City Corporate Plan - Municipal

City Corporate Plan - Municipal

City Corporate Plan - Municipal

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Tamil Nadu Urban Infrastructure Financial Services Limited (TNUIFSL)<br />

Final Report<br />

Conversion of <strong>City</strong> <strong>Corporate</strong> <strong>Plan</strong> to Business <strong>Plan</strong> for<br />

Mayiladuthurai municipality<br />

June 2007<br />

ICRA Management Consulting Services Limited

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

Table of Contents<br />

1. Introduction ___________________________________________________________ 1<br />

1.1 Background to the study ____________________________________________________ 1<br />

1.2 Scope of work ___________________________________________________________ 1<br />

1.3 IMaCS approach to the study ________________________________________________ 1<br />

1.4 Structure of the report _____________________________________________________ 2<br />

2. Mayiladuthurai - a brief profile ___________________________________________ 3<br />

2.1 Location and connectivity __________________________________________________ 3<br />

2.2 Social and demographic characteristics ________________________________________ 3<br />

2.3 Economic Development ____________________________________________________ 4<br />

2.4 Land use management _____________________________________________________ 5<br />

2.5 Strategy for development ___________________________________________________ 5<br />

3. Review of operating performance __________________________________________ 7<br />

3.1 Water Supply ____________________________________________________________ 7<br />

3.2 Sanitation _______________________________________________________________ 8<br />

3.3 Storm water drains ________________________________________________________ 8<br />

3.4 Solid Waste Management___________________________________________________ 9<br />

3.5 Roads __________________________________________________________________ 9<br />

3.6 Street lights ____________________________________________________________ 10<br />

3.7 Bus stands _____________________________________________________________ 10<br />

3.8 Capital Investment <strong>Plan</strong> ___________________________________________________ 10<br />

4. Analysis of financial performance ________________________________________ 12<br />

4.1 Income and Expenditure summary of MyM ____________________________________ 12<br />

4.2 Revenue streams of ULB in Tamil Nadu ______________________________________ 12<br />

4.3 Revenues ______________________________________________________________ 13<br />

4.4 Analysis of Costs ________________________________________________________ 17<br />

5. Potential areas for improvement _________________________________________ 20<br />

5.1 Public private partnerships (PPP) ____________________________________________ 20<br />

5.2 Potential for revenue enhancement___________________________________________ 20<br />

5.3 Measures for cost management _____________________________________________ 23<br />

5.4 Other measures / interventions ______________________________________________ 24<br />

6. Business plan projections and investment capacity of MyM ___________________ 25<br />

6.1 Financial and Operating <strong>Plan</strong> – time horizon and scenarios ________________________ 25<br />

6.2 Basis and assumptions ____________________________________________________ 25<br />

6.3 Revenues ______________________________________________________________ 25<br />

6.4 Financial projections _____________________________________________________ 29<br />

6.5 Key results _____________________________________________________________ 30

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

List of Exhibits<br />

Exhibit 1.1 IMaCS approach to the study ............................................................................................................... 1<br />

Exhibit 2.1 Population trend................................................................................................................................... 3<br />

Exhibit 2.2 Land-use - 1996 and 2011 (proposed) ................................................................................................. 5<br />

Exhibit 3.1 Water supply ........................................................................................................................................ 7<br />

Exhibit 3.3 Sanitation facilities – ............................................................................................................................ 8<br />

Exhibit 3.4 Storm water drain network ................................................................................................................... 9<br />

Exhibit 3.5 Solid Waste Management - current status ............................................................................................ 9<br />

Exhibit 3.6 Road network ....................................................................................................................................... 9<br />

Exhibit 3.7 Existing Street Lighting Facilities ...................................................................................................... 10<br />

Exhibit 3.8 MyM - Felt needs (2006-15) ............................................................................................................... 11<br />

Exhibit 4.1 Income and Expenditure of MyM - Last five years ............................................................................. 12<br />

Exhibit 4.2 Revenue streams - ULBs in Tamil Nadu............................................................................................. 13<br />

Exhibit 4.3 Revenue trend ..................................................................................................................................... 13<br />

Exhibit 4.4 Property tax - analysis of key revenue drivers ................................................................................... 14<br />

Exhibit 4.5 Property Tax - breakup of assessees ................................................................................................. 15<br />

Exhibit 4.6 Professional Tax - revenue drivers .................................................................................................... 15<br />

Exhibit 4.7 Professional Tax – assessee break up ................................................................................................ 15<br />

Exhibit 4.8 Water charges - revenue drivers ........................................................................................................ 16<br />

Exhibit 4.9 Water charges - category wise connections and tariff ....................................................................... 16<br />

Exhibit 4.10 Costs - FY 2001 and FY 2004 .......................................................................................................... 17<br />

Exhibit 4.11 Power costs - Water & Sewerage and Street Lights ......................................................................... 18<br />

Exhibit 4.12 Loan Statement ................................................................................................................................. 18<br />

Exhibit 5.1 Key issues and suggested measures ................................................................................................... 21<br />

Exhibit 6.1 Assumptions for other income ............................................................................................................ 27<br />

Exhibit 6.2 Expenditure ........................................................................................................................................ 27<br />

Exhibit 6.3 Assumptions - Assets .......................................................................................................................... 28<br />

Exhibit 6.4: Loan Statement as on 30.09.2005 (Rs in lakhs) ................................................................................ 28<br />

Exhibit 6.5 New loans ........................................................................................................................................... 29<br />

Exhibit 6.6 Other Liabilities ................................................................................................................................. 29<br />

Exhibit 6.8 Income and Expenditure projections .................................................................................................. 30<br />

Exhibit 6.9 Summary of key results ....................................................................................................................... 30

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

List of abbreviations<br />

BOT Build –Operate –Transfer<br />

CAGR Cumulative Annual Growth Rate<br />

CIP Capital Investment Program<br />

CCP <strong>City</strong> <strong>Corporate</strong> <strong>Plan</strong><br />

FOP Financial and Operating <strong>Plan</strong><br />

GLR Ground Level Reservoir<br />

IMaCS ICRA Management Consulting Services<br />

LPCD Litres per capita per day<br />

MyM Mayiladuthurai municipality<br />

MSW <strong>Municipal</strong> Solid Waste<br />

NRCP National River Conservation Program<br />

OHT Over Head Tanks<br />

PPP Public Private Partnerships<br />

STP Sewerage Treatment <strong>Plan</strong>t<br />

SWM Solid Waste Management<br />

TNUDF Tamil Nadu Urban Development Fund<br />

TNUDP Tamil Nadu Urban Development Program<br />

TNUIFSL Tamil Nadu Urban Infrastructure Financial Services Limited<br />

UGD Under Ground Drainage

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

Executive Summary<br />

The Tamil Nadu Urban Infrastructure Financial Services (TNUIFSL) mandated ICRA Management<br />

Consulting Services (IMaCS) for conversion of <strong>City</strong> <strong>Corporate</strong> <strong>Plan</strong> (CCP) of Mayiladuthurai<br />

<strong>Municipal</strong>ity (MYM) into a Business <strong>Plan</strong>. The CCP for Mayiladuthurai was prepared in 2002, under<br />

the Tamil Nadu Urban Development Project - II (TNUDP-II) to develop vision, strategies and tasks to<br />

be carried out by MYM. Subsequently, MyM has prepared a Vision <strong>Plan</strong>, identifying various projects<br />

that it plans to undertake during 2004-09. The objective of this study is to enable effective<br />

implementation of projects envisaged in its CCP and Vision <strong>Plan</strong> through preparation of this report on<br />

conversion of the <strong>City</strong> <strong>Corporate</strong> <strong>Plan</strong> to a Business <strong>Plan</strong>.<br />

<strong>City</strong> profile and growth potential<br />

The population of Mayiladuthurai was 84,505 in 2001,<br />

implying a growth of 9.29 % over the population of 76,837<br />

in 1991. The population growth has slowed down during<br />

the last couple of decades, after double digit growth in the<br />

previous decades.<br />

As per Census 2001, the slum population in Mayiladuthurai was 13% of the population. However, the<br />

municipal data shows an increase in slum population and this is a major concern area for the<br />

municipal corporation. As per the Vision <strong>Plan</strong> of MyM, there were 26 slums with a total slum<br />

population of 16,434. Of these 23 slums have been provided with amenities. Mayiladuthurai is an<br />

industrially backward town and there is no major industry in this town.<br />

Being a temple town (the Mayuranathar Temple attracts pilgrims from other places), Mayiladuthurai a<br />

tourist centre. It is also strategically located in close proximity to the famous nine Navagraha temples.<br />

