City Corporate & Business Plan - Municipal

City Corporate & Business Plan - Municipal

City Corporate & Business Plan - Municipal

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

SEPTEMBER 2 0 0 9<br />

S S T A G E ññ IV<br />

C L U S S T T E E R R ññ VV<br />

Submitted by:<br />

Tamil Nadu Urban Infrastructure<br />

Financial Services Limited (TNUIFSL)<br />

Final Report<br />

for<br />

<strong>City</strong> <strong>Corporate</strong> cum <strong>Business</strong> <strong>Plan</strong><br />

for<br />

Ambur Town<br />

(Vellore District)<br />

Voyants Solutions Pvt. Ltd<br />

Level ñ 4, ìDiamond Duneî<br />

323, P.H. Road, Chennai ñ 600 029<br />

Tele: 044 4269 8584 Fax: 044 2668 1180<br />

E-mail: vsplchennai@voyants.in

Final Report <strong>City</strong> <strong>Corporate</strong> Cum <strong>Business</strong> <strong>Plan</strong><br />

EXECUTIVE SUMMARY ñ AMBUR MUNICIPALITY<br />

1. CITY CORPORATE CUM BUSINESS PLAN ñ CONTEXT and CONTENT<br />

The Tamil Nadu Urban Infrastructure Financial Services (TNUIFSL) aims to assist<br />

municipality in strengthening and improving its financial position for effective capital<br />

investment management and urban service delivery. The CMA and TNUIFSL have<br />

initiated the process of preparing the CCCBP for the municipality to enhance the vision<br />

of stakeholders in the growth of the town. The objective of this study is<br />

1. To assess the present status of infrastructure facilities available in the ULB and to<br />

suggest a comprehensive infrastructure plan with capital investment plan to meet<br />

the future needs.<br />

2. To outline issues in revenue realization in the ULB and suggest measures for<br />

revenue enhancement & financial improvement in the ULB<br />

3. In consultations with Stake holders and Council, suggest Action <strong>Plan</strong> and FOP to<br />

implement the infrastructure plan.<br />

2. SWOT and VISION<br />

Ambur, is a Selection Grade municipality, located on the Chennai-Bengaluru National<br />

Highway in Vellore district at a distance of 200 km from Chennai. The town is situated on<br />

the banks of Palar River. The population of Ambur <strong>Municipal</strong>ity is 99,624(Census 2001)<br />

and the area is 17.97 sq.km. Ambur municipality is geographically located at<br />

12 48'0"N Latitude 78 43'11"E longitude. The town is at an average elevation of 316 m<br />

(1036 ft) above MSL.<br />

Copious Palar water and policy decisions of the Govt. have made Ambur a leading<br />

exporter of finished and unfinished leather products in India. It is known as the ìLeather<br />

<strong>City</strong> of Tamil Nadu."<br />

A town level SWOT analysis, with reference to its regional context has been done based<br />

on feedback from stakeholder workshops and analysis of the status of various sectors of<br />

the city.

SWOT Analysis for Ambur <strong>Municipal</strong>ity<br />

Strength Weakness<br />

Leather city - Major industrial center and<br />

marketing center for leather products<br />

Well established society for sustainable industrial<br />

development- AEDOL , AMBURTEC etc<br />

Discharge of untreated effluents into the<br />

agriculture fields ,nearby areas and river Palar<br />

due to non-compliance / intermittent usage of<br />

CETPs<br />

Frequent oppositions form Welfare societies and<br />

consumer forums highlighting pollution due to<br />

tanneries.<br />

Traffic congestion due to encroachments on<br />

road and Absence of traffic management<br />

measures<br />

Establishment and maintenance of ETPS with the<br />

co-operation of business houses.<br />

Continuous monitoring & advice from premier<br />

institutes like Central Leather Research Institute<br />

(CLRI), National Environment Engineering Non - availability of green and affordable<br />

Research Institute (NEERI) and UNIDO.<br />

technology, with minimized usage of water.<br />

Availability of skilled and semi-skilled man power Inadequate financial strength of <strong>Municipal</strong>ity to<br />

in the town and hinterland<br />

take up major infrastructure projects.<br />

Famous cuisine influenced by the Nawab of High maintenance methodologies for existing<br />

Arcots ñ a marketable opportunity for the region . CETPs.<br />

Opportunities Threat<br />

Employment opportunities due to the presence of<br />

mills and small scale industrial establishments<br />

Most tanneries covered under the network of<br />

CETPs .<br />

Development of export and marketing centers<br />

and Establishment of Leather SEZs in the region<br />

TWIC- AEDOL ñ Pioneering initiatives in waste<br />

water recycle and reuse for tanneries<br />

Central Government subsidises and grants for the<br />

establishment of CETPs and allied facilities.<br />

Availability of land for future development<br />

Source: Feedback from stakeholders meeting and analysis.<br />

Degradation of environment - Palar River &<br />

agricultural lands upto 1500 ha due to<br />

discharge of untreated effluents<br />

Threats from Judicial authorities such as Green<br />

Bench for non-compliance of Environmental<br />

regulations<br />

Use of highly toxic and indisposable chemicals<br />

such as hexavalent chromium, trivalent<br />

chromium, etc in tanning processes<br />

Inadequate service delivery in the slums and<br />

poor living conditions.<br />

Inter-Regional Competitions for Economic<br />

Space<br />

The vision for the Ambur town is proposed as î A vibrant regional industrial hub on the<br />

Corridor of Excellence providing good infrastructure facilities to its citizens to promote an<br />

inclusive and sustainable developmentî.<br />

Supporting this vision is a set of development objectives, defined along various sectors of<br />

infrastructure. It covers the current status, issues in the sector, likely future demand,<br />

strategies for improvement and identified projects to meet these objectives. The sectors<br />

covered in the report for Ambur include water supply, sewerage and sanitation, solid<br />

waste management, storm water drains, street lights, slum improvement and other<br />

remunerative and social projects.

