Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

140<br />

<str<strong>on</strong>g>Guide</str<strong>on</strong>g> <str<strong>on</strong>g>to</str<strong>on</strong>g> <str<strong>on</strong>g>Us<strong>in</strong>g</str<strong>on</strong>g> <str<strong>on</strong>g>Internati<strong>on</strong>al</str<strong>on</strong>g> <str<strong>on</strong>g>Standards</str<strong>on</strong>g> <strong>on</strong> <strong>Audit<strong>in</strong>g</strong> <strong>in</strong> the Audits of Small- and Medium-Sized Entities Volume 1—Core C<strong>on</strong>cepts<br />

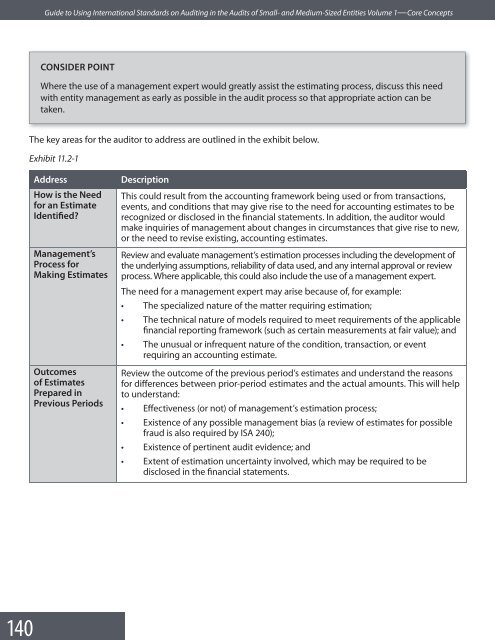

CONSIDER POINT<br />

Where the use of a management expert would greatly assist the estimat<strong>in</strong>g process, discuss this need<br />

with entity management as early as possible <strong>in</strong> the audit process so that appropriate acti<strong>on</strong> can be<br />

taken.<br />

The key areas for the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r <str<strong>on</strong>g>to</str<strong>on</strong>g> address are outl<strong>in</strong>ed <strong>in</strong> the exhibit below.<br />

Exhibit 11.2-1<br />

Address<br />

How is the Need<br />

for an Estimate<br />

Identified?<br />

Management’s<br />

Process for<br />

Mak<strong>in</strong>g Estimates<br />

Outcomes<br />

of Estimates<br />

Prepared <strong>in</strong><br />

Previous Periods<br />

Descripti<strong>on</strong><br />

This could result from the account<strong>in</strong>g framework be<strong>in</strong>g used or from transacti<strong>on</strong>s,<br />

events, and c<strong>on</strong>diti<strong>on</strong>s that may give rise <str<strong>on</strong>g>to</str<strong>on</strong>g> the need for account<strong>in</strong>g estimates <str<strong>on</strong>g>to</str<strong>on</strong>g> be<br />

recognized or disclosed <strong>in</strong> the f<strong>in</strong>ancial statements. In additi<strong>on</strong>, the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r would<br />

make <strong>in</strong>quiries of management about changes <strong>in</strong> circumstances that give rise <str<strong>on</strong>g>to</str<strong>on</strong>g> new,<br />

or the need <str<strong>on</strong>g>to</str<strong>on</strong>g> revise exist<strong>in</strong>g, account<strong>in</strong>g estimates.<br />

Review and evaluate management’s estimati<strong>on</strong> processes <strong>in</strong>clud<strong>in</strong>g the development of<br />

the underly<strong>in</strong>g assumpti<strong>on</strong>s, reliability of data used, and any <strong>in</strong>ternal approval or review<br />

process. Where applicable, this could also <strong>in</strong>clude the use of a management expert.<br />

The need for a management expert may arise because of, for example:<br />

• The specialized nature of the matter requir<strong>in</strong>g estimati<strong>on</strong>;<br />

• The technical nature of models required <str<strong>on</strong>g>to</str<strong>on</strong>g> meet requirements of the applicable<br />

f<strong>in</strong>ancial report<strong>in</strong>g framework (such as certa<strong>in</strong> measurements at fair value); and<br />

• The unusual or <strong>in</strong>frequent nature of the c<strong>on</strong>diti<strong>on</strong>, transacti<strong>on</strong>, or event<br />

requir<strong>in</strong>g an account<strong>in</strong>g estimate.<br />

Review the outcome of the previous period’s estimates and understand the reas<strong>on</strong>s<br />

for differences between prior-period estimates and the actual amounts. This will help<br />

<str<strong>on</strong>g>to</str<strong>on</strong>g> understand:<br />

• Effectiveness (or not) of management’s estimati<strong>on</strong> process;<br />

• Existence of any possible management bias (a review of estimates for possible<br />

fraud is also required by ISA 240);<br />

• Existence of pert<strong>in</strong>ent audit evidence; and<br />

• Extent of estimati<strong>on</strong> uncerta<strong>in</strong>ty <strong>in</strong>volved, which may be required <str<strong>on</strong>g>to</str<strong>on</strong>g> be<br />

disclosed <strong>in</strong> the f<strong>in</strong>ancial statements.