A number of important tourist places including Poompuhar, Mayuram, Tanquebar and Therazendur<br />

are in close proximity to the town. Since Mayiladuthurai has a good road and rail system, it acts as a<br />

halting junction for pilgrimages. The CCP points out that there is good scope for exploiting tourist<br />

potential. The CCP observes the need for initiatives for economic development and outlines following<br />

strategies for development.<br />

• Provision of food processing centre for fruit and milk products<br />

• Improvement of agro-processing industries around the town<br />

• Improvement of linkages of the town to other urban centres<br />

Parameter Details<br />

Population (2001) 84505<br />

Decadal Growth (1991-2001) 9.3%<br />

No. of Wards 36<br />

Sex Ratio 1012<br />

Literacy rate – 2001 80%<br />

• Provision of better facilities including lodging and boarding facilities for tourists.<br />

Additional areas that emerged based on consultation with Chairperson and select ward members on<br />

potential economic activities for the town include the need to create employment intensive investment<br />

including rice milling and tourism development. It was also suggested that the municipality along<br />

with the Tamil Nadu Slum Clearance Board should identify vacant/acquirable land areas within the<br />

municipal areas to create land parcels for industrial development and slum rehabilitation.

<strong>Municipal</strong> Services - Status assessment, gaps and actions being taken<br />

Exhibit 1 presents a summary of service levels and status with respect to select indicators in Water<br />

Supply, Sanitation, Transportation, Street lights and Solid Waste Management.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

Exhibit 1 - Status of <strong>Municipal</strong> services<br />

Sl. no Parameter / Indicator Value Issues and Gaps<br />

A. Water Supply<br />

1 Total Water Supply (MLD) 7.5 • Demand – Supply – MyM’s supply of 7.5 MLD<br />

2 Water Connections - nos. ~ 6300 corresponds to 90 LPCD which is in line with<br />

3 Public Fountains - nos. ~ 180<br />

•<br />

municipal norms.<br />

Pumping equipment requires upgrade from 120<br />

4 Daily Per Capita Supply (LPCD) 90<br />

kVA to 180 KVA. Additional borewells are also<br />

5 Storage Capacity / Daily Supply (%) 63% required to augment capacity.<br />

6 Pipe length / Road Length (%) 100%<br />

• Scope for adding water connections – Water<br />

7 Water connections / properties (%) 37%<br />

connections account for only about 37 % of the<br />

number of properties assessed and indicate the<br />

scope for adding more connections.<br />

• Poor collection efficiency - Current collection<br />

efficiency was only 65 % in FY 2005 and is a<br />

major cause for concern.<br />

• Other issues - Uneven distribution and low<br />

pressure supply complaints prevail in select<br />

wards in the town.<br />

8 UGD network (Yes/No/In progress) In<br />

B. Sanitation<br />

progress<br />

9 Households with septic tanks ~ 12000<br />

10 Number of Public conveniences 31<br />

11 Length of Storm drains (km) 43<br />

12 Est. access to sanitation (%) 85%<br />

13 Storm Drains - % of road length 10%<br />

C. Roads, Transportation and Street Lights<br />

• MyM is currently implementing an Underground<br />

sewerage system with assistance under NRCP.<br />

About 31 km of additional areas uncovered<br />

under the initial scheme has been identified to<br />

be covered at an outlay of Rs. 4 crore.<br />

• Storm water drains are provided only in<br />

approximately 10 % of the total road length<br />

within MyM limits and require significant<br />

improvement<br />

14 Total Length of Roads 107 • MyM maintains a road network of nearly 87.5<br />

15 Total number of Street Lights ~ 3100 km of which surfaced roads (both B.T. and CC)<br />

16 BT + CC roads / Road length (%) 93%<br />

constitute 87 %. In addition, nearly 20 km of<br />

highway roads traverses the MyM area. The<br />

17 Road length per Street Light (m) 28 m<br />

road network requires significant upgradation in<br />

view of the ongoing UGD scheme.<br />

• Nearly 76 % of the lights are tube lights and 24<br />

% are sodium vapour lamps. Average spacing<br />

between the lights (~ 28 m) is in line with the<br />

municipal norm of 30m<br />

• MyM proposes to develop a new Class A bus<br />

stand at Thennamara salai at an outlay of Rs.<br />

6.5 crore

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

D. Solid Waste Management<br />

18 Total Waste Generation (MT) 38 • MyM is in the process of implementing a project<br />

19 Collection - % of waste generated 92% at an outlay of Rs. 53 lakh to improve its solid<br />

20 Compost yard area -available 4.62<br />

waste management handling infrastructure<br />

21 Compost yard - required (Acres) 8.8<br />

22 Compost Yard - Gap - Acres (4.15)<br />

Analysis of financial performance<br />

Exhibit 2 provides a summary of the financials of MYM, along with a) an analysis of the growth and<br />

b) change in composition of various revenue and expenditure heads. Key highlights are summarised<br />

below:<br />

• A 10 % growth in operating surplus and a 8 % CAGR in revenue and by keeping costs in check.<br />

Tax income has grown at a CAGR of 5 % over the last five years in spite of no revision in<br />

Average Rental Value (ARV) since 1998.<br />

User charges have grown by a healthy 30 %, aided by increased in collection of water charges<br />

and other fee income including sewerage deposits The share of user charges/fees has<br />

increased from 12 % of revenue to 25 % of revenue over the last five years.<br />

Grants / Contributions from state have been the biggest revenue driver and have doubled in<br />

the last five years. They contribute to nearly 23% of income.<br />

Expenditure has remained flat over the last few years, showed an increasing trend till FY<br />

2003 and marginally declining over the next two years. Salaries have marginally declined due<br />

to reduction in staff, while Operating expenditure has grown at 13 %. Overall, revenue<br />

expenditure appears to have been in control.<br />

Interest expenditure has shown a steep increase, up from 2% of income in 2001 to 12% of<br />

income in 2005.<br />

Capital Investment <strong>Plan</strong><br />

We have compiled the felt needs of the city under various service areas, based on<br />

• Review of projects recommended in the <strong>City</strong> <strong>Corporate</strong> <strong>Plan</strong><br />

• Status and progress on projects identified as part of the Vision <strong>Plan</strong> (2004-09)<br />

