Regulation of Fuels and Fuel Additives: Renewable Fuel Standard ...

Regulation of Fuels and Fuel Additives: Renewable Fuel Standard ...

Regulation of Fuels and Fuel Additives: Renewable Fuel Standard ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

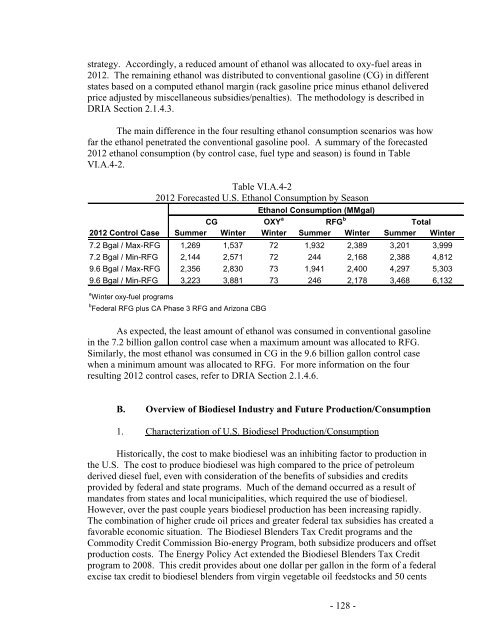

strategy. Accordingly, a reduced amount <strong>of</strong> ethanol was allocated to oxy-fuel areas in<br />

2012. The remaining ethanol was distributed to conventional gasoline (CG) in different<br />

states based on a computed ethanol margin (rack gasoline price minus ethanol delivered<br />

price adjusted by miscellaneous subsidies/penalties). The methodology is described in<br />

DRIA Section 2.1.4.3.<br />

The main difference in the four resulting ethanol consumption scenarios was how<br />

far the ethanol penetrated the conventional gasoline pool. A summary <strong>of</strong> the forecasted<br />

2012 ethanol consumption (by control case, fuel type <strong>and</strong> season) is found in Table<br />

VI.A.4-2.<br />

Table VI.A.4-2<br />

2012 Forecasted U.S. Ethanol Consumption by Season<br />

OXY a<br />

CG RFG<br />

2012 Control Case Summer Winter Winter Summer Winter Summer Winter<br />

7.2 Bgal / Max-RFG 1,269 1,537 72 1,932 2,389 3,201 3,999<br />

7.2 Bgal / Min-RFG 2,144 2,571 72 244 2,168 2,388 4,812<br />

9.6 Bgal / Max-RFG 2,356 2,830 73 1,941 2,400 4,297 5,303<br />

9.6 Bgal / Min-RFG 3,223 3,881 73 246 2,178 3,468 6,132<br />

b<br />

Ethanol Consumption (MMgal)<br />

Total<br />

a<br />

Winter oxy-fuel programs<br />

b<br />

Federal RFG plus CA Phase 3 RFG <strong>and</strong> Arizona CBG<br />

As expected, the least amount <strong>of</strong> ethanol was consumed in conventional gasoline<br />

in the 7.2 billion gallon control case when a maximum amount was allocated to RFG.<br />

Similarly, the most ethanol was consumed in CG in the 9.6 billion gallon control case<br />

when a minimum amount was allocated to RFG. For more information on the four<br />

resulting 2012 control cases, refer to DRIA Section 2.1.4.6.<br />

B. Overview <strong>of</strong> Biodiesel Industry <strong>and</strong> Future Production/Consumption<br />

1. Characterization <strong>of</strong> U.S. Biodiesel Production/Consumption<br />

Historically, the cost to make biodiesel was an inhibiting factor to production in<br />

the U.S. The cost to produce biodiesel was high compared to the price <strong>of</strong> petroleum<br />

derived diesel fuel, even with consideration <strong>of</strong> the benefits <strong>of</strong> subsidies <strong>and</strong> credits<br />

provided by federal <strong>and</strong> state programs. Much <strong>of</strong> the dem<strong>and</strong> occurred as a result <strong>of</strong><br />

m<strong>and</strong>ates from states <strong>and</strong> local municipalities, which required the use <strong>of</strong> biodiesel.<br />

However, over the past couple years biodiesel production has been increasing rapidly.<br />

The combination <strong>of</strong> higher crude oil prices <strong>and</strong> greater federal tax subsidies has created a<br />

favorable economic situation. The Biodiesel Blenders Tax Credit programs <strong>and</strong> the<br />

Commodity Credit Commission Bio-energy Program, both subsidize producers <strong>and</strong> <strong>of</strong>fset<br />

production costs. The Energy Policy Act extended the Biodiesel Blenders Tax Credit<br />

program to 2008. This credit provides about one dollar per gallon in the form <strong>of</strong> a federal<br />

excise tax credit to biodiesel blenders from virgin vegetable oil feedstocks <strong>and</strong> 50 cents<br />

- 128 -