Second Half 2011 Focus on the Horizon - Kantar Retail

Second Half 2011 Focus on the Horizon - Kantar Retail

Second Half 2011 Focus on the Horizon - Kantar Retail

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

<str<strong>on</strong>g>Sec<strong>on</strong>d</str<strong>on</strong>g> <str<strong>on</strong>g>Half</str<strong>on</strong>g> <str<strong>on</strong>g>2011</str<strong>on</strong>g> <str<strong>on</strong>g>Focus</str<strong>on</strong>g> <strong>on</strong> <strong>the</strong> Horiz<strong>on</strong>

Design<br />

Jennifer Zipp<br />

Lisa Weiderman<br />

© <str<strong>on</strong>g>2011</str<strong>on</strong>g> – <strong>Kantar</strong> <strong>Retail</strong> LLC. All Rights Reserved.<br />

Disclaimer: The analyses and c<strong>on</strong>clusi<strong>on</strong>s presented herein represent <strong>the</strong> opini<strong>on</strong>s of <strong>Kantar</strong> <strong>Retail</strong>. The views expressed in this publicati<strong>on</strong> do<br />

not necessarily reflect <strong>the</strong> views of <strong>the</strong> companies covered by this publicati<strong>on</strong>. This publicati<strong>on</strong> is not endorsed, or o<strong>the</strong>rwise supported, by <strong>the</strong><br />

management of any of <strong>the</strong> companies covered herein.<br />

Copyright Notice: No part of this publicati<strong>on</strong> may be reproduced in any form or by any means without <strong>the</strong> express written permissi<strong>on</strong> of <strong>the</strong><br />

copyright owner.<br />

96 Breakthrough Insights<br />

/ Research Team<br />

Sara Al-Tukhaim<br />

Frank Badillo<br />

Jessica Campbell<br />

Wils<strong>on</strong> Chen<br />

Alida Destrempe<br />

Karolina Fiedler<br />

Ray Gaul<br />

Bryan Gildenberg<br />

Kaina Hamed<br />

Doug Hermans<strong>on</strong><br />

Yi Ting Hu<br />

Rema Iyer<br />

Sim<strong>on</strong> Johnst<strong>on</strong>e<br />

Laura Kennedy<br />

Vadim Khetsuriani<br />

Amy Koo<br />

Jim Le<strong>on</strong>ard<br />

Stephen Mader<br />

David Marcotte<br />

Alexandra Mansfield<br />

Rachel McGuire<br />

Le<strong>on</strong> Nicholas<br />

Ivana Nikolic<br />

Mike Paglia<br />

Himanshu Pal<br />

John Rand<br />

Bryan Roberts<br />

Kate Senzamici<br />

Robin Sherk<br />

Steve Spiwak<br />

Xue Fei Sun<br />

Lynne Vantassel<br />

Mary Brett Whitfield<br />

Lisa Wiltshire<br />

Fan Zhang<br />

Anne Zybowski

In This Issue<br />

Foreword 2<br />

<strong>Retail</strong> Insights<br />

UK Online Grocery: Comparis<strong>on</strong> Shopping Trips 5<br />

Online <strong>Retail</strong> in China: Getting Ahead of <strong>the</strong> Curve 14<br />

Adding Clarity or Clutter? A First Look at Walgreens and CVS’s 20<br />

New Private Brands, “Nice!” and “Nuance”<br />

What Target’s Suppliers Need to Know about Walmart Canada 24<br />

Getting it Right: Anticipating Amaz<strong>on</strong>’s Growth Trajectory 34<br />

Tesco Price Drop: Seismic Shift or Smoke and Mirrors? 39<br />

Safeway’s Strategic In-Store Marketing 44<br />

Bey<strong>on</strong>d <strong>the</strong> Box: Costco’s Digital Dive 49<br />

Shopper Insights<br />

Value Discounters C<strong>on</strong>tinue to Attract More Shoppers 59<br />

Where <strong>the</strong> Men Are/Aren’t 67<br />

Shopping Through <strong>the</strong> Eyes of a Low-Income Shopper 73<br />

Ec<strong>on</strong>omic Insights<br />

The Global Macroec<strong>on</strong>omic Outlook for <strong>Retail</strong>: Danger from Europe to China 80<br />

The Macroec<strong>on</strong>omic Outlook for U.S. <strong>Retail</strong>: Pushed Toward Recessi<strong>on</strong> 88

FOREWORD<br />

Welcome to <strong>Kantar</strong> <strong>Retail</strong>’s semi-annual collecti<strong>on</strong> of<br />

Breakthrough Insights—our recent research pieces that we<br />

feel best reflect <strong>the</strong> key issues in <strong>the</strong> rapidly changing retail<br />

landscape.<br />

Many years ago, my fa<strong>the</strong>r took me deep-sea fishing for <strong>the</strong> first time,<br />

and during <strong>the</strong> voyage I began to feel more than a little queasy. My<br />

Dad looked down at me at <strong>on</strong>e point and saw me closing my eyes,<br />

hoping that <strong>the</strong> swells rocking <strong>the</strong> boat would pass. His simple instructi<strong>on</strong><br />

to me at <strong>the</strong> time is something that has stuck with me ever<br />

since:“The <strong>on</strong>ly way you’ll feel better is if you keep your eyes open and<br />

focused <strong>on</strong> <strong>the</strong> horiz<strong>on</strong>. Your eyes will see <strong>the</strong> movement you feel in<br />

your head, and you’ll stop feeling sick.”<br />

I’ve thought of that advice many times over <strong>the</strong> years, and quite frequently<br />

recently as <strong>the</strong> queasiness has come back with a vengeance<br />

in <strong>the</strong> sec<strong>on</strong>d half of <str<strong>on</strong>g>2011</str<strong>on</strong>g>. Those of us in <strong>the</strong> nor<strong>the</strong>astern United<br />

States have experienced hurricanes, earthquakes, tornadoes, floods,<br />

and a freak late autumn blizzard in this six-m<strong>on</strong>th period, and that’s<br />

even before we think about <strong>the</strong> turbulent global ec<strong>on</strong>omic and retail<br />

landscape! I’ve written many times in <strong>the</strong> last six m<strong>on</strong>ths about <strong>the</strong><br />

need to cope more effectively in uncertain and volatile times, but I have gradually come to realize a simple point<br />

that to some degree c<strong>on</strong>tradicts that characterizati<strong>on</strong> of <strong>the</strong> world today: <strong>on</strong>ly infrequent volatility is uncertain.<br />

What we are faced with today, and what <strong>Kantar</strong> <strong>Retail</strong> believes will be <strong>the</strong> modus operandi for <strong>the</strong> global retail<br />

marketplace in 2012 and bey<strong>on</strong>d, is a sort of perpetual volatility—at which point volatility becomes a known that<br />

needs to be planned for, not an unknown that surprises. Management guru Jim Collins builds <strong>on</strong> this idea in his<br />

writings <strong>on</strong> why formerly great companies fail. Great companies are rarely derailed by <strong>the</strong> unknown, as <strong>the</strong> unknown<br />

tends to relatively evenly impact all companies and <strong>the</strong>ir competitors. Great companies that avoid failure<br />

do so with <strong>on</strong>e simple skill: <strong>the</strong> ability to sift through <strong>the</strong> known to find <strong>the</strong> truly important, and to plan and act in a<br />

way that deals with and capitalizes <strong>on</strong> that “known.”<br />

In pursuit of that <strong>the</strong>me, what you will find in <strong>Kantar</strong> <strong>Retail</strong>’s H2 Breakthrough Insights collecti<strong>on</strong> is a series of<br />

works that define <strong>the</strong> major factors that are shaping <strong>the</strong> retail landscape and what <strong>the</strong> strategies should be that<br />

surround those “great big knowns.” To establish <strong>the</strong> case for this more permanent volatility, our Chief Ec<strong>on</strong>omist<br />

Frank Badillo has c<strong>on</strong>tributed two pieces that highlight its root causes and effects: <strong>the</strong> first <strong>on</strong> <strong>the</strong> uncertainty<br />

associated with many of <strong>the</strong> major retail markets around <strong>the</strong> world and <strong>the</strong> sec<strong>on</strong>d focusing <strong>on</strong> <strong>the</strong> c<strong>on</strong>tinued<br />

troubled outlook for <strong>the</strong> U.S. retail envir<strong>on</strong>ment.<br />