• Consultations with stakeholders and<br />

• Discussion with officials

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

Exhibit 2 - Financial analysis<br />

Exhibit 3 provides a summary of the CIP for MYM.<br />

Segment<br />

Outlay as given in<br />

Vision<br />

<strong>Plan</strong><br />

CCP SFC<br />

Exhibit 3 Capital Investment <strong>Plan</strong><br />

Outlay reqd.*<br />

2006-15<br />

Roads 1052 350 1,125 2000<br />

Storm Water<br />

Drains<br />

1100 120 325 1000<br />

Water Supply 30 130 200<br />

Solid Waste<br />

Management<br />

18 170 81 150<br />

Street Lights 64 12 30 30<br />

Bus stands and<br />

rem.enterprises<br />

2001 2002 2003 2004 2005 CAGR %<br />

INCOME<br />

Own Income 295 300 377 526 382 7%<br />

Property tax 155 164 177 182 187 5%<br />

Professional tax 16 16 19 19 23 10%<br />

Water charges 19 13 36 109 89 47%<br />

Sewerage charges 1 5 38 121 49 214%<br />

Service Charges and fees 36 33 44 41 18 -16%<br />

Other Income 68 70 65 54 16 -30%<br />

Assigned Revenue 87 38 147 154 92 1%<br />

Devolution and Grants 73 77 144 200 144 18%<br />

Prior Period - 34 3 1 -<br />

Total 456 449 671 880 618 8%<br />

EXPENDITURE<br />

Staff and terminal benefits 261 254 361 270 249 -1%<br />

O & M 50 55 66 84 81 13%<br />

Program - - - - -<br />

Admin 10 126 59 34 31 32%<br />

Prior Period - 8 3 1 0<br />

Operating Expenditure 321 443 490 389 361 3%<br />

Operating surplus 134 6 181 492 258 18%<br />

Finance charges 9 - 12 49 76 69%<br />

Depreciation 7 13 104 81 30 46%<br />

Cash surplus 125 6 169 443 182 10%<br />

Overall surplus 118 (8) 64 362 152 6%<br />

200 712 671 1000<br />

Remarks on ongoing projects/Projects envisaged<br />

• Roads require significant upgradation in view of<br />

the ongoing UGD scheme<br />

• CCP highlights significant gaps in storm water<br />

drains<br />

• Comprehensive water supply project undertaken.<br />

• Outlay required for distribution gaps, pumping<br />

system upgradation, additional borewells and<br />

providing new connections<br />

• Immediate outlay for procuring equipment (Tipper<br />

lorry / Dumper place bins) for upgrading primary<br />

collection and secondary collection<br />

• Installation of timers / energy saving timers and<br />

additional lamps<br />

• Bus stand at an outlay of Rs. 6.5 crore and other<br />

market developments at an outlay of 92 lakh<br />

Education 70 50 100 • Development of school infrastructure

Segment<br />

Sewerage and<br />

Sanitation<br />

Outlay as given in<br />

Vision<br />

<strong>Plan</strong><br />

CCP SFC<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

Outlay reqd.*<br />

2006-15<br />

4216 4280 622 650<br />

Remarks on ongoing projects/Projects envisaged<br />

• Completion of remaining part of UGD scheme<br />

• Coverage of additional areas of approx. 31 kms to<br />

be covered<br />

Others 82 316 1,054 100 • Health centres, burial ground etc, Tourism projects<br />

TOTAL 6732 6060 4,184 5130<br />

List of priority projects<br />

Priority projects identified by the municipality are listed below. These projects and the capital<br />

expenditure estimates given above have been arrived at based on projects identified in the <strong>City</strong><br />

<strong>Corporate</strong> <strong>Plan</strong> prepared earlier and based on discussion with Chairperson, Commissioner and<br />

municipal officials. Select projects identified by MyM are identified below<br />

• Completion of ongoing UGD scheme. Additional areas left out in the current scheme of<br />

approximately 31 km of roads as identified by MyM also need to be taken up.<br />

• Restoration and upgradation of roads in view of the poor condition following implementation of<br />

UGD scheme and heavy rains last year.<br />

• Development of new Bus stand. This could be taken up on BOT basis to reduce pressure on<br />

financials of the municipality.<br />

• Remunerative projects on a BOT basis, specifically relating to tourism development. There is a<br />

proposal to develop a Theme park on a BOT basis at Chitarkadu, where 6 acres of municipal land<br />

is available.<br />

Reform Agenda<br />

ULB level<br />

MYM could potentially increase its own income to Rs. 550 lakh by 2010 through focused<br />

interventions in the following areas:<br />

1. Property tax: – through revision in ARV, widening assessee base and closer scrutiny.<br />

2. Professional tax – sustaining a growth in assessments of 5 % in the assessments through<br />

widening tax base among traders and self-employed professionals<br />

3. User charges - MYM should target achieving another 4000 water connections even by FY 2010.<br />

Implementation of UGD scheme structured partly on public deposits and user charges could also<br />

add to revenues and investment capacity.<br />

4. PPP / remunerative projects - MYM also needs to explore land development as a revenue<br />

enhancement mechanism and should focus on attracting private sector participation through<br />

appropriate BOT/ SPV structures for implementing remunerative projects. There is a proposal to<br />

develop a Theme park on a BOT basis at Chitarkadu, where 6 acres of municipal land is available.<br />

5. Energy costs - A savings of 10-15% reduction in energy costs appears imminently achievable. A<br />

comprehensive energy audit is required in this regards.<br />

6. Collection Efficiencies - MyM’s collection efficiency is very low across all its revenue heads<br />

namely, property tax, professional tax and user charges and needs significant improvement from

current levels. MyM should consider a) a focused one-time drive to clear up its dues and b)<br />

strengthening of its collection process and organisation to ensure that the overall levels of<br />

efficiency in order to improve and sustain its collection efficiencies.<br />

7. NGOs / <strong>Corporate</strong> participation - Intensify focus on attracting NGOs/advertising revenue for<br />

city beautification projects.<br />

Actions from GoTN and GoTN agencies<br />

1. Initiate action to complete ongoing updation of land use and master plan for Mayiladuthurai<br />

municipality on priority to guide future growth of the town in an orderly manner.<br />

2. Revise ARV for property taxes, pending since 1998 at the earliest.<br />

3. Develop model concessions / formats for involving Private sector in various areas including Solid<br />

waste, STP O&M, street light maintenance and remunerative projects<br />

4. Incentivise energy conservation and implementation of SWM guidelines through specific grants<br />

5. GoTN should continue its thrust on e-governance, accounting systems and capacity<br />

building/training. Specific actions on this have been identified in the report.<br />

FOP, borrowing capacity and investment capacity<br />

While the borrowing capacity computed as the minimum of NPV of operating surplus, 30% of<br />

revenues during the projection period works out to Rs. 464 lakh, actual projections reveal that<br />

Mayiladuthurai faces a severe Debt Service Coverage issue even at this level of borrowing. This is<br />

due to the strain of repayments on its existing loans which stood at nearly 13 crore in FY 2006.<br />

Therefore, Mayiladuthurai borrowing capacity is negligible even with improvements.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity<br />

Exhibit 4 Summary of key results<br />

Summary of FOP results<br />

Revenues – FY 2006 (Rs. Lakh) 467<br />

Revenues – FY 2015 (Rs. Lakh) 799<br />

Revenue CAGR % - FY 2006-15 6.14<br />

Avg. Op. Surplus (Rs. Lakh) (53)<br />

Avg. Cash Operating Surplus<br />

Avg. TE (excluding depreciation)/TR<br />

41<br />

(%) 94%<br />

Average Debt Servicing/TR (%) 26%<br />

Borrowing Capacity as a minimum of NPV of<br />

NPV of 50% of Cash Surplus (without<br />

new loans) 80<br />

NPV of 30% of Revenue 1,239<br />

Borrowing Capacity 80<br />

Investment Capacity 612<br />

Investment Requirement 3,767<br />

IC/ IR 16%<br />

Some drastic measures including restructuring of its existing loans is required for Mayiladuthurai<br />

municipality to improve its investment capacity. Otherwise, MyM would need to utilize Grants from<br />

schemes like UIDSSMT and IHSDP to undertake its investments. Further, MyM could also consider<br />

involvement of private sector in implementing remunerative projects including bus-stands, markets<br />

and slaughter houses etc.

1.1 Background to the study<br />

1. Introduction<br />

Mayiladuthurai is a selection grade <strong>Municipal</strong> Town and taluk headquarters of the Nagapattinam<br />

District in Tamil Nadu. Under the Tamil Nadu Urban Development Project - II (TNUDP-II), a <strong>City</strong><br />

<strong>Corporate</strong> <strong>Plan</strong> (CCP) was prepared for Mayiladuthurai <strong>Municipal</strong>ity (MyM) in 2004. The objective<br />

of the CCP was to outline a vision for development of the city and to identify strategies and tasks to<br />

be carried out by MyM. Subsequently, MyM has also developed a 5-year Vision <strong>Plan</strong> (2004-09),<br />

identifying various projects that it plans to undertake during this period. In order to enable effective<br />

implementation of projects envisaged in its CCP and Vision <strong>Plan</strong>, The Tamil Nadu Urban<br />

Infrastructure Financial Services (TNUIFSL) mandated ICRA Management Consulting Services<br />

(IMaCS) for conversion of <strong>City</strong> <strong>Corporate</strong> <strong>Plan</strong> (CCP) into a Business <strong>Plan</strong> (BP).<br />

1.2 Scope of work<br />

The scope of work for the study covered a) assessment of the financial and operating aspects, b)<br />

Review issues relating to revenue realisation and cost management and identification of improvement<br />

(revenue enhancement and cost reduction) measures and c) Development of a Financial and Operating<br />

<strong>Plan</strong> (FOP), taking into account potential revenue enhancement and cost reduction measures.<br />