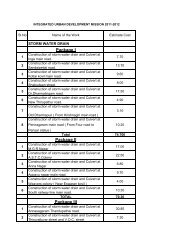

3. CITY INVESTMENT PLAN<br />

The summary of sector-wise investment requirements and prioritisation is given in the<br />

following table. The total investment required would be over Rs. 22167.00 lakhs.<br />

Capital Investment Needs forAmbur<br />

S.N Projects<br />

Estimated cost in<br />

lakhs<br />

1 Water supply 13667.00<br />

Mettur CWSS 11436.00<br />

Water supply improvement scheme 2231.00<br />

2 Sewerage 3950.00<br />

3 Storm water drain 684.00<br />

4 Solid Waste Management 847.00<br />

5 Traffic and transportation 268.00<br />

Road improvement 256.00<br />

Bus stand Improvement 12.00<br />

6 Street light 111.00<br />

7 Slum 2272.00<br />

8 Education 25.70<br />

9 Medicare 54.30<br />

10 Parks and open spaces 11.00<br />

11 Market 3.00<br />

12 Shopping Complex 100.00<br />

Shopping complex at V.A.Kareem OHT 36.80<br />

Shopping Complex at ESI hospital 63.20<br />

13 Slaughter House 36.00<br />

14 Burial ground 73.00<br />

15 E-Governance 18.00<br />

16 GIS Mapping for Comprehensive Property Database 37.00<br />

17 Mobile tax collection vehicle 10.00<br />

Total 22167.00<br />

4. FINANCIAL PERFORMANCE OF AMBUR MUNICIPALITY<br />

The summary of the financial status of Ambur municipality is as follows:<br />

It is observed that the <strong>Municipal</strong>ity has shown deficit in 4 out of the last 6 years.<br />

Prior to depreciation also the <strong>Municipal</strong>ity has shown deficit in 4 out of last 6 years.<br />

The <strong>Municipal</strong>ity needs to undertake lot of fiscal reforms and full leverage of its<br />

assets over the next few years to improve its financial strength.<br />

The average current collection efficiency of the municipality is very poor, with 50%<br />

efficiency in property tax, 75% efficiency in profession tax and 10% efficiency in<br />

water charges. The arrears collection performance is also poor.<br />

The broad financial analysis of the Ambur <strong>Municipal</strong>ity finances reveal that the<br />

<strong>Municipal</strong>ity has further scope for increasing its own sources of income and<br />

collection efficiency for servicing the additional borrowings in the future.<br />

The municipality also has very high borrowings at Rs. 331 lacs and is fully<br />

leveraged. The municipality can resort to further borrowings for new project<br />

identified only based on the additional income to be generated.

To summarise, the overall income pattern of the Ambur <strong>Municipal</strong>ity indicates more<br />

negative features than positive features. The positive trends are on the income side,<br />

where the <strong>Municipal</strong>ity has higher growth rate in income than growth in expenditure.<br />

5. PROPOSED REFORMS<br />

The proposed mandatory municipal reforms are broadly classified under the heads of:<br />

a. Reforms in resource mobilization<br />

i. Reforms in Taxation<br />

Property mapping - Onetime assessment of all unassessed and under assessed<br />

properties.<br />

Regular and periodic increment of property tax at the rate of 15% every 5<br />

years<br />

ii. Improving revenue from user charges<br />

The <strong>Municipal</strong> council may assume charge of increase in water charges, to<br />

recover full O&M Cost of water supply and UGSS.<br />

Increase in the connections to at least 85% of total assessments.<br />

Pre-mobilization of deposits for the proposed WS or UGSS project<br />

Implementation of Conservancy fee for SWM for hotels, marriage halls,<br />

industries and other commercial establishments<br />

Revenue Generation from sale of compost and scrap.<br />

iii. Reforms in Energy and Resource efficiency<br />

Conducting energy audits, leak detection studies, Enforce regulations on<br />

illegal tapping of water, Fixing flow control valves and meters.<br />

Provision of energy saving lights and equipments, Privatizing the maintenance<br />

of street lights to ESCO companies.<br />

iv. Formation of new sustainable revenue sources<br />

The remunerative proposals idenfied are<br />

Construction of shopping complex at V.A.Kareem OHT (14 shops)<br />

Construction of shopping complex at ESI Hospital (40 shops)<br />

Construction of new slaughter house with waste treatment facilities.<br />

v. Reforms in Audit and Accounting<br />

Timely auditing of accounts - August 30 th of next fiscal year<br />

Appointing a private Chartered Accountant as consultant<br />

Publishing audited statement in municipal website - September 30 th of next<br />

fiscal year<br />

vi. Regular and mandatory capacity buildings sessions for elected representatives<br />

& municipal officials

6. BORROWING AND INVESTMENT CAPACITY<br />

The borrowing and investment capacities of the town are arrived considering the<br />

revenue income and expenditure under the sustainable scenario, after implementation<br />

of the mandatory reforms proposed in this report.<br />

The investment capacity for the sustainable scenario assuming entire capital and O&M<br />

of Mettur CWSS is as grant, the following is summed up as below:<br />

Description<br />

Summary of Borrowing and Investment Capacity<br />

Base case<br />

Scenario 1<br />

Sustainable<br />

Scenario 2<br />

Sustainable<br />

Scenario 3<br />

No project With Mettur Without Mettur<br />

Borrowing Capacity Rs.1024.76 lacs -ve Rs. 46.61 lacs<br />

Investment Capacity Rs.4099.05 lacs -ve Rs. 1165.16 lacs<br />

Investment Requirement - Rs. 22167.00 lacs Rs. 22167.00 lacs<br />

Sustainable Investment<br />

Capacity % - IC / IR<br />

- -ve -ve<br />

The investment capacity of Ambur <strong>Municipal</strong>ity on ëAs is Where Basisí works out to<br />

Rs. 4099 lacs.<br />

The investment capacity of Ambur <strong>Municipal</strong>ity works to Nil in case of Scenario II<br />

(With Mettur CWSS project) and Nil in case of Scenario III (Without Mettur CWSS<br />

project).<br />

Thus it can be inferred that Ambur <strong>Municipal</strong>ityís financial position is weak and is<br />

not in a position to undertake major projects like water supply improvements and<br />

underground Sewerage system by way of borrowings on account of high<br />

operation & maintenance expenses and interest cost.<br />

Based on the above, it can be concluded that the <strong>Municipal</strong>ity based on its<br />

financial position can undertake only smaller projects identified in the CCP as<br />

