Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

94<br />

8. Risk Assessment Procedures<br />

Chapter C<strong>on</strong>tent<br />

The nature and use of risk assessment procedures by an audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r <str<strong>on</strong>g>to</str<strong>on</strong>g><br />

identify and assess the risks of material misstatement.<br />

Relevant ISAs<br />

240, 315<br />

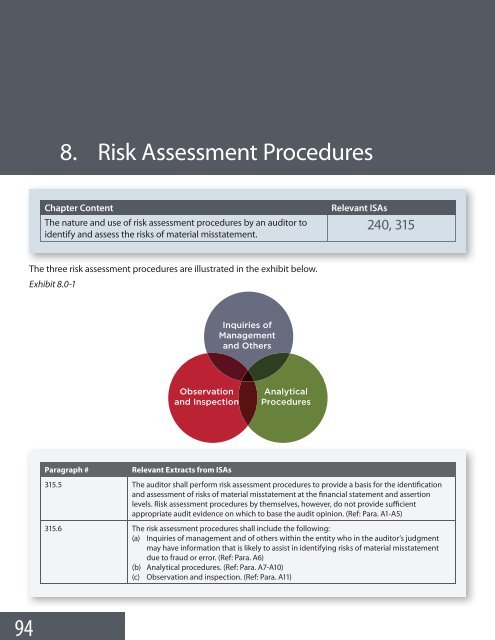

The three risk assessment procedures are illustrated <strong>in</strong> the exhibit below.<br />

Exhibit 8.0-1<br />

<br />

<br />

<br />

<br />

<br />

<br />

<br />

Paragraph #<br />

Relevant Extracts from ISAs<br />

315.5 The audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r shall perform risk assessment procedures <str<strong>on</strong>g>to</str<strong>on</strong>g> provide a basis for the identificati<strong>on</strong><br />

and assessment of risks of material misstatement at the f<strong>in</strong>ancial statement and asserti<strong>on</strong><br />

levels. Risk assessment procedures by themselves, however, do not provide sufficient<br />

appropriate audit evidence <strong>on</strong> which <str<strong>on</strong>g>to</str<strong>on</strong>g> base the audit op<strong>in</strong>i<strong>on</strong>. (Ref: Para. A1-A5)<br />

315.6 The risk assessment procedures shall <strong>in</strong>clude the follow<strong>in</strong>g:<br />

(a) Inquiries of management and of others with<strong>in</strong> the entity who <strong>in</strong> the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s judgment<br />

may have <strong>in</strong>formati<strong>on</strong> that is likely <str<strong>on</strong>g>to</str<strong>on</strong>g> assist <strong>in</strong> identify<strong>in</strong>g risks of material misstatement<br />

due <str<strong>on</strong>g>to</str<strong>on</strong>g> fraud or error. (Ref: Para. A6)<br />

(b) Analytical procedures. (Ref: Para. A7-A10)<br />

(c) Observati<strong>on</strong> and <strong>in</strong>specti<strong>on</strong>. (Ref: Para. A11)