1.3 IMaCS approach to the study<br />

Exhibit 1.1 gives a snapshot of IMaCS’ approach to the study.<br />

DIAGNOSIS<br />

Demands on ULB for<br />

various services<br />

Review of ULB<br />

performance<br />

Clarity on ‘As-is’ state of the ULB in<br />

terms of financial and operating<br />

performance<br />

CCP<br />

Vision <strong>Plan</strong><br />

Existing proposals<br />

of the ULB<br />

Understanding of<br />

context in which<br />

the ULB operates<br />

Assessment of<br />

Past Financials<br />

Underlying<br />

Operational<br />

indicators and<br />

service delivery<br />

Exhibit 1.1 IMaCS approach to the study<br />

EVALUATION OF<br />

CHOICES<br />

Clarify ULB priorities on<br />

projects /schemes<br />

Analysis of likely trends in<br />

revenue and cost drivers<br />

Areas and scope for<br />

revenue and cost<br />

improvement<br />

Crystallize Strategic Choices<br />

going forward<br />

DEVELOP FINANCIAL &<br />

OPERATING PLAN<br />

Base Case Business <strong>Plan</strong><br />

Sensitivity analysis on key<br />

business drivers<br />

Critical operational<br />

outcomes to be achieved<br />

Steps to be taken by ULB/<br />

GoTN /TNUIFSL towards<br />

achieving the Business<br />

plan milestones and targets<br />

Translate options into tangible<br />

and measurable projections<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 1

1.3.1 Step I – Diagnostic review<br />

The diagnostic review involved an assessment of the current status of MyM, its activities and<br />

financial performance, review of the <strong>City</strong> <strong>Corporate</strong> <strong>Plan</strong> (CCP) and discussions with TNUIFSL and<br />

MyM. We had the opportunity to interact with the Commissioner along with their team and had<br />

extensive interactions during our field visits.<br />

We collected relevant information on the performance (operational and financial) from MyM. Our<br />

review was focused on the following areas:<br />

• Financial position<br />

• Operational performance<br />

• Demands on urban services in the town/municipality<br />

The diagnostic review was directed towards achieving a clear understanding of the operating and<br />

financial performance of MyM.<br />

1.3.2 Step II – Evaluation of options for financial improvement and projects<br />

Based on the diagnostic review, we crystallised the options for MyM covering a) analysis of areas for<br />

revenue enhancement and cost management and b) Felt needs in terms of projects and estimate of<br />

capital outlay.<br />

1.3.3 Step III –Projection of financial statements and estimation of investment and<br />

borrowing capacity<br />

We have projected financial statements for MyM under two scenarios namely, a) base case and b)<br />

with potential improvements. Under both scenarios, the optimum borrowing capacity and sustainable<br />

investment capacity have been computed.<br />

The Draft Final Report for the study was presented to the office of CMA, officials of Trichy<br />

Corporation and TNUIFSL in April 2006. Subsequently, the report was presented to Chairperson and<br />

select council members. This was followed by a review of the report at TNUIFSL by officials of<br />

TNUIFSL, CMA and MyM. This report incorporates the suggestions from these consultations.<br />

1.4 Structure of the report<br />

This report is organised as follows:<br />

• Section 1 Introduction<br />

• Section 2 Mayiladuthurai - a brief profile<br />

• Section 3 Review of operating performance<br />

• Section 4 Analysis of financial performance<br />

• Section 5 Potential areas for improvement<br />

• Section 6 Business plan projections and investment capacity<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 2

2.1 Location and connectivity<br />

2. Mayiladuthurai - a brief profile<br />

Mayiladuthurai is a selection grade <strong>Municipal</strong> Town and taluk headquarters of the Nagapattinam<br />

District in Tamil Nadu. Mayiladuthurai is located at a distance of 281 kms from Chennai and is well<br />

connected to all major towns in Tamil Nadu by road and rails. Mayiladuthurai is home to the famous<br />

‘Mayuranathar’ Shiva temple and the historic tourist centres, Suriyanar Temple, Theralandur and<br />

Thirunallar are situated near to the town. The river Cauvery traverses through this town.<br />

2.2 Social and demographic characteristics<br />

Mayiladuthurai with a total land area of 11.26 sq. km had a population of 84,290 in 2001.<br />

Year<br />

Exhibit 2.1 Population trend<br />

Population Decadal<br />

Population Variation Growth rate %<br />

1951 43,436 10,766 32.95 %<br />

1961 51,399 7,693 18.33 %<br />

1971 60,196 8,797 17.12 %<br />

1981 67,710 7,514 12.48 %<br />

1991 76,837 9,332 13.78 %<br />

2001 84,290 7,158 9.29 %<br />

Source: Census of India<br />

The CCP projects the population in the town to reach 92023 by 2013 and 99070 by 2023. Population<br />

density is higher in the core areas and lower in the peripheral areas of the city. But the CCP points out<br />

that there is outward movement of people to the periphery. Population density is more along the river<br />

palam Kaveri that run across the town from east to west in the southern part of the town. Low density<br />

areas are of new settlements that spread along the river banks at the periphery of the town. Due to the<br />

direction of the river and major roads being in the east west directions, developments are taking place<br />

in the same pattern.<br />

Mayiladuthurai 1 recorded an overall literacy rate of 80.2 % with female literacy of 76.1 %, while the<br />

sex ratio was 1012 females per 1000 males. As per Census 2001, the slum population in<br />

Mayiladuthurai is 13% of the population. However, the municipal data shows an increase in slum<br />

population and this is a major concern area for the municipal corporation.<br />

1 Source: http://gisd.tn.nic.in/census-paper2/TABLES/table-1c.htm<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 3

2.3 Economic Development<br />

2.3.1 Composition of workforce<br />

The economic base of Mayiladuthurai is predominantly, tertiary sector activities with trading of agro<br />

products and cottage industries. Hence the participation rate is more in the tertiary sector.<br />

As per census data of 1991, worker population is about 28.6% of the total population, which is low<br />

compared to the state figure. The economic based of the town is predominantly tertiary sector<br />

activities with trading in agri-products and cottage industries. Nearly 67 % of the workforce is<br />

engaged in the tertiary sector.<br />

2.3.2 Economic activities<br />

Industry<br />

Mayiladuthurai is an industrially backward town and there is no major industry in this town. There are<br />

about 79 small agro based and household industry spread over the entire developed area. There are<br />

few engineering industries, welding and lathe works, auto works, tri-cycle manufacturing works and a<br />

large number of agro based industries that accommodate larger portion of workers. Only 6.325<br />

hectares are under industrial use, which is very low compared to the standard of 370 hectares use. Key<br />

industries include rice mills, engineering works, printing press and confectionery making. The CCP<br />

indicates that the proposed ITI could spur the growth of small scale industry. Additional areas that<br />

emerged based on consultation with Chairperson and select ward members on potential economic<br />

activities for the town include the need to create employment intensive investment including rice<br />

milling and tourism development. It was also suggested that the municipality along with the Tamil<br />

Nadu Slum Clearance Board should identify vacant/acquirable land areas within the municipal areas<br />

to create land parcels for industrial development and slum rehabilitation.<br />

Heritage and tourism activities<br />

Being a temple town (the Mayuranathar Temple attracts pilgrims from other places), Mayiladuthurai a<br />

tourist centre. It is also strategically located in close proximity to the famous nine Navagraha temples.<br />

A number of important tourist places including Poompuhar, Mayuram, Tanquebar and Therazendur<br />

are in close proximity to the town. Since Mayiladuthurai has a good road and rail system, it acts as a<br />

halting junction for pilgrimages. The CCP points out that there is good scope for exploiting tourist<br />

potential and substantially increasing the economic growth of the town.<br />

Trade and commerce<br />

In terms of commercial activity, there are weekly markets and daily markets and an Uzhavar Sandhai<br />

functioning at present in Mayiladuthurai. The <strong>Municipal</strong>ity runs the commercial complex with 11<br />

shops in the Kittapa Commercial complex. Apart from these, there are flower and vegetable markets<br />

from where goods are exported to other cities. The town is an aggregation centre for a special variety<br />

of mangoes called ‘Pathiri’ got from the surrounding villages. Milk production is also an important<br />

activity around the town.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 4

2.4 Land use management<br />

Mayiladuthurai <strong>Municipal</strong>ity covers an extent of 11.27 sq. km. The CCP observes that the<br />

developments extend from the core of the town along the main roads as ribbon developments. High<br />

density residential areas are in the older parts of the town. Mayiladuthurai is located amidst a fairly<br />

large agricultural belt and trading in agricultural products thus forms an important activity in the<br />

town.<br />

2.4.1 Issues in land-use<br />

Mayiladuthurai municipal area has been declared as Mayiladuthurai Local <strong>Plan</strong>ning area. The member<br />

of the council form members of the planning area as well. Exhibit 2.2 provides details of land use.<br />