2 Breakthrough Insights<br />

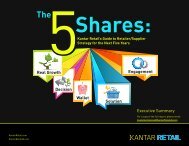

Figure 1: The 5 Shares Map<br />

Share of<br />

Real Growth<br />

Share of<br />

Soluti<strong>on</strong><br />

<strong>Retail</strong>er/<br />

Landscape<br />

Market Evoluti<strong>on</strong><br />

and C<strong>on</strong>diti<strong>on</strong>s<br />

Share of<br />

Wallet<br />

Informati<strong>on</strong><br />

Post-Desktop<br />

Informati<strong>on</strong><br />

Shopper<br />

Post-Recessi<strong>on</strong><br />

Digital Shopper<br />

Share of<br />

Engagement<br />

Share of<br />

Decisi<strong>on</strong><br />

Source: <strong>Kantar</strong> <strong>Retail</strong>

Two framing perspectives provide a lens to view <strong>the</strong> remaining articles. The first is <strong>Kantar</strong> <strong>Retail</strong>’s proprietary “5 Shares”<br />

framework, and <strong>the</strong> sec<strong>on</strong>d is those shares married with <strong>the</strong> fundamental questi<strong>on</strong>s companies will need to grapple with in<br />

order to thrive in this era of perpetual volatility.<br />

Share of Real Growth: Where Will I Grow?<br />

Fans of <strong>Kantar</strong> <strong>Retail</strong>’s analysis will be familiar with our oft-repeated phrase that growth is going to c<strong>on</strong>tinue to come from<br />

less comfortable places. Phil Smiley and Justin Cook profile <strong>on</strong>e of those uncomfortable “knowns”: <strong>on</strong>line retail/e-commerce<br />

in China and how digital commerce today is going to make <strong>the</strong> Chinese retail landscape of tomorrow look foundati<strong>on</strong>ally different<br />

than o<strong>the</strong>r major global markets. We also know that U.S. retailers are increasingly going to be pushed to intensify internati<strong>on</strong>al<br />

expansi<strong>on</strong> as U.S. retail market growth sputters, and Robin Sherk maps out <strong>the</strong> showdown we expect to see as Walmart<br />

and Target square off against <strong>on</strong>e ano<strong>the</strong>r in <strong>the</strong> Canadian market.<br />

“Where will I grow” also is a relevant questi<strong>on</strong> even for U.S.-centric companies. There are unexplored channels, segments,<br />

and niches that though unfamiliar can be sources of real growth. Mary Brett Whitfield previews our findings about arguably<br />

<strong>the</strong> largest under-served shopping populati<strong>on</strong> in <strong>the</strong> United States today—men—by drawing c<strong>on</strong>clusi<strong>on</strong>s from our recently<br />

augmented ShopperScape ® m<strong>on</strong>thly U.S. shopper panel that has been expanded to more precisely analyze male shopping behavior.<br />

For <strong>the</strong> first time, channels such as home improvement, c<strong>on</strong>sumer electr<strong>on</strong>ics, and c<strong>on</strong>venience get a fair shake from<br />

our analysis as <strong>the</strong> male voice is heard more clearly. Gen Xers redefining gender roles at home and marriage-delayed Gen Ys<br />

are resp<strong>on</strong>sible for <strong>the</strong> dramatically increased men’s involvement in shopping and shopping decisi<strong>on</strong>s. <strong>Kantar</strong> <strong>Retail</strong>’s work<br />

here can help our clients develop strategies to capitalize <strong>on</strong> this key known.<br />

Share of Engagement: How Will I Cut Through <strong>the</strong> Clutter and C<strong>on</strong>nect to Shoppers?<br />

The risk of focusing <strong>on</strong> <strong>the</strong> known is in resorting to lazy cliché or not challenging c<strong>on</strong>venti<strong>on</strong>al ideas, and nowhere is this<br />

risk greater in a “known” which needs more dimensi<strong>on</strong>: <strong>the</strong> idea that retailers need to make <strong>the</strong>ir stores “more experiential”<br />

to compete with <strong>on</strong>line competitors. Some retailers do, but in fact, some may compete by making <strong>the</strong>ir stores simpler and<br />

faster to shop instead of more interesting and engaging. <strong>Retail</strong>ers that are enhancing <strong>the</strong>ir store experience need to do so<br />

with a firm eye <strong>on</strong> how that improved experience causes sales increases. As our <strong>Kantar</strong> brethren at TNS are f<strong>on</strong>d of reminding<br />

us, keeping people in <strong>the</strong> store l<strong>on</strong>ger doesn’t necessarily sell more—most retailers that are successful sell and close quickly<br />

and effectively. With that screen in place, Alida Destrempe evaluates Safeway’s attempts to re-invigorate its store experience<br />

and value communicati<strong>on</strong> in a photo-based study.<br />

Share of Decisi<strong>on</strong>: Why Will Shoppers Choose Outlets and Brands?<br />

Price today remains a cornerst<strong>on</strong>e of shopper outlet choice, and <strong>the</strong>re is no c<strong>on</strong>cept more fundamental to <strong>the</strong> relati<strong>on</strong>ship<br />

between retailers, suppliers, and shoppers than price. To a casual reader of <strong>the</strong> newspaper, a short-durati<strong>on</strong> extreme discounting<br />

c<strong>on</strong>cept like Group<strong>on</strong> having a market capitalizati<strong>on</strong> of more than USD10 billi<strong>on</strong> should highlight <strong>on</strong>e simple known:<br />

list price and average selling price are going to become increasingly disassociated from <strong>on</strong>e ano<strong>the</strong>r. The implicati<strong>on</strong>s of this<br />

known are massive and impact virtually every core retail industry process—pricing strategy, promoti<strong>on</strong>, placement, product<br />

availability, branding, and new item strategy. Our price-based analysis this m<strong>on</strong>th takes us to <strong>the</strong> United Kingdom, where<br />

Bryan Roberts highlights <strong>the</strong> offline grocery price battle that has turned into an Orwellian state of permanent total war, and to<br />

<strong>the</strong> United States, where Le<strong>on</strong> Nicholas investigates how low-income shoppers are getting price signals from retailer opening<br />

price point (OPP) assortments and pricing models.<br />

Breakthrough Insights 3

Share of Wallet: How Much Will Shoppers Spend?<br />

Building <strong>on</strong> <strong>the</strong> OPP <strong>the</strong>me, <strong>the</strong> rise of discount formats in various retail markets around <strong>the</strong> world is ano<strong>the</strong>r key known. The<br />

United States in particular is susceptible to this, as it by far <strong>the</strong> largest retail market in <strong>the</strong> world and <strong>on</strong>e with a relatively<br />

large disparity of income (o<strong>the</strong>rwise known as a Gini coefficient). To understand this phenomena in much more detail Dave<br />

Marcotte profiles <strong>the</strong> rise of discounters in <strong>the</strong> United States and shares insights <strong>on</strong> both who is shopping in <strong>the</strong>se stores<br />

and what is driving <strong>the</strong>m <strong>the</strong>re. A few key categories—such as party, occasi<strong>on</strong>s and greeting cards—are resp<strong>on</strong>sible for a<br />

surprisingly high amount of destinati<strong>on</strong> traffic. Understanding this is key to understanding this channel in <strong>the</strong> United States,<br />

Walmart’s c<strong>on</strong>tinued attempts to resp<strong>on</strong>d to it, and to understanding low-income shoppers in general. U.S. shoppers making<br />

less than <strong>the</strong> median household income would be <strong>the</strong> third-largest retail market in <strong>the</strong> world (behind <strong>on</strong>ly <strong>the</strong> wealthy U.S.<br />

shoppers and China) if <strong>the</strong>y were a standal<strong>on</strong>e country.<br />

Share of Soluti<strong>on</strong>: What Will We Sell Shoppers?<br />

Share of wallet’s l<strong>on</strong>g-term cousin is really share of soluti<strong>on</strong>:what can our share of wallet be over time? Brendan Langan<br />

takes this discount phenomen<strong>on</strong> <strong>on</strong> from a different angle and investigates <strong>the</strong> increased competitive intensity as <strong>the</strong> value<br />

channel c<strong>on</strong>tinues to expand into areas traditi<strong>on</strong>ally dominated by drug. In particular, this overlap is now exacerbated by <strong>the</strong><br />

senior leadership at both major U.S. n<strong>on</strong>-food discount operators being veterans of <strong>the</strong> drugstore industry. In this case, <strong>the</strong><br />

major known is that low-income shoppers are increasingly looking to alternative vehicles to stay healthy or cure ailments in an<br />

ec<strong>on</strong>omically challenging envir<strong>on</strong>ment, and <strong>the</strong> value channel will almost certainly play a critical role in this adaptati<strong>on</strong> by <strong>the</strong><br />

bottom tiers of <strong>the</strong> ec<strong>on</strong>omic pyramid.<br />

Ano<strong>the</strong>r retailer seeking to aggressively expand its footprint from a soluti<strong>on</strong> perspective is Amaz<strong>on</strong>.com, and our final article<br />

for this period is Anne Zybowski’s overview of how Amaz<strong>on</strong>.com used its 2010 acquisiti<strong>on</strong> of Quidsi (soap.com, diapers.com,<br />

and yoyo.com) to expand its footprint into c<strong>on</strong>venti<strong>on</strong>al replenishment categories. There is no thinking observer of shopper<br />

behavior who would deny that a massive amount of volume in categories that have predictable replenishment, low shopper<br />

engagement, and high shopper benefit for <strong>the</strong>ir household being in-stock <strong>on</strong> those items (diapers, toilet paper, etc.) increasingly<br />

is going to move to some sort of <strong>on</strong>line-facilitated auto-replenishment model. Today, it remains somewhat surprising<br />

how few retailers, suppliers, or agencies have addressed this fundamental “known” with specific acti<strong>on</strong> steps to compete with<br />

or leverage this inexorable sea change in shopping behavior.<br />

We hope that <strong>the</strong>se articles motivate you to attack <strong>the</strong>se specific issues of course, but more importantly perhaps we hope<br />

that this overview gives you <strong>the</strong> c<strong>on</strong>fidence to act, c<strong>on</strong>vincingly and boldly, in this world of perpetual volatility. Closing your<br />

eyes or pretending that <strong>the</strong> seas aren’t rough is <strong>on</strong>ly going to make you sick. Visi<strong>on</strong> firmly focused <strong>on</strong> <strong>the</strong> horiz<strong>on</strong> of <strong>the</strong> Great<br />

