Guide to Using International Standards on Auditing in - IFAC

Guide to Using International Standards on Auditing in - IFAC Guide to Using International Standards on Auditing in - IFAC

124

125

- Page 73 and 74: 73 Guide t

- Page 75 and 76: 75 Guide t

- Page 77 and 78: 77 6. Financial Statement Assertion

- Page 79 and 80: 79 Guide t

- Page 81 and 82: 81 Guide t

- Page 83 and 84: 83 Guide t

- Page 85 and 86: 85 Guide t

- Page 87 and 88: 87 Guide t

- Page 89 and 90: 89 Guide t

- Page 91 and 92: 91 Guide t

- Page 93 and 94: 93 Guide t

- Page 95 and 96: 95 Guide t

- Page 97 and 98: 97 Guide t

- Page 99 and 100: 99 Guide t

- Page 101 and 102: 101 Guide

- Page 103 and 104: 103 Guide

- Page 105 and 106: 105 Guide

- Page 107 and 108: 107 Guide

- Page 109 and 110: 109 Guide

- Page 111 and 112: 111 Guide

- Page 113 and 114: 113 Guide

- Page 115 and 116: 115 10. Further Audit Procedures Ch

- Page 117 and 118: 117 Guide

- Page 119 and 120: 119 Guide

- Page 121 and 122: 121 Guide

- Page 123: 123 Guide

- Page 127 and 128: 127 Guide

- Page 129 and 130: 129 Guide

- Page 131 and 132: 131 Guide

- Page 133 and 134: 133 Guide

- Page 135 and 136: 135 Guide

- Page 137 and 138: 137 Guide

- Page 139 and 140: 139 Guide

- Page 141 and 142: 141 Guide

- Page 143 and 144: 143 Guide

- Page 145 and 146: 145 12. Related Parties Chapter Con

- Page 147 and 148: 147 Guide

- Page 149 and 150: 149 Guide

- Page 151 and 152: 151 Guide

- Page 153 and 154: 153 Guide

- Page 155 and 156: 155 Guide

- Page 157 and 158: 157 Guide

- Page 159 and 160: 159 Guide

- Page 161 and 162: 161 14. Going Concern Chapter Conte

- Page 163 and 164: 163 Guide

- Page 165 and 166: 165 Guide

- Page 167 and 168: 167 Guide

- Page 169 and 170: 169 Guide

- Page 171 and 172: 171 15. Summary of Other ISA Requir

- Page 173 and 174: 173 Guide

124<br />

<str<strong>on</strong>g>Guide</str<strong>on</strong>g> <str<strong>on</strong>g>to</str<strong>on</strong>g> <str<strong>on</strong>g>Us<strong>in</strong>g</str<strong>on</strong>g> <str<strong>on</strong>g>Internati<strong>on</strong>al</str<strong>on</strong>g> <str<strong>on</strong>g>Standards</str<strong>on</strong>g> <strong>on</strong> <strong>Audit<strong>in</strong>g</strong> <strong>in</strong> the Audits of Small- and Medium-Sized Entities Volume 1—Core C<strong>on</strong>cepts<br />

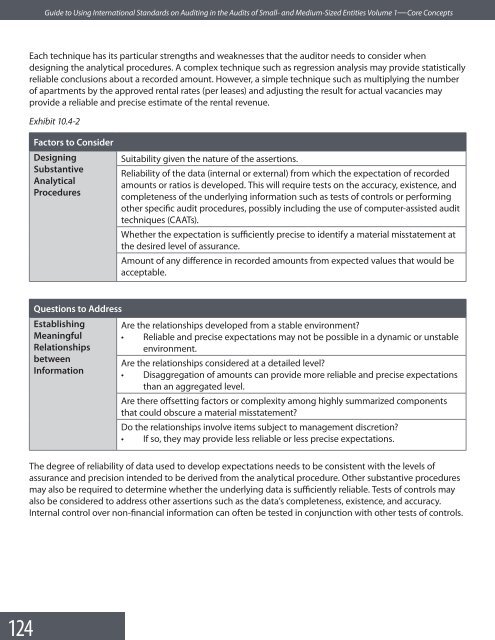

Each technique has its particular strengths and weaknesses that the audi<str<strong>on</strong>g>to</str<strong>on</strong>g>r needs <str<strong>on</strong>g>to</str<strong>on</strong>g> c<strong>on</strong>sider when<br />