The urbanised area constitutes 620 hectares out of the total 1137 hectares. About 44.9% of the total<br />

area comes under undeveloped / non-urbanised land. The land use pattern in 1996 is as given below:<br />

Exhibit 2.2 Land-use - 1996 and 2011 (proposed)<br />

Sl. No Type 1996 Provided in master plan (2011)<br />

Land (ha) % of total Land (ha) % of total<br />

1 Residential 498.84 44.27 892.20 79.2<br />

2 Commercial 68.87 6.11 78 6.9<br />

3 Industrial 6.33 0.56 12 1.1<br />

4 Educational 22.35 1.98 45 4.0<br />

5 Public and semi-public 24.27 2.16 25 2.2<br />

6 Agricultural and others 506.35 44.92 74.5 6.6<br />

Total 1127 100 `1127 100<br />

Residential areas proposed include Pattamangalam, Koradadu, Sithakadu, Mayuram, Tiruvillandu and<br />

Vellalagaram village parts with low-medium densities. The residential areas are divided into primary<br />

residential and mixed residential. The primary residential area has been zoned on newly developed<br />

areas and the central part of the town has been designated as mixed residential. The majority of<br />

commercial activity is spread around the existing bus stand area. Commercial areas have been<br />

proposed in the centre of the town around the bus stand between Mahathanapuram road and hospital<br />

road. Commerical areas are also proposed along the major highways including Kumbakonam road<br />

and Avoor road. An ITI is provided for as part of the master plan as part of the Industrial area, for<br />

which 12 acres have been allocated.<br />

2.5 Strategy for development<br />

The CCP outlines the following strategies for development:<br />

• Provision of food processing centre for fruit and milk products<br />

• Improvement of agro-processing industries around the town that have direct and indirect impact<br />

on employment opportunities<br />

• Improvement of linkages of the town to other urban centres<br />

• Provision of better facilities including lodging and boarding facilities for tourists.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 5

Additional areas that emerged based on consultation with Chairperson and select ward members on<br />

potential economic activities for the town include the need to create employment intensive investment<br />

including rice milling and tourism development. It was also suggested that the municipality should<br />

identify vacant/acquirable land areas within the municipal areas to create land parcels for industrial<br />

development and other economic activities.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 6

3. Review of operating performance<br />

This section presents a review of the status of infrastructure development undertaken by MyM<br />

3.1 Water Supply<br />

Water Supply to Mayiladuthurai town is through two water supply schemes of TWAD and hand<br />

pumps<br />

• Scheme I – This was initiated in 1969 to provide protected water supply to the town and was<br />

designed to cater to ultimate population of 62000 at a per capita supply of 70 litres per day<br />

(LPCD). However the carrying capacity has been reduced to 55 LPCD.<br />

• Scheme II – TWAD has implemented an augmentation project at a cost of Rs. 11.25 crore<br />

including construction of a collector well and a pumping main of length of 20.2 km. Water supply<br />

is effected through three additional service reservoirs and a new distribution system of 45.8 km.<br />

• Hand pumps - 296 hand pumps have been installed at various places in the town.<br />

The new water supply scheme was designed to meet the intermediate stage (2011) and ultimate stage<br />

(2026) requirement of water supply, worked out to 103.5 lakh litres and 139.5 lakh litres respectively.<br />

Hence the water supply scheme is expected to satisfy the present and future demand of water for the<br />

projected population.<br />

3.1.1 Key issues<br />

Exhibit 3.1 Water supply<br />

Source I Source 2 Source 2<br />

Supply<br />

Source Location Sitharkadu Gandhi Nagar Mamarathu medai<br />

Daily intake (Lakh litres) 27 6 9<br />

Transmission type Pumping Pumping Pumping<br />

Location of Head works Vennar Coleroon<br />

Avg. per capita supply 90 LPCD<br />

Distribution<br />

Distribution main (km) 99.47 km<br />

% of road length covered 99.8%<br />

Storage<br />

Storage Capacity<br />

Existing capacity 4 OHTs with capacity of 4.75 million litres<br />

Norm 3.7 Million Litres<br />

Some of the key issues with respect to water supply are highlighted below:<br />

• Demand – Supply – MyM’s supply of 7.5 MLD corresponds to 90 LPCD which is in line with<br />

municipal norms.<br />

• Scope for adding water connections – Water connections account for only about 37 % of the<br />

number of properties assessed and indicate the scope for adding more connections. However, the<br />

high proportion of slum population and availability of water fountains constrain the ability to add<br />

more connections. Further, availability of ground water for households also deters people from<br />

taking household connections.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 7

• Poor collection efficiency - Current collection efficiency was only 65 % in FY 2005. Overall<br />

collection efficiency is even lower due to poor arrears collection ( 40 % efficiency) and is a major<br />

cause for concern, especially considering the significant debt servicing obligation that MyM has.<br />

• Other issues - Uneven distribution and low pressure supply complaints prevail in select wards in<br />

the town. Also certain extended areas of the town need to be provided with distribution main.<br />

There has been no formal leakage audit and this initiative could enable improve the efficiency of<br />

water supply.<br />

3.2 Sanitation<br />

3.2.1 Under Ground Drainage (UGD)<br />

Mayiladuthurai is currently implementing an Underground sewerage system with assistance<br />

under the National River Conservation Program (NRCP)<br />

Mayiladuthurai is in the process of implementing comprehensive Underground drainage scheme with<br />

assistance from NRCD at an outlay of Rs. 42 crore. Nearly 80 % of the pipeline work for the project<br />

has been completed. When completed the project is expected to be ready to serve more than 13000<br />

house service connections. The project would have 8 pumping stations with 1 sewerage treatment<br />

plant. The UGD scheme is expected to be completed during the course of the next two years. Exhibit<br />

3.3 provides details of the existing sanitation facilities in Mayiladuthurai.<br />

Exhibit 3.3 Sanitation facilities –<br />

% of<br />

households<br />

Households 16070<br />

Septic tanks 12535<br />

Low cost sanitation 1562<br />

Public conveniences (usable) 12<br />

Public conveniences (non usable) 19<br />

Source: CCP<br />

Cost of additional areas covering 31 km which were not covered by the above project is estimated at<br />

Rs. 4 crore. MyM is keen to implement the same upon completion of the existing project<br />

3.3 Storm water drains<br />

Storm water drains are provided in approximately 10 % of the total road length within MyM limits.<br />

Exhibit 3.4 provides the details.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 8

Exhibit 3.4 Storm water drain network<br />

Details Length in km % coverage<br />

Open pucca / surfaced 39 36%<br />

Kutcha / unlined 4 4%<br />

Total Drains (km) 43 40%<br />

Roads without drains 64 60%<br />

Total Road Length (km) 107 100%<br />

Source: SFC Questionnaire Jun 2005<br />

3.4 Solid Waste Management<br />

Mayiladuthurai generates nearly 104 MT of solid waste per day, while collection is estimated about<br />

85 MT per day (implying nearly 80% collection). Exhibit 3.5 gives the current status of solid waste<br />

generation and management system of MyM.<br />

Exhibit 3.5 Solid Waste Management - current status<br />

Generation / day 38 MT<br />

Collection / day 35 MT<br />

Door - to - door collection All wards<br />

Privatisation of door-to-door collection 39 streets<br />

Compost Yard area 4.62 acres<br />

MyM’s vision plan has identified deficiencies in terms of compost yards and transportation<br />

infrastructure. MyM is in the process of implementing a project at an outlay of Rs. 53 lakh to improve<br />

its solid waste management handling infrastructure.<br />

3.5 Roads<br />

Exhibit 3.6 provides details of the road network under the jurisdiction of MyM.<br />

Exhibit 3.6 Road network<br />

Type <strong>Municipal</strong> Roads Highways<br />

Cement Concrete pavement 5.617 6%<br />

km % km %<br />

BT. Roads 75.784 87% 20.854 100%<br />

W.B.M roads 3.457 4%<br />

Earthen Roads 2.685 3%<br />

Total 87.543 100.00% 20.854 100<br />

MyM maintains a road network of nearly 87.5 km of which surfaced roads (both B.T. and CC)<br />

constitute 87 %. In addition, nearly 20 km of highway roads traverses the MyM area. The road<br />

network requires significant upgradation in view of the ongoing UGD scheme.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 9