Big Knowns and a dedicati<strong>on</strong> to turning insights around those knowns into acti<strong>on</strong> appear to be <strong>the</strong> core survival skills for <strong>the</strong><br />

bumpy ocean of 2012 and bey<strong>on</strong>d.<br />

Best of luck, and hope to see you somewhere so<strong>on</strong>,<br />

Bryan Gildenberg<br />

Chief Knowledge Officer, <strong>Kantar</strong> <strong>Retail</strong><br />

4 Breakthrough Insights

UK Online Grocery:<br />

Comparis<strong>on</strong> Shopping Trips<br />

By: Bryan Roberts / Originally published: September 19, <str<strong>on</strong>g>2011</str<strong>on</strong>g><br />

While it is relatively easy to complete<br />

comparis<strong>on</strong> shopping trips at bricks &<br />

mortar stores, a comparis<strong>on</strong> of <strong>on</strong>line<br />

grocery retailers (all <strong>the</strong> way from<br />

browsing <strong>on</strong>line to receiving <strong>the</strong> products)<br />

is a slightly more complex, not to menti<strong>on</strong><br />

expensive, affair. To c<strong>on</strong>duct a genuine<br />

comparis<strong>on</strong>, we felt it was necessary to<br />

actually complete a series of shopping<br />

trips with all of <strong>the</strong> major <strong>on</strong>line grocers<br />

in <strong>the</strong> UK. Here we present <strong>the</strong> findings<br />

from our experience shopping all of <strong>the</strong><br />

major <strong>on</strong>line grocers, covering issues<br />

such as <strong>the</strong> <strong>on</strong>line shopping experience,<br />

pricing, delivery, and accuracy.<br />

Tesco App Enables Shoppers to Scan Ads and Add Them to Online Shopping Lists<br />

Survey background<br />

Our survey comprised a series of <strong>on</strong>line shopping<br />

trips c<strong>on</strong>ducted over a two-week period, at Tesco,<br />

Asda, Sainsbury’s, Waitrose, and Ocado. We<br />

selected 15 SKUs (Figure 1) across a variety of<br />

categories that we assumed would be available<br />

through all of <strong>the</strong> retailer’s e-commerce sites. For<br />

<strong>the</strong> sake of price comparability we selected <strong>on</strong>ly<br />

branded items and avoided categories such as fresh<br />

produce where product weights and pack sizes<br />

are significantly variable and/or where branded<br />

penetrati<strong>on</strong> is low.<br />

We registered as a first-time customer at all of <strong>the</strong><br />

sites, so, in effect, <strong>the</strong>se were all first-time shops<br />

with <strong>the</strong> <strong>on</strong>line retailers. During <strong>the</strong> shopping<br />

process, we timed how l<strong>on</strong>g it took to find and<br />

Source: Tesco<br />

Breakthrough Insights 5

Figure 1: Selected 15 SKUS Across Variety of Categories<br />

1 Shower gel Original Source Lime Shower<br />

Gel 250ml<br />

2 Dishwasher tabs Finish All In 1 Regular 28 Pack<br />

3 Kitchen roll Plenty Kitchen Towel White<br />

2 Roll<br />

4 Laundry tabs Ariel Liquitabs Colour 23’s<br />

5 Tea Yorkshire 80 Teabags 250g<br />

6 Water Highland Spring Sparkling<br />

Water 6x500ml<br />

7 Fruit Squash Squash Robins<strong>on</strong>s No Added<br />

Sugar Orange Drink 1l<br />

8 Baked beans Heinz Baked Bean In Tomato<br />

Sauce 415g<br />

9 Brown sauce HP Brown Sauce 425g<br />

10 Cider Str<strong>on</strong>gbow Cider 4x440ml<br />

11 Bread Warburt<strong>on</strong>s Wholemeal Bread<br />

Medium Sliced 400g<br />

12 Cheese Ca<strong>the</strong>dral City Extra Mature<br />

350g<br />

13 Wine Wolf Blass Yellow Label<br />

Chard<strong>on</strong>nay 75cl<br />

14 Sausages Walls Classic 8 Pork Sausages<br />

454g<br />

15 Toothpaste Colgate Max White Toothpaste<br />

100ml<br />

Source:<strong>Kantar</strong> <strong>Retail</strong><br />

select <strong>the</strong> 15 SKUs and kept separate timings of<br />

<strong>the</strong> check-out process. Throughout <strong>the</strong> process,<br />

we were keeping an eye out for features such as<br />

<strong>the</strong> hierarchy of brands/private labels as <strong>the</strong>y<br />

appeared in each category, product suggesti<strong>on</strong>s or<br />

recommendati<strong>on</strong>s, special offers and multi-buys,<br />

any evidence of vendor investment in terms of<br />

“space <strong>on</strong> shelf,” availability of <strong>the</strong> 15 SKUs, and any<br />

hints or reminders that were intended to prompt us<br />

to exploit special offers.<br />

6 Breakthrough Insights<br />

In terms of price comparis<strong>on</strong>s, <strong>the</strong> fact that some<br />

of <strong>the</strong> SKUs were not stocked by some of <strong>the</strong><br />

retailers meant that exact comparis<strong>on</strong>s across all<br />

retailers was not possible. But in order to achieve<br />

comparability, we made <strong>the</strong> assumpti<strong>on</strong> that when<br />

a retailer did not carry a particular item, <strong>the</strong> item<br />

would be included in that retailer’s basket at <strong>the</strong><br />

lowest n<strong>on</strong>-promoti<strong>on</strong>al price offered by <strong>on</strong>e of<br />

<strong>the</strong> o<strong>the</strong>r retailers. While we acknowledge that<br />

this methodology is not strictly watertight, it was<br />

preferable to simply deleting four SKUs from our<br />

15-SKU basket. Throughout, we have ranked <strong>the</strong><br />

retailers <strong>on</strong> <strong>the</strong> various criteria featured, with 5 as<br />

<strong>the</strong> best score, and 1 as <strong>the</strong> worst.<br />

Availability<br />

The 15 SKUs were selected<br />

with <strong>the</strong> assumpti<strong>on</strong> that<br />

as well-known brands and<br />

routine pack sizes, <strong>the</strong>y<br />

would be available through<br />

all of <strong>the</strong> retailers. Alas, this<br />

was not to be, creating <strong>the</strong><br />

Availability scores<br />

Asda 4<br />

Ocado 4<br />

Sainsbury’s 3<br />

Tesco 5<br />

Waitrose 5<br />

aforementi<strong>on</strong>ed complicati<strong>on</strong> in price comparis<strong>on</strong>s.<br />

Waitrose and Tesco offered all 15 products; <strong>the</strong>re<br />

was <strong>on</strong>e SKU missing from <strong>the</strong> Asda shop (Highland<br />

Spring water was available in a 9-pack ra<strong>the</strong>r than<br />

a 6 pack); Ocado did not sell <strong>the</strong> 80-pack Yorkshire<br />

Tea bags; and Sainsbury’s did not offer Finish<br />

dishwash tabs in <strong>the</strong> required pack-size and Wall’s<br />

sausages were simply unavailable in a category<br />

dominated by brand leader Richm<strong>on</strong>d, private label,<br />

and more upscale ‘gourmet’ ranges.

Shopping trip durati<strong>on</strong><br />

The relative navigability of<br />

stores clearly had an impact<br />

<strong>on</strong> <strong>the</strong> length of time each<br />

shopping trip took. We<br />

expect subsequent trips to<br />

be faster as we get <strong>the</strong> hang<br />

of <strong>the</strong> vagaries and quirks<br />

of navigating each site.<br />

That said, <strong>the</strong>re were clear<br />

Shopping trip<br />

durati<strong>on</strong> scores<br />

Asda 3<br />

Ocado 5<br />

Sainsbury’s 5<br />

Tesco 4<br />

Waitrose 2<br />

disparities in shopping trip durati<strong>on</strong>. Sainsbury’s<br />

and Ocado came out <strong>on</strong> top as <strong>the</strong> easiest/fastest<br />

sites to shop, with Tesco and <strong>the</strong>n Asda offering <strong>the</strong><br />

next fastest sites to navigate. Rounding out <strong>the</strong> pack<br />

is Waitrose, a site where we believe <strong>the</strong>re is still<br />

a huge amount of work to be d<strong>on</strong>e to improve <strong>the</strong><br />

shopper experience.<br />

Checkout<br />

The next stage of <strong>the</strong><br />

Checkout scores<br />

shopping process was<br />

Asda 5<br />

checkout and, again, <strong>the</strong>re<br />

Ocado 3<br />

was a marked variati<strong>on</strong> in<br />

Sainsbury’s 2<br />

<strong>the</strong> speed of this process.<br />

Tesco 3<br />

Coming in last was<br />

Waitrose 4<br />

Sainsbury’s, with around five<br />

minutes needed to complete our order. The Tesco<br />

experience was marred by <strong>the</strong> site crashing midway<br />

through checkout, although we were quickly able<br />

to log back in and thankfully retrieve <strong>the</strong> shopping<br />

basket and restart checkout. Asda was <strong>the</strong> clear<br />

winner, offering a rapid and effective checkout<br />

process that took just two minutes.<br />

Delivery time-slots: Proximity<br />

While not necessarily<br />

something that is within<br />

a retailer’s c<strong>on</strong>trol (a<br />

successful service will be<br />

heavily booked up), <strong>the</strong>re<br />

were some real differences<br />

in terms of how quickly<br />

<strong>the</strong> retailers were able<br />

to provide delivery. Asda<br />

was able to offer us a delivery later in <strong>the</strong> day of<br />

our order, while Ocado, Tesco, and Sainsbury’s<br />

were all able to fit our delivery <strong>on</strong> <strong>the</strong> following<br />

day. The biggest lag was for Waitrose, where <strong>the</strong><br />

nearest available timeslot was two days from <strong>the</strong><br />

time of order. A useful feature offered by Asda<br />

allows shoppers to choose a timeslot (indicated<br />

by a van symbol <strong>on</strong> <strong>the</strong> scheduling tool) for when<br />

a van is already scheduled to be in your area—<br />

enabling shoppers to coordinate <strong>the</strong>ir deliveries<br />

with o<strong>the</strong>r shoppers in <strong>the</strong>ir area, minimising<br />

