br />

Ifo Institute, München:<br />

Andreas Kuhlmann<br />

Gabriele Roubal<br />

Frank Fiedler<br />

Hans-Gün<strong>the</strong>r Vieweg<br />

GzF/VDMA, Frankfurt:<br />

Susanne Krebs<br />

Anke Uhlig<br />

ZSG/ZVEI, Frankfurt:<br />

Jürgen Polzin<br />

Ulrich Scheinost<br />

Bernhard Bambullis<br />

Munich, November, 2005

I<br />

Table of Contents<br />

1 Executive Summary................................................................................................... 1<br />

1.1 The European <strong>Engineering</strong> Sec<strong>to</strong>rs .................................................................... 3<br />

1.2 Structural Changes in <strong>the</strong> New Member States.................................................. 4<br />

1.3 Performance in International Trade.................................................................... 5<br />

1.4 Technological Competitiveness.......................................................................... 7<br />

1.5 Price Competititveness ....................................................................................... 7<br />

1.6 Conclusions ........................................................................................................ 8<br />

2 Importance <strong>and</strong> Evolution of <strong>the</strong> <strong>Engineering</strong> Sec<strong>to</strong>rs in <strong>the</strong> New<br />

Member States .......................................................................................................... 11<br />

2.1 <strong>Engineering</strong> Sec<strong>to</strong>rs in all of <strong>the</strong> New Member States Compared <strong>to</strong> EU-15 ... 11<br />

2.2 Investigation in <strong>the</strong> <strong>Engineering</strong> Subsec<strong>to</strong>rs.................................................. 18<br />

2.2.1 Engines <strong>and</strong> Turbines (ex. aircraft, vehicle <strong>and</strong> cycle mach)<br />

CE .11)................................................................................................. 18<br />

2.2.2 Pumps <strong>and</strong> Compressors (NACE 29.12) ........................................... 21<br />

2.2.3 Taps <strong>and</strong> Valves (NACE 29.13) ........................................................ 23<br />

2.2.4 Bearings, Gears, Gearing <strong>and</strong> Driving Elements (NACE 29.14)..... 25<br />

2.2.5 Industrial Furnaces <strong>and</strong> Furnace Burners (NACE 29.21) ................ 26<br />

2.2.6 Lifting <strong>and</strong> H<strong>and</strong>ling Equipment (NACE 29.22).............................. 29<br />

2.2.7 Non-domestic Cooling <strong>and</strong> Ventilation Equipment<br />

NACE 29.23)....................................................................................... 32<br />

2.2.8 O<strong>the</strong>r General Purpose Machinery n.e.c. (NACE 29.24) ................. 33<br />

2.2.9 Agricultural Trac<strong>to</strong>rs (NACE 29.31)................................................. 36<br />

2.2.10 O<strong>the</strong>r Agricultural Machinery (NACE 29.32) .................................. 38<br />

2.2.11 Machine Tools, Woodworking Machinery, Welding Equipment<br />

(NACE 29.40) ..................................................................................... 40<br />

2.2.12 Machinery for Metallurgy (NACE 29.51)......................................... 42<br />

2.2.13 Machinery for Mining <strong>and</strong> Quarrying <strong>and</strong> Construction (NACE<br />

29.52)................................................................................................... 45<br />

2.2.14 Machinery for Food, Beverage <strong>and</strong> Tobacco Processing (NACE<br />

29.53)................................................................................................... 47<br />

2.2.15 Machinery for Textile, Apparel <strong>and</strong> Lea<strong>the</strong>r Production (NACE<br />

29.54)................................................................................................... 48<br />

2.2.16 Machinery for Paper <strong>and</strong> Paperboard Production (NACE 29.55).... 51<br />

2.2.17 O<strong>the</strong>r Special Purpose Machinery n.e.c. (NACE 29.56).................. 53

II<br />

2.2.18 <strong>Electrical</strong> Domestic Appliances (NACE 29.71) ............................... 55<br />

2.2.19 Non-electric Domestic Appliances (NACE 29.72)........................... 57<br />

2.2.20 Electric Mo<strong>to</strong>rs, Genera<strong>to</strong>rs <strong>and</strong> Transformers (NACE 31.10) ....... 59<br />

2.2.21 <strong>Electrical</strong> Distribution <strong>and</strong> Control Apparatus (NACE 31.20) ........ 62<br />

2.2.22 Insulated Wire <strong>and</strong> Cable (NACE 31.30).......................................... 64<br />

2.2.23 Accumula<strong>to</strong>rs, Primary Cells <strong>and</strong> Primary Batteries<br />

(NACE 31.40) ..................................................................................... 66<br />

2.2.24 Lighting Equipment <strong>and</strong> Electric Lamps (NACE 31.50) ................. 68<br />

2.2.25 <strong>Electrical</strong> Equipment for Engines <strong>and</strong> Vehicles (NACE 31.61)...... 70<br />

2.2.26 O<strong>the</strong>r <strong>Electrical</strong> Equipment n.e.c. (NACE 31.62) ............................ 73<br />

2.3 Investigation in <strong>the</strong> <strong>Engineering</strong> Sec<strong>to</strong>rs by Member State ............................. 74<br />

2.3.1 <strong>Engineering</strong> Sec<strong>to</strong>rs in <strong>the</strong> Czech Republic ...................................... 75<br />

2.3.2 <strong>Engineering</strong> Sec<strong>to</strong>rs in Hungary .......................................................... 81<br />

2.3.3 <strong>Engineering</strong> Sec<strong>to</strong>rs in Pol<strong>and</strong>............................................................. 87<br />

2.3.4 <strong>Engineering</strong> Sec<strong>to</strong>rs in Slovakia .......................................................... 90<br />

2.3.5 <strong>Engineering</strong> Sec<strong>to</strong>rs in Slovenia .......................................................... 96<br />

2.3.6 <strong>Engineering</strong> Sec<strong>to</strong>rs in Baltic States .................................................. 100<br />

3 <strong>Engineering</strong> Sec<strong>to</strong>rs in an Enlarged EU .............................................................. 102<br />

3.1 Importance <strong>and</strong> Evolution of <strong>the</strong> <strong>Engineering</strong> Sec<strong>to</strong>rs in EU-25 ................... 102<br />

3.2 Division of Labour ......................................................................................... 103<br />

4 EU <strong>Engineering</strong> Sec<strong>to</strong>rs in Global Competition ................................................. 113<br />

4.1 Trade Performance of <strong>the</strong> <strong>Engineering</strong> industries in <strong>the</strong> Triad ...................... 113<br />

4.2 Challenge from Emerging Countries.............................................................. 115<br />

4.3 Price Competitiveness of <strong>Engineering</strong> Industries........................................... 118<br />

4.4 Assessment of <strong>the</strong> Technological Competitiveness ....................................... 122<br />

5 Conclusions............................................................................................................. 126<br />

5.1 Final assessment of <strong>the</strong> competitiveness ........................................................ 126<br />

5.2 Proposal for a Future in -Depth Analysis of <strong>the</strong> Competitive Assets <strong>and</strong><br />

Liabilities of <strong>the</strong> <strong>Engineering</strong> Industries in <strong>the</strong> New Member States............... 127<br />

6 Information Provider ............................................................................................ 131<br />

Annexes

III<br />

List of Tables<br />

Table 2.1: Key data for <strong>the</strong> New Member States’ <strong>Engineering</strong> Sec<strong>to</strong>rs 2004 .....12<br />

Table 2.2: Key data for <strong>the</strong> EU-15 <strong>Engineering</strong> Sec<strong>to</strong>rs 2004 ............................13<br />

Table 2.3: Evolution of New Member States’ <strong>Engineering</strong> Sec<strong>to</strong>rs 1995-2004..15<br />

Table2.4: Evolution of EU-15 <strong>Engineering</strong> Sec<strong>to</strong>rs 1995 - 2004.......................15<br />

Table 2.5: Key data for NACE 29.11 in 2004 ....................................................20<br />

Table 2.6: Key data for NACE 29.12 in 2004 ....................................................22<br />

Table 2.7: Key data for NACE 29.13 in 2004 ....................................................24<br />

Table 2.8: Key data for NACE 29.14 in 2004 ....................................................26<br />

Table 2.9: Key data for NACE 29.21 in 2004 ....................................................28<br />

Table 2.10: Key data for NACE 29.22 in 2004 ....................................................31<br />

Table 2.11: Key data for NACE 29.23 in 2004 ....................................................33<br />

Table 2.12: Key data for NACE 29.24 in 2004 ....................................................35<br />

Table 2.13: Key data for NACE 29.31 in 2004 ....................................................37<br />

Table 2.14: Key data for NACE 29.32 in 2004 ....................................................39<br />

Table 2.15: Key data for NACE 29.40 in 2004 ....................................................42<br />