given below :<br />

Projects Identified for Implementation based on financial position<br />

S.N. Particulars Total Priority<br />

Means of<br />

Finance<br />

A Physical Infrastructure Facilities L : G : O<br />

I Water Supply<br />

a)<br />

Improvements to Water Supply & Water<br />

Treatment 1591.00 A 60:30:10<br />

V Roads<br />

a) BT & CC Roads - Improvements 136.00 A&B 60:30:10<br />

b) BT & CC Roads - New Roads 120.00 C 60:30:10<br />

VI Bus Stand<br />

a) Bus stand Improvement 12.00 B 0:50:50<br />

VII Street Lights<br />

a) Proposed new lights 91.00 B 100% ULB<br />

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5

Retrofitting existing lights & energy<br />

b) saving devices 20.00 A ESCO<br />

VIII Market<br />

a) Improvements to Weekly market 3.00 A 100% ULB<br />

IX Shopping Complex<br />

a) Shopping Complex at V A Kareem OHT 36.80 A 90:00:10<br />

b) Shopping Complex at ESI Hospital 63.20 A 90:00:10<br />

B Social Infrastructure Facilities<br />

II Education<br />

a) Improvements to Schools 25.70 A 100% ULB<br />

III Parks & Playgrounds<br />

a) Improvement of parks 11.00 B 100% ULB<br />

IV Burial Ground / Crematorium<br />

a) Burial Ground with Gasifier (at Kapsa) 59.00 A 0:50:50<br />

b)<br />

Burial Ground improvement at<br />

Sanrorkuppam 14.00 B 0:90:10<br />

V Maternity Centre<br />

a) Improvement to maternity centre 54.30 A 0:50:50<br />

VI Slaughter House<br />

a)<br />

Improvement of Slaughter House<br />

(Treatment <strong>Plan</strong>t) 8.00 B 0:50:50<br />

b) New Beef Slaughter House 28.00 C 0:50:50<br />

C Other Projects<br />

I Vehicles<br />

a) Mobile tax collection van 10.00 A 100% ULB<br />

II E-Governance<br />

a) E-Governance 18.00 C 100% Grant<br />

III<br />

GIS Mapping for Comprehensive<br />

Property Database<br />

a) Property Mapping 7.00 A 0:90:10<br />

b) GIS database 30.00 C 0:90:10<br />

Total 2338.00<br />

As regards major projects like underground sewerage scheme, storm water drains,<br />

solid waste management, roads, improvement to slums etc., the <strong>Municipal</strong>ity can<br />

undertake these projects with minimum or Nil borrowings and more support from<br />

the Government towards capital cost.<br />

Metur CWSS project can be taken up by the <strong>Municipal</strong>ity only if both capital cost<br />

and operation & maintenance expenses is supported by the Government.<br />

Since the town does not have the borrowing capacity to take up the proposed<br />

UGSS and Mettur CWSS, it is suggested that remunerative projects and PPP<br />

projects be taken up initially. The state Government needs to extend support to<br />

Ambur <strong>Municipal</strong>ity to take up the proposed UGSS and WS schemes. After the<br />

implementation of the proposed mandatory reforms and improving the<br />

<strong>Municipal</strong>ityí s own revenue sources, the other projects could be taken up.

TTAABBLLEE OFF CCONTTEENTTSS<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

11<br />

1.1.<br />

BBAACCKKGRROUND AAND MEETTHODOLLOGIICCAALL FFRRAAMEEWORRK OFF TTHEE SSTTUDYY .. . .. ... .. ... .. .. ... .. ... .. .. 1111<br />

BACKGROUND ............................................................................................................................... 11<br />

1.2. OBJECTIVES .................................................................................................................................... 11<br />

1.3. SCOPE OF WORK ............................................................................................................................ 11<br />

1.4. STAGE III: DRAFT FINAL STAGE ................................................................................................ 13<br />

1.5. PRESENTATION AND DISCUSSION WITH REVIEW COMMITTEE ....................................... 13<br />

1.6. DISCUSSION WITH STAKEHOLDERS ........................................................................................ 15<br />

22<br />

2.1<br />

TTOWN PPRROFFIILLEE .. . ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 1166<br />

AMBUR . . . TOWN PROFILE .......................................................................................................... 16<br />

2.2 REGIONAL CONNECTIVITY .......................................................................................................... 16<br />

2.3 HISTORY OF THE MUNICIPALITY .................................................................................................. 16<br />

2.4 POPULATION CHARACTERISTICS ............................................................................................... 17<br />

2.4.1 POPULATION DISTRIBUTION .................................................................................................................. 17<br />

2.4.2 POPULATION GROWTH ........................................................................................................................ 18<br />

2.4.3 POPULATION PROJECTIONS ................................................................................................................. 18<br />

2.4.4 POPULATION DENSITY .......................................................................................................................... 18<br />

2.4.5 SEX RATIO ........................................................................................................................................... 19<br />

2.4.6 LITERACY ............................................................................................................................................. 19<br />

33<br />

3.1<br />

EECCONOMIICC DEEVVEELLOOPPMEENTT AAND PPHYYSSIICCAALL PPLLAANNIING ... . .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 2200<br />

URBAN ECONOMIC DEVELOPMENT ......................................................................................... 20<br />

3.1.1 OCCUPATIONAL PATTERN ................................................................................................................... 20<br />

3.2 PHYSICAL PLANNING .................................................................................................................... 21<br />

3.2.1 PHYSICAL GROWTH TREND .................................................................................................................. 21<br />

3.2.2 LAND USE ANALYSIS ............................................................................................................................ 22<br />

3.2.3 LAND RATES ......................................................................................................................................... 23<br />

3.3 GROWTH MANAGEMENT ISSUES ............................................................................................... 23<br />

44<br />

4.1<br />

SSTTAAKEEHOLLDEERRSS CCONSSULLTTAATTIIONSS ... . .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 2244<br />

CITY OPINION SURVEY .................................................................................................................. 24<br />

4.2 KEY ISSUES HIGHLIGHTED IN THE CONSULTATION MEETING ................................................ 24<br />

4.2.1 SECTOR PRIORITISATION ...................................................................................................................... 25<br />

A. PHYSICAL INFRASTRUCTURE PRIORITY ................................................................................................... 25<br />

B. SOCIAL INFRASTRUCTURE PRIORITY: ...................................................................................................... 26<br />

C. ENVIRONMENTAL ISSUES ...................................................................................................................... 27<br />

55<br />

5.1<br />

VVIISSI IOON AAND SSTTRRAATTEEGIICC PPLLAAN .. . .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 2288<br />

TOWN LEVEL SWOT........................................................................................................................ 28<br />

5.2 VISION FORMULATION ................................................................................................................. 29<br />

5.3 STRATEGY OPTION FOR ECONOMIC DEVELOPMENT ........................................................... 30<br />

5.4 ROTECTION OF PALAR RIVER BASIN ......................................................................................... 33<br />

66 HOUSSIING AAND SSLLUMSS .. . .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 3366<br />

6.1 EXISTING HOUSING SCENARIO ................................................................................................... 36<br />

6.1.1 HOUSING CONDITION ......................................................................................................................... 36<br />

6.1.2 HOUSING STOCK ................................................................................................................................. 36<br />

6.1.3 EXISTING HOUSING DEMAND- SUPPLY GAP ........................................................................................ 37<br />

6.2 EXISTING SLUM SCENARIO ........................................................................................................... 37<br />

6.2.1 SLUM POPULATION .............................................................................................................................. 37<br />

6.2.2 SLUM IMPROVEMENT PROGRAMMES ................................................................................................... 40<br />

do<br />

- i -<br />

Voyants Solutions Private Limited

do<br />

- ii -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

6.3 ISSUES ................................................................................................................................................ 40<br />

6.4 PROPOSAL ...................................................................................................................................... 40<br />

6.5 SWOT ANALYSIS ............................................................................................................................. 40<br />

6.6 CONCLUSION ................................................................................................................................. 41<br />

77 IINSSTTIITTUTTIIONAALL FFRRAAMEEWORRK .. . .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 4422<br />

7.1 ELECTED COUNCIL ........................................................................................................................ 42<br />