<strong>the</strong> envir<strong>on</strong>mental impact of <strong>the</strong>ir deliveries and<br />

increasing efficiencies for Asda. A similar feature<br />

also is offered by Ocado.<br />

Delivery Timeslots: Durati<strong>on</strong><br />

One of <strong>the</strong> inc<strong>on</strong>veniences<br />

associated with any sort<br />

of home shopping is <strong>the</strong><br />

requirement for some<strong>on</strong>e<br />

to be in at <strong>the</strong> delivery<br />

address to receive <strong>the</strong> order.<br />

Indeed, this is <strong>on</strong>e of <strong>the</strong> key<br />

drivers behind <strong>the</strong> growth<br />

Time-slots:<br />

proximity scores<br />

Asda 5<br />

Ocado 4<br />

Sainsbury’s 4<br />

Tesco 4<br />

Waitrose 3<br />

Time-slots:<br />

durati<strong>on</strong> scores<br />

Asda 4<br />

Ocado 5<br />

Sainsbury’s 5<br />

Tesco 4<br />

Waitrose 4<br />

Breakthrough Insights 7

of <strong>the</strong> “drive-thru” grocery ecommerce model in<br />

markets as diverse as <strong>the</strong> US, Germany, France,<br />

<strong>the</strong> UK, and Spain; such services provide all of <strong>the</strong><br />

c<strong>on</strong>venience of <strong>on</strong>line shopping without <strong>the</strong> burden<br />

of being housebound. In ranking timeslot durati<strong>on</strong>,<br />

higher scores have been awarded for <strong>the</strong> shortest<br />

timeslots, <strong>the</strong> logic being that <strong>the</strong>se shorter slots<br />

are more c<strong>on</strong>venient for time-pressed shoppers.<br />

Sainsbury’s and Ocado triumphed thanks to <strong>the</strong><br />

availabilityof <strong>on</strong>e-hour slots as opposed to <strong>the</strong> two<br />

hours offered by <strong>the</strong> alternative services.<br />

Communicati<strong>on</strong>s<br />

A comm<strong>on</strong> <strong>the</strong>me with<br />

home shopping in general<br />

is <strong>the</strong> need for c<strong>on</strong>firmati<strong>on</strong><br />

and reassurance <strong>on</strong><br />

orders and deliveries. The<br />

supermarkets in questi<strong>on</strong><br />

here varied enormously<br />

in <strong>the</strong> way that <strong>the</strong>y<br />

communicated between <strong>the</strong><br />

time <strong>the</strong> order was placed and <strong>the</strong> time <strong>the</strong> delivery<br />

was received. All of <strong>the</strong> supermarkets issued a<br />

c<strong>on</strong>firmati<strong>on</strong> email up<strong>on</strong> receipt of <strong>the</strong> order. This<br />

is where Waitrose and Asda both stopped: <strong>the</strong> next<br />

time we heard from <strong>the</strong>m was when our groceries<br />

were delivered. Ocado was much more active in<br />

communicating with us: as well as <strong>the</strong> c<strong>on</strong>firmati<strong>on</strong><br />

e-mail, we received a reminder SMS message<br />

<strong>the</strong> day before delivery. On <strong>the</strong> day of delivery, we<br />

received an SMS telling us of changes to <strong>the</strong> order<br />

and ano<strong>the</strong>r SMS <strong>on</strong> <strong>the</strong> day to remind us of <strong>the</strong><br />

delivery time and to assure us that <strong>the</strong>re were no<br />

unavailable items. Both Tesco and Sainsbury’s<br />

8 Breakthrough Insights<br />

Communicati<strong>on</strong><br />

scores<br />

Asda 3<br />

Ocado 5<br />

Sainsbury’s 4<br />

Tesco 4<br />

Waitrose 3<br />

sent a reminder SMS <strong>on</strong> <strong>the</strong> day before delivery.<br />

The clear winner here was Ocado—we were fully<br />

informed throughout <strong>the</strong> process and were left<br />

c<strong>on</strong>fident that our delivery would be timely and<br />

accurate.<br />

Pricing<br />

As referenced above, <strong>the</strong> Pricing scores<br />

fact that not all of <strong>the</strong> Asda 4<br />

retailers stocked all of <strong>the</strong> Ocado 5<br />

SKUs meant that we had to Sainsbury’s 3<br />

improvise slightly in order Tesco 2<br />

to c<strong>on</strong>struct comparable<br />

baskets. We accept that<br />

Waitrose 1<br />

this might not be <strong>the</strong> most scientifically rigorous<br />

piece of analysis, but it was ei<strong>the</strong>r this soluti<strong>on</strong> or<br />

disregarding <strong>the</strong> SKU for all of <strong>the</strong> retailers. The<br />

instances of unavailability are highlighted in red in<br />

<strong>the</strong> Figure 2, while promoti<strong>on</strong>s are highlighted in<br />

green. Where products were replaced by items of a<br />

different value, we have included <strong>the</strong> original price<br />

of <strong>the</strong> item, again for <strong>the</strong> sake of comparability. And<br />

finally, as was <strong>the</strong> case with Tesco, when a retailer<br />

ended up not processing/delivering an item, we<br />

have included that item’s price as though it were<br />

delivered.<br />

Surprisingly, perhaps, <strong>the</strong> clear winner in terms of<br />

basket pricing was Ocado. This is a clear result of<br />

its brand price-matching with Tesco plus a couple of<br />

fortuitous promoti<strong>on</strong>s (<strong>on</strong> wine and dishwash tabs)<br />

that brought its basket in at <strong>the</strong> lowest price by far.<br />

Without <strong>the</strong> promoti<strong>on</strong>s, Ocado would have been<br />

beaten <strong>on</strong> price by Asda—its EDLP strategy coming<br />

through—as well as by Tesco and Sainsbury’s.

Figure 2: Price Comparis<strong>on</strong>s<br />

Product Waitrose Asda Tesco Ocado Sainsbury’s<br />

Original Source Lime Shower Gel 250ml £1.94 £1.94 £1.94 £1.94 £2.00<br />

Finish All In 1 Regular 28 Pack 7.65 5.00 6.00 3.83 5.00<br />

Plenty Kitchen Towel White 2 Roll 1.87 1.86 1.87 1.87 2.00<br />

Ariel Liquitabs Colour 23’S 7.09 6.79 6.79 6.79 7.09<br />

Yorkshire 80 Teabags 250g 2.28 2.28 2.28 2.28 2.28<br />

Highland Spring Sparkling Water 6X500ml 2.39 2.34 1.99 2.34 2.39<br />

Robins<strong>on</strong>s No Added Sugar Orange Drink 1l 1.25 1.10 1.25 1.25 1.25<br />

Heinz Baked Bean In Tomato Sauce 415g 0.69 0.69 0.50 0.69 0.69<br />

HP Brown Sauce 425g 1.99 1.68 1.69 1.50 1.69<br />

Str<strong>on</strong>gbow Cider 4x440ml 3.83 3.50 3.99 4.79 3.99<br />

Warburt<strong>on</strong>s Wholemeal Bread Medium Sliced 400g 0.70 0.70 0.70 0.70 0.70<br />

Ca<strong>the</strong>dral City Extra Mature 350g 4.50 3.98 3.98 3.98 4.48<br />

Wolf Blass Yellow Label Chard<strong>on</strong>nay 75cl 9.99 7.98 9.99 6.66 7.49<br />