3.6 Street lights<br />

Exhibit 1 provides details of provision of street lights by MyM. Nearly 76 % of the lights are tube<br />

lights and 24 % are sodium vapour lamps. Average spacing between the lights (~ 28 m) is in line with<br />

the municipal norm of 30m. Exhibit 3.7 provides the details.<br />

3.7 Bus stands<br />

Exhibit 3.7 Existing Street Lighting Facilities<br />

Type Nos.<br />

Tube lights 2334<br />

Sodium Vapour Lamps 708<br />

Mercury Lamps -<br />

High Mast /Others 3<br />

Total 3045<br />

The existing bus stand in Mayiladuthurai is on the Kumbakonam Sirkazhi road. It is a class B bus<br />

stand with about 12 bus bays. The CCP observes that the bus stand is highly saturated. MyM has<br />

proposed to develop a Class A bus stand to the 8.74 acre site at Thenamara salai. The proposed bus<br />

stand is to developed at an outlay of Rs. 7 crore and would have 51 bus bays and all required<br />

amenities.<br />

3.8 Capital Investment <strong>Plan</strong><br />

We have compiled the felt needs of the city under various service areas, based on<br />

• Review of projects recommended in the <strong>City</strong> <strong>Corporate</strong> <strong>Plan</strong> prepared earlier under TNUDP - II<br />

• Status and progress on projects identified as part of the Vision <strong>Plan</strong> (2004-09) prepared by MyM<br />

• Discussion with MyM officials<br />

Priority projects as identified by MyM are listed below<br />

1. Completion of ongoing UGD scheme. Additional areas left out in the current scheme of<br />

approximately 31 km of roads as identified by MyM also need to be taken up.<br />

2. Restoration and upgradation of roads in view of the poor condition following implementation of<br />

UGD scheme and heavy rains last year.<br />

3. Development of new Bus stand. This could be taken up on BOT basis to reduce pressure on<br />

financials of the municipality.<br />

4. Storm Water Drains<br />

5. Remunerative projects on a BOT basis, specifically relating to tourism development. There is a<br />

proposal to develop a Theme park on a BOT basis at Chitarkadu, where 6 acres of municipal land<br />

is available.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 10

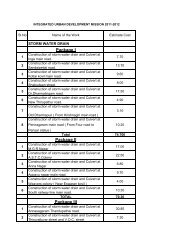

Exhibit 3.8 provides a brief snapshot of the felt needs of MyM over the next ten years for various<br />

services and the estimated outlay for implementing these projects.<br />

Segment<br />

Outlay as given in<br />

Vision<br />

<strong>Plan</strong><br />

CCP SFC<br />

Exhibit 3.8 MyM - Felt needs (2006-15)<br />

Outlay reqd.*<br />

2006-15<br />

Roads 1052 350 1,125 2000<br />

Storm Water<br />

Drains<br />

Remarks on ongoing projects/Projects envisaged<br />

• Roads require significant upgradation in view of the<br />

ongoing UGD scheme<br />

1100 120 325 1000 • CCP highlights significant gaps in storm water drains<br />

Water Supply 30 130 200<br />

Solid Waste<br />

Management<br />

18 170 81 150<br />

Street Lights 64 12 30 30<br />

Bus stands and<br />

rem.enterprises<br />

200 712 671 1000<br />

• Comprehensive water supply project undertaken.<br />

• Outlay required for distribution gaps, pumping system<br />

upgradation, additional borewells and providing new<br />

connections<br />

• Immediate outlay for procuring equipment (Tipper lorry<br />

/ Dumper place bins) for upgrading primary collection<br />

and secondary collection<br />

• Installation of timers / energy saving timers and<br />

additional lamps<br />

• Bus stand at an outlay of Rs. 6.5 crore and other<br />

market developments at an outlay of 92 lakh<br />

Education 70 50 100 • Development of school infrastructure<br />

Sewerage and<br />

Sanitation<br />

4216 4280 622 650<br />

• Completion of remaining part of UGD scheme<br />

• Coverage of additional areas of approx. 31 kms to be<br />

covered<br />

Others 82 316 1,054 100 • Health centres, burial ground etc, Tourism projects<br />

TOTAL 6732 6060 4,184 5130<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 11

4. Analysis of financial performance<br />

This section provides a summary analysis of the financial performance of MyM.<br />

4.1 Income and Expenditure summary of MyM<br />

Exhibit 4.1 provides a summary of the income and expenditure of MyM. This summary has been<br />

prepared based on information provided by MyM 2 .<br />

Exhibit 4.1 Income and Expenditure of MyM - Last five years<br />

4.2 Revenue streams of ULB in Tamil Nadu<br />

Revenue of ULBs in Tamil Nadu can be categorised along three areas:<br />

• Own Revenue - comprising taxes (property tax and professional tax), user charges (water,<br />

sewerage, solid waste etc.) and other non-tax income (lease and rents, sale & hire charges etc)<br />

• Assigned Revenue - Income generated revenues shared with the ULB<br />

• Grants and Contributions - Grants and transfers made by GoTN<br />

2 We have received the audited accounts from MyM for FY 2001 to FY 2004 and information on FY 2005 (as in the case of<br />

DCB statements)<br />

2001 2002 2003 2004 2005 CAGR %<br />

INCOME<br />

Own Income 295 300 377 526 382 7%<br />

Property tax 155 164 177 182 187 5%<br />

Professional tax 16 16 19 19 23 10%<br />

Water charges 19 13 36 109 89 47%<br />

Sewerage charges 1 5 38 121 49 214%<br />

Service Charges and fees 36 33 44 41 18 -16%<br />

Other Income 68 70 65 54 16 -30%<br />

Assigned Revenue 87 38 147 154 92 1%<br />

Devolution and Grants 73 77 144 200 144 18%<br />

Prior Period - 34 3 1 -<br />

Total 456 449 671 880 618 8%<br />

EXPENDITURE<br />

Staff and terminal benefits 261 254 361 270 249 -1%<br />

O & M 50 55 66 84 81 13%<br />

Program - - - - -<br />

Admin 10 126 59 34 31 32%<br />

Prior Period - 8 3 1 0<br />

Operating Expenditure 321 443 490 389 361 3%<br />

Operating surplus 134 6 181 492 258 18%<br />

Finance charges 9 - 12 49 76 69%<br />

Depreciation 7 13 104 81 30 46%<br />

Cash surplus 125 6 169 443 182 10%<br />

Overall surplus 118 (8) 64 362 152 6%<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 12

Exhibit 4.2 provides a detailed classification of the revenue streams.<br />

4.3 Revenues<br />

Assigned<br />

Revenue<br />

Entertainment<br />

Tax<br />

Stamp Duty<br />

Exhibit 4.2 Revenue streams - ULBs in Tamil Nadu<br />

Non- Tax Income<br />

Water Charges<br />

Other Charges<br />

Other Income<br />

ULB-Income<br />

Own Income<br />

Tax Income<br />

Property Tax<br />

Profession Tax<br />

Other Taxes<br />

Transfer from<br />

Govt<br />

Devolution Fund<br />

Grants and<br />

Contribution<br />

Exhibit 4.3 provides details of revenue of MyM along various heads between FY 2001 and FY 2005.<br />

1000<br />

500<br />

0<br />

Exhibit 4.3 Revenue trend<br />

68<br />

73<br />

87<br />

56<br />

104<br />

77<br />

38<br />

51<br />

147<br />

118<br />

271<br />

92<br />

156<br />

171 180 195 201 210<br />

Figures in Rs. Lakh<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 13<br />

68<br />

144<br />

55<br />

200<br />

154<br />

16<br />

144<br />

2001 2002 2003 2004 2005<br />

Taxes User charges Assigned Revenue Devolution and Grants Others

4.3.1 Tax Income<br />

Tax income has grown at a CAGR of 5 % over the last five years. Share of taxes have declined from<br />

