A Guide to HMDA Reporting - ffiec

A Guide to HMDA Reporting - ffiec

A Guide to HMDA Reporting - ffiec

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

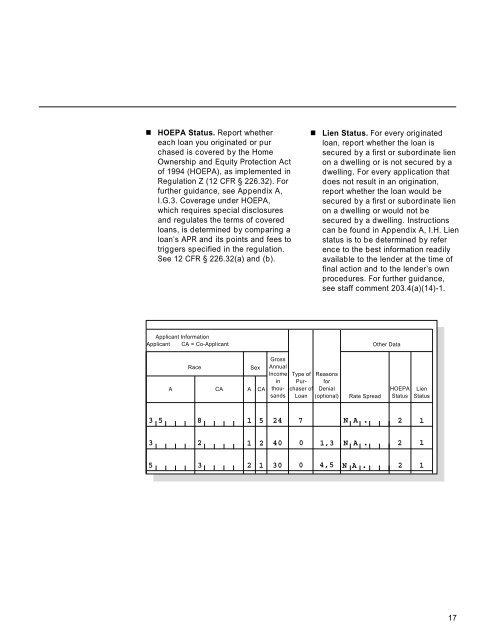

¢ HOEPA Status. Report whether<br />

each loan you originated or purchased<br />

is covered by the Home<br />

Ownership and Equity Protection Act<br />

of 1994 (HOEPA), as implemented in<br />

Regulation Z (12 CFR § 226.32). For<br />

further guidance, see Appendix A,<br />

I.G.3. Coverage under HOEPA,<br />

which requires special disclosures<br />

and regulates the terms of covered<br />

loans, is determined by comparing a<br />

loan’s APR and its points and fees <strong>to</strong><br />

triggers specified in the regulation.<br />

See 12 CFR § 226.32(a) and (b).<br />

¢ Lien Status. For every originated<br />

loan, report whether the loan is<br />

secured by a first or subordinate lien<br />

on a dwelling or is not secured by a<br />

dwelling. For every application that<br />

does not result in an origination,<br />

report whether the loan would be<br />

secured by a first or subordinate lien<br />

on a dwelling or would not be<br />

secured by a dwelling. Instructions<br />

can be found in Appendix A, I.H. Lien<br />

status is <strong>to</strong> be determined by reference<br />

<strong>to</strong> the best information readily<br />

available <strong>to</strong> the lender at the time of<br />

final action and <strong>to</strong> the lender’s own<br />

procedures. For further guidance,<br />

see staff comment 203.4(a)(14)-1.<br />

Applicant Information<br />

A = Applicant CA = Co-Applicant Other Data<br />

A<br />

Race<br />

Sex<br />

CA A CA<br />

Gross<br />

Annual<br />

Income<br />

in<br />

thousands<br />

Type of<br />

Pur<br />

chaser of<br />

Loan<br />

Reasons<br />

for<br />

Denial<br />

(optional) Rate Spread<br />

HOEPA<br />

Status<br />

3 5 8 1 5 24 7 N A . 2 1<br />

3 2 1 2 40 0 1,3 N A . 2 1<br />

5 3 2 1 30 0 4,5 N A . 2 1<br />

Lien<br />

Status<br />

17