Walls Classic 8 Pork Sausages 454g 2.28 2.28 1.14 2.28 2.28<br />

Colgate Max White Toothpaste 100ml 2.00 2.00 2.00 2.00 2.00<br />

Total basket 50.45 44.12 46.11 42.90 45.33<br />

Key: Unavailable; Promoti<strong>on</strong><br />

The most expensive by far was Waitrose, which<br />

comes as a surprise as it also price matches Tesco<br />

<strong>on</strong> 1,000 branded SKUs. This price matching was<br />

claimed by <strong>the</strong> Waitrose website to apply to baked<br />

beans, squash, tea, sausages, bread, shower gel,<br />

and sauce, but it became clear when we shopped<br />

Tesco that Waitrose was 19p more expensive <strong>on</strong><br />

baked beans and 30p more expensive <strong>on</strong> brown<br />

sauce. For sausages, Tesco’s half-price offer meant<br />

that Waitrose was really off <strong>the</strong> mark. It might be<br />

<strong>the</strong> case that we shopped Waitrose at a time when it<br />

was in between Tesco price comparis<strong>on</strong>s (although<br />

it claims to check prices twice per week), but even<br />

so, we are not left with a huge sense of c<strong>on</strong>fidence<br />

in Waitrose’s price matching claims.<br />

Delivery charges<br />

The issue of delivery charges<br />

can be a complex <strong>on</strong>e, as<br />

many of <strong>the</strong> retailers have<br />

a sliding scale of delivery<br />

charges depending <strong>on</strong> size of<br />

shopping basket, day of <strong>the</strong><br />

week, and time of day. We<br />

<strong>the</strong>refore acknowledge that,<br />

Source:<strong>Kantar</strong> <strong>Retail</strong><br />

Deliver charges<br />

scores<br />

Asda 3<br />

Ocado 4<br />

Sainsbury’s 1<br />

Tesco 2<br />

Waitrose 5<br />

if we had spent more m<strong>on</strong>ey, or chosen ano<strong>the</strong>r day/<br />

time, <strong>the</strong>n some of <strong>the</strong>se charges might have been<br />

lower or not have existed at all. It’s clear that <strong>on</strong>line<br />

retailing is more ec<strong>on</strong>omical for larger trolley-style<br />

shops than it is for <strong>the</strong> relatively small basket such<br />

as ours. A larger basket will often avoid delivery<br />

Breakthrough Insights 9

charges, or at least reduce <strong>the</strong>m in terms of cost<br />

per item.<br />

Waitrose’s approach is much simpler (free delivery<br />

for shops of over £50), while <strong>the</strong> o<strong>the</strong>r retailers<br />

have a sliding scale depending <strong>on</strong> order value and<br />

schedule of delivery. Asda charges between £3 and<br />

£5. Ocado deliveries can be free (in <strong>the</strong> graveyard<br />

slot of 10:30–11:30 p.m.) but usual charges vary<br />

from 49p to £4.99. Tesco’s scale ranges from £3.00<br />

to £6.00, while Sainsbury’s has a similar range of<br />

£3.50 to £6.00.<br />

What our shopping experience revealed is that<br />

<strong>the</strong>re are a number of trade-offs available to <strong>on</strong>line<br />

shoppers. The Waitrose delivery is free, but we<br />

are likely to pay a higher price for our groceries.<br />

Similarly, a higher delivery charge will be levied<br />

for those times of day that are c<strong>on</strong>venient for most<br />

shoppers: we must trade off between low cost and<br />

c<strong>on</strong>venience. One trade-off becomes very clear:<br />

for <strong>on</strong>line grocery to be at its most ec<strong>on</strong>omical<br />

from <strong>the</strong> shopper’s perspective, shoppers must<br />

purchase high-value, large-basket orders. Funnily<br />

enough, we suspect that <strong>the</strong> same logic holds from<br />

<strong>the</strong> retailer’s perspective—by baking in delivery<br />

charges based <strong>on</strong> basket size and schedule,<br />

shopper behaviour is being shepherded in <strong>the</strong><br />

directi<strong>on</strong> desired by <strong>the</strong> retailers.<br />

Timeliness<br />

Clearly, a key performance attribute for grocery<br />

e-commerce operators is timeliness, and n<strong>on</strong>e of<br />

<strong>the</strong> providers let us down here. Sainsbury’s was<br />

actually a few minutes early, while Asda, Waitrose,<br />

10 Breakthrough Insights<br />

and Tesco all arrived within<br />

<strong>the</strong>ir allotted time slots.<br />

Ocado dem<strong>on</strong>strated some<br />

typically elegant customer<br />

service: our driver (James in<br />

<strong>the</strong> Odette Oni<strong>on</strong> Van) called<br />

to say that he was in <strong>the</strong><br />

area and asked if we were<br />

willing to accept an early<br />

Timeliness<br />

scores<br />

Asda 5<br />

Ocado 5<br />

Sainsbury’s 5<br />

Tesco 5<br />

Waitrose 5<br />

delivery. We answered in <strong>the</strong> affirmative, and he<br />

arrived 30 minutes ahead of schedule.<br />

Delivery service<br />

The basic distincti<strong>on</strong> here<br />

Service scores<br />

is: will <strong>the</strong> driver offer to<br />

Asda 4<br />

take groceries into <strong>the</strong><br />

Ocado 5<br />

customer’s kitchen, and<br />

Sainsbury’s 5<br />

possibly even offer to help<br />

Tesco 3<br />

unpack? The experience<br />

Waitrose 5<br />

here varied from extremely<br />

good (Waitrose, Ocado,<br />

and Sainsbury’s all delivered <strong>the</strong> bags into <strong>the</strong><br />

kitchen), to <strong>the</strong> moderate (Asda dumped our bags<br />

<strong>on</strong> <strong>the</strong> fr<strong>on</strong>t door mat) to <strong>the</strong> less than ideal (we<br />

had to unpack our own bags from a Tesco crate<br />

<strong>on</strong> <strong>the</strong> fr<strong>on</strong>t step). While we appreciate that <strong>the</strong>re<br />

might be certain legal/insurance/safety c<strong>on</strong>cerns<br />

with delivery staff entering customers’ homes, <strong>the</strong><br />

delivery experience actually can have a significant<br />

effect <strong>on</strong> <strong>the</strong> entire process.<br />

Bags<br />

The UK press has periodically had a field day<br />

over <strong>the</strong> excessive bagging perpetrated by <strong>on</strong>line

grocers. We certainly had a mixed experience. The<br />

sec<strong>on</strong>d-best performer here was Ocado, which<br />

used four bags for 15 items. The delivery, from<br />

<strong>the</strong> main Hatfield fulfilment centre, came in four<br />

colour-coded bags (purple for ambient and red for<br />

fridge) and our excellent Ocado driver was keen to<br />

point out <strong>the</strong> bag recycling service that <strong>the</strong> company<br />

offered.<br />

Asda was <strong>the</strong> worst for bagging—using seven bags<br />

for 14 SKUs. One bag was dedicated to a single<br />

substitute product (“Substituti<strong>on</strong>s are easy to spot—<br />

<strong>the</strong>y’re always delivered in a separate bag and are<br />

clearly marked <strong>on</strong> your delivery note”), although,<br />

as <strong>the</strong>re was no bag colour-coding, this was not<br />

immensely helpful.<br />

Tesco’s bags were colour coded: green for<br />

chilled products; white for ambient, and blue for<br />

substituti<strong>on</strong>s. Some of <strong>the</strong> bagging was faintly<br />

ridiculous, obviously based <strong>on</strong> <strong>the</strong> picking regimen<br />

in <strong>the</strong> Greenford dark store: baked beans and brown<br />

sauce came in <strong>the</strong>ir own bags, while some products<br />

were loose in <strong>the</strong> crate. A total of five bags were<br />

used.<br />

Waitrose did very well here: four bags were used for<br />

15 items. They were colour-coded (blue for fridge<br />

and green for ambient) and <strong>the</strong> driver reminded us<br />

of <strong>the</strong> bag recycling service offered by <strong>the</strong> retailer.<br />

Accuracy<br />

Aside from <strong>the</strong> issue of substituti<strong>on</strong>s (see next<br />

secti<strong>on</strong>), we <strong>on</strong>ly had <strong>on</strong>e example of poor accuracy.<br />

Despite ordering a bottle of wine <strong>on</strong> Tesco.com,<br />

and despite this bottle of wine being featured in<br />

our email c<strong>on</strong>firmati<strong>on</strong><br />

from Tesco, <strong>the</strong> delivery<br />

receipt omitted <strong>the</strong> wine<br />

and, indeed, <strong>the</strong> wine was<br />

nowhere to be found in <strong>the</strong><br />

delivery. For <strong>the</strong> purposes<br />

of <strong>the</strong> pricing comparis<strong>on</strong>,<br />

we have assumed it was<br />

delivered at <strong>the</strong> same<br />

price, but this explains Tesco’s poor standing in <strong>the</strong><br />

accuracy scores. The <strong>on</strong>ly c<strong>on</strong>solati<strong>on</strong> was that we<br />

were not charged for <strong>the</strong> missing item.<br />

Substituti<strong>on</strong>s<br />

Product substituti<strong>on</strong>s have<br />

been ano<strong>the</strong>r c<strong>on</strong>tentious<br />

issue for <strong>on</strong>line grocers,<br />

with assorted inappropriate<br />

and/or comedic substituti<strong>on</strong>s<br />

making <strong>the</strong> press. Ocado<br />

and Sainsbury’s were<br />

<strong>the</strong> <strong>on</strong>ly two retailers to<br />

escape unsca<strong>the</strong>d in this<br />

Accuracy<br />

scores<br />

Asda 5<br />

Ocado 5<br />

Sainsbury’s 5<br />

Tesco 4<br />

Waitrose 5<br />

Substituti<strong>on</strong>s<br />

scores<br />

Asda 4<br />

Ocado 5<br />

Sainsbury’s 5<br />

Tesco 4<br />

Waitrose 3<br />

way, delivering exactly <strong>the</strong> products as ordered.<br />

Waitrose made two substituti<strong>on</strong>s for out of stock<br />

items, replacing Plenty kitchen towels at £1.87 with<br />

Thirst Pockets at £1.22 and <strong>the</strong> 350g Ca<strong>the</strong>dral City<br />