Table 2.16: Key data for NACE 29.51 in 2004 ....................................................44<br />

Table 2.17: Key data for NACE 29.52 in 2004 ....................................................46<br />

Table 2.18: Key data for NACE 29.53 in 2004 ....................................................48<br />

Table 2.19: Key data for NACE 29.54 in 2004 ....................................................50<br />

Table 2.20: Key data for NACE 29.55 in 2004 ....................................................53<br />

Table 2.21: Key data for NACE 29.56 in 2004 ....................................................55<br />

Table 2.22: Key data for NACE 29.71 in 2004 ....................................................57<br />

Table 2.23: Key data for NACE 29.72 in 2004 ....................................................59<br />

Table 2.24: Key data for NACE 31.10 in 2004 ....................................................61<br />

Table 2.25: Key data for NACE 31.20 in 2004 ....................................................63<br />

Table 2.26: Key data for NACE 31.30 in 2004 ....................................................65<br />

Table 2.27: Key data for NACE 31.40 in 2004 ....................................................68<br />

Table 2.28: Key data for NACE 31.50 in 2004 ....................................................70<br />

Table 2.29: Key data for NACE 31.61 in 2004 ....................................................72<br />

Table 2.30: Key data for NACE 31.62 in 2004 ....................................................74

IV<br />

Table 2.31: Key data for <strong>the</strong> Czech <strong>Engineering</strong> Sec<strong>to</strong>rs 2004 ............................76<br />

Table 2.32: Key data for <strong>the</strong> Hungarian <strong>Engineering</strong> Sec<strong>to</strong>rs 2004......................81<br />

Table 2.33: Key data for <strong>the</strong> Polish <strong>Engineering</strong> Sec<strong>to</strong>rs 2004 ............................88<br />

Table 2.34: Key data for <strong>the</strong> Slovakian <strong>Engineering</strong> Sec<strong>to</strong>rs 2004.......................90<br />

Table 2.35: Key data for <strong>the</strong> Slovenian <strong>Engineering</strong> Sec<strong>to</strong>rs 2004.......................96<br />

Table 2.36: Key data for <strong>the</strong> Baltic <strong>Engineering</strong> Sec<strong>to</strong>rs 2004........................... 101<br />

Table 3.1: Key data for <strong>the</strong> EU-25 <strong>Engineering</strong> Sec<strong>to</strong>rs 2004 .......................... 102<br />

Table 3.2: Evolution of EU-25 <strong>Engineering</strong> Sec<strong>to</strong>rs 1995 - 2004..................... 103<br />

Table 3.3: Production of <strong>the</strong> new <strong>and</strong> old Member States’ engineering<br />

industries – Comparison of <strong>the</strong> structure ......................................... 106<br />

Table 4.1: The Triad Exports in <strong>Engineering</strong> Industries ................................... 113<br />

Table 4.2: EU Trade with China in <strong>Engineering</strong> Industries.............................. 117<br />

Table 4.3: Changes in <strong>the</strong> Price Competitiveness between 1996 <strong>and</strong> 2004 ...... 120<br />

Table 4.4: Changes in <strong>the</strong> Price Competitiveness between 2000 <strong>and</strong> 2004 ...... 121<br />

Table 4.5: International Comparison Innovation Intensity in Total<br />

<strong>Engineering</strong> Industries..................................................................... 123<br />

Table 4.6: Share of <strong>Engineering</strong> Industries in Patent Applications in<br />

all areas of Technology, 1995 - 2002............................................... 124

V<br />

List of figures<br />

Figure 2.1: <strong>Engineering</strong> Industries in EU-15 <strong>and</strong> <strong>the</strong> new Member States.. 17<br />

Figure 2.2: Comparison of NACE 29.11 <strong>to</strong> <strong>to</strong>tal engineering..................... 20<br />

Figure 2.4: Comparison of NACE 29.12 <strong>to</strong> <strong>to</strong>tal engineering..................... 23<br />

Figure 2.5: Comparison of NACE 29.13 <strong>to</strong> <strong>to</strong>tal engineering..................... 24<br />

Figure 2.6: Comparison of NACE 29.14 <strong>to</strong> <strong>to</strong>tal engineering..................... 26<br />

Figure 2.7: Comparison of NACE 29.21 <strong>to</strong> <strong>to</strong>tal engineering..................... 29<br />

Figure 2.8: Comparison of NACE 29.22 <strong>to</strong> <strong>to</strong>tal engineering..................... 31<br />

Figure 2.9: Comparison of NACE 29.23 <strong>to</strong> <strong>to</strong>tal engineering..................... 33<br />

Figure 2.10: Comparison of NACE 29.24 <strong>to</strong> <strong>to</strong>tal engineering..................... 35<br />

Figure 2.11: Comparison of NACE 29.31 <strong>to</strong> <strong>to</strong>tal engineering..................... 37<br />

Figure 2.12: Comparison of NACE 29.32 <strong>to</strong> <strong>to</strong>tal engineering..................... 39<br />

Figure 2.13: Comparison of NACE 29.40 <strong>to</strong> <strong>to</strong>tal engineering..................... 42<br />

Figure 2.14: Comparison of NACE 29.51 <strong>to</strong> <strong>to</strong>tal engineering..................... 44<br />

Figure 2.15: Comparison of NACE 29.52 <strong>to</strong> <strong>to</strong>tal engineering..................... 46<br />

Figure 2.16: Comparison of NACE 29.53 <strong>to</strong> <strong>to</strong>tal engineering..................... 48<br />

Figure 2.17: Comparison of NACE 29.54 <strong>to</strong> <strong>to</strong>tal engineering..................... 51<br />

Figure 2.18: Comparison of NACE 29.55 <strong>to</strong> <strong>to</strong>tal engineering..................... 53<br />

Figure 2.19: Comparison of NACE 29.56 <strong>to</strong> <strong>to</strong>tal engineering..................... 55<br />

Figure 2.20: Comparison of NACE 29.71 <strong>to</strong> <strong>to</strong>tal engineering..................... 57<br />

Figure 2.21: Comparison of NACE 29.72 <strong>to</strong> <strong>to</strong>tal engineering..................... 59<br />

Figure 2.22: Comparison of NACE 31.10 <strong>to</strong> <strong>to</strong>tal engineering..................... 61<br />

Figure 2.23: Comparison of NACE 31.20 <strong>to</strong> <strong>to</strong>tal engineering..................... 63<br />

Figure 2.24: Comparison of NACE 31.30 <strong>to</strong> <strong>to</strong>tal engineering..................... 66<br />

Figure 2.25: Comparison of NACE 31.40 <strong>to</strong> <strong>to</strong>tal engineering..................... 68<br />

Figure 2.26: Comparison of NACE 31.50 <strong>to</strong> <strong>to</strong>tal engineering..................... 70<br />

Figure 2.27: Comparison of NACE 31.61 <strong>to</strong> <strong>to</strong>tal engineering..................... 72<br />

Figure 2.28: Comparison of NACE 31.62 <strong>to</strong> <strong>to</strong>tal engineering..................... 74

VI<br />

Figure 3.1:<br />

Figure 3.2:<br />

The evolution of intrasec<strong>to</strong>ral trade between <strong>the</strong> new<br />

<strong>and</strong> <strong>the</strong> old Member States ..................................................... 108<br />

Similarity of EU-15 <strong>and</strong> new Member States’ exports <strong>to</strong><br />

third countries ........................................................................ 109<br />

Figure 4.1: Share of new Member States on EU-25 Exports .................... 115<br />

Figure 4.2: Comparison of Innovation Intensities of EU-15 <strong>and</strong><br />

new Member States by subsec<strong>to</strong>rs of <strong>the</strong> <strong>Engineering</strong><br />

Industries................................................................................ 125

VII<br />

Preliminary Remark<br />

The study report comprises <strong>the</strong> results of a project carried out for <strong>the</strong> Direc<strong>to</strong>rate-<br />

General “Enterprise <strong>and</strong> Industry” under <strong>the</strong> Tender No ENTR/04/0463.<br />

It consists of <strong>the</strong> analytical part on <strong>the</strong> initial assessment of <strong>the</strong> engineering industries<br />

competitiveness of <strong>the</strong> new Member States. It is followed by a Methodological Annex<br />

<strong>and</strong> an annex which contains <strong>the</strong> data base created in course of <strong>the</strong> project.<br />

The slides for <strong>the</strong> presentation <strong>and</strong> <strong>the</strong> CD are enclosed in <strong>the</strong> delivery.<br />

Munich, 15 November 2005<br />

Hans-Gün<strong>the</strong>r Vieweg

1<br />

1 Executive Summary<br />

The study report comprises <strong>the</strong> results of a project carried out for <strong>the</strong> Direc<strong>to</strong>rate-<br />