37% to 34 % of income.<br />

Property Tax<br />

Property tax alone accounted for a 30 % of income of MyM in FY 2005 and is an important<br />

contributor of revenues to MyM. Following are the key issues / observations with respect to property<br />

tax. Exhibit 4.4 provides a summary.<br />

Year<br />

Exhibit 4.4 Property tax - analysis of key revenue drivers<br />

Collection Efficiency Properties<br />

Arrears Current Total Numbers Tax/property Growth %<br />

2000-01 18% 79% 56% 15737 1054 na<br />

2001-02 20% 81% 57% 15827 1090 1%<br />

2002-03 19% 81% 55% 15938 1142 1%<br />

2003-04 16% 69% 47% 16163 1146 1%<br />

2004-05 42% 82% 67% 16373 1095 1%<br />

a) Decline in share of property tax - Even though the property tax has increased in absolute<br />

terms, its share in total income has declined from 34% to 30 % over the last five years.<br />

b) Low assessments growth - Assessments have grown at just 1% and the average tax per<br />

assessment has also been stagnant. The quinquennial revision of Annual Rental Value<br />

(ARV) due in 2003 has not been undertaken as of date.<br />

c) Low collection efficiencies - Collection efficiency is a cause for concern. While collection<br />

efficiency in current demand has been around 82 % in 2005, efficiency in overall collection<br />

has been very low (47% - 67% in the last 5 years). Overall efficiency has improved to 67 % in<br />

FY 2005, but needs significant improvement.<br />

d) Aging of arrears - Growth in arrears in the last 5 years is a disturbing trend and needs to be<br />

arrested.<br />

e) Break-up of assesses - Residential segment contributes 71 % of the total assessments, but<br />

only 58% of the total property tax demand. The municipality must take steps to increase<br />

property tax from this category. Exhibit 4.5 below gives the detailed break-up of assesses for<br />

property tax.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 14

Professional tax<br />

Exhibit 4.5 Property Tax - breakup of assessees<br />

Category of Property Number of<br />

Assessments<br />

% Tax Demand<br />

2005 - Rs. lakh<br />

Residential 11618 71% 105 58%<br />

Commercial 4433 27% 45 25%<br />

Industrial 84 1% 24 13%<br />

State Government Properties 309 2% 7 4%<br />

Public Sector Undertakings 2 0% 1 1%<br />

Total 16446 100.00% 182<br />

Exhibit 4.6 provides an analysis of key drivers for professional tax revenue.<br />

Year<br />

Exhibit 4.6 Professional Tax - revenue drivers<br />

Collection Efficiency Assessments<br />

Arrears Current Total Numbers Tax/assessment Growth %<br />

2000-01 3% 90% 26% 3140 503 na<br />

2001-02 1% 88% 23% 3142 498 0%<br />

2002-03 0% 84% 24% 1840 1009 -41%<br />

2003-04 1% 85% 25% 1562 1240 -15%<br />

2004-05 3% 87% 29% 1505 1552 -4%<br />

a) Share of professional tax in total income has increased from 3% to 4%<br />

b) Demand per assessment was Rs. 1552 per assessee in FY 2005.<br />

c) Collection efficiency has been very low While a current collection has been more than 85%,<br />

arrears collection is negligible.<br />

d) Composition of professional tax assessments - Exhibit 4.7 below shows the composition of<br />

assessments.<br />

Exhibit 4.7 Professional Tax – assessee break up<br />

Category Number of<br />

Assessments<br />

State/Central/Quasi Govt.<br />

Employees<br />

% Annual Tax<br />

demand<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 15<br />

%<br />

69 5% 1820 78%<br />

Traders 1362 90% 421 18%<br />

Self-employed professionals 42 3% 52 2%<br />

Private employers/<br />

Companies<br />

13 1% 20 1%<br />

Private employees 19 1% 24 1%<br />

Total 1505 2337 100%<br />

%

4.3.2 User Charges / Fees<br />

User charges have also grown by a healthy 30%, aided by 47% increase in collection of water charges<br />

and initiation of collection of deposits for sewerage connections. As a result, the share of user<br />

charges/fees has doubled from 12% of revenue to 25 % of revenue over the last five years.<br />

Exhibit 4.8 provides an analysis of key drivers for water charges.<br />

Year<br />

Exhibit 4.8 Water charges - revenue drivers<br />

Collection Efficiency Connections<br />

Arrears Current Total Numbers<br />

Charges/<br />

connection<br />

Growth<br />

rate<br />

2000-01 17% 70% 42% 5131 245 na<br />

2001-02 24% 85% 51% 5204 242 1%<br />

2002-03 30% 81% 62% 5439 428 5%<br />

2003-04 27% 52% 45% 5674 705 4%<br />

2004-05 40% 66% 55% 6131 701 8%<br />

a) No. of connections - There has been an increase in the number of connections from 245 in<br />

FY 2001 to more than 701 connections in FY 2005. Water connections account for about 37<br />

% of properties assessed, indicating scope for increasing the number of connections. The low<br />

penetration is also due to the availability of water fountains in several areas (covering nearly<br />

35% of population) which lead to loss of revenue for MyM.<br />

b) Water tariff / connection has increased from about Rs. 245 per year per connection to<br />

Rs.701 per connection in FY 2005.<br />

c) While 80% of the water connections are metered, water billing is being done on a flat<br />

(monthly) basis. Refer exhibit 4.9 for details of type of connections and water charges. MyM<br />

is considering collections on the basis of meter readings.<br />

d) Collection efficiency - Current collection efficiencies have ranged from a low of 63% (FY<br />

2004) to a high of 75% (FY 2005) and have not shown a linear trend. Arrears collection<br />

efficiency has been very low and has ranged between 21% and 33%. The overall collection<br />

efficiency of 55% is quite low and needs significant improvement.<br />

Exhibit 4.9 Water charges - category wise connections and tariff<br />

Connections Metered Un-metered Total % Billing<br />

system<br />

Domestic 6098 - 6098 97% Flat rate<br />

Commercial 183 - 183 3% Flat rate<br />

Total 6281 - 6281 100%<br />

Connection Type Flat rate Per KL<br />

Domestic Minimum Rs. 70 /-PM Rs.5/-<br />

Commercial Minimum Rs. 122/-PM Rs. 10/-<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 16

4.3.3 Assigned Revenue<br />

Assigned Revenue (which includes transfers of stamp duty and entertainment tax) has grown from Rs.<br />

87 lakh to Rs. 92 lakh over the last five years, but its share in total income has declined from 19% to<br />

15%.<br />

4.3.4 Grants/Contributions<br />

Grants / Contributions from state have one of the biggest revenue drivers and have doubled during FY<br />

2001-05. They contributed to nearly 23 % of revenues of MyM in FY 2004.<br />

4.4 Analysis of Costs<br />

Exhibit 4.10 provides details of costs of MyM along various heads between FY 2001 and FY 2005.<br />

Total expenditure has shown an increasing trend till FY 2003, before decreased over the next two<br />

years. Salary expenditure has declined, while O&M and finance charges have shown an increase.<br />

1000<br />

500<br />

4.4.1 Salary and wages<br />

0<br />

Exhibit 4.10 Costs - FY 2001 and FY 2004<br />

9 134<br />

10<br />

50 55<br />

261 254<br />

While salary and wages account for the highest expenditure (more than 40%% of total expenditure), it<br />

has shown a declining trend during FY 2001 to FY 2004. This has been due to the lack of addition in<br />

staff over the last few years and a number of posts remaining vacant. As of March 2005, the number<br />

of employees was 343.<br />

4.4.2 Operations and Maintenance<br />

0<br />

O & M forms the other major component of total expenditure. In absolute terms, this expenditure has<br />

been around 10-13% of total income during this period.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 17<br />

12<br />

62<br />

66<br />

361<br />

49<br />

35<br />

76<br />

31<br />

84 81<br />

270 249<br />

2001 2002 2003 2004 2005<br />

Staff O & M Admin Finance charges

Power costs<br />

Exhibit 4.11 gives the details of power costs out of the total repair and maintenance expenditure<br />

relating to Water & Sewerage and Street lights. Power costs have grown at a CAGR of 13%, driven<br />

primarily by a steep increase in power costs for street lights.<br />

Exhibit 4.11 Power costs - Water & Sewerage and Street Lights<br />

Power costs FY 2001 FY 2002 FY 2003 FY 2004 FY 2005<br />

Water & Sewerage (WS) 6 7 10 20 25<br />

% of total W&S 29% 29% 49% 50% 51%<br />

Street lights 21 23 43 41 42<br />

% of total Street light 65% 63% 83% 79% 76%<br />

Total 27 30 53 61 67<br />

Source: SFC questionnaire<br />

Power costs account for nearly 51 % of repair & maintenance costs of water and sewerage and t76%<br />

of operating street lights.<br />

Power costs have gone up from 19 % of O& M expenditure in FY 2001 to nearly 29 % of O&M<br />

expenditure in FY 2005.<br />

4.4.3 Operations and Maintenance<br />

Exhibit 4.12 gives the details of outstanding loans of MyM at the end of last five years.<br />