Extra Mature with a Mature 600g pack (charging<br />

<strong>the</strong> lower price of £4.50 ra<strong>the</strong>r than £5.29), slightly<br />

compensating us for <strong>the</strong> wr<strong>on</strong>g flavour of cheese<br />

with extra volume. A nice touch here was that <strong>the</strong><br />

substituti<strong>on</strong>s brought us below <strong>the</strong> free delivery<br />

threshold of £50, but we were still given free<br />

delivery. Asda’s <strong>on</strong>e substituti<strong>on</strong> saw <strong>the</strong>m replace<br />

<strong>the</strong> dishwasher tabs with Finish’s Lem<strong>on</strong> variant<br />

Breakthrough Insights 11

at same price, while Tesco also substituted this<br />

product. The £6.00 28 pack was unavailable, so<br />

(according to <strong>the</strong> delivery receipt) we were given<br />

two 15 packs for £7.76, <strong>the</strong> £1.76 difference being<br />

refunded. One problem here is that we were<br />

actually given two packs of 14.<br />

Shelf-life<br />

The final criteria <strong>the</strong><br />

retailers were judged <strong>on</strong><br />

was shelf-life. Some of <strong>the</strong><br />

retailers (e.g. Waitrose) use<br />

<strong>the</strong> l<strong>on</strong>gest possible shelf<br />

lives as <strong>on</strong>e of <strong>the</strong>ir selling<br />

points, while o<strong>the</strong>rs have<br />

been castigated for using<br />

<strong>on</strong>line shopping as a complex stock rotati<strong>on</strong> system,<br />

foisting near-expired products <strong>on</strong> <strong>the</strong> unsuspecting<br />

public. In this basket, this criteria boils down to <strong>the</strong><br />

sausages, as <strong>the</strong> cheese ordered lasted a couple of<br />

m<strong>on</strong>ths from all of <strong>the</strong> retailers.<br />

Sainsbury’s did not stock <strong>the</strong> sausages, so <strong>the</strong>y<br />

get <strong>the</strong> benefit of <strong>the</strong> doubt here, while Asda was<br />

<strong>the</strong> <strong>on</strong>ly retailer with an issue here. A use-by date<br />

of August 20, with <strong>the</strong> delivery occurring <strong>on</strong> <strong>the</strong><br />

evening of <strong>the</strong> August 18, meant that an enforced<br />

change of menu planning was in order. Only two<br />

days’ shelf life compared poorly to <strong>the</strong> eight from<br />

Tesco, seven from Waitrose and five from Ocado.<br />

We have arbitrarily given Sainsbury’s <strong>the</strong> same<br />

average score as Ocado as <strong>the</strong>y did not stock <strong>the</strong><br />

item in questi<strong>on</strong>.<br />

12 Breakthrough Insights<br />

Shelf-Life<br />

scores<br />

Asda 2<br />

Ocado 3<br />

Sainsbury’s 3<br />

Tesco 5<br />

Waitrose 4<br />

Final scores<br />

Having judged <strong>the</strong> various<br />

services <strong>on</strong> 14 criteria,<br />

Ocado , <strong>the</strong> <strong>on</strong>ly <strong>on</strong>line<strong>on</strong>ly<br />

specialist under<br />

c<strong>on</strong>siderati<strong>on</strong>, emerges as<br />

<strong>the</strong> clear winner. All three<br />

of <strong>the</strong> “Big Three” retailers<br />

scored level points, with<br />

Waitrose pipping <strong>the</strong>m at <strong>the</strong><br />

Final<br />

scores<br />

Asda 52<br />

Ocado 62<br />

Sainsbury’s 52<br />

Tesco 52<br />

Waitrose 54<br />

post in sec<strong>on</strong>d place. Asda was let down by a poor<br />

show in terms of bagging and shelf-life; Ocado’s<br />

<strong>on</strong>ly real weakness was <strong>the</strong> checkout experience;<br />

Tesco was undermined by pricing, delivery charges,<br />

and accuracy; Sainsbury’s fared badly <strong>on</strong> <strong>the</strong> cost<br />

of delivery and availability; and Waitrose has work<br />

to do <strong>on</strong> improving its website and sharpening its<br />

pricing.<br />

The good news for all operators is that not <strong>on</strong>e of<br />

<strong>the</strong>m had an absolute shocker; most were let down<br />

by <strong>on</strong>e or two facets of <strong>the</strong>ir <strong>on</strong>line operati<strong>on</strong>s.<br />

Implicati<strong>on</strong>s for suppliers:<br />

There was not a great deal of evidence throughout<br />

our shopping trips that suppliers are currently able<br />

(or perhaps willing) to secure a more prominent<br />

place “<strong>on</strong> shelf” in <strong>the</strong> <strong>on</strong>line shopping experience.<br />

Indeed, most of <strong>the</strong> sites/categories we shopped<br />

were in alphabetical order or were fr<strong>on</strong>t-loaded<br />

with private brand.

There are clearly some ways of bolstering a<br />

presence in <strong>the</strong>se retailers’ <strong>on</strong>line stores. Securing<br />

space to announce new products or promoti<strong>on</strong>s is<br />

comm<strong>on</strong>place, and we encountered several ‘sticky”<br />

product advertisements that followed us around a<br />

shopping trip, even into different categories.<br />

In terms of <strong>the</strong> alphabetical-order issue, and<br />

this might sounds like something of a fatuous<br />

recommendati<strong>on</strong>, ensuring that brands (or<br />

rebrands) are named with an early letter in <strong>the</strong><br />

alphabet might be a relatively simple way of<br />

ensuring <strong>on</strong>line prominence.<br />

Ano<strong>the</strong>r way of securing prominence will be to<br />

ensure a brand’s participati<strong>on</strong> in <strong>on</strong>line features<br />

such as recipe-based shopping lists and pre-made<br />

shopping lists. At <strong>the</strong> moment, <strong>the</strong>se pre-made<br />

features are extraordinarily skewed toward private<br />

brands.<br />

Sampling is an opportunity with <strong>on</strong>line. Ra<strong>the</strong>r than<br />

relying <strong>on</strong> <strong>the</strong> hit and miss approach of instore<br />

sampling, which is untargeted and dependent <strong>on</strong><br />

traffic flow in <strong>the</strong> store, delivering free product<br />

or product miniatures al<strong>on</strong>gside e-commerce<br />

deliveries enables manufacturers to send samples<br />

directly into shoppers’ homes, often targeted by<br />

shopper group or by geography.<br />

Impulse, c<strong>on</strong>trary to popular belief, can still be<br />

achieved <strong>on</strong>line, such as with Tesco’s “Goes Nicely<br />

With” feature that can lead shoppers into new<br />

categories and new adjacencies. This appears to be<br />

a currently underutilised functi<strong>on</strong> by both retailers<br />

and suppliers.<br />

Online also appears to be a more favourable<br />

arena for multi-brand or multi-category suppliers<br />

to implement cross-brand or cross-category<br />

promoti<strong>on</strong>s. These win favour with retailers through<br />

basket-building but are often difficult/expensive<br />

to achieve instore as space c<strong>on</strong>straints mean that<br />

displaying <strong>the</strong> participating SKUS in close proximity<br />

is often problematic, meaning that shoppers<br />

might have to visit four or five different aisles. By<br />

displaying <strong>the</strong>se promoti<strong>on</strong>s during <strong>the</strong> <strong>on</strong>line<br />

shopping trip or at check-out, shoppers, retailers,<br />

and brands should be able to more readily benefit<br />

from trans-category promoti<strong>on</strong>al programmes.<br />

Breakthrough Insights 13

Online <strong>Retail</strong> in China:<br />

Getting Ahead of <strong>the</strong> Curve<br />

By: Phil Smiley and Justin Cook / Originally published: August 2, <str<strong>on</strong>g>2011</str<strong>on</strong>g><br />

Rapid growth in China’s fledgling modern<br />

retail market will drive companies—both<br />

retailers and manufacturers—to invest<br />

heavily in gaining market share. Online<br />

retailing still represents a fracti<strong>on</strong> of total<br />

retail sales in China. However, <strong>on</strong>line<br />

retailing represents a very large and<br />

fast growing porti<strong>on</strong> of modern retailing<br />

in China. <strong>Kantar</strong> <strong>Retail</strong> predicts that<br />

many executives will learn that investing<br />

heavily in <strong>on</strong>line business platforms will<br />

be a requirement for retailers wishing<br />

to dominate share in China’s rapidly<br />

evolving modern trade. The result will be<br />

a modern trade envir<strong>on</strong>ment <strong>the</strong> likes of<br />

which we’ve never seen before.<br />

When Walmart had just 300 stores in <strong>the</strong> United<br />

States, <strong>the</strong> Internet didn’t exist. Today, Walmart<br />

operates 338 stores in China, a country with more<br />

than 400 milli<strong>on</strong> Internet users and <strong>on</strong>e where <strong>the</strong><br />

<strong>on</strong>line shopping bug is spreading fast.<br />

Online retail is going to play a major role in <strong>the</strong><br />

development of China’s retail market. It will<br />

likely occupy a larger share of transacti<strong>on</strong>s than<br />

14 Breakthrough Insights<br />

in Western markets. Online shopping in China is<br />

already gaining adopti<strong>on</strong> faster than we have seen<br />

in Western markets.<br />

C<strong>on</strong>sequently, <strong>on</strong>line retail will play a disruptive<br />

role in <strong>the</strong> development of modern retailing in<br />

China. Many Chinese cities d<strong>on</strong>’t have a modern<br />

retail store and are unlikely to get <strong>on</strong>e so<strong>on</strong>, but<br />

<strong>the</strong>y do have extensive Internet access. These cities<br />

also have milli<strong>on</strong>s of c<strong>on</strong>sumers with a desire for<br />

c<strong>on</strong>venience and value. Online retail can and will<br />

deliver for <strong>the</strong>se c<strong>on</strong>sumers.

