Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

199<br />

<str<strong>on</strong>g>Guide</str<strong>on</strong>g> <str<strong>on</strong>g>to</str<strong>on</strong>g> <str<strong>on</strong>g>Us<strong>in</strong>g</str<strong>on</strong>g> <str<strong>on</strong>g>Internati<strong>on</strong>al</str<strong>on</strong>g> <str<strong>on</strong>g>Standards</str<strong>on</strong>g> <strong>on</strong> <strong>Audit<strong>in</strong>g</strong> <strong>in</strong> the Audits of Small- and Medium-Sized Entities Volume 1—Core C<strong>on</strong>cepts<br />

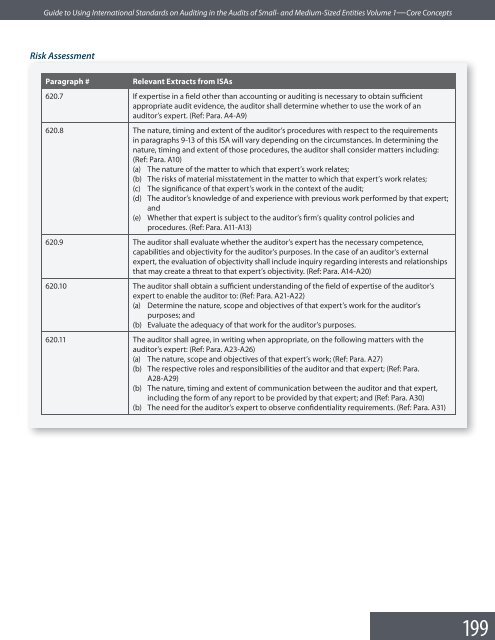

Risk Assessment<br />

Paragraph #<br />

Relevant Extracts from ISAs<br />

620.7 If expertise <strong>in</strong> a field other than account<strong>in</strong>g or audit<strong>in</strong>g is necessary <str<strong>on</strong>g>to</str<strong>on</strong>g> obta<strong>in</strong> sufficient<br />

appropriate audit evidence, the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r shall determ<strong>in</strong>e whether <str<strong>on</strong>g>to</str<strong>on</strong>g> use the work of an<br />

audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s expert. (Ref: Para. A4-A9)<br />

620.8 The nature, tim<strong>in</strong>g and extent of the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s procedures with respect <str<strong>on</strong>g>to</str<strong>on</strong>g> the requirements<br />

<strong>in</strong> paragraphs 9-13 of this ISA will vary depend<strong>in</strong>g <strong>on</strong> the circumstances. In determ<strong>in</strong><strong>in</strong>g the<br />

nature, tim<strong>in</strong>g and extent of those procedures, the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r shall c<strong>on</strong>sider matters <strong>in</strong>clud<strong>in</strong>g:<br />

(Ref: Para. A10)<br />

(a) The nature of the matter <str<strong>on</strong>g>to</str<strong>on</strong>g> which that expert’s work relates;<br />

(b) The risks of material misstatement <strong>in</strong> the matter <str<strong>on</strong>g>to</str<strong>on</strong>g> which that expert’s work relates;<br />

(c) The significance of that expert’s work <strong>in</strong> the c<strong>on</strong>text of the audit;<br />

(d) The audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s knowledge of and experience with previous work performed by that expert;<br />

and<br />

(e) Whether that expert is subject <str<strong>on</strong>g>to</str<strong>on</strong>g> the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s firm’s quality c<strong>on</strong>trol policies and<br />

procedures. (Ref: Para. A11-A13)<br />

620.9 The audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r shall evaluate whether the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s expert has the necessary competence,<br />

capabilities and objectivity for the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s purposes. In the case of an audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s external<br />

expert, the evaluati<strong>on</strong> of objectivity shall <strong>in</strong>clude <strong>in</strong>quiry regard<strong>in</strong>g <strong>in</strong>terests and relati<strong>on</strong>ships<br />

that may create a threat <str<strong>on</strong>g>to</str<strong>on</strong>g> that expert’s objectivity. (Ref: Para. A14-A20)<br />

620.10 The audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r shall obta<strong>in</strong> a sufficient understand<strong>in</strong>g of the field of expertise of the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s<br />

expert <str<strong>on</strong>g>to</str<strong>on</strong>g> enable the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r <str<strong>on</strong>g>to</str<strong>on</strong>g>: (Ref: Para. A21-A22)<br />

(a) Determ<strong>in</strong>e the nature, scope and objectives of that expert’s work for the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s<br />

purposes; and<br />

(b) Evaluate the adequacy of that work for the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s purposes.<br />

620.11 The audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r shall agree, <strong>in</strong> writ<strong>in</strong>g when appropriate, <strong>on</strong> the follow<strong>in</strong>g matters with the<br />

audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s expert: (Ref: Para. A23-A26)<br />

(a) The nature, scope and objectives of that expert’s work; (Ref: Para. A27)<br />

(b) The respective roles and resp<strong>on</strong>sibilities of the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r and that expert; (Ref: Para.<br />

A28-A29)<br />

(b) The nature, tim<strong>in</strong>g and extent of communicati<strong>on</strong> between the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r and that expert,<br />

<strong>in</strong>clud<strong>in</strong>g the form of any report <str<strong>on</strong>g>to</str<strong>on</strong>g> be provided by that expert; and (Ref: Para. A30)<br />

(b) The need for the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s expert <str<strong>on</strong>g>to</str<strong>on</strong>g> observe c<strong>on</strong>fidentiality requirements. (Ref: Para. A31)