7.2 EXECUTIVE WING ........................................................................................................................... 43<br />

7.2.1 GENERAL ADMINISTRATION ................................................................................................................. 43<br />

7.2.2 HEALTH SECTION ................................................................................................................................. 44<br />

7.2.3 ENGINEERING SECTION ....................................................................................................................... 44<br />

7.2.4 TOWN PLANNING SECTION.................................................................................................................. 44<br />

7.2.5 ACCOUNTS SECTION ........................................................................................................................... 44<br />

7.3 CITIZENíS CHARTER ........................................................................................................................ 45<br />

7.4 INFORMATION CENTRE ................................................................................................................ 45<br />

7.5 STAFF STRENGTH POSITION AND VACANCY POSITION ........................................................ 45<br />

7.6 ADDITIONAL STAFF REQUIREMENT: ............................................................................................ 46<br />

7.7 INSTITUTIONAL FRAMEWORK FOR SERVICE DELIVERY ........................................................... 47<br />

7.8 ORGANIZATION MANAGEMENT ................................................................................................ 48<br />

88<br />

8.1<br />

URRBBAAN IINFFRRAASSTTRRUCCTTURREE AAND SSEERRVVIICCEESS .. . ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 4499<br />

WATER SUPPLY ................................................................................................................................ 49<br />

8.1.1 EXISTING SCENARIO FOR WATER SUPPLY ............................................................................................. 49<br />

8.1.2 SOURCES ............................................................................................................................................. 50<br />

8.1.3 STORAGE AND DISTRIBUTION NETWORK ............................................................................................... 53<br />

8.1.4 DEMAND SUPPLY SCENARIO ............................................................................................................... 55<br />

8.1.5 PERFORMANCE INDICATORS ............................................................................................................... 56<br />

8.1.6 ISSUES IN WATER SUPPLY SECTOR ......................................................................................................... 56<br />

8.1.7 PROPOSALS ......................................................................................................................................... 57<br />

8.2 SEWERAGE AND SANITATION ..................................................................................................... 57<br />

8.2.1 EXISTING SEWERAGE ............................................................................................................................ 57<br />

8.2.2 SANITATION ......................................................................................................................................... 57<br />

8.2.3 ISSUES IN SANITATION SECTOR.............................................................................................................. 58<br />

8.2.4 PROPOSALS BY THE MUNICIPALITY / TWAD BOARD ............................................................................ 58<br />

8.3 STORM WATER DRAINAGE .......................................................................................................... 59<br />

8.3.1 EXISTING CONDITION OF STORM WATER DRAINAGE ........................................................................... 59<br />

8.3.2 HOUSEHOLD CONNECTIVITY TO DRAINAGE ......................................................................................... 60<br />

8.3.3 PERFORMANCE INDICATORS ............................................................................................................... 61<br />

8.3.4 ISSUES IN DRAINAGE SECTOR ............................................................................................................... 61<br />

8.3.5 PROPOSALS ......................................................................................................................................... 61<br />

8.4 SOLID WASTE MANAGEMENT ..................................................................................................... 61<br />

8.4.1 GENERATION OF SOLID WASTE ............................................................................................................ 61<br />

8.4.2 COLLECTION OF SOLID WASTE ............................................................................................................ 62<br />

8.4.3 TRANSPORTATION FACILITIES ................................................................................................................ 63<br />

8.4.4 DISPOSAL OF SOLID WASTE ................................................................................................................. 64<br />

8.4.5 PERFORMANCE INDICATORS ............................................................................................................... 64<br />

8.4.6 ISSUES IN SOLID WASTE MANAGEMENT SECTOR................................................................................... 65<br />

8.4.7 PROPOSAL ........................................................................................................................................... 65<br />

8.5 STREET LIGHTING ............................................................................................................................ 65<br />

Voyants Solutions Private Limited

do<br />

- iii -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

8.5.1 STATUS OF STREET LIGHTING ................................................................................................................. 65<br />

8.5.2 PERFORMANCE INDICATORS ............................................................................................................... 67<br />

8.5.3 ISSUES .................................................................................................................................................. 67<br />

8.5.4 PROPOSALS ......................................................................................................................................... 67<br />

8.6 TRAFFIC AND TRANSPORTATION ............................................................................................... 68<br />

8.6.1 REGIONAL LINKAGES- ROADS, RAILWAYS AND AIRWAYS .................................................................... 68<br />

8.6.2 TOWN LEVEL ROAD NETWORK AND HIERARCHY .................................................................................. 68<br />

8.6.3 NATIONAL AND STATE HIGHWAY ......................................................................................................... 68<br />

8.6.4 MUNICIPAL ROADS ............................................................................................................................. 68<br />

8.6.5 PARKING ............................................................................................................................................. 69<br />

8.6.6 PUBLIC TRANSPORT SYSTEM ................................................................................................................. 69<br />

8.6.7 ISSUES IN TRAFFIC AND TRANSPORTATION SECTOR ............................................................................... 69<br />

8.6.8 PROPOSAL FOR ROAD ........................................................................................................................ 70<br />

8.7 SOCIAL INFRASTRUCTURE FACILITIES ........................................................................................ 70<br />

8.8 EDUCATIONAL FACILITIES ............................................................................................................ 70<br />

8.8.1 EXISTING SCENARIO IN EDUCATIONAL FACILITIES ................................................................................. 71<br />

8.8.2 ISSUES IN EDUCATIONAL SECTOR ......................................................................................................... 71<br />

8.8.3 PROPOSAL .......................................................................................................................................... 72<br />

8.9 HEALTH FACILITIES .......................................................................................................................... 72<br />

8.9.1 ISSUES .................................................................................................................................................. 72<br />

8.9.2 PROPOSAL ...................................................................................................................................... 73<br />

8.10 PARKS ............................................................................................................................................... 73<br />

8.10.1 ISSUES ................................................................................................................................................ 73<br />

8.10.2 PROPOSAL ...................................................................................................................................... 73<br />

8.11 MARKETS .......................................................................................................................................... 73<br />

8.11.1 ISSUES ................................................................................................................................................ 73<br />

8.12 SLAUGHTER HOUSE........................................................................................................................ 73<br />

8.12.1 ISSUES ................................................................................................................................................ 73<br />

8.13 BURIAL GROUND ........................................................................................................................... 73<br />

8.13.1 ISSUES ................................................................................................................................................ 74<br />

99<br />

9.1<br />

MUNI ICCIIPPAALL FFIINAANCCEE ... . .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 7755<br />

INTRODUCTION TO URBAN LOCAL BODY FINANCIALS: ...................................................... 75<br />

9.2 GENERAL DETAILS .......................................................................................................................... 75<br />

9.3 RECEIPTS .......................................................................................................................................... 75<br />

9.3.1 PROPERTY TAX ..................................................................................................................................... 75<br />