Could it be that offline store networks of <strong>the</strong> size we<br />

see in o<strong>the</strong>r markets, such as <strong>the</strong> US or European<br />

markets, will not materialize in China due to <strong>the</strong><br />

early and fast penetrati<strong>on</strong> of <strong>on</strong>line retail?<br />

Judging by recent events, Walmart China al<strong>on</strong>g with<br />

o<strong>the</strong>r leading local and global retailers may already<br />

be thinking this way. Walmart operates more than<br />

4,300 stores in <strong>the</strong> US and 338 stores in China. But<br />

will Walmart build more than 4,000 stores in China?<br />

It is more likely that Walmart and o<strong>the</strong>r leading<br />

retailers will operate a two-tier strategy. First, <strong>the</strong>y<br />

will develop an <strong>on</strong>line retail network that can reach<br />

all 400 milli<strong>on</strong> modern trade c<strong>on</strong>sumers. <str<strong>on</strong>g>Sec<strong>on</strong>d</str<strong>on</strong>g>,<br />

<strong>the</strong>y will invest in growing and c<strong>on</strong>necting this<br />

network to ‘<strong>on</strong>line-integrated’ brick-and-mortar<br />

stores. They’ll grow both businesses at <strong>the</strong> same<br />

speed. The result is a very different business model<br />

from what is seen in Western markets.<br />

Because <strong>the</strong> business model is different from<br />

models we’ve seen before, it is hard to visualize.<br />

For example, recently, Walmart acquired a stake<br />

of China’s largest “<strong>on</strong>line hypermarket” called<br />

“Yihaodian,” which means “No.1 store.” Yihaodian<br />

is a promising company with a promising <strong>on</strong>line<br />

platform. Yihaodian has grown <strong>on</strong>line sales<br />

from USD 0.64 milli<strong>on</strong> (RMB 4.17 milli<strong>on</strong>) in 2008<br />

to USD 125 milli<strong>on</strong> (RMB 805 milli<strong>on</strong>) in 2010.<br />

They have recently set up an <strong>on</strong>line retail team<br />

in Shanghai to handle <strong>on</strong>line operati<strong>on</strong>s in China.<br />

This move indicates Walmart China’s plans to<br />

focus <strong>on</strong> ecommerce operati<strong>on</strong>s in <strong>the</strong> future. This<br />

ecommerce center joins Walmart’s original center,<br />

located in New York.<br />

O<strong>the</strong>r leading retailers are setting up and expanding<br />

<strong>the</strong>ir <strong>on</strong>line businesses. In additi<strong>on</strong> to Walmart,<br />

Tesco and Carrefour also have announced plans to<br />

expand <strong>the</strong>ir <strong>on</strong>line retail operati<strong>on</strong>s in China.<br />

Taobao, <strong>the</strong> leading <strong>on</strong>line retail site which hosts<br />

B2C and C2C transacti<strong>on</strong>s, has experienced rapid<br />

growth in recent years. Taobao revenues in 2010<br />

were estimated to be USD 60 billi<strong>on</strong>. In fact, if we<br />

classed Taobao as a retailer it would be by far <strong>the</strong><br />

largest retailer in China, dwarfing <strong>the</strong> sales of high<br />

profile retailers such as Walmart, Carrefour, and<br />

Tesco.<br />

China’s Online C<strong>on</strong>sumers<br />

China has a huge base of Internet users, and it<br />

is still growing at an amazing speed. <strong>Retail</strong>ers<br />

in China are finding it easier to reach remote<br />

c<strong>on</strong>sumers via ‘clicks and ship’ retail models<br />

Figure 1: Penetrati<strong>on</strong> of Shopping Online (% HHs) - Pers<strong>on</strong>al<br />

Care<br />

18%<br />

16%<br />

14%<br />

12%<br />

10%<br />

8%<br />

6%<br />

4%<br />

2%<br />

0%<br />

12%<br />

Nati<strong>on</strong>al<br />

Urban<br />

China<br />

16%<br />

4 Key<br />

Cities<br />

10%<br />

11%<br />

13%<br />

8%<br />

A Cities B Cities C Cities D Cities<br />

Source: <strong>Kantar</strong> Worldpanel China: 52 weeks ended<br />

25 March <str<strong>on</strong>g>2011</str<strong>on</strong>g><br />

Breakthrough Insights 15

a<strong>the</strong>r than by building new stores. China’s<br />

Internet-savvy c<strong>on</strong>sumers are willing to accept<br />

new technology and innovati<strong>on</strong> in <strong>the</strong>ir life and<br />

are already accustomed to Internet shopping. In<br />

some categories, such as Baby, it is estimated<br />

that up to 15% of sales are taking place through<br />

<strong>on</strong>line channels. <strong>Kantar</strong> Worldpanel reported that<br />

17% of Nati<strong>on</strong>al Urban Chinese households have<br />

used <strong>the</strong> Internet to purchase grocery products<br />

<strong>on</strong>line with sales growing at 59% year-<strong>on</strong>-year.<br />

Pers<strong>on</strong>al care products are more sought after <strong>on</strong>line<br />

compared with food and household cleaning items<br />

(Figure 1). The proporti<strong>on</strong> of households who shop<br />

<strong>on</strong>line for pers<strong>on</strong>al care items is actually higher in<br />

<strong>the</strong> C cities compared with A cities (13% vs. 10%).<br />

This is because shoppers in <strong>the</strong> lower tier cities<br />

may struggle to find <strong>the</strong> products <strong>the</strong>y want to buy<br />

in traditi<strong>on</strong>al brick and mortar stores, so as an<br />

alternative, seek <strong>the</strong>m out through <strong>on</strong>line stores.<br />

<strong>Kantar</strong> Worldpanel identifies two key motivati<strong>on</strong>s<br />

for purchasing FMCG products <strong>on</strong>line: price and<br />

c<strong>on</strong>venience. The key pers<strong>on</strong>al care categories,<br />

which are more likely to be sought after, are <strong>the</strong><br />

more expensive <strong>on</strong>es, such as cosmetics, facial<br />

skincare, perfume, and hair colorants. Within <strong>the</strong>se<br />

categories, shoppers are opting for more premium<br />

brands, but are actually paying a much lower price<br />

per item. Therefore, shoppers want premium but at<br />

a value price.<br />

C<strong>on</strong>venience also plays a key role, particularly for<br />

categories which are heavy or bulky in <strong>the</strong>ir nature.<br />

For categories such as soft drinks, laundry powder,<br />

and instant coffee, shoppers are purchasing much<br />

16 Breakthrough Insights<br />

bigger pack sizes to take advantage of <strong>the</strong> items<br />

being delivered to <strong>the</strong>ir home. For example, <strong>the</strong><br />

average pack size for soft drinks is 2.3 liters in<br />

traditi<strong>on</strong>al stores but 3.5 liters <strong>on</strong>line.<br />

Making Sense of <strong>the</strong> Online <strong>Retail</strong> Market<br />

The <strong>on</strong>line market can be a c<strong>on</strong>fusing place, littered<br />

with different terminology and jarg<strong>on</strong>. <strong>Kantar</strong> <strong>Retail</strong><br />

analysts break <strong>the</strong> <strong>on</strong>line retail market in China into<br />

four segments, as illustrated in Figure 2.<br />

The first segment is B2C key accounts which would<br />

include internet retailers such as Amaz<strong>on</strong>.cn,<br />

Buy 360, Dang Dang, and <strong>the</strong> <strong>on</strong>line operati<strong>on</strong>s of<br />

retailers such as Tesco, Carrefour, and Walmart. In<br />

this segment products are selected by <strong>the</strong> retailer<br />

who <strong>the</strong>n takes full c<strong>on</strong>trol of assortment, price,<br />

promoti<strong>on</strong>, website design, and <strong>the</strong> user experience.<br />

The sec<strong>on</strong>d segment is what we call <strong>the</strong> <strong>on</strong>line<br />

B2C General Trade. This segment is effectively<br />

<strong>the</strong> small, independent business traders operating<br />

and selling directly to c<strong>on</strong>sumers via <strong>the</strong> Taobao<br />

exchange.<br />

Figure 2: Online <strong>Retail</strong> Market Segmentati<strong>on</strong><br />

