Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

141<br />

<str<strong>on</strong>g>Guide</str<strong>on</strong>g> <str<strong>on</strong>g>to</str<strong>on</strong>g> <str<strong>on</strong>g>Us<strong>in</strong>g</str<strong>on</strong>g> <str<strong>on</strong>g>Internati<strong>on</strong>al</str<strong>on</strong>g> <str<strong>on</strong>g>Standards</str<strong>on</strong>g> <strong>on</strong> <strong>Audit<strong>in</strong>g</strong> <strong>in</strong> the Audits of Small- and Medium-Sized Entities Volume 1—Core C<strong>on</strong>cepts<br />

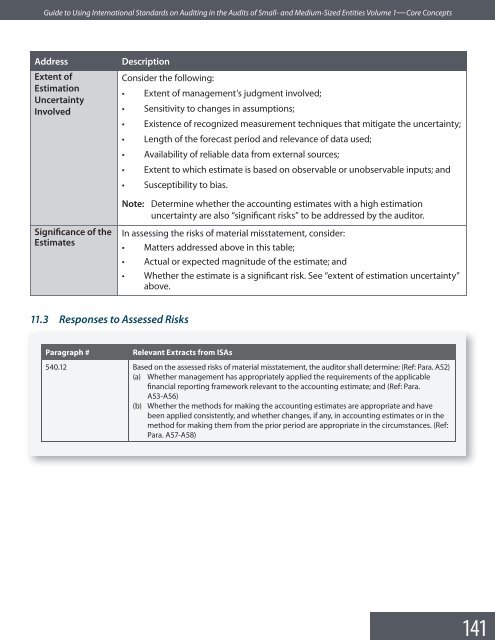

Address<br />

Extent of<br />

Estimati<strong>on</strong><br />

Uncerta<strong>in</strong>ty<br />

Involved<br />

Descripti<strong>on</strong><br />

C<strong>on</strong>sider the follow<strong>in</strong>g:<br />

• Extent of management’s judgment <strong>in</strong>volved;<br />

• Sensitivity <str<strong>on</strong>g>to</str<strong>on</strong>g> changes <strong>in</strong> assumpti<strong>on</strong>s;<br />

• Existence of recognized measurement techniques that mitigate the uncerta<strong>in</strong>ty;<br />

• Length of the forecast period and relevance of data used;<br />

• Availability of reliable data from external sources;<br />

• Extent <str<strong>on</strong>g>to</str<strong>on</strong>g> which estimate is based <strong>on</strong> observable or unobservable <strong>in</strong>puts; and<br />

• Susceptibility <str<strong>on</strong>g>to</str<strong>on</strong>g> bias.<br />

Note: Determ<strong>in</strong>e whether the account<strong>in</strong>g estimates with a high estimati<strong>on</strong><br />

uncerta<strong>in</strong>ty are also “significant risks” <str<strong>on</strong>g>to</str<strong>on</strong>g> be addressed by the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r.<br />

Significance of the<br />

Estimates<br />

In assess<strong>in</strong>g the risks of material misstatement, c<strong>on</strong>sider:<br />

• Matters addressed above <strong>in</strong> this table;<br />

• Actual or expected magnitude of the estimate; and<br />

• Whether the estimate is a significant risk. See “extent of estimati<strong>on</strong> uncerta<strong>in</strong>ty”<br />

above.<br />

11.3 Resp<strong>on</strong>ses <str<strong>on</strong>g>to</str<strong>on</strong>g> Assessed Risks<br />

Paragraph #<br />

Relevant Extracts from ISAs<br />

540.12 Based <strong>on</strong> the assessed risks of material misstatement, the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r shall determ<strong>in</strong>e: (Ref: Para. A52)<br />

(a) Whether management has appropriately applied the requirements of the applicable<br />

f<strong>in</strong>ancial report<strong>in</strong>g framework relevant <str<strong>on</strong>g>to</str<strong>on</strong>g> the account<strong>in</strong>g estimate; and (Ref: Para.<br />

A53-A56)<br />

(b) Whether the methods for mak<strong>in</strong>g the account<strong>in</strong>g estimates are appropriate and have<br />

been applied c<strong>on</strong>sistently, and whether changes, if any, <strong>in</strong> account<strong>in</strong>g estimates or <strong>in</strong> the<br />

method for mak<strong>in</strong>g them from the prior period are appropriate <strong>in</strong> the circumstances. (Ref:<br />

Para. A57-A58)