General “Enterprise <strong>and</strong> Industry”. The object of <strong>the</strong> investigation was <strong>the</strong> engineering<br />

sec<strong>to</strong>rs of <strong>the</strong> new EU-Member States. Two <strong>to</strong>pics were <strong>to</strong> belaboured, <strong>the</strong> creation of a<br />

data base <strong>and</strong> an assessment of <strong>the</strong> sec<strong>to</strong>rs competitiveness. The latter <strong>to</strong>pic was divided<br />

in<strong>to</strong> three steps, an analysis of <strong>the</strong> engineering sec<strong>to</strong>rs during <strong>the</strong> period under investigation,<br />

<strong>the</strong>ir integration in<strong>to</strong> <strong>the</strong> European market, in particular <strong>the</strong> division of labour between<br />

<strong>the</strong> old <strong>and</strong> <strong>the</strong> new Member States, <strong>and</strong> <strong>the</strong> potential for an improved global<br />

competitiveness of <strong>the</strong> European engineering industries stimulated by <strong>the</strong> enlarged EU.<br />

As a conclusion of <strong>the</strong> experiences in <strong>the</strong> assessment of <strong>the</strong> competitiveness a proposal<br />

is submitted which stresses <strong>the</strong> design for a more detailed <strong>and</strong> better founded in-depth<br />

investigation.<br />

The Ifo Institute was responsible for <strong>the</strong> execution of <strong>the</strong> overall project <strong>and</strong> contributed<br />

<strong>the</strong> analysis of <strong>the</strong> competitiveness. The German associations of <strong>the</strong> engineering sec<strong>to</strong>rs<br />

joined <strong>the</strong> project, <strong>the</strong> GzF/VDMA for mechanical engineering <strong>and</strong> <strong>the</strong> ZSG/ZVEI for<br />

<strong>the</strong> electrical engineering <strong>and</strong> domestic appliances. Both of <strong>the</strong>se organizations have a<br />

longst<strong>and</strong>ing experience in <strong>the</strong> creation of European data bases for <strong>the</strong>ir respective sec<strong>to</strong>rs.<br />

The study report is composed of an analytical part. There are two supplements, a Methodological<br />

Annex which provides information on <strong>the</strong> most important indica<strong>to</strong>rs applied<br />

in <strong>the</strong> report <strong>and</strong> a Statistical Annex which provides <strong>the</strong> data base for <strong>the</strong> engineering<br />

sec<strong>to</strong>rs of <strong>the</strong> new Member States.<br />

The analytical part of <strong>the</strong> study is structured as follows.<br />

♦ Chapter 2.1 gives an overview on <strong>to</strong>tal engineering for all of <strong>the</strong> acceded countries.<br />

<strong>Engineering</strong> is compared <strong>to</strong> <strong>the</strong> EU-15 by its size <strong>and</strong> its development. Special attention<br />

is paid <strong>to</strong> <strong>the</strong> pattern of <strong>the</strong> evolution during <strong>the</strong> phase of transition in particular<br />

tendencies in employment, growth <strong>and</strong> productivity are shown.<br />

♦ Chapter 2.2 provides a more detailed investigation of <strong>the</strong> engineering sec<strong>to</strong>rs. For<br />

each of <strong>the</strong> subsec<strong>to</strong>rs under consideration <strong>the</strong> product range is described <strong>and</strong> driving<br />

fac<strong>to</strong>rs for <strong>the</strong> development are mentioned. The statistical analysis compares it <strong>to</strong> <strong>the</strong><br />

superior sec<strong>to</strong>r, mechanical or electrical engineering. The subsec<strong>to</strong>r’s importance <strong>and</strong><br />

evolution over time is mirrored against all of <strong>the</strong> new Member States <strong>and</strong> EU-15. Not

2<br />

only economic efficiency data are analysed, but also <strong>the</strong> pace of <strong>the</strong> technological<br />

progress as measured by an innovation intensity indica<strong>to</strong>r.<br />

♦ Chapter 2.3 provides an investigation of <strong>the</strong> engineering sec<strong>to</strong>rs by Member State.<br />

The five bigger new Member States are analysed in detail, whereas <strong>the</strong> three Baltic<br />

States are put <strong>to</strong>ge<strong>the</strong>r because of <strong>the</strong>ir small size. The presentation of <strong>the</strong> countries<br />

starts with a statistical overview which provides information on <strong>the</strong> importance of <strong>the</strong><br />

engineering sec<strong>to</strong>rs within <strong>the</strong> country as a share of <strong>to</strong>tal manufacturing <strong>and</strong> within<br />

<strong>the</strong> new Member States as a share of <strong>the</strong> region’s engineering sec<strong>to</strong>r. The development<br />

over time <strong>and</strong> <strong>the</strong> efficiency indica<strong>to</strong>rs are confronted with <strong>the</strong> region’s average.<br />

The innovation activity of each of <strong>the</strong> new Member States has been checked <strong>and</strong><br />

compared <strong>to</strong> <strong>the</strong> average of all of <strong>the</strong> countries under investigation. Each of <strong>the</strong> country<br />

reports is followed by a more qualitative illustration of each of <strong>the</strong> sec<strong>to</strong>rs, mechanical<br />

engineering, domestic appliances <strong>and</strong> electrical engineering. The portrayal<br />

is derived from desk<strong>to</strong>p research as well as interviews carried out with experts of <strong>the</strong><br />

engineering sec<strong>to</strong>rs <strong>and</strong> <strong>the</strong> public administration.<br />

♦ Chapter 3 provides an overview on <strong>the</strong> engineering industries of <strong>the</strong> EU-25 <strong>and</strong> compares<br />

it <strong>to</strong> <strong>the</strong> o<strong>the</strong>r Triad members. Moreover it analyses <strong>the</strong> integration of <strong>the</strong> old<br />

<strong>and</strong> new Member States. Different patterns of <strong>the</strong> development of mechanical <strong>and</strong><br />

electrical engineering were identified, which can be explained by <strong>the</strong> different kind<br />

of products, a different division of labour along <strong>the</strong> value-added chain <strong>and</strong> a different<br />

strategic orientation of <strong>the</strong> players in <strong>the</strong> markets.<br />

♦ Chapter 4 is dedicated <strong>to</strong> <strong>the</strong> assessment of <strong>the</strong> competitiveness of <strong>the</strong> EU engineering<br />

industries. The focus – as stressed in <strong>the</strong> Call for Tender – is on <strong>the</strong> new Member<br />

States. It was shown that <strong>the</strong>ir evolution is more <strong>and</strong> more affiliated with <strong>the</strong> engineering<br />

industries of <strong>the</strong> “old” Member States. This is why this chapter takes in<strong>to</strong> account<br />

<strong>the</strong> new Member States as well as <strong>the</strong> development of <strong>the</strong> EU-15. As benchmark<br />

for <strong>the</strong> assessment of <strong>the</strong> performance in a globalized world Japan <strong>and</strong> <strong>the</strong> USA<br />

are used. Since <strong>the</strong> early 1990s an emerging competition from newly industrializing<br />

Asian countries is a feature in <strong>the</strong> markets for engineering products. As supplementary<br />

information on this issue an analysis of <strong>the</strong> trade between <strong>the</strong> new Member<br />

States, <strong>the</strong> EU-15 <strong>and</strong> China has been executed.<br />

♦ Chapter 5 concludes <strong>the</strong> assessment of <strong>the</strong> new Member States’ engineering sec<strong>to</strong>rs<br />

competitiveness <strong>and</strong> suggests a procedure for a more detailed investigation of <strong>the</strong><br />

competitiveness.