B2C<br />

Key Acc<br />

Amaz<strong>on</strong>.cn<br />

Buy 360<br />

Dang Dang<br />

Tesco.com<br />

Carrefour.com<br />

ONLINE RETAIL<br />

B2C<br />

GT<br />

B2C FLAGSHIP C2C<br />

Taobao<br />

Small<br />

Business<br />

Trader<br />

Eg L’Oreal<br />

Flagship Store,<br />

Wyeth Flagship<br />

Store<br />

Taobao<br />

Exchange<br />

Source: <strong>Kantar</strong> <strong>Retail</strong> Analysis

The third segment is B2C Flagship. These are<br />

<strong>on</strong>line stores that are generally operated by<br />

manufacturers and hosted <strong>on</strong> Taobao Mall. In<br />

this case, manufacturers are selling <strong>the</strong>ir brands<br />

directly to <strong>the</strong> c<strong>on</strong>sumer via proprietary <strong>on</strong>line<br />

stores. As such, Taobao is effectively operating<br />

as an <strong>on</strong>line broker between manufacturers and<br />

c<strong>on</strong>sumers.<br />

The fourth segment is <strong>on</strong>line retail from C<strong>on</strong>sumer<br />

to C<strong>on</strong>sumer. This is most prevalent through <strong>the</strong><br />

Taobao exchange where c<strong>on</strong>sumers sell goods and<br />

services to each o<strong>the</strong>r, much in <strong>the</strong> same way that<br />

eBay operates in o<strong>the</strong>r markets.<br />

How Will China’s Online Channel Evolve?<br />

There is no doubt that Taobao leads <strong>the</strong> game<br />

at <strong>the</strong> moment, yet B2C <strong>on</strong>line retailers such as<br />

Amaz<strong>on</strong> and Dang Dang and <strong>the</strong> <strong>on</strong>line operati<strong>on</strong>s<br />

of retailers such as Tesco, Carrefour, and Walmart<br />

are making str<strong>on</strong>g progress in <strong>the</strong> market. <strong>Kantar</strong><br />

<strong>Retail</strong> forecasts that while Taobao will retain its<br />

dominant positi<strong>on</strong>, <strong>on</strong>line retailers such as Amaz<strong>on</strong><br />

and <strong>the</strong> major hypermarket retailers will grow<br />

faster in coming years and wrestle business away<br />

from Taobao.<br />

Taobao, China’s largest <strong>on</strong>line retailer, has already<br />

recognized <strong>the</strong> threat from growing B2C Online<br />

retailers such as Amaz<strong>on</strong> and Dang Dang and has<br />

taken steps to restructure its business model.<br />

Taobao has recently split into three separate<br />

companies to better address its target markets,<br />

according to parent company Alibaba Group. The<br />

restructuring creates Taobao Marketplace, a<br />

C<strong>on</strong>sumer-to-C<strong>on</strong>sumer platform designed for<br />

c<strong>on</strong>sumers and small businesses; Taobao Mall,<br />

a business-to-c<strong>on</strong>sumer marketplace; and eTao,<br />

which will target <strong>the</strong> shopping search market. All<br />

three companies will c<strong>on</strong>tinue under <strong>the</strong> Alibaba<br />

Group.<br />

In an e-mail to Alibaba employees, company CEO<br />

Jack Ma said <strong>the</strong> company is making <strong>the</strong> move<br />

as e-commerce has faced “disruptive changes,”<br />

pointing to social trends and <strong>the</strong> entrance of new<br />

companies in <strong>the</strong> market. He stated that “significant<br />

change has taken place in customer demand … we<br />

need to offer c<strong>on</strong>sumers more sophisticated and<br />

customized services.”<br />

Online Can Change <strong>the</strong> Rules of <strong>the</strong> Game<br />

Traditi<strong>on</strong>al marketing models d<strong>on</strong>’t necessarily<br />

apply in <strong>on</strong>line retail. An example of this is <strong>the</strong><br />

diapers category in China, where Procter & Gamble<br />

dominates <strong>the</strong> offline market with its Pampers<br />

brand. P&G has gained its positi<strong>on</strong> through heavy<br />

marketing expenditure al<strong>on</strong>gside str<strong>on</strong>g in-store<br />

presence and promoti<strong>on</strong>. Yet for certain <strong>on</strong>line<br />

retailers, <strong>the</strong> Mamy Poko brand challenges <strong>the</strong><br />

dominance of Pampers. This is due to two reas<strong>on</strong>s.<br />

First, Mamy Poko’s lower price point appeals to<br />

value-seeking <strong>on</strong>line shoppers. <str<strong>on</strong>g>Sec<strong>on</strong>d</str<strong>on</strong>g>, Mamy<br />

Poko receives <strong>on</strong>line c<strong>on</strong>sumer reviews and ratings<br />

that are equal to or better than Pampers’ ratings<br />

(Figure 3). C<strong>on</strong>sumer recommendati<strong>on</strong>s go a l<strong>on</strong>g<br />

way to helping sell <strong>the</strong> brand.<br />

Breakthrough Insights 17

18 Breakthrough Insights<br />

Figure 3: Diaper Wars <strong>on</strong> Amaz<strong>on</strong><br />

What Are <strong>the</strong> Prospects for Online <strong>Retail</strong> in<br />

China?<br />

Online retail is set to c<strong>on</strong>tinue its exp<strong>on</strong>ential<br />

growth in China with little in <strong>the</strong> way to stop it.<br />

The potential introducti<strong>on</strong> of taxes and <strong>the</strong> lack<br />

of infrastructure in some parts of <strong>the</strong> country<br />

may inhibit <strong>the</strong> speed of growth. However, <strong>the</strong>se<br />

potential changes pale in comparis<strong>on</strong> to some<br />

factors driving growth such as:<br />

High Internet usage and rapidly expanding<br />

broadband network<br />

High mobile ph<strong>on</strong>e penetrati<strong>on</strong>—it is estimated<br />

that 300 milli<strong>on</strong> c<strong>on</strong>sumers go <strong>on</strong>line via <strong>the</strong>ir<br />

ph<strong>on</strong>es in China<br />

Source: Amaz<strong>on</strong>.com<br />

Growing c<strong>on</strong>sumer desire for c<strong>on</strong>venience and<br />

value<br />

Poor access to offline retail stores in rural<br />

areas<br />

Rapidly improving nati<strong>on</strong>al infrastructure<br />

Improving <strong>on</strong>line payment systems<br />

These factors will ensure that <strong>on</strong>line retail will<br />

enjoy a str<strong>on</strong>g and enduring growth trajectory.<br />

Supplier Implicati<strong>on</strong>s<br />

All suppliers need to form a point of view <strong>on</strong> how<br />

<strong>the</strong>ir category fits with China’s <strong>on</strong>line retail market.<br />

This will help frame up <strong>the</strong> potential opportunity of

doing business <strong>on</strong>line. This can be d<strong>on</strong>e in three<br />

steps.<br />

First, suppliers need to c<strong>on</strong>sider which products<br />

are best suited to <strong>the</strong> servicing <strong>the</strong> needs of <strong>on</strong>line<br />

shoppers. Within pers<strong>on</strong>al care, for example,<br />

shoppers are seeking more premium products<br />

at a value price. Also, shoppers will look to take<br />

advantage of <strong>the</strong> c<strong>on</strong>venience of delivery and<br />

purchase larger pack size which is particularly<br />

important for drink and baby categories.<br />

<str<strong>on</strong>g>Sec<strong>on</strong>d</str<strong>on</strong>g>, suppliers need a plan to develop <strong>the</strong>ir<br />

business in this fast-growing and unfamiliar<br />

channel. Without <strong>on</strong>e, <strong>the</strong>y risk getting left behind<br />

or missing <strong>the</strong> opportunity to c<strong>on</strong>vert offline brand<br />

share to <strong>on</strong>line brand share. Developing a plan<br />

means figuring out “where to play” and “how to win”<br />

in <strong>the</strong> <strong>on</strong>line retail market.<br />

Third, companies need to learn before moving<br />

ahead in <strong>on</strong>line brand promoti<strong>on</strong>. In many ways<br />

<strong>on</strong>line brand promoti<strong>on</strong> is unchartered territory.<br />

Most suppliers have mastered <strong>the</strong> art of brand<br />

promoti<strong>on</strong> via key customers using <strong>the</strong> annual joint<br />

business planning process. However, most <strong>on</strong>line<br />

retailers do not even c<strong>on</strong>duct annual planning.<br />

<strong>Kantar</strong> <strong>Retail</strong> Point of View<br />

A Checklist for Suppliers<br />

Prepare a strategy for <strong>on</strong>line retail<br />

Identify which sectors of <strong>on</strong>line retail you want to focus <strong>on</strong><br />

Get to know <strong>the</strong> B2C retailers early<br />

The business is much more sp<strong>on</strong>taneous and fast<br />

moving. As a result, no manufacturer has built an<br />

instituti<strong>on</strong>al understanding of how to drive business<br />

with <strong>on</strong>line retailers. Manufacturers struggle to<br />

build visibility and meet <strong>the</strong> dissimilar needs of<br />

<strong>on</strong>line retailers.<br />

This third activity is critical. Online retailers<br />

operate differently from offline retailers and have<br />

different requirements from suppliers. A good pack<br />

shot and product descripti<strong>on</strong> can be <strong>the</strong> difference<br />

between success and failure. Yet many suppliers<br />

fail to provide adequate support to <strong>on</strong>line retailers.<br />

By <strong>the</strong> same token, some <strong>on</strong>line retailers, such<br />

as Amaz<strong>on</strong>, offer a nati<strong>on</strong>al distributi<strong>on</strong> service<br />