Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

168<br />

<str<strong>on</strong>g>Guide</str<strong>on</strong>g> <str<strong>on</strong>g>to</str<strong>on</strong>g> <str<strong>on</strong>g>Us<strong>in</strong>g</str<strong>on</strong>g> <str<strong>on</strong>g>Internati<strong>on</strong>al</str<strong>on</strong>g> <str<strong>on</strong>g>Standards</str<strong>on</strong>g> <strong>on</strong> <strong>Audit<strong>in</strong>g</strong> <strong>in</strong> the Audits of Small- and Medium-Sized Entities Volume 1—Core C<strong>on</strong>cepts<br />

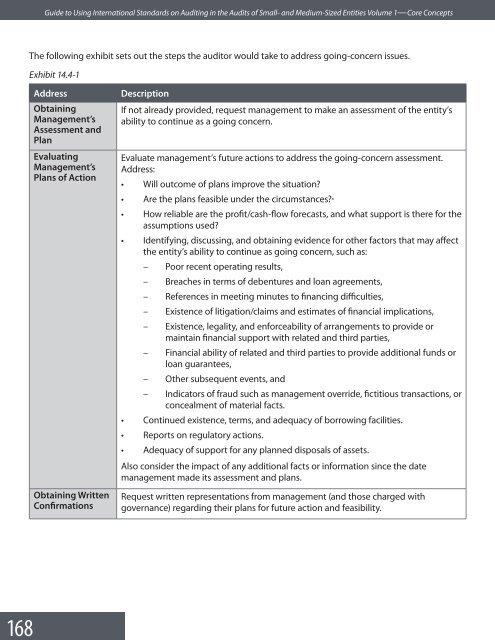

The follow<strong>in</strong>g exhibit sets out the steps the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r would take <str<strong>on</strong>g>to</str<strong>on</strong>g> address go<strong>in</strong>g-c<strong>on</strong>cern issues.<br />

Exhibit 14.4-1<br />

Address<br />

Obta<strong>in</strong><strong>in</strong>g<br />

Management’s<br />

Assessment and<br />

Plan<br />

Evaluat<strong>in</strong>g<br />

Management’s<br />

Plans of Acti<strong>on</strong><br />

Obta<strong>in</strong><strong>in</strong>g Written<br />

C<strong>on</strong>firmati<strong>on</strong>s<br />

Descripti<strong>on</strong><br />

If not already provided, request management <str<strong>on</strong>g>to</str<strong>on</strong>g> make an assessment of the entity’s<br />

ability <str<strong>on</strong>g>to</str<strong>on</strong>g> c<strong>on</strong>t<strong>in</strong>ue as a go<strong>in</strong>g c<strong>on</strong>cern.<br />

Evaluate management’s future acti<strong>on</strong>s <str<strong>on</strong>g>to</str<strong>on</strong>g> address the go<strong>in</strong>g-c<strong>on</strong>cern assessment.<br />

Address:<br />

• Will outcome of plans improve the situati<strong>on</strong>?<br />

• Are the plans feasible under the circumstances?<br />

• How reliable are the profit/cash-flow forecasts, and what support is there for the<br />

assumpti<strong>on</strong>s used?<br />

• Identify<strong>in</strong>g, discuss<strong>in</strong>g, and obta<strong>in</strong><strong>in</strong>g evidence for other fac<str<strong>on</strong>g>to</str<strong>on</strong>g>rs that may affect<br />

the entity’s ability <str<strong>on</strong>g>to</str<strong>on</strong>g> c<strong>on</strong>t<strong>in</strong>ue as go<strong>in</strong>g c<strong>on</strong>cern, such as:<br />

– Poor recent operat<strong>in</strong>g results,<br />

– Breaches <strong>in</strong> terms of debentures and loan agreements,<br />

– References <strong>in</strong> meet<strong>in</strong>g m<strong>in</strong>utes <str<strong>on</strong>g>to</str<strong>on</strong>g> f<strong>in</strong>anc<strong>in</strong>g difficulties,<br />

– Existence of litigati<strong>on</strong>/claims and estimates of f<strong>in</strong>ancial implicati<strong>on</strong>s,<br />

– Existence, legality, and enforceability of arrangements <str<strong>on</strong>g>to</str<strong>on</strong>g> provide or<br />

ma<strong>in</strong>ta<strong>in</strong> f<strong>in</strong>ancial support with related and third parties,<br />

– F<strong>in</strong>ancial ability of related and third parties <str<strong>on</strong>g>to</str<strong>on</strong>g> provide additi<strong>on</strong>al funds or<br />

loan guarantees,<br />

– Other subsequent events, and<br />

– Indica<str<strong>on</strong>g>to</str<strong>on</strong>g>rs of fraud such as management override, fictitious transacti<strong>on</strong>s, or<br />

c<strong>on</strong>cealment of material facts.<br />

• C<strong>on</strong>t<strong>in</strong>ued existence, terms, and adequacy of borrow<strong>in</strong>g facilities.<br />

• Reports <strong>on</strong> regula<str<strong>on</strong>g>to</str<strong>on</strong>g>ry acti<strong>on</strong>s.<br />

• Adequacy of support for any planned disposals of assets.<br />

Also c<strong>on</strong>sider the impact of any additi<strong>on</strong>al facts or <strong>in</strong>formati<strong>on</strong> s<strong>in</strong>ce the date<br />

management made its assessment and plans.<br />

Request written representati<strong>on</strong>s from management (and those charged with<br />

governance) regard<strong>in</strong>g their plans for future acti<strong>on</strong> and feasibility.