3<br />

1.1 The European <strong>Engineering</strong> Sec<strong>to</strong>rs<br />

The output of <strong>the</strong> new Member States’ engineering sec<strong>to</strong>rs reached a value of <strong>to</strong>tal production<br />

of €35.7 bn 2004. This corresponds <strong>to</strong> a value added of €11.0 bn. These are<br />

small values as compared <strong>to</strong> <strong>the</strong> EU-15 with an engineering production amounting <strong>to</strong><br />

€588 bn, but with regard <strong>to</strong> <strong>the</strong> size of <strong>the</strong> economies of <strong>the</strong> acceded countries <strong>the</strong>ir engineering<br />

sec<strong>to</strong>rs comm<strong>and</strong> a somewhat bigger share of all of <strong>the</strong> manufacturing industries<br />

value added which comes up <strong>to</strong> 14.4%, <strong>the</strong> respective figure for <strong>the</strong> EU-15 is<br />

13.3%.<br />

The engineering sec<strong>to</strong>rs output shows structural differences between both of <strong>the</strong> regions<br />

of <strong>the</strong> Single Market. <strong>Mechanical</strong> engineering only accounts for 40% of <strong>the</strong> output of<br />

<strong>the</strong> new Member States, electrical engineering reaches more than 50% <strong>and</strong> scarcely<br />

10% are provided by domestic appliances. In contrast mechanical engineering is in <strong>the</strong><br />

lead in <strong>the</strong> EU-15 with a share of nearly two thirds; electrical engineering comes up <strong>to</strong><br />

only 30% <strong>and</strong> domestic appliances contribution <strong>to</strong> <strong>the</strong> output of <strong>the</strong> engineering sec<strong>to</strong>rs<br />

is a reminder.<br />

The evolution of <strong>the</strong> engineering industries has been analysed for <strong>the</strong> years 1995 <strong>to</strong><br />

2004. This period of <strong>the</strong> transition phase has been characterized by <strong>the</strong> fact that for most<br />

of <strong>the</strong> countries under consideration <strong>the</strong> initial dis<strong>to</strong>rtions after <strong>the</strong> breakdown of <strong>the</strong><br />

socialistic planned economy have been fading away <strong>and</strong> <strong>the</strong> economic development has<br />

ga<strong>the</strong>red momentum. For <strong>the</strong> whole period under review <strong>the</strong> annual average growth rate<br />

- calculated in real terms – was 10.5%. The most dynamic development experienced<br />

electrical engineering with a rate of 15.7%, whereas mechanical engineering experienced<br />

only a moderate 6.0%. Domestic appliances grew on average of <strong>the</strong> sec<strong>to</strong>rs.<br />

The high growth momentum was made possible by remarkable gains in efficiency for<br />

<strong>the</strong> labour input. The investment in advanced production technology <strong>and</strong> management<br />

techniques induced an improvement of labour productivity at <strong>the</strong> same pace as production<br />

grew, but <strong>the</strong> engineering sec<strong>to</strong>rs value added grew somewhat slower. As a result of<br />

this development employment fell by an annual rate of 1.3%. Within <strong>the</strong> sec<strong>to</strong>rs <strong>the</strong><br />

development was quite different. A slump in <strong>the</strong> number of workplaces was reported for<br />

mechanical engineering <strong>and</strong> for domestic appliances. Simultaneously <strong>the</strong> EU-15 discloses<br />

a moderate production growth of 2.1% for all engineering sec<strong>to</strong>rs, small gains in<br />

labour productivity <strong>and</strong> a similar employment record. The number of workplaces fell by<br />

an average rate of 1.0%.

4<br />

1.2 Structural Changes in <strong>the</strong> New Member States<br />

The development in <strong>the</strong> new Member States was strongly affected by privatization <strong>and</strong><br />

<strong>the</strong> entry of foreign inves<strong>to</strong>rs. In domestic appliances <strong>and</strong> in electrical engineering <strong>the</strong><br />

big players in <strong>the</strong> global market from Europe <strong>and</strong> overseas have become important<br />

stakeholders. In mechanical engineering <strong>the</strong> situation is somewhat different. Above all<br />

European companies have acquired shares <strong>and</strong> beside big companies medium-sized<br />

firms have heavily invested.<br />

The predominant motive for investment in <strong>the</strong> new Member States’ mechanical engineering<br />

has been <strong>the</strong> acquisition of capacities for <strong>the</strong> manufacture of intermediary products.<br />

Typically <strong>the</strong>se new production sites have been integrated in <strong>the</strong> companies’ valueadded<br />

chain. As a consequence <strong>the</strong> intra-sec<strong>to</strong>ral trade between old <strong>and</strong> new Member<br />

States has intensified. A new wider competitive cluster has evolved which exploits <strong>the</strong><br />

comparative advantages as available in <strong>the</strong> old <strong>and</strong> new Member States. A similar pattern<br />

in <strong>the</strong> division of labour has not been traceable, nei<strong>the</strong>r for electrical engineering<br />

nor for domestic appliances. For both of <strong>the</strong>se sec<strong>to</strong>rs this motive was <strong>to</strong> a lesser extent<br />

of importance for companies’ investment activities. The acquisition of plants was <strong>to</strong> a<br />

large extent dedicated for <strong>the</strong> production of final goods <strong>and</strong> intermediary products,<br />

which are dedicated for o<strong>the</strong>r industries. This is in particular for electrical engineering<br />

relevant which delivers a noteworthy share of its products <strong>to</strong> manufacturers of vehicles.<br />

The concerned subsec<strong>to</strong>r of electrical engineering enjoyed <strong>the</strong> highest growth momentum<br />

during <strong>the</strong> period under investigation.<br />

The privatization of <strong>the</strong> engineering sec<strong>to</strong>rs was accompanied by a structural change.<br />

The former big conglomerates have been dismantled. Most of <strong>the</strong> newly created companies<br />

got rid of <strong>the</strong>ir distribution channels which in <strong>the</strong> socialistic era were centrally organized.<br />

In most cases <strong>the</strong>re was no direct access <strong>to</strong> Western markets. Bigger independent<br />

engineering groups of <strong>the</strong> new Member States were able <strong>to</strong> maintain <strong>and</strong> streng<strong>the</strong>n<br />

distribution channels. For <strong>the</strong> smaller firms this was <strong>the</strong> exception. This has raised major<br />

problems above all for <strong>the</strong> manufacturers of final goods. The manufacturers of intermediary<br />

goods are better off if <strong>the</strong>y succeed <strong>to</strong> get access <strong>to</strong> big clients.<br />

In mechanical engineering <strong>the</strong>se problems have induced a remarkable structural change.<br />

The production of mobile machinery, trac<strong>to</strong>rs, construction machines etc., a former<br />

strength of <strong>the</strong> region suffered remarkable losses in <strong>the</strong> output of mechanical engineering.<br />

This decline happened while simultaneously manufacturers of <strong>the</strong> EU-15 gained<br />

market shares in central <strong>and</strong> Eastern Europe. Several fac<strong>to</strong>rs <strong>to</strong>ge<strong>the</strong>r explain <strong>the</strong> devel-

5<br />

opment: superior Western products <strong>and</strong> production technology were decisive, but also<br />

<strong>the</strong> experience in marketing <strong>and</strong> heavy investment in distribution channels contributed<br />

<strong>to</strong> <strong>the</strong> success of <strong>the</strong> big European players. The manufacturers of mobile machinery increased<br />

<strong>the</strong>ir contribution <strong>to</strong> <strong>the</strong> EU-15 mechanical engineering.<br />

There is a noteworthy number of small companies which is in a stalemate position in <strong>the</strong><br />

new Member States. Many are final goods manufacturers which have lost much of <strong>the</strong>ir<br />

client basis. Poor dem<strong>and</strong> for <strong>the</strong>ir final goods makes <strong>the</strong>m more <strong>and</strong> more dependent<br />

on spare parts business for old machinery yet in use. If <strong>the</strong>y succeed <strong>to</strong> attract foreign<br />

companies <strong>the</strong>ir final products are sold via <strong>the</strong> distribution channels of <strong>the</strong> partner.<br />

However a sustainable success as an au<strong>to</strong>nomous company is dependent on <strong>the</strong> availability<br />

of own product or manufacturing know-how. O<strong>the</strong>r small companies are subcontrac<strong>to</strong>rs<br />

<strong>to</strong> big clients. Numerous firms run short of resources <strong>and</strong> do not have sufficient<br />

means for investment in <strong>the</strong> equipment necessary <strong>to</strong> fulfil <strong>the</strong> ever growing requirements<br />

of <strong>the</strong> big clients.<br />

Many of <strong>the</strong> bigger companies held by domestic entrepreneurs or financial inves<strong>to</strong>rs are<br />

better off. They own manufacturing know-how <strong>and</strong> supply complex intermediary goods.<br />

They can trust in <strong>the</strong> advantages of <strong>the</strong>ir location for production <strong>and</strong> have a certain bargaining<br />

power with big clients. They will gain importance in <strong>the</strong> ongoing structural<br />

change <strong>and</strong> are perceived as <strong>the</strong> stronghold of <strong>the</strong> engineering sec<strong>to</strong>rs in <strong>the</strong> new Member<br />

States.<br />

A noteworthy change in <strong>the</strong> product programme of <strong>the</strong> new Member States’ mechanical<br />

engineering has taken place in <strong>the</strong> last decade. It has become more different from <strong>the</strong><br />

structure of <strong>the</strong> old Member States. This development is interpreted as a shift <strong>to</strong>wards a<br />

division of labour in line with <strong>the</strong> respective comparative advantages. This evolution is<br />

mirrored in trade of <strong>the</strong> new <strong>and</strong> old Member States with non EU-countries. The structure<br />

of exports has become more dissimilar during <strong>the</strong> period under investigation. In<br />

contrast <strong>the</strong> exports of electrical engineering <strong>and</strong> domestic appliances do not disclose a<br />

similar development <strong>to</strong>wards a specialisation between <strong>the</strong> old <strong>and</strong> new Member States.<br />

