Comprehensive Annual Financial Report - Minnesota State ...

Comprehensive Annual Financial Report - Minnesota State ...

Comprehensive Annual Financial Report - Minnesota State ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

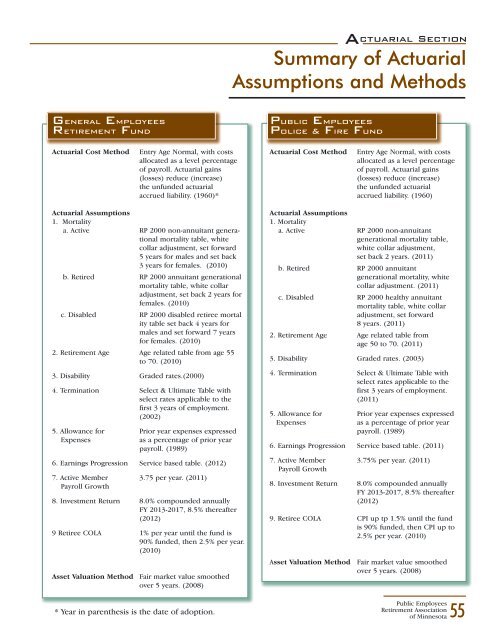

General Employees<br />

Retirement Fund<br />

Actuarial Cost Method Entry Age Normal, with costs<br />

allocated as a level percentage<br />

of payroll. Actuarial gains<br />

(losses) reduce (increase)<br />

the unfunded actuarial<br />

accrued liability. (1960)*<br />

Actuarial Assumptions<br />

1. Mortality<br />

a. Active RP 2000 non-annuitant generational<br />

mortality table, white<br />

collar adjustment, set forward<br />

5 years for males and set back<br />

3 years for females. (2010)<br />

b. Retired RP 2000 annuitant generational<br />

mortality table, white collar<br />

adjustment, set back 2 years for<br />

females. (2010)<br />

c. Disabled RP 2000 disabled retiree mortal<br />

ity table set back 4 years for<br />

males and set forward 7 years<br />

for females. (2010)<br />

2. Retirement Age Age related table from age 55<br />

to 70. (2010)<br />

3. Disability Graded rates.(2000)<br />

4. Termination Select & Ultimate Table with<br />

select rates applicable to the<br />

first 3 years of employment.<br />

(2002)<br />

5. Allowance for Prior year expenses expressed<br />

Expenses as a percentage of prior year<br />

payroll. (1989)<br />

6. Earnings Progression Service based table. (2012)<br />

7. Active Member 3.75 per year. (2011)<br />

Payroll Growth<br />

8. Investment Return 8.0% compounded annually<br />

FY 2013-2017, 8.5% thereafter<br />

(2012)<br />

9 Retiree COLA 1% per year until the fund is<br />

90% funded, then 2.5% per year.<br />

(2010)<br />

Asset Valuation Method Fair market value smoothed<br />

over 5 years. (2008)<br />

* Year in parenthesis is the date of adoption.<br />

Actuarial Section<br />

Summary of Actuarial<br />

Assumptions and Methods<br />

Public Employees<br />

Police & Fire Fund<br />

Actuarial Cost Method Entry Age Normal, with costs<br />

allocated as a level percentage<br />

of payroll. Actuarial gains<br />

(losses) reduce (increase)<br />

the unfunded actuarial<br />

accrued liability. (1960)<br />

Actuarial Assumptions<br />

1. Mortality<br />

a. Active RP 2000 non-annuitant<br />

generational mortality table,<br />

white collar adjustment,<br />

set back 2 years. (2011)<br />

b. Retired RP 2000 annuitant<br />

generational mortality, white<br />

collar adjustment. (2011)<br />

c. Disabled RP 2000 healthy annuitant<br />

mortality table, white collar<br />

adjustment, set forward<br />

8 years. (2011)<br />

2. Retirement Age Age related table from<br />

age 50 to 70. (2011)<br />

3. Disability Graded rates. (2003)<br />

4. Termination Select & Ultimate Table with<br />

select rates applicable to the<br />

first 3 years of employment.<br />

(2011)<br />

5. Allowance for Prior year expenses expressed<br />

Expenses as a percentage of prior year<br />

payroll. (1989)<br />

6. Earnings Progression Service based table. (2011)<br />

7. Active Member 3.75% per year. (2011)<br />

Payroll Growth<br />

8. Investment Return 8.0% compounded annually<br />

FY 2013-2017, 8.5% thereafter<br />

(2012)<br />

9. Retiree COLA CPI up tp 1.5% until the fund<br />

is 90% funded, then CPI up to<br />

2.5% per year. (2010)<br />

Asset Valuation Method Fair market value smoothed<br />

over 5 years. (2008)<br />

Public Employees<br />

Retirement Association<br />

of <strong>Minnesota</strong><br />

55