Presentation - Italcementi Group

Presentation - Italcementi Group

Presentation - Italcementi Group

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

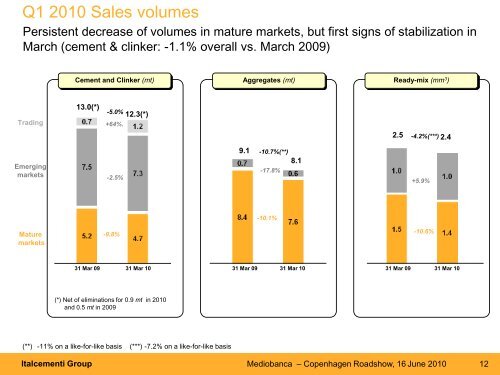

Q1 2010 Sales volumes<br />

Persistent decrease of volumes in mature markets, but first signs of stabilization in<br />

March (cement & clinker: -1.1% overall vs. March 2009)<br />

Cement and Clinker (mt)<br />

Aggregates (mt)<br />

Ready-mix (mm 3 )<br />

Trading<br />

13.0(*)<br />

-5.0%<br />

+64%.<br />

12.3(*)<br />

2.5 -4.2%(***) 2.4<br />

Emerging<br />

markets<br />

-2.5%<br />

9.1 -10.7%(**)<br />

-17.8%<br />

8.1<br />

+5.9%<br />

-10.1%<br />

Mature<br />

markets<br />

-9.8%<br />

-10.6%<br />

31 Mar 09 31 Mar 10<br />

31 Mar 09 31 Mar 10<br />

31 Mar 09 31 Mar 10<br />

(*) Net of eliminations for 0.9 mt in 2010<br />

and 0.5 mt in 2009<br />

(**) -11% on a like-for-like basis<br />

(***) -7.2% on a like-for-like basis<br />

<strong>Italcementi</strong> <strong>Group</strong> Mediobanca – Copenhagen Roadshow, 16 June 2010<br />

12