1.3 Performance in International Trade<br />

The engineering market is characterized by global competition. Most important suppliers<br />

are up <strong>to</strong> now from mature industrialized countries. As compared <strong>to</strong> Japan <strong>and</strong> <strong>the</strong><br />

USA <strong>the</strong> European engineering industries performed well during <strong>the</strong> period under inves-

6<br />

tigation between 1995 <strong>and</strong> 2004 The EU-15 exports grew at an average annual rate of<br />

6.3% much stronger than both of <strong>the</strong> o<strong>the</strong>r major manufacturing nations. Simultaneously<br />

<strong>the</strong> new Member States extra EU-exports soared at a high double digit rate of<br />

12.7%. As a result <strong>the</strong> EU-25 increased its share in <strong>the</strong> Triad exports by nearly 1-<br />

percantage point up <strong>to</strong> 41.1% on average of <strong>the</strong> years 2002 <strong>to</strong> 2004 compared <strong>to</strong> 1995 <strong>to</strong><br />

1997.<br />

Global competition in engineering markets has changed since <strong>the</strong> early 1990s. New<br />

competi<strong>to</strong>rs have tapped in<strong>to</strong> <strong>the</strong> market among <strong>the</strong>m Chinese manufacturers. In interviews<br />

fears were raised that <strong>the</strong>re is a Chinese threat. This is why trade with China in<br />

engineering products has been taken in<strong>to</strong> account. It has intensified markedly since<br />

1995. In contrast <strong>to</strong> <strong>the</strong> EU-15 <strong>the</strong> new Member States trade with China reveals a trade<br />

deficit. In absolute figures it is not high, but in relation <strong>to</strong> <strong>the</strong> trade volume <strong>the</strong> imports<br />

exceed <strong>the</strong> exports by a fac<strong>to</strong>r of three. Up <strong>to</strong> now Chinese deliveries <strong>to</strong> <strong>the</strong> new Member<br />

States are on a low level as compared with <strong>the</strong> EU-15 deliveries, but <strong>the</strong> growth<br />

rates are much higher. This development is primarily driven by <strong>the</strong> integration of <strong>the</strong><br />

new Member States in <strong>the</strong> international division of labour. This will – as far as intermediary<br />

products are concerned – increase <strong>the</strong> competitiveness of <strong>the</strong> European engineering<br />

industries, but it simultaneously results in a loss of workplaces no longer competitive<br />

in <strong>the</strong> region. The equilibrium will be dependent on <strong>the</strong> advantages of <strong>the</strong> respective<br />

countries as locations for production.<br />

The comparison of Chinese <strong>and</strong> <strong>the</strong> New Member States’ deliveries <strong>to</strong> <strong>the</strong> EU-15 shows<br />

that <strong>the</strong>re is a certain competitive pressure in <strong>the</strong>ir most important sales market. The<br />

acceded states import penetration is 2.3 times as high as for China. Growth momentum<br />

for <strong>the</strong> more recent years is on a comparable level for both regions of origin. The overall<br />

growth rates do not unveil any immanent threat. But for <strong>the</strong> period 1995 <strong>to</strong> 2003 Chinese<br />

exports grew much stronger. This is above all of note for domestic appliances a<br />

market which is dominated by global players which heavily invested in China <strong>and</strong> <strong>the</strong><br />

new Member States. In this sec<strong>to</strong>r <strong>the</strong> Chinese import penetration in <strong>the</strong> EU-15 is higher<br />

than <strong>the</strong> penetration of <strong>the</strong> new Member States’. This sec<strong>to</strong>r is more exposed <strong>to</strong> a direct<br />

competition from China than mechanical <strong>and</strong> electrical engineering.<br />

The analysis of <strong>the</strong> new Member States’ competitiveness has revealed that <strong>the</strong>re is competence<br />

for engineering products <strong>and</strong> <strong>the</strong>y provide advantageous conditions as a location<br />

for production. However up <strong>to</strong> now much of <strong>the</strong> activities are related <strong>to</strong> <strong>the</strong> manufacture<br />

of low-<strong>and</strong> medium-tech products <strong>and</strong> processes which have come under com-

7<br />

petitive pressure in recent years. The threat of relocation <strong>to</strong> production sites outside <strong>the</strong><br />

Single Market requires an upgrading of <strong>the</strong> technology basis.<br />

1.4 Technological Competitiveness<br />

The pace of technological progress was analyzed by an investigation of inventions of<br />

international importance applied for a patent. The basis for <strong>the</strong> statistical work is <strong>the</strong> Ifo<br />

Patent Statistics which uses <strong>the</strong> information of epidos/INPADOC. The number of patent<br />

application is divided by <strong>the</strong> output of <strong>the</strong> sec<strong>to</strong>r <strong>and</strong> describes <strong>the</strong> innovation intensity,<br />

an indica<strong>to</strong>r which gives an impression of a country’s efforts in <strong>the</strong> global technological<br />

competition independently from its size. This indica<strong>to</strong>r discloses that <strong>the</strong> new Member<br />

States innovation intensity is on a low level as compared <strong>to</strong> <strong>the</strong> leading supplying nations<br />

of engineering products. This result cannot be blamed on a specific weakness in<br />

technologies related <strong>to</strong> engineering industries. It is explained by <strong>the</strong> overall efforts in all<br />

areas of technology. This means that on average all R&D efforts are lower than in mature<br />

industrialized countries.<br />

A higher innovation intensity than on average for <strong>the</strong> engineering industries in <strong>the</strong> new<br />

Member States was identified for mechanical engineering. Within this sec<strong>to</strong>r innovation<br />

activities in textile <strong>and</strong> clothing machinery as well as industrial burners are on a remarkable<br />

high level. In electrical engineering <strong>and</strong> in domestic appliances innovation activities<br />

are extremely low. To a certain extent this can be explained by <strong>the</strong> product programme<br />

which comprises in some subsec<strong>to</strong>rs above all serial products which are manufactured<br />

in big batches. Moreover much of <strong>the</strong> R&D is carried out by <strong>the</strong> big companies<br />

of both sec<strong>to</strong>rs outside <strong>the</strong> new Member States. There are only few exceptions, as for<br />

instance in Slovenia.<br />

1.5 Price Competitiveness<br />

The analysis of price competitiveness has been based on labour, <strong>the</strong> most challenged<br />

input fac<strong>to</strong>r in <strong>the</strong> era of globalization. The analysis covers <strong>the</strong> years 1995 - 2004. For<br />

<strong>the</strong> whole period <strong>the</strong> new Member States outperformed <strong>the</strong> EU-15 <strong>and</strong> <strong>the</strong> USA by far.<br />

The driver for this development was labour productivity caused by an introduction of<br />

new production technologies <strong>and</strong> management techniques. Much of <strong>the</strong>se efficiency<br />

gains were absorbed by growing wages. However unit-labour costs sunk at an average<br />

yearly rate of 1.49%, much stronger than in <strong>the</strong> o<strong>the</strong>r considered regions. Moreover <strong>the</strong>

8<br />

currencies of <strong>the</strong> new Member States depreciated at an average rate of 1.95% per year.<br />

Both effects <strong>to</strong>ge<strong>the</strong>r streng<strong>the</strong>ned <strong>the</strong> price competitiveness of <strong>the</strong> engineering industries<br />

at a yearly rate of 2.21% as compared <strong>to</strong> EU-15 for <strong>the</strong> <strong>to</strong>tal period from 1995 <strong>to</strong><br />

2004.<br />

The price competitiveness in <strong>the</strong> new Member States developed quite different over <strong>the</strong><br />

period under review. During <strong>the</strong> early stage of <strong>the</strong> transition a high double digit growth<br />

rate of labour productivity more than compensated wage increases. In <strong>the</strong> more recent<br />

years productivity gains slowed down <strong>and</strong> were no longer sufficient <strong>to</strong> compensate<br />

wage increases which grew at <strong>the</strong> same pace as during preceding years. The unit-labour<br />

costs started growing. Moreover macro-economic stabilization made some progress.<br />

Measures were taken <strong>to</strong> prepare for <strong>the</strong> accession <strong>to</strong> <strong>the</strong> euro zone. A stricter fiscal <strong>and</strong><br />

monetary policy led <strong>to</strong> confidence in <strong>the</strong> New Member States’ currencies. As a consequence<br />

<strong>the</strong>y appreciated against <strong>the</strong> Euro. Price competitiveness shrunk – induced by<br />

both of <strong>the</strong>se effects.<br />

The worsening of <strong>the</strong> advantage in price competitiveness against <strong>the</strong> EU-15 must not be<br />

interpreted as a general loss of <strong>the</strong> new Member States attractiveness as a location for<br />

production. The still high wage differentials as compared <strong>to</strong> <strong>the</strong> old Member States will<br />

incite fur<strong>the</strong>r relocation of capacities. But this development underscores that <strong>the</strong>re is a<br />

loss of competitiveness as a location for labour intensive, less qualified production.<br />