Lending Agency<br />

Amount of<br />

Loan<br />

Year of<br />

drawal<br />

Exhibit 4.12 Loan Statement<br />

Interest<br />

Rate %<br />

Repayment<br />

period<br />

(years)<br />

Total loan repaid as on<br />

30.9.2005<br />

Principal Interest Total<br />

Outstanding<br />

loan amount<br />

(3-9+13+14)<br />

2 3 4 5 6 9 10 11 16<br />

Govt. Loan 76.65 1998 13.5% 20 35.76 7.16 42.92 40.89<br />

1) Roads &<br />

Drainage<br />

2) Construction of<br />

Shops<br />

17.79 1994 8.75% 20 8.66 20.53<br />

20.06 1995 8.75% 15 8.12 22.65<br />

29.19 9.01<br />

30.77 11.96<br />

3) Special Roads 89.65 2003 9.05% 13 - 8.62 8.62 89.65<br />

1) Water Supply 367.06 2003 9.05% 15 - 74.30 74.30 367.06<br />

Water Supply 850.60 2004 8.20% 9 33.36 34.96 68.32 817.24<br />

Total 1421.81 85.90 168.22 254.12 1335.81<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 18

To summarise,<br />

MyM’s financial position has improved from an cash surplus of Rs. 125 lakh in FY 2001 to a cash<br />

surplus of Rs. 182 lakh in FY 2005, though its outstanding debt (Outstanding loan of Rs. 13 crore) is<br />

high. Key highlights are summarised below:<br />

• A 8 % CAGR in revenue and by keeping costs in check.<br />

Tax income has grown at a CAGR of 5 % over the last five years in spite of no revision in<br />

Average Rental Value (ARV) since 1998.<br />

User charges have grown by a healthy 30 %, aided by increased in collection of water charges<br />

and other fee income including sewerage deposits The share of user charges/fees has<br />

increased from 12 % of revenue to 25 % of revenue over the last five years.<br />

Grants / Contributions from state have been the biggest revenue driver and have doubled in<br />

the last five years. They contribute to nearly 23% of income.<br />

• Expenditure has remained flat over the last few years, showed an increasing trend till FY 2003<br />

and marginally declining over the next two years. Salaries have marginally declined due to<br />

reduction in staff, while Operating expenditure has grown at 13 %. Overall, revenue expenditure<br />

appears to have been in control.<br />

• Interest expenditure has shown a steep increase, up from 2% of income in 2001 to 12% of<br />

income in 2005.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 19

5.1 Public private partnerships (PPP)<br />

5. Potential areas for improvement<br />

MyM should consider handling the operations and maintenance of the Sewerage Treatment <strong>Plan</strong>t of<br />

the ongoing UGD scheme and implementation of the proposed slaughter house project through private<br />

sector participation. MyM should explore more areas to augment its own resources through use of<br />

PPPs. PPPs have been found to be very effective in addressing efficiency and asset management<br />

(through pre-defined service levels and accountability for operations and maintenance) aspects of<br />

infrastructure development. In this regard,<br />

1. CMA, GoTN should develop a framework for PPP including specific policies and guidelines.<br />

2. MyM should explore use of private sector participation in undertaking any remunerative<br />

projects in areas such as slaughter house, market development etc., through public private<br />

partnerships. To start with, MyM should explore developing the proposed new bus-stand and the<br />

amusement park at Chittarkadu through BOT / PPP structure.<br />

3. Being part of an heritage circuit, MyM should actively pursue projects that improve the tourist<br />

experience in the town. Several initiatives relating to tourism development can be pursued in<br />

partnership with private sector investment / corporate donations and NGO/Self Help Group<br />

partnerships. In Mayiladuthurai, MyM should pursue the following<br />

• Encourage corporate / NGO partnerships for heritage preservation and city beautification<br />

projects, including development and maintenance of parks.<br />

• Consider addition of more identified parking zones and pay-and-use toilets in the town. These<br />

could be maintained through Self-Help Groups.<br />

• Explore the feasibility of provision of integrated concrete roads with ducts for underground<br />

cabling and storm water drains around important heritage/tourist areas and align traffic movement<br />

to ensure ease of tourist movement during festivals. This would also enable better tourist<br />

experience and better maintenance of heritage centres.<br />

4. TNUIFSL should provide assistance covering necessary capacity building (in terms of<br />

evaluating mechanisms - BOT, SPV etc) and financing for developing projects through<br />

private sector participation.<br />

5.2 Potential for revenue enhancement<br />

5.2.1 Property Tax<br />

Exhibit 5.1 highlights the key issues and recommended interventions with respect to property tax.<br />

While a substantial improvement in property tax is contingent upon implementation of ARV revision<br />

(due in 2003), there are other interventions that would enable effective property tax realisation.<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 20

Exhibit 5.1 Key issues and suggested measures<br />

Issues Recommended Interventions Agency<br />

Revision of Annual rental Value (ARV)<br />

has fallen due in 2003. The revision is<br />

yet to be implemented.<br />

In 1998 when the ARV scheme for<br />

assessing property tax was introduced,<br />

the old assesses were allowed to pay<br />

taxes based on capital value with<br />

marginal increase, leading to<br />

distortions and non-uniform rates.<br />

Survey of properties happens only<br />

when the ARV revision takes place.<br />

Apart from addition in properties<br />

without getting assessed, addition to<br />

area in existing properties or<br />

conversion of property from residential<br />

to commercial category also goes<br />

unnoticed leading to revenue loss<br />

On an absolute basis, property tax<br />

arrears have shown an increasing<br />

trend.<br />

While Property tax is payable on a<br />

semi-annual basis, no interest /penal<br />

charges are levied on late payment.<br />

5. GOTN should implement the SFC<br />

recommendation of revision of property<br />

tax every three years, linked to inflation.<br />

This is will ensure gradual and stable<br />

increase, rather than the existing<br />

quinquennial revision.<br />

6. All assesses should be taxed on the<br />

same basis through a uniform and<br />

transparent approach to property tax<br />

assessment. Existing anomalies need to<br />

be removed at the earliest.<br />

7. Initiate a one-time survey to prepare a<br />

comprehensive database of properties<br />

available with it with updated information<br />

on the area / type and property tax details<br />

8. Institutionalise a mechanism for<br />

conducting surprise checks on a sample<br />

basis in all wards on an ongoing basis<br />

and mandatory re-assessment of<br />

9.<br />

properties every five years.<br />

Streamline procedures for assessment/<br />

approvals of new properties / expansion<br />

of existing properties to encourage selfdisclosure<br />

of property development /<br />

modification<br />

10. Computerise and web-enable property<br />

tax assessment and billing processes<br />

11. Develop a GIS based system for effective<br />

data capture and monitoring<br />

12. Launch a focused drive on existing<br />

arrears<br />

13. Conduct one time settlement scheme for<br />

old arrears and incentivise payments<br />

through marginal rebates for arrears<br />

pending for more than 5 years.<br />

14. Work with GOTN to moot creation of a<br />

special tribunal for speedy disposal of<br />

properties under litigation<br />

15. Make provisions for the debtors and take<br />

steps for writing off bad debts<br />

16. Implement Payment Due Date along with<br />

a 90 day grace period during which<br />

payments would involve a nominal<br />

interest payment.<br />

17. Payments beyond the grace period<br />

should include a steep penal charge to<br />

encourage payments on time.<br />

GoTN<br />

GoTN / MyM<br />

Conversion of CCP to BP - Mayiladuthurai <strong>Municipal</strong>ity 21<br />

Ku<br />

GoTN/MyM<br />

GoTN/MyM

Issues Recommended Interventions Agency<br />

Tax Dispute cases where the assessee<br />