9.3.2 PROFESSION TAX ................................................................................................................................. 77<br />

9.3.3 ASSIGNED REVENUES ........................................................................................................................... 78<br />

9.3.4 REVENUE DEVOLUTION FUNDS IN AID OF REVENUE EXPENDITURE .......................................................... 78<br />

9.3.5 WATER CHARGES ............................................................................................................................... 79<br />

9.3.6 DRAINAGE CHARGES.......................................................................................................................... 80<br />

9.3.7 SERVICE CHARGES & FEES .................................................................................................................. 81<br />

9.3.8 INCOME FROM PROPERTIES & OTHER INCOME .................................................................................... 81<br />

9.4 EXPENDITURE ................................................................................................................................... 82<br />

9.4.1 ESTABLISHMENT EXPENSES .................................................................................................................... 82<br />

9.4.2 O&M EXPENSES ñ WATER SUPPLY ...................................................................................................... 82<br />

9.4.3 O&M EXPENSES ñ STREET LIGHTS & OTHERS ....................................................................................... 83<br />

9.4.4 ADMINISTRATION & OTHER EXPENSES .................................................................................................. 84<br />

Voyants Solutions Private Limited

do<br />

- iv -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

9.5 SUMMARY OF FINANCES ............................................................................................................. 84<br />

9.6 KEY FINANCIAL INDICATORS .................................................................................................... 88<br />

9.6.1 RESOURCE MOBILISATION INDICATORS ................................................................................................ 88<br />

9.6.2 FUND APPLICATION INDICATORS ......................................................................................................... 88<br />

9.6.3 LIABILITY MANAGEMENT INDICATORS .................................................................................................. 89<br />

9.6.4 OVERALL FINANCIAL PERFORMANCE INDICATORS .............................................................................. 89<br />

9.6.5 EFFICIENCY INDICATORS ...................................................................................................................... 90<br />

9.7 MEASURES TO BE TAKEN FOR IMPROVING COLLECTION EFFICIENCY ............................. 90<br />

1100 CCAAPPIITTAALL IINVVEESSTTMEENTT NEEEEDDSS FFORR IIDEENTTIIFFIIEED PPRROJJEECCTTSS ... . .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. 9933<br />

10.1 PHYSICAL INFRASTRUCTURE - IMPROVEMENT NEEDS ........................................................... 94<br />

10.1.1 WATER SUPPLY: ................................................................................................................................... 94<br />

10.1.2 SEWERAGE SYSTEM .............................................................................................................................. 98<br />

10.1.3 DRAINAGE .......................................................................................................................................... 98<br />

10.1.4 SOLID WASTE MANAGEMENT .............................................................................................................. 99<br />

10.1.5 STREET LIGHT...................................................................................................................................... 101<br />

10.1.6 ROADS AND TRANSPORTATION .......................................................................................................... 102<br />

10.1.7 EDUCATIONAL INSTITUTIONS ............................................................................................................... 102<br />

10.1.8 HEALTH FACILITIES.............................................................................................................................. 103<br />

10.1.9 PARKS AND PLAY GROUND .............................................................................................................. 103<br />

10.1.10 MARKET DEVELOPMENT .................................................................................................................... 104<br />

10.1.11 SLAUGHTER HOUSE DEVELOPMENT .................................................................................................... 105<br />

10.1.12 BURIAL GROUND DEVELOPMENT ....................................................................................................... 105<br />

10.1.13 SLUM IMPROVEMENT ......................................................................................................................... 106<br />

10.1.14 SYSTEM IMPROVEMENT AND E-GOVERNANCE ................................................................................... 107<br />

10.2 OTHER DEPARTMENTAL WORKS ....................................................................................................... 108<br />

1111<br />

11.1<br />

RRIISSKK AAND MIITTIIGAATTIION MEEAASSURREESS .. . ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... . 111100<br />

PROJECT RISKS AND MITIGATE MEASURES ............................................................................ 110<br />

1122<br />

12.1<br />

RREEFFORRMSS AAND AACCTTIION PPLLAAN .. . ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... . 111144<br />

PRESENT SCENARIO IN URBAN REFORMS .............................................................................. 114<br />

12.2 PROPOSED INTERVENTIONS AT STATE LEVEL ......................................................................... 115<br />

12.3 PROPOSED INTERVENTION AT MUNICIPAL LEVEL ................................................................ 118<br />

12.4 STRATEGIES FOR ENVIRONMENTAL IMPROVEMENT ............................................................ 118<br />

12.5 REFORMS IN RESOURCE MOBILISATION ................................................................................. 119<br />

12.6 ACTION PLAN: IMPROVING REVENUE FROM OWN SOURCES ........................................ 119<br />

12.2 ROAD MAP - IMPROVING REVENUE FROM OWN SOURCES ................................................................ 121<br />

12.7 ACTION PLAN : IMPROVING REVENUE FROM USER CHARGES ....................................... 121<br />

12.8 ACTION PLAN: FORMATION OF NEW SUSTAINABLE REVENUE BASES ............................. 122<br />

12.9 ACTION PLAN: PRIVATISATION INITIATIVES ............................................................................ 124<br />

12.10 ACTION PLAN: ENERGY & RESOURCE EFFICIENCY ............................................................. 125<br />

12.11 ACTION PLAN: COMPUTERIZATION AND E-GOVERNANCE ................................................................. 127<br />

12.12 ACTION PLAN: ACCOUNTS AND AUDITING ......................................................................... 128<br />

12.13 ACTION PLAN: INSTITUTIONAL MANAGEMENT ..................................................................... 128<br />

12.14 CAPACITY BUILDING FOR ELECTED REPRESENTATIVES AND COMMITTEE MEMBERS .. 128<br />

12.15 CAPACITY BUILDING FOR ULB STAFF ...................................................................................... 129<br />

12.16 FORMS IN MUNICIPAL SERVICE DELIVERY ............................................................................. 132<br />

1133 AASSSSEETT MAANAAGEEMEENTT PPLLAAN .. . ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... . 113333<br />

13.1 ACTIVITIES OF ASSET MANAGEMENT PLAN (AMP) .............................................................. 133<br />

Voyants Solutions Private Limited

do<br />

- v -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

13.2 INFRASTRUCTURE ASSETS ............................................................................................................ 134<br />

13.2.1 MOVABLE AND IMMOVABLE ASSETS................................................................................................... 134<br />

13.3 PRIORITY ASSET MANAGEMENT OPTIONS .............................................................................. 136<br />

13.4 PROPOSED NEW ASSETS ............................................................................................................ 137<br />

1144 FFIINAANCCIIAALL AAND OPPEERRAATTIING PPLLAAN .. . ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... . 113399<br />

14.1 CAPITAL INVESTMENT PLAN ...................................................................................................... 139<br />

14.2 OTHER PROJECTS AND ON GOING PROJECTS .................................................................... 141<br />

14.3 MEANS OF FINANCE ................................................................................................................... 142<br />