These workplaces have helped <strong>to</strong> keep unemployment on an endurable albeit high level<br />

during <strong>the</strong> transition period. It is not very likely that a relocation of production from<br />

EU-15 <strong>to</strong> <strong>the</strong> new Member States accompanied by fur<strong>the</strong>r eastward relocation will result<br />

in a growth of employment in <strong>the</strong> engineering sec<strong>to</strong>rs in <strong>the</strong> enlarged European Union.<br />

A remarkable wage hike happened in domestic appliances <strong>and</strong> in electrical engineering.<br />

Both of <strong>the</strong>se sec<strong>to</strong>rs were responsible for <strong>the</strong> worsening of <strong>the</strong> price competitiveness of<br />

<strong>to</strong>tal engineering. In mechanical engineering <strong>the</strong> development was quite different, productivity<br />

gains were somewhat lower, but wages grew “only” at a yearly rate of 10%.<br />

Unit-labour costs fell in contrast <strong>to</strong> <strong>the</strong> development of both of <strong>the</strong> o<strong>the</strong>r sec<strong>to</strong>rs.<br />

1.6 Conclusions<br />

The engineering sec<strong>to</strong>rs of <strong>the</strong> new Member States have been growing strongly over <strong>the</strong><br />

period under investigation. They gained shares in international trade, as compared <strong>to</strong> <strong>the</strong><br />

EU-15, Japan <strong>and</strong> <strong>the</strong> USA. In electrical engineering <strong>and</strong> domestic appliances exports

9<br />

in<strong>to</strong> <strong>the</strong> global market grew most dynamically. For mechanical engineering <strong>the</strong> intra<br />

European linkages have been intensified <strong>and</strong> <strong>the</strong> creation of a new wider cluster is an<br />

important feature of <strong>the</strong> enlarged European Union.<br />

High investment <strong>and</strong> <strong>the</strong> introduction of advanced management techniques induced<br />

enormous efficiency gains. However <strong>the</strong> overall price competitiveness improved only<br />

during <strong>the</strong> earlier years of <strong>the</strong> period under investigation. During <strong>the</strong> more recent years a<br />

reduction was reported. For all engineering industries price competitiveness fell slightly<br />

compared <strong>to</strong> <strong>the</strong> EU-15, although in absolute terms <strong>the</strong>re is a qualified labour supply<br />

<strong>and</strong> wages are still extremely attractive. The worsening of price competitiveness is a<br />

challenge for those productions in <strong>the</strong> new Member States which are built primarily on<br />

<strong>the</strong> availability of cheap, less qualified labour <strong>and</strong> are exposed <strong>to</strong> <strong>to</strong>ugh international<br />

competition. The losses of price competitiveness <strong>to</strong>ok place above all in domestic appliances<br />

<strong>and</strong> electrical engineering.<br />

The employment record of <strong>the</strong> engineering industries in <strong>the</strong> new Member States is, notwithst<strong>and</strong>ing<br />

high output growth, disappointing. Despite gains in global trade <strong>and</strong> relocation<br />

from <strong>the</strong> old Member States workplaces got lost, even at a marginal higher pace<br />

than in <strong>the</strong> EU-15. This development points <strong>to</strong> <strong>the</strong> question in how far framework conditions<br />

<strong>and</strong> labour market institutions are adequate for international competitive locations<br />

for production in <strong>the</strong> new Member States. In this respect <strong>the</strong> interviews disclosed<br />

that <strong>the</strong> harmonization as required by <strong>the</strong> Acquis Communautaire in advance of <strong>the</strong> accession<br />

has not been perceived as a hindrance for entrepreneurial freedom. Only little<br />

criticism was raised on <strong>the</strong> working time directive <strong>and</strong> <strong>the</strong> regulation of health <strong>and</strong><br />

safety in <strong>the</strong> working environment.<br />

Never<strong>the</strong>less <strong>the</strong> strong growth of wages, which has not been compensated by efficiency<br />

gains in recent years, suggests that flexibility in <strong>the</strong> labour market is not sufficient<br />

for <strong>the</strong> countries during <strong>the</strong>ir transition phase. The investigation revealed that <strong>the</strong>re<br />

is a high number of companies at <strong>the</strong> threshold of survival. These marginal firms are<br />

endangered by wage hikes. Fur<strong>the</strong>r losses of workplaces will be suffered in <strong>the</strong> engineering<br />

industries. In particular labour intensive production will be relocated <strong>to</strong> non EU<br />

locations.<br />

From <strong>the</strong> st<strong>and</strong>point of <strong>the</strong> more mature European countries <strong>the</strong> labour market in <strong>the</strong><br />

new Member States is perceived as flexible. However interviews in some of <strong>the</strong> countries<br />

unveiled criticism that decision making on <strong>to</strong>pics with relevance for <strong>the</strong> labour<br />

market <strong>and</strong> social issues is cumbersome <strong>and</strong> needs a broad consensus. In most of <strong>the</strong><br />

states high level agreements are characterized by three partite negotiations of entrepre-

10<br />

neurs associations, unions <strong>and</strong> <strong>the</strong> government. The situation is similar <strong>to</strong> o<strong>the</strong>r continental<br />

European countries which suffer from poor functioning labour markets.<br />

A solution <strong>to</strong> <strong>the</strong> problems of unemployment can be achieved by an upgrading of labour<br />

quality <strong>and</strong> an entry in<strong>to</strong> a more knowledge based economy. However a growth in <strong>the</strong><br />

number of workplaces will only take place in <strong>the</strong> long run. An important lesson <strong>to</strong> be<br />

learned in <strong>the</strong> more mature EU Member States is, that it will be extremely difficult <strong>to</strong><br />

compensate losses of workplaces for low qualified labour by gains in employment for<br />

qualified labour. A necessary prerequisite for such a development is a well functioning<br />

labour market. This is in particular true for countries during a transition period with its<br />

extreme structural changes which result in losses of employment in some sec<strong>to</strong>rs <strong>and</strong><br />

gains in o<strong>the</strong>rs. Only well functioning labour markets can avoid frictions raised by local<br />

disequilibria.<br />

The investigation in <strong>the</strong> engineering sec<strong>to</strong>rs of <strong>the</strong> new Member States provides an initial<br />

impression on strengths <strong>and</strong> weaknesses. Fur<strong>the</strong>r research is suggested <strong>to</strong> evaluate<br />

policies which should be designed <strong>to</strong> streng<strong>the</strong>n <strong>the</strong> competitiveness of <strong>the</strong> engineering<br />

industries. It should be directed <strong>to</strong>ward price <strong>and</strong> technology competition. An in-depth<br />

assessment of <strong>the</strong> challenges from emerging competi<strong>to</strong>rs, namely China is proposed.<br />

This requires a more detailed analysis of trade flows by product groups as well as an<br />

assessment of <strong>the</strong> supply side conditions in <strong>the</strong> newly industrializing economies <strong>and</strong> <strong>the</strong><br />

entrepreneurial potential which contributes <strong>to</strong> <strong>the</strong>ir comparative advantages.<br />

The analysis of <strong>the</strong> technological competition in this study has focused on areas that are<br />

directly related <strong>to</strong> engineering industries. Many of <strong>the</strong>se technologies are mature. In a<br />

more detailed investigation <strong>the</strong> so-called new technologies, such as information <strong>and</strong><br />

communication technology, new materials etc. should be taken in<strong>to</strong> consideration. To a<br />

large extent progress in <strong>the</strong>se technologies is provided by upstream industries <strong>and</strong> has<br />

not been considered in <strong>the</strong> study at h<strong>and</strong>. These technologies <strong>and</strong> <strong>the</strong> related industries<br />

should be integrated in a more comprehensive investigation of <strong>the</strong> competitiveness.<br />

Likewise linkages <strong>to</strong> downstream industries should be taken in<strong>to</strong> account. The spanning<br />

<strong>to</strong>pic for <strong>the</strong> investigation should be an assessment of different policy options <strong>and</strong> <strong>the</strong>ir<br />

impact on <strong>the</strong> development of <strong>the</strong> engineering industries’ competitiveness <strong>and</strong> employment.

