Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

30<br />

<str<strong>on</strong>g>Guide</str<strong>on</strong>g> <str<strong>on</strong>g>to</str<strong>on</strong>g> <str<strong>on</strong>g>Us<strong>in</strong>g</str<strong>on</strong>g> <str<strong>on</strong>g>Internati<strong>on</strong>al</str<strong>on</strong>g> <str<strong>on</strong>g>Standards</str<strong>on</strong>g> <strong>on</strong> <strong>Audit<strong>in</strong>g</strong> <strong>in</strong> the Audits of Small- and Medium-Sized Entities Volume 1—Core C<strong>on</strong>cepts<br />

Requirements<br />

Use of Professi<strong>on</strong>al<br />

Judgment<br />

Descripti<strong>on</strong><br />

The ISA audit requirements require the use and then documentati<strong>on</strong> of significant<br />

judgments made by the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r throughout the audit. Typical examples of tasks<br />

throughout the risk assessment process <strong>in</strong>clude:<br />

• Decid<strong>in</strong>g <str<strong>on</strong>g>to</str<strong>on</strong>g> accept or c<strong>on</strong>t<strong>in</strong>ue with the client;<br />

• Develop<strong>in</strong>g the overall audit strategy;<br />

• Establish<strong>in</strong>g materiality;<br />

• Assess<strong>in</strong>g risks of material misstatement, <strong>in</strong>clud<strong>in</strong>g the identificati<strong>on</strong> of significant<br />

risks and other areas where special audit c<strong>on</strong>siderati<strong>on</strong> may be necessary; and<br />

• Develop<strong>in</strong>g expectati<strong>on</strong>s for use when perform<strong>in</strong>g analytical procedures.<br />

Risk Resp<strong>on</strong>se<br />

Paragraph #<br />

ISA Objective(s)<br />

330.3 The objective of the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r is <str<strong>on</strong>g>to</str<strong>on</strong>g> obta<strong>in</strong> sufficient appropriate audit evidence regard<strong>in</strong>g the<br />

assessed risks of material misstatement, through design<strong>in</strong>g and implement<strong>in</strong>g appropriate<br />

resp<strong>on</strong>ses <str<strong>on</strong>g>to</str<strong>on</strong>g> those risks.<br />

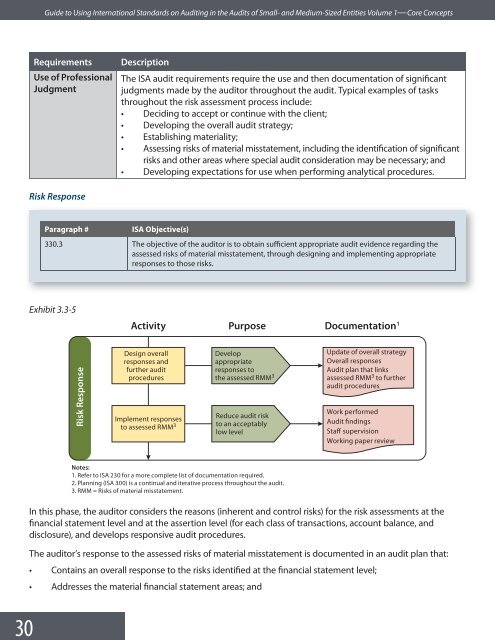

Exhibit 3.3-5<br />

Activity Purpose Documentati<strong>on</strong> 1<br />

Risk Resp<strong>on</strong>se<br />

Design overall<br />

resp<strong>on</strong>ses and<br />

further audit<br />

procedures<br />

Implement resp<strong>on</strong>ses<br />

<str<strong>on</strong>g>to</str<strong>on</strong>g> assessed RMM 3<br />

Develop<br />

appropriate<br />

resp<strong>on</strong>ses <str<strong>on</strong>g>to</str<strong>on</strong>g><br />

the assessed RMM 3<br />

Reduce audit risk<br />

<str<strong>on</strong>g>to</str<strong>on</strong>g> an acceptably<br />

low level<br />

Update of overall strategy<br />

Overall resp<strong>on</strong>ses<br />

Audit plan that l<strong>in</strong>ks<br />

assessed RMM 3 <str<strong>on</strong>g>to</str<strong>on</strong>g> further<br />

audit procedures<br />

Work performed<br />

Audit f<strong>in</strong>d<strong>in</strong>gs<br />

Staff supervisi<strong>on</strong><br />

Work<strong>in</strong>g paper review<br />

Notes:<br />

1. Refer <str<strong>on</strong>g>to</str<strong>on</strong>g> ISA 230 for a more complete list of documentati<strong>on</strong> required.<br />

2. Plann<strong>in</strong>g (ISA 300) is a c<strong>on</strong>t<strong>in</strong>ual and iterative process throughout the audit.<br />

3. RMM = Risks of material misstatement.<br />

In this phase, the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r c<strong>on</strong>siders the reas<strong>on</strong>s (<strong>in</strong>herent and c<strong>on</strong>trol risks) for the risk assessments at the<br />

f<strong>in</strong>ancial statement level and at the asserti<strong>on</strong> level (for each class of transacti<strong>on</strong>s, account balance, and<br />

disclosure), and develops resp<strong>on</strong>sive audit procedures.<br />

The audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s resp<strong>on</strong>se <str<strong>on</strong>g>to</str<strong>on</strong>g> the assessed risks of material misstatement is documented <strong>in</strong> an audit plan that:<br />

• C<strong>on</strong>ta<strong>in</strong>s an overall resp<strong>on</strong>se <str<strong>on</strong>g>to</str<strong>on</strong>g> the risks identified at the f<strong>in</strong>ancial statement level;<br />

• Addresses the material f<strong>in</strong>ancial statement areas; and