Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC Guide to Using International Standards on Auditing in - IFAC

194

195

- Page 143 and 144: 143 Guide

- Page 145 and 146: 145 12. Related Parties Chapter Con

- Page 147 and 148: 147 Guide

- Page 149 and 150: 149 Guide

- Page 151 and 152: 151 Guide

- Page 153 and 154: 153 Guide

- Page 155 and 156: 155 Guide

- Page 157 and 158: 157 Guide

- Page 159 and 160: 159 Guide

- Page 161 and 162: 161 14. Going Concern Chapter Conte

- Page 163 and 164: 163 Guide

- Page 165 and 166: 165 Guide

- Page 167 and 168: 167 Guide

- Page 169 and 170: 169 Guide

- Page 171 and 172: 171 15. Summary of Other ISA Requir

- Page 173 and 174: 173 Guide

- Page 175 and 176: 175 Guide

- Page 177 and 178: 177 Guide

- Page 179 and 180: 179 Guide

- Page 181 and 182: 181 Guide

- Page 183 and 184: 183 Guide

- Page 185 and 186: 185 Guide

- Page 187 and 188: 187 Guide

- Page 189 and 190: 189 Guide

- Page 191 and 192: 191 Guide

- Page 193: 193 Guide

- Page 197 and 198: 197 Guide

- Page 199 and 200: 199 Guide

- Page 201 and 202: 201 Guide

- Page 203 and 204: 203 Guide

- Page 205 and 206: 205 16. Audit Documentation Chapter

- Page 207 and 208: 207 Guide

- Page 209 and 210: 209 Guide

- Page 211 and 212: 211 Guide

- Page 213 and 214: 213 Guide

- Page 215 and 216: 215 Guide

- Page 217 and 218: 217 Guide

- Page 219 and 220: 219 Guide

- Page 221 and 222: 221 Guide

- Page 223 and 224: 223 Guide

- Page 225 and 226: 225 Guide

- Page 227 and 228: 227 Guide

- Page 229 and 230: 229 Guide

- Page 231 and 232: 231 Guide

- Page 233 and 234: 233 Guide

- Page 235 and 236: 235 Guide

194<br />

<str<strong>on</strong>g>Guide</str<strong>on</strong>g> <str<strong>on</strong>g>to</str<strong>on</strong>g> <str<strong>on</strong>g>Us<strong>in</strong>g</str<strong>on</strong>g> <str<strong>on</strong>g>Internati<strong>on</strong>al</str<strong>on</strong>g> <str<strong>on</strong>g>Standards</str<strong>on</strong>g> <strong>on</strong> <strong>Audit<strong>in</strong>g</strong> <strong>in</strong> the Audits of Small- and Medium-Sized Entities Volume 1—Core C<strong>on</strong>cepts<br />

Documentati<strong>on</strong><br />

600.50<br />

Summarized Extracts from the Requirements Secti<strong>on</strong><br />

The group engagement team shall <strong>in</strong>clude <strong>in</strong> the audit documentati<strong>on</strong> the follow<strong>in</strong>g matters:<br />

• An analysis of comp<strong>on</strong>ents, <strong>in</strong>dicat<strong>in</strong>g those that are significant, and the type of<br />

work performed <strong>on</strong> the f<strong>in</strong>ancial <strong>in</strong>formati<strong>on</strong> of the comp<strong>on</strong>ents;<br />

• The nature, tim<strong>in</strong>g, and extent of the group engagement team’s <strong>in</strong>volvement <strong>in</strong> the<br />

work performed by the comp<strong>on</strong>ent audi<str<strong>on</strong>g>to</str<strong>on</strong>g>rs <strong>on</strong> significant comp<strong>on</strong>ents, <strong>in</strong>clud<strong>in</strong>g,<br />

where applicable, the group engagement team’s review of relevant parts of the<br />

comp<strong>on</strong>ent audi<str<strong>on</strong>g>to</str<strong>on</strong>g>rs’ audit documentati<strong>on</strong> and c<strong>on</strong>clusi<strong>on</strong>s there<strong>on</strong>; and<br />

• Written communicati<strong>on</strong>s between the group engagement team and the<br />

comp<strong>on</strong>ent audi<str<strong>on</strong>g>to</str<strong>on</strong>g>rs about the group engagement team’s requirements.<br />

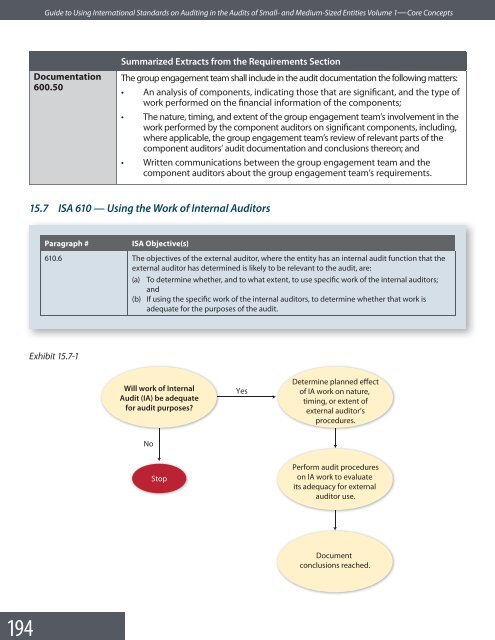

15.7 ISA 610 — <str<strong>on</strong>g>Us<strong>in</strong>g</str<strong>on</strong>g> the Work of Internal Audi<str<strong>on</strong>g>to</str<strong>on</strong>g>rs<br />

Paragraph #<br />

ISA Objective(s)<br />

610.6 The objectives of the external audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r, where the entity has an <strong>in</strong>ternal audit functi<strong>on</strong> that the<br />

external audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r has determ<strong>in</strong>ed is likely <str<strong>on</strong>g>to</str<strong>on</strong>g> be relevant <str<strong>on</strong>g>to</str<strong>on</strong>g> the audit, are:<br />

(a) To determ<strong>in</strong>e whether, and <str<strong>on</strong>g>to</str<strong>on</strong>g> what extent, <str<strong>on</strong>g>to</str<strong>on</strong>g> use specific work of the <strong>in</strong>ternal audi<str<strong>on</strong>g>to</str<strong>on</strong>g>rs;<br />

and<br />

(b) If us<strong>in</strong>g the specific work of the <strong>in</strong>ternal audi<str<strong>on</strong>g>to</str<strong>on</strong>g>rs, <str<strong>on</strong>g>to</str<strong>on</strong>g> determ<strong>in</strong>e whether that work is<br />

adequate for the purposes of the audit.<br />

Exhibit 15.7-1<br />

Will work of Internal<br />

Audit (IA) be adequate<br />

for audit purposes?<br />

Yes<br />

Determ<strong>in</strong>e planned effect<br />

of IA work <strong>on</strong> nature,<br />

tim<strong>in</strong>g, or extent of<br />

external audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r’s<br />

procedures.<br />

No<br />

S<str<strong>on</strong>g>to</str<strong>on</strong>g>p<br />

Perform audit procedures<br />

<strong>on</strong> IA work <str<strong>on</strong>g>to</str<strong>on</strong>g> evaluate<br />

its adequacy for external<br />

audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r use.<br />

Document<br />

c<strong>on</strong>clusi<strong>on</strong>s reached.