11<br />

2 Importance <strong>and</strong> Evolution of <strong>the</strong> <strong>Engineering</strong> Sec<strong>to</strong>rs in <strong>the</strong> New Member States<br />

This chapter provides <strong>the</strong> in-depth analysis of <strong>the</strong> new Member States engineering, distinguished<br />

by sec<strong>to</strong>r <strong>and</strong> by country. Chapter 2.1 gives an overview on <strong>to</strong>tal engineering<br />

for all of <strong>the</strong> acceded countries. The engineering sec<strong>to</strong>rs of <strong>the</strong>se countries are compared<br />

<strong>to</strong> <strong>the</strong> EU-15 by its size <strong>and</strong> its development. Special attention is paid <strong>to</strong> <strong>the</strong> evolution<br />

pattern during <strong>the</strong> phase of transition in particular tendencies in employment,<br />

growth <strong>and</strong> productivity are shown. This analysis illustrates that <strong>the</strong> new Member States<br />

growth was above all made possible by a markedly increased efficiency of labour input.<br />

Albeit strongly growing output <strong>the</strong> employment record was even worse than for <strong>the</strong> EU-<br />

15.<br />

Following in Chapter 2.2 <strong>the</strong> subsec<strong>to</strong>rs of <strong>the</strong> engineering industries are described in<br />

detail. They are compared <strong>to</strong> <strong>the</strong> EU-15 by output, employment, productivity, labour<br />

costs <strong>and</strong> unit-labour costs. The efficiency indica<strong>to</strong>rs of <strong>the</strong> subsec<strong>to</strong>rs are also calculated<br />

as a percentage of <strong>the</strong> respective indica<strong>to</strong>r for <strong>to</strong>tal engineering <strong>and</strong> give thus an<br />

insight in <strong>the</strong> relative position of <strong>the</strong> subsec<strong>to</strong>r as compared <strong>to</strong> <strong>to</strong>tal new Member States<br />

engineering sec<strong>to</strong>rs <strong>and</strong> <strong>the</strong> relative position of this subsec<strong>to</strong>r as compared <strong>to</strong> its counterpart<br />

in <strong>the</strong> EU-15.<br />

Chapter 2.3 analyses <strong>the</strong> performance of <strong>the</strong> engineering industries by each of <strong>the</strong><br />

Member States under consideration. The five bigger Member States are analysed separately<br />

<strong>and</strong> <strong>the</strong> Baltic States are regarded <strong>to</strong>ge<strong>the</strong>r. The absolute figures, <strong>the</strong> efficiency<br />

indica<strong>to</strong>rs <strong>and</strong> <strong>the</strong> development are compared <strong>to</strong> all of <strong>the</strong> acceded countries. This chapter<br />

also contains a qualitative description <strong>and</strong> assessment of <strong>the</strong> sec<strong>to</strong>rs mechanical <strong>and</strong><br />

electrical engineering as well as for domestic appliances. Additionally this chapter gives<br />

insight in<strong>to</strong> micro-economic developments exemplarily stressed for selected companies.<br />

2.1 <strong>Engineering</strong> Sec<strong>to</strong>rs in all of <strong>the</strong> New Member States Compared <strong>to</strong> EU-15<br />

The engineering sec<strong>to</strong>rs in <strong>the</strong> new Member States contribute 14.4% <strong>to</strong> <strong>to</strong>tal manufacturing<br />

output (Table 2.1). As compared <strong>to</strong> <strong>the</strong> former EU-15 <strong>the</strong> weight of <strong>the</strong> engineering<br />

industries on <strong>to</strong>tal manufacturing is quite similar, 13.3% in 2004 (Table2.2).<br />

There are three sec<strong>to</strong>rs under consideration, mechanical engineering (NACE 29.1-5),<br />

electrical engineering (NACE 31) <strong>and</strong> domestic appliances (NACE 29.7). Both of <strong>the</strong><br />

first two sec<strong>to</strong>rs supply investment goods <strong>and</strong> affiliated intermediary goods, whereas <strong>the</strong>

12<br />

third sec<strong>to</strong>r comprises durable consumer goods. This means that <strong>the</strong> market environment<br />

differs much from <strong>the</strong> first two sec<strong>to</strong>rs. It is characterized by a supply of st<strong>and</strong>ard<br />

Table 2.1: Key data for <strong>the</strong> New Member States’ <strong>Engineering</strong> Sec<strong>to</strong>rs 2004<br />

Indica<strong>to</strong>r Total engineering <strong>Mechanical</strong> engineering<br />

<strong>Electrical</strong> engineering<br />

Household appliances<br />

Units in % 1) Units in % 2) Units in % 2) Units in % 2)<br />

Production (€ m) 35,698 14,267 40.0 18,285 51.2 3,147 8.8<br />

Value added (€ m) 11,035 14.4 5,243 47.5 5,063 45.9 729 6.6<br />

Employees (1000) 760 13.8 381 50.1 338 44.4 42 5.5<br />

Labour productivity 3) 14.5 105.0 13.8 94.9 15.0 103.3 17.3 119.2<br />

Unit-labour costs 4) 0.62 146.7 0.65 109.5 0.67 111.9 0.84 141.3<br />

Innovation intensity 5) 6.9 11.0 159.2 3.6 51.8 4.0 58.5<br />

Extra EU-25 exports<br />

(€ m)<br />

5,190 12.6 3,323 64.0 1,866 36.0 617 11.9<br />

Extra EU-25 imports<br />

(€ m)<br />

6,815 12.7 3,282 48.1 3,534 51.9 504 7.4<br />

Exports <strong>to</strong> EU-15<br />

(€ m) 6) 21,620 24.1 9,816 45.4 11,804 54.6 2,316 10.7<br />

Imports from EU-15<br />

(€ m) 6) 26,811 35.5 16,923 63.1 9,888 36.9 1,473 5.5<br />

1) As a percentage of <strong>to</strong>tal manufacturing; 2) As a percentage of <strong>to</strong>tal engineering; 3) 1000€ per capita<br />

<strong>and</strong> annum; 4) Labour Costs (€) per Value Added (€); 5) Patent applications in at least 2 countries per<br />

1 billion € production; 6) For <strong>the</strong> EU-15: foreign trade with NMS.<br />

Source: EUROSTAT; epidos/INPADOC; VDMA; ZVEI; Calculation by <strong>the</strong> Ifo Institute.

13<br />

Table2.2: Key data for <strong>the</strong> EU-15 <strong>Engineering</strong> Sec<strong>to</strong>rs 2004<br />

Indica<strong>to</strong>r<br />

Total engineering <strong>Mechanical</strong> engineerinneering<br />

<strong>Electrical</strong> engi-<br />

Household<br />

appliances 3)<br />

Units Share 1) Units Share 2) Units Share 2) Units 3) Share 2)<br />

Production (€ m) 588,272 11.0 380,068 64.6 177,905 30.2 30,299 5.2<br />

Value added (€ m) 193,128 13.3 127,560 66.0 54,876 28.4 9,638 5.0<br />

Employees (1000) 3,298 11.8 2,211 67.0 1,087 33.0 183 5.6<br />

Labour productivity 58.6 112.7 57.7 98.5 50.5 86.2 52.6 89.9<br />

Unit-labour costs 0.75 0.77 102.0 0.74 98.3 0.71 94.3<br />

Innovation intensity 37.9 42.5 112.1 27.7 72.9 34.3 90.5<br />

Extra EU-25 exports (€ 141,626 95,615 67.5 38,741 27.4 7,270 5.1<br />

m)<br />

Extra EU-25 imports 88,772 50,001 56.3 32,293 36.4 6,478 7.3<br />

(€ m)<br />

Exports <strong>to</strong> NMS (€ 26,811 16,923 63.1 9,888 36.9 1,414 5.3<br />

m)<br />

Imports from NMS 21,620 9,816 45.4 11,804 54.6 2,161 10.0<br />

(€ m)<br />

1) As a percentage of <strong>to</strong>tal manufacturing industries; 2) As a percentage of <strong>to</strong>tal engineering; 3) <strong>Electrical</strong><br />

household appliances (For <strong>the</strong> definition of <strong>the</strong> respective variables see Table 2.1)<br />

Source: EUROSTAT; epidos/INPADOC; VDMA; ZVEI; Calculation by <strong>the</strong> Ifo Institute.<br />

ized volume products. Efficient distribution channels, economies of scale <strong>and</strong> <strong>the</strong> selection<br />

of a location for production are of outst<strong>and</strong>ing importance. For <strong>the</strong> o<strong>the</strong>r sec<strong>to</strong>rs<br />

under investigation close relationships <strong>to</strong> clients <strong>and</strong> <strong>the</strong> design of cus<strong>to</strong>mized solutions<br />

are more important.<br />

If one compares mechanical <strong>and</strong> electrical engineering <strong>the</strong>re are also some noteworthy<br />

differences <strong>to</strong> be mentioned. <strong>Mechanical</strong> engineering is – with <strong>the</strong> exception of a few<br />

subgroups – <strong>the</strong> main supplying sec<strong>to</strong>r of manufacturing technologies. <strong>Electrical</strong> engineering<br />

does not only comprise capital goods, such as mo<strong>to</strong>rs, genera<strong>to</strong>rs <strong>and</strong> related<br />

intermediary goods, but also a broad range of products, such as lighting, batteries <strong>and</strong><br />

accumula<strong>to</strong>rs which are <strong>to</strong> a certain extent dedicated for private households. In some<br />

segments <strong>the</strong>re is a large-batch production. Fur<strong>the</strong>r on <strong>the</strong> au<strong>to</strong>motive industry is an<br />

important client industry, which orders starters, batteries, lighting etc. This sec<strong>to</strong>r has<br />

got some stimulus from foreign direct investment (FDI) for <strong>the</strong> production of cars in <strong>the</strong><br />

new Member States <strong>and</strong> an additional growth impetus, as measured by <strong>the</strong> production.<br />