14.4 FINANCIAL SUSTAINABILITY ........................................................................................................ 148<br />

14.5 BASIC ASSUMPTIONS FOR PROJECTIONS : ............................................................................ 149<br />

14.5.1 PROPERTY TAX ................................................................................................................................... 149<br />

14.5.2 PROFESSION TAX ............................................................................................................................... 150<br />

14.5.3 ASSIGNED REVENUE ........................................................................................................................... 150<br />

14.5.4 DEVOLUTION FUND ........................................................................................................................... 150<br />

14.5.5 SERVICE CHARGES AND FEES ............................................................................................................. 150<br />

14.5.6 GRANT AND CONTRIBUTION .............................................................................................................. 151<br />

14.5.7 SALES AND HIRE CHARGES ................................................................................................................ 151<br />

14.5.8 OTHER INCOME ................................................................................................................................. 151<br />

14.5.9 WATER SUPPLY CHARGES ................................................................................................................. 151<br />

14.5.10 DRAINAGE CHARGES........................................................................................................................ 152<br />

14.5.11 SOLID WASTE MANAGEMENT ............................................................................................................. 153<br />

14.5.12 BUS STAND ........................................................................................................................................ 153<br />

14.5.13 MARKETS ........................................................................................................................................... 153<br />

14.5.14 REMUNERATIVE PROJECTS ................................................................................................................. 154<br />

14.5.15 SLAUGHTER HOUSE & GASIFIER CREMATORIUM ................................................................................ 154<br />

14.5.16 ADVERTISEMENTS ............................................................................................................................... 154<br />

14.5.17 PARKING FEES ................................................................................................................................... 155<br />

14.5.18 EXPENDITURE ..................................................................................................................................... 155<br />

14.5.19 OPERATION AND MAINTENANCE ...................................................................................................... 155<br />

14.5.20 POWER CHARGES ............................................................................................................................. 156<br />

14.5.21 INTEREST ............................................................................................................................................ 156<br />

14.5.22 DEPRECIATION .................................................................................................................................. 156<br />

14.5.23 PROVISION OF DOUBTFUL DEBTS ......................................................................................................... 156<br />

14.5.24 COLLECTIONS ................................................................................................................................... 156<br />

14.5.25 ANNUITY FACTOR .............................................................................................................................. 157<br />

14.6 PROJECT CASH FLOWS AND FOP RESULTS : ......................................................................... 158<br />

14.7 IMPACT OF POTENTIAL IMPROVEMENTS ................................................................................ 165<br />

14.8 SCENARIO I - ESTIMATION OF INVESTMENT CAPACITY ON AS IS WHERE BASIS............ 166<br />

14.9 SCENARIO II ñ ESTIMATION OF BORROWING AND INVESTMENT CAPACITY WITH<br />

METUR CWSS. ................................................................................................................................ 166<br />

14.10 SCENARIO III ñ ESTIMATION OF BORROWING AND INVESTMENT CAPACITY WITHOUT<br />

METUR CWSS. ................................................................................................................................ 167<br />

14.11 KEY INDICATOR OF SCENARIO II (FULL PROJECT SCENARIO WITH METUR CWSS). ..... 167<br />

14.12 INFERENCE. ................................................................................................................................... 168<br />

AANNEEXXURREE .. . ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... .. .. ... .. ... . 117711<br />

Voyants Solutions Private Limited

do<br />

LIST OF FIGURES<br />

- vi -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

Figure 2-1: Regional Setting of Ambur <strong>Municipal</strong>ity ............................................................ 17<br />

Figure 3-1: Town map ñ Ambur <strong>Municipal</strong>ity ........................................................................ 22<br />

Figure 4-1: Priorities for Physical Infrastructure ...................................................................... 25<br />

Figure 4-2: Priorities for Social Infrastructure .......................................................................... 26<br />

Figure 4-3: Priorities for Environment Issues ............................................................................ 27<br />

Figure 5-1: Chennai-Bengaluru Industrial corridor of excellence .................................... 31<br />

Figure 5-2: Key Environmental Issues ñPalar River Basin ..................................................... 35<br />

Figure 6-1: Break- Up of Housing Condition .......................................................................... 36<br />

Figure 6-2: Ambur <strong>Municipal</strong>ity ................................................................................................ 39<br />

Figure 7-1: Organisational structure of Ambur <strong>Municipal</strong>ity .............................................. 43<br />

Figure 8-1: Break up of Water Supply Connections ........................................................... 49<br />

Figure 8-2: Schematic water supply flow diagram for Ambur <strong>Municipal</strong>ity .................. 54<br />

Figure 8-3: Status of Toilet Facility in Ambur Town ............................................................... 58<br />

Figure 10-1: Mettur Combined Water Supply Scheme ...................................................... 95<br />

Figure 10-2 : Site Identification for Landfill ...........................................................................100<br />

Voyants Solutions Private Limited

do<br />

LIST OF TABLES<br />

- vii -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

Table 2-1: Urban Population Share in the Town and the Region ..................................... 17<br />

Table 2-2: Population Growth in Ambur <strong>Municipal</strong>ity ......................................................... 18<br />

Table 2-3: Population projection ............................................................................................. 18<br />

Table 2-4: Comparative Population Density ........................................................................ 19<br />

Table 2-5: Comparative Sex Ratio .......................................................................................... 19<br />

Table 2-6: Comparative Literacy Rate .................................................................................. 19<br />

Table 3-1: Work Force Participation Ratio in Ambur Town ................................................ 20<br />

Table 3-2: Occupational classification of Main Workers in Ambur Town ....................... 21<br />

Table 3-3: Land Use Allocation- Ambur-1984 ....................................................................... 22<br />

Table 5-1 Town level SWOT ....................................................................................................... 28<br />

Table 6-1: Housing Condition ................................................................................................... 36<br />

Table 6-2: Existing Housing Stock ............................................................................................. 37<br />

Table 6-3: Existing Demand- Supply Gap .............................................................................. 37<br />

Table 6-4: Existing Slum Population ......................................................................................... 37<br />

Table 6-5: Details of infrastructure available in slums ......................................................... 38<br />

Table 6-6: Proposal for Integrated Housing and Slum Development Programme<br />

(IHSDP) .......................................................................................................................................... 40<br />

Table 7-1: Existing Staff Strength .............................................................................................. 45<br />

Table 7-2: Additional Staff Requirement ............................................................................... 47<br />

Table 7-3: Institutional Framework for Urban Service Delivery .......................................... 47<br />

Table 8-1: Break up of Water Supply Connections ............................................................. 49<br />

Table 8-2: Classification of Sources of Water by type in Ambur ...................................... 50<br />

Table 8-3: Details of Scheme and Head works .................................................................... 50<br />

Table 8-4: Location of Reservoirs and Sumps ....................................................................... 53<br />

