Formelsammlung: Methoden der empirischen Wirtschaftsforschung

Formelsammlung: Methoden der empirischen Wirtschaftsforschung

Formelsammlung: Methoden der empirischen Wirtschaftsforschung

Erfolgreiche ePaper selbst erstellen

Machen Sie aus Ihren PDF Publikationen ein blätterbares Flipbook mit unserer einzigartigen Google optimierten e-Paper Software.

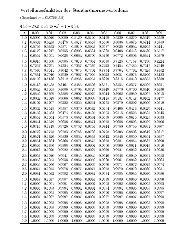

Dynamische RegressionsgleichungDynamische Modelley t =T ∗∑τ=0Bayessches Informationskriterium nach Schwarzb τ x t−τ + u t (84)SC = ln ˆσ 2 ML,T ∗ + T ∗ ln TTAutoregressiver Prozess p-ter Ordnung(85)y t = θ 0 +p∑τ=1Autoregressiver Prozess erster OrdnungAutokorrelationsfunktionE(y) = θ 01 − θ 1; V (y) = σ21 − θ 2 1ρ τ = Cov(y t, y t−τ )V (y)Folge <strong>der</strong> partiellen Autokorrelationskoezientenθ τ y t−τ + u t (86)(87)= θ τ 1 τ = 1, 2, . . . (88)y t = θ 1 0 + θ 1 1y t−1 + u 1y t = θ 2 0 + θ 2 1y t−1 + θ 2 2y t−2 + u 2.y t = θ p 0 + θ p 1y t−1 + θ p 2y t−2 + . . . + θ p py t−p + u pTest auf AutokorrelationskoezientenT k =ˆθ kk √ 1T(89)Partielle Anpassungy t − y t−1 = y ∗ t − y t−1 (90)y t − y t−τ = γ(y ∗ t − y t−1 ) 0 < γ < 1 (91)y ∗ t = a + bx t + u t (92)11