design<strong>in</strong>g the analytical procedures. A complex technique such as regressi<strong>on</strong> analysis may provide statistically<br />

reliable c<strong>on</strong>clusi<strong>on</strong>s about a recorded amount. However, a simple technique such as multiply<strong>in</strong>g the number<br />

of apartments by the approved rental rates (per leases) and adjust<strong>in</strong>g the result for actual vacancies may<br />

provide a reliable and precise estimate of the rental revenue.<br />

Exhibit 10.4-2<br />

Fac<str<strong>on</strong>g>to</str<strong>on</strong>g>rs <str<strong>on</strong>g>to</str<strong>on</strong>g> C<strong>on</strong>sider<br />

Design<strong>in</strong>g<br />

Substantive<br />

Analytical<br />

Procedures<br />

Suitability given the nature of the asserti<strong>on</strong>s.<br />

Reliability of the data (<strong>in</strong>ternal or external) from which the expectati<strong>on</strong> of recorded<br />

amounts or ratios is developed. This will require tests <strong>on</strong> the accuracy, existence, and<br />

completeness of the underly<strong>in</strong>g <strong>in</strong>formati<strong>on</strong> such as tests of c<strong>on</strong>trols or perform<strong>in</strong>g<br />

other specific audit procedures, possibly <strong>in</strong>clud<strong>in</strong>g the use of computer-assisted audit<br />

techniques (CAATs).<br />

Whether the expectati<strong>on</strong> is sufficiently precise <str<strong>on</strong>g>to</str<strong>on</strong>g> identify a material misstatement at<br />

the desired level of assurance.<br />

Amount of any difference <strong>in</strong> recorded amounts from expected values that would be<br />

acceptable.<br />

Questi<strong>on</strong>s <str<strong>on</strong>g>to</str<strong>on</strong>g> Address<br />

Establish<strong>in</strong>g<br />

Mean<strong>in</strong>gful<br />

Relati<strong>on</strong>ships<br />

between<br />

Informati<strong>on</strong><br />

Are the relati<strong>on</strong>ships developed from a stable envir<strong>on</strong>ment?<br />

• Reliable and precise expectati<strong>on</strong>s may not be possible <strong>in</strong> a dynamic or unstable<br />

envir<strong>on</strong>ment.<br />

Are the relati<strong>on</strong>ships c<strong>on</strong>sidered at a detailed level?<br />

• Disaggregati<strong>on</strong> of amounts can provide more reliable and precise expectati<strong>on</strong>s<br />

than an aggregated level.<br />

Are there offsett<strong>in</strong>g fac<str<strong>on</strong>g>to</str<strong>on</strong>g>rs or complexity am<strong>on</strong>g highly summarized comp<strong>on</strong>ents<br />

that could obscure a material misstatement?<br />

Do the relati<strong>on</strong>ships <strong>in</strong>volve items subject <str<strong>on</strong>g>to</str<strong>on</strong>g> management discreti<strong>on</strong>?<br />

• If so, they may provide less reliable or less precise expectati<strong>on</strong>s.<br />

The degree of reliability of data used <str<strong>on</strong>g>to</str<strong>on</strong>g> develop expectati<strong>on</strong>s needs <str<strong>on</strong>g>to</str<strong>on</strong>g> be c<strong>on</strong>sistent with the levels of<br />

assurance and precisi<strong>on</strong> <strong>in</strong>tended <str<strong>on</strong>g>to</str<strong>on</strong>g> be derived from the analytical procedure. Other substantive procedures<br />

may also be required <str<strong>on</strong>g>to</str<strong>on</strong>g> determ<strong>in</strong>e whether the underly<strong>in</strong>g data is sufficiently reliable. Tests of c<strong>on</strong>trols may<br />

also be c<strong>on</strong>sidered <str<strong>on</strong>g>to</str<strong>on</strong>g> address other asserti<strong>on</strong>s such as the data’s completeness, existence, and accuracy.<br />

Internal c<strong>on</strong>trol over n<strong>on</strong>-f<strong>in</strong>ancial <strong>in</strong>formati<strong>on</strong> can often be tested <strong>in</strong> c<strong>on</strong>juncti<strong>on</strong> with other tests of c<strong>on</strong>trols.