Table 8-5: Water Supply Distribution Details in Ambur Town ............................................. 55<br />

Table 8-6: Supply gap Analysis ................................................................................................ 55<br />

Table 8-7: Sanitation Facilities .................................................................................................. 57<br />

Table 8-8: Classification of modes of sanitary waste disposal by type ........................... 58<br />

Table 8-9-Zone wise demand Estimation for Provision Sewerage Facilities ................... 59<br />

Table 8-10-Under Ground Drainage system ñSalient Features ......................................... 59<br />

Table 8-11: Storm Water Drainage Coverage ..................................................................... 60<br />

Table 8-12: Existing Drainage Scenario .................................................................................. 60<br />

Table 8-13: Sources of Waste Generated from Ambur <strong>Municipal</strong>ity ............................... 62<br />

Table 8-14: Zone-Wise Collection............................................................................................ 62<br />

Table 8-15: Solid Waste Practices in Ambur Town ............................................................... 62<br />

Table 8-16: Number and Type of dustbins for waste collection ....................................... 63<br />

Table 8-17: Detail of Vehicles for Solid Waste Management in Ambur <strong>Municipal</strong>ity .. 63<br />

Table 8-18: Number and Type of vehicles used for Transportation ................................. 64<br />

Table 8-19: Number of Street Lights in Ambur <strong>Municipal</strong>ity ............................................... 66<br />

Table 8-20: Length of National Highways Passing through Ambur .................................. 68<br />

Voyants Solutions Private Limited

do<br />

- viii -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

Table 8-21: Types of Roads in Ambur <strong>Municipal</strong>ity .............................................................. 69<br />

Table 8-22: Roads by Hierarchy .............................................................................................. 69<br />

Table 8-23: Details of Education Facilities ............................................................................. 70<br />

Table 8-24: Existing Educational facilities in Ambur ............................................................. 71<br />

Table 8-25: Existing Health facilities in Ambur Town ............................................................ 72<br />

Table 9-1- Property Tax Components .................................................................................... 76<br />

Table 9-2- Property Tax Assessments ...................................................................................... 76<br />

Table 9-3- Property Tax ñ Growth during last 6 years .......................................................... 76<br />

Table 9-4 - Property Tax ñ Demand Collection % ................................................................ 76<br />

Table 9-5- Profession Tax ñ Growth during last 6 years ....................................................... 77<br />

Table 9-6- Profession Tax ñ Demand Collection % .............................................................. 77<br />

Table 9-7- Assigned Revenue ñ Growth & % of Total Income........................................... 78<br />

Table 9-8 - Devolution Fund ñ Growth & % of Total Income (Rs. In Lacs) ...................... 79<br />

Table 9-9 -Water Tariff & Deposit............................................................................................. 79<br />

Table 9-10- No. of House Service Connections.................................................................... 79<br />

Table 9-11 - Water Charges ñ Growth & % of Total Income (Rs. in Lacs) ..................... 79<br />

Table 9-12 - Water Connection Charges ñ Growth & % of Total Income (Rs.in Lacs)<br />

....................................................................................................................................................... 80<br />

Table 9-13 - Water Charges ñ Demand Collection % (Rs. in Lacs) ................................ 80<br />

Table 9-14 - Service Charges & Fees ñ Growth & % of Total Income (Rs. in Lacs) ...... 81<br />

Table 9-15 - Income from Properties & Other Income ñ Growth & % of Total Income 81<br />

Table 9-16 - Non Tax Income ñ Demand Collection % (Rs. in Lacs) ............................... 82<br />

Table 9-17 - Establishment Expenses ñ Growth & % of Total Expenditure (Rs. in Lacs) . 82<br />

Table 9-18 - O&M Expenses (Water Supply) ñ Growth & % of Total Expenditure (Rs. in<br />

Lacs).............................................................................................................................................. 83<br />

Table 9-19 - O&M Expenses (Street Lights & Others) ñ Growth & % of Total Expt (Rs. in<br />

Lacs).............................................................................................................................................. 83<br />

Table 9-20 - Administration Expenses ñ Growth & % of Total Expenditure- (Rs. in<br />

Lacs).............................................................................................................................................. 84<br />

Table 9-21- Summary of Finances for last 6 years (Rs. in Lacs) ......................................... 84<br />

Table 9-22 - Head-wise Income & Expenditure for last 6 years (Rs. in Lacs) ................. 85<br />

Table 9-23 - Borrowings of the <strong>Municipal</strong>ity (Rs. in Lacs) .................................................... 86<br />

Table 9-24 - Status of Contributions & Grants ....................................................................... 86<br />

Table 9-25 - Resource Mobilisation Indicators ...................................................................... 88<br />

Table 9-26- Fund Application Indicators ............................................................................... 89<br />

Table 9-27- Liability Management Indicators ....................................................................... 89<br />

Table 9-28 - Financial Performance Indicators .................................................................... 90<br />

Table 9-29 - Efficiency Indicators ............................................................................................ 90<br />

Table 10-1: Summery of Capital Investments under CCCBP ............................................ 93<br />

Table 10-2- : Water source to meet intermediate and Ultimate Demand .................... 96<br />

Table 10-3: Investment requirement in water supply sector for Ambur <strong>Municipal</strong>ity .. 97<br />

Table 10-4: Capital Investment Needs for the Sewerage System.................................... 98<br />

Voyants Solutions Private Limited

do<br />

- ix -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

Table 10-5: Capital Investment Needs for the Storm Water Drainage System ............. 99<br />

Table 10-6: Capital Investment Needs for the Solid Waste Management ..................101<br />

Table 10-7: Capital Investment Needs for the Street Light ..............................................102<br />

Table 10-8: Capital Investment Needs for the Roads and Transportation ...................102<br />

Table 10-9: Capital Investment Needs for the Educational Institutions ........................103<br />

Table 10-10: Capital Investment Needs for the Health Facilities ....................................103<br />

Table 10-11: Capital Investment Needs for the Parks and Play Grounds .....................104<br />

Table 10-12: Capital Investment Needs for the Market Development .........................105<br />

Table 10-13: Capital Investment Needs for the Slaughter House Development ........105<br />

Table 10-14: Capital Investment Needs for the Burial Ground .......................................106<br />

Table 10-15: Capital Investment Needs for the Slum Improvement..............................106<br />

Table 10-16: Capital Investment Needs for the e-Governance .....................................107<br />

Table 10-17: Projects to be taken by other departments ................................................109<br />

Table 11-1: As per the Guidelines on Environmental & Social Concerns of CCCBP<br />

projects ñ Ambur ......................................................................................................................110<br />

Table 12-1: Road Map ñ Environmental improvement ....................................................119<br />

Table 12-2: Road Map Improving revenue from user charges ......................................122<br />

Table 12-3: Road Map for Formation of new sustainable revenue bases ...................123<br />