The sec<strong>to</strong>rs electrical engineering <strong>and</strong> domestic appliances were in <strong>the</strong> focus of big international<br />

players in <strong>the</strong> market, whereas in mechanical engineering even mediumsized<br />

companies above all from <strong>the</strong> EU-15 have overtaken a noteworthy stake in pro-

14<br />

duction. These discrepancies suggest analysing <strong>the</strong> three sec<strong>to</strong>rs independently from<br />

each o<strong>the</strong>r.<br />

In <strong>the</strong> new Member States electrical engineering is bigger than mechanical engineering<br />

<strong>and</strong> comm<strong>and</strong>s more than half <strong>the</strong> engineering sec<strong>to</strong>rs production. Domestic appliances<br />

contributes roughly one tenth. In contrast, within <strong>the</strong> EU-15 <strong>the</strong>re is a dominance of<br />

mechanical engineering with a contribution of around two thirds, whereas electrical<br />

engineering only comes up <strong>to</strong> 30% of <strong>to</strong>tal engineering industries output.<br />

Since <strong>the</strong> mid 1990s <strong>the</strong> engineering industries enjoy - as many o<strong>the</strong>r manufacturing<br />

industries - strong growth. In all of <strong>the</strong> three sec<strong>to</strong>rs rates varied between 6.0% for mechanical<br />

<strong>and</strong> 15.7% for electrical engineering on average between 1995 <strong>and</strong> 2004. A<br />

comparison with <strong>the</strong> EU-15 discloses a major gap in <strong>the</strong> growth momentum with only<br />

1.6% for domestic appliances <strong>and</strong> 2.6% for both of <strong>the</strong> engineering sec<strong>to</strong>rs. However<br />

employment record of <strong>the</strong> new Member States’ engineering sec<strong>to</strong>rs was even worse than<br />

in <strong>the</strong> EU-15. The number of employees shrank during <strong>the</strong> period under investigation in<br />

mechanical engineering <strong>and</strong> domestic appliances. Only in electrical engineering which<br />

enjoyed <strong>the</strong> most dynamic upswing <strong>the</strong> number of workplaces grew. But this was not<br />

sufficient for a positive balance for <strong>the</strong> engineering sec<strong>to</strong>rs as a whole. The enabler for<br />

growth was labour productivity which improved much over time. No additional job opportunities<br />

were provided (Table 2.3, Table2.4 for a comparison <strong>to</strong> <strong>the</strong> EU-15).

15<br />

Table 2.3: Evolution of New Member States’ <strong>Engineering</strong> Sec<strong>to</strong>rs 1995 –<br />

2004<br />

Indica<strong>to</strong>r<br />

Manufacturing<br />

industries<br />

Total engineering<br />

<strong>Mechanical</strong><br />

engineering<br />

<strong>Electrical</strong><br />

engineering<br />

Household<br />

appliances<br />

Aagr 1) Aagr 1) Aagr 1) Aagr 1) Aagr 1)<br />

Production 10.5 6.0 15.7 10.5<br />

Value added 7.2 9.1 6.4 12.6 8.4<br />

Employees -1.5 -1.3 -4.2 1.0 -3.2<br />

Labour productivity<br />

8.9 10.5 11.7 10.8 12.0<br />

Unit-labour costs -1.5 -1.9 1.4 2.0<br />

Extra EU-25 exports<br />

13.0 9.5 8.8 9.6 13.1<br />

Extra EU-25 imports<br />

15.5 17.8 14.6 22.0 17.8<br />

Exports <strong>to</strong> EU-15 17.2 10.6 6.2 15.9 14.9<br />

Imports from<br />

EU-15<br />

14.0 10.9 7.8 14.3 14.0<br />

1) Average annual growth rate in % (For <strong>the</strong> definition of <strong>the</strong> respective variables see<br />

Table 2.1)<br />

Source: EUROSTAT; VDMA; ZVEI; Calculation by <strong>the</strong> Ifo Institute<br />

Table2.4: Evolution of EU-15 <strong>Engineering</strong> Sec<strong>to</strong>rs 1995 - 2004<br />

Indica<strong>to</strong>r<br />

Manufacturing<br />

industries<br />

Total engineering<br />

<strong>Mechanical</strong><br />

engineering<br />

<strong>Electrical</strong><br />

engineering<br />

Household<br />

appliances<br />

2)<br />

Aagr 1) Aagr 1) Aagr 1) Aagr 1) Aagr 1)<br />

Production (€ m) 3.6 2.5 2.6 2.6 1.6<br />

Value added (€ m) 1.2 1.3 1.5 0.8 -0.2<br />

Employees (1000) -1.0 -1.0 -0.1 -0.8 -2.0<br />

Labour productivity 1.9 1.6 1.2 0.8<br />

Unit-labour costs -0.1 -0.1 0.0<br />

Extra EU-25 exports<br />

(€ m)<br />

5.2 4.5 6.1 9.8<br />

Extra EU-25 imports<br />

(€ m)<br />

9.4 11.0 6.3 16.0<br />

Exports <strong>to</strong> NMS (€ m) 11.3 10.9 13.1 6.5<br />

Imports from NMS (€<br />

16.2 16.7 16.7 11.4<br />

m)<br />

1) Aggregate average growth 2) <strong>Electrical</strong> household appliances (For <strong>the</strong> definition of <strong>the</strong><br />

respective variables see Table 2.1)<br />

Source: EUROSTAT; epidos/INPADOC; VDMA; ZVEI; Calculation by <strong>the</strong> Ifo Institute.

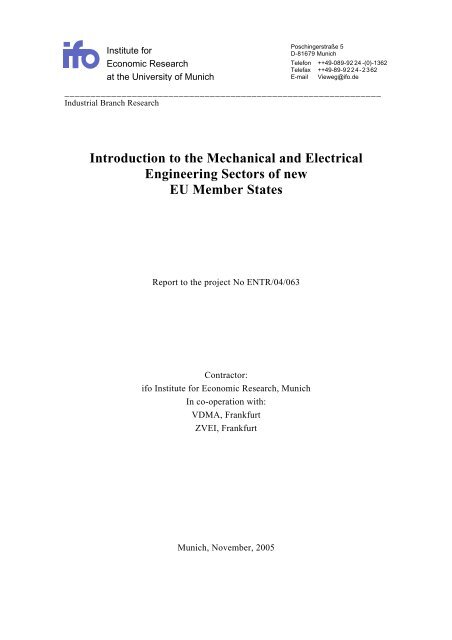

16<br />

The differing patterns between <strong>the</strong> EU-15 <strong>and</strong> <strong>the</strong> new Member States in engineering<br />

industries are disclosed in Fehler! Verweisquelle konnte nicht gefunden werden..<br />

The growth of production in <strong>the</strong> EU-15 engineering industries is characterized by a<br />

moderate expansion for <strong>the</strong> period under investigation, whereas in <strong>the</strong> new Member<br />

States’ output soars. But <strong>the</strong> employment is stable for <strong>the</strong> EU-15, only in domestic appliances<br />

- with its quite different market environment - employment shrinks. For <strong>the</strong><br />

new Member States <strong>the</strong> employment record is worse than for <strong>the</strong> EU-15. Noteworthy<br />

losses <strong>to</strong>ok place between 1995 <strong>and</strong> 2002 in mechanical engineering <strong>and</strong> in domestic<br />

appliances. Only in electrical engineering new job opportunities were created. The balance<br />

of all engineering industries shows a slight decline in <strong>the</strong> number of workplaces in<br />

spite of growth <strong>and</strong> relocation. This pattern is typical for many of <strong>the</strong> manufacturing<br />

industries in <strong>the</strong> new Member States <strong>and</strong> not restricted <strong>to</strong> <strong>the</strong> engineering sec<strong>to</strong>rs under<br />

consideration.

17<br />

Figure 2.1:<br />

<strong>Engineering</strong> Industries in EU-15 <strong>and</strong> <strong>the</strong> new Member States<br />

Production<br />

<strong>Mechanical</strong> engineering<br />

Employees<br />

<strong>Mechanical</strong> <strong>Engineering</strong><br />

150<br />

150<br />

130<br />

130<br />

110<br />

110<br />

90<br />

70<br />

50<br />

1995<br />

1996<br />

1997<br />