Table 12-4: Road Map for Privatization initiatives ..............................................................125<br />

Table 12-5: Road Map for Energy and Resource efficiency ...........................................126<br />

Table 12-6: Road map for Computerization and E-Governance ..................................127<br />

Table 12-7: Technical Assistance for Elected representatives ........................................128<br />

Table 12-8: Technical Assistance for ULB staff ....................................................................129<br />

Table 12-9: Road map for Accounts & auditing and Institutional Management ......130<br />

Table 12-10: Road map for implementation of all projects ............................................131<br />

Table 12-11: Road map Reform Agenda <strong>Municipal</strong> Service Delivery ..........................132<br />

Table 13-1: Land Assets ñ Proposed use ..............................................................................136<br />

Table 13-2: Income Details from Remunerative Assets ....................................................136<br />

Table 13-3: Income from Proposed new Projects..............................................................137<br />

Table 13-4: New Assets for the year -2009-10 to 2013 -14 ................................................138<br />

Table 14-1: Projects to be executed by the <strong>Municipal</strong>ity ................................................139<br />

Table 14-2: Projects under Implementation by the <strong>Municipal</strong>ity ...................................142<br />

Table 14-3: Multi Year Investment <strong>Plan</strong> and Means of Finance .....................................142<br />

Table 14-4: Consolidated Means of Finance .....................................................................148<br />

Table 14-5: Ratio of Property tax ...........................................................................................150<br />

Table 14-6: Water supply Charges ñ Existing ......................................................................151<br />

Table 14-7: House Service Connections - Percentage ....................................................152<br />

Table 14-8: Sewage Charges ................................................................................................152<br />

Table 14-9: Assumptions - Increase in Expenditure ...........................................................155<br />

Table 14-10: Assumptions ñ O&M ..........................................................................................155<br />

Table 14-11: Assumptions ñ Provision of doubtful debts ...................................................156<br />

Table 14-12: Assumptions ñ Property tax collection ..........................................................156<br />

Voyants Solutions Private Limited

do<br />

- x -<br />

Final Report: Ambur <strong>Municipal</strong>ity<br />

Table 14-13: Assumptions ñ Profession tax ...........................................................................157<br />

Table 14-14: Assumptions ñ Other Non Tax Income ..........................................................157<br />

Table 14-15: Assumptions ñ Water Charges ........................................................................157<br />

Table 14-16: Assumptions ñ Drainage Charges .................................................................157<br />

Table 14-17: Terms of Loan Funding for Proposed Investments ......................................158<br />

Table 14-18: Consolidated Income & Expenditure for next 20 years (up to FY 2028-29)<br />

.....................................................................................................................................................159<br />

Table 14-19: Consolidated Balance Sheet for next 20 years (up to FY 2028 ñ 29)......161<br />

Table 14-20: Key Indicators ....................................................................................................168<br />

Voyants Solutions Private Limited

Chapter - 1 Final Report: Ambur <strong>Municipal</strong>ity<br />

1 BACKGROUND AND METHODOLOGIICAL<br />

FRAMEWORK OF THE STUDY<br />

1.1. BACKGROUND<br />

The Tamil Nadu Urban Infrastructure Financial Services Limited (TNUIFSL) aims to assist<br />

Ambur <strong>Municipal</strong>ity in strengthening and improving its financial position for effective<br />

capital investment management and urban service delivery. The municipality has<br />

good potential for immediate implementation of financial reforms for which it is<br />

essential to formulate a <strong>City</strong> <strong>Corporate</strong> Cum <strong>Business</strong> <strong>Plan</strong> (CCCBP).<br />

The CMA and TNUIFSL have initiated the process of preparing CCCBP for the<br />

municipality with the vision of stakeholdersí growth of the town.<br />

1.2. OBJECTIVES<br />

The objective of this exercise is to visualise the town in the next 25 -30 years and<br />

1. Define the growth direction and service up-gradations in relation to the<br />

do<br />

activity mix / growth;<br />

2. Assess the demand for the projects specified by the ULB, and come out with<br />

gap in services with respect to the vision;<br />

3. Broadly outline the infrastructure needs;<br />

4. Define specific rehabilitation of infrastructure and capital improvement needs<br />

with regard to provision of infrastructure in slums and other areas;<br />

5. Indicate the priority of projects<br />

6. Define revenue enhancement and revenue management improvements<br />

required to sustain the rehabilitation proposed;<br />

7. Suggest reforms required in local administration and service delivery including<br />

public private partnership in infrastructure development<br />

8. Suggest Measures to address common growth and infrastructure issues and to<br />

promote integrated development<br />

1.3. SCOPE OF WORK<br />

The scope of work covers the following:<br />

1. To assess the demand for the Projects listed out by these municipalities.<br />

2. Financial Assessment of the ULBS- an assessment of the ULB finances for the past<br />

5 years, in terms of sources and uses of funds, base and basis of levy, revision<br />

history and impacts, state assignment and transfer-base and basis of transfer<br />

and its predictability; use of funds outstanding liabilities (loans, power dues,<br />

pension etc) and a review of revenue and service management arrangements.<br />

- 11 -<br />

Voyants Solutions Private Limited

Chapter - 1 Final Report: Ambur <strong>Municipal</strong>ity<br />

do<br />

Levels of service and quality of municipal services in both poor and non-poor<br />

localities. Staffing and management arrangements in delivery of services.<br />

3. Outline issues in revenue realisation, quality of existing assets in relation to service<br />

levels and coverage and institutional constraints. Develop quick indicators of<br />

performance, based on the following:<br />

Current coverage and additional population during medium term (10 years)<br />

Unit cost indicates city level investment requirements for Up-gradation of<br />

city wide infrastructures.<br />

To improve service coverage and asset quality<br />

Define priority assets and indicative costs of rehabilitation<br />

Conduct fiscal impact analysis of investments: life-cycle of O&M costs,<br />

revenues from project and costs/impacts on finances and of not doing the<br />

project.<br />

Explore funding options for rehabilitation facilities.<br />

4. Prepare a financial and operating plan (FOP). The FOP in the medium time frame<br />

works for the ULBs and shall present the following.<br />

A. Areas of reduction in expenditure<br />

Energy audit resulting in savings energy.<br />

Leak detection resulting either in connection or in the tariff (or)<br />

Privatizing the MSW collection and identifying a BOT operator for eliminating,<br />

composting etc, items of revenue can be identified.<br />

Laying of cement concrete road /Fly ash and savings on a maintenance cost<br />

resulting in increasing operating surplus.<br />

Water recycling /refuse<br />

Rejuvenation of tanks and reduction of cost/liters of water produced<br />

Privatization & options for raising revenue<br />

B. Options for increasing the revenues through non traditional methods<br />

Land development for raising revenues<br />

Suggestions for improvement of revenues.<br />

5 Prepare a draft Memorandum of Association (MoA) between ULB